Are you looking to understand How To Calculate Cost Of Sales For Income Statement to boost your business’s profitability and explore strategic partnerships? Calculating your cost of sales is crucial for assessing financial health and identifying areas for improvement. At income-partners.net, we help businesses like yours master these calculations and find the right partners to drive growth. This understanding is vital for business growth, profit margin analysis, and making sound financial decisions.

1. What Does Cost Of Sales Mean?

Cost of sales, also known as the cost of goods sold (COGS), represents the direct expenses related to producing and selling goods or services. This includes the cost of materials, direct labor, and any other costs directly tied to production.

To gain more clarity on this, let’s consider some vital components and the comprehensive formula for determining your cost of sales.

1.1. Key Components of Cost of Sales

Understanding the components that make up the cost of sales is essential for accurate calculation:

- Beginning Inventory: This is the value of inventory at the start of an accounting period.

- Additional Inventory: This includes all inventory purchased or produced during the period.

- Ending Inventory: This is the value of unsold inventory remaining at the end of the accounting period.

1.2. The Cost of Sales Formula

The basic formula for calculating the cost of sales is:

Cost of Sales = (Beginning Inventory + Additional Inventory) – Ending Inventory

Let’s break it down with an example. Imagine “Green Gadgets,” a company selling eco-friendly tech accessories:

- Beginning Inventory: $10,000

- Additional Inventory Purchased: $50,000

- Ending Inventory: $15,000

Using the formula:

- Cost of Sales = ($10,000 + $50,000) – $15,000 = $45,000

This calculation shows Green Gadgets spent $45,000 to sell their products during the period.

2. Why is Calculating Cost of Sales Important?

Calculating cost of sales is not merely an accounting exercise; it is a critical tool that provides insights into a company’s profitability and efficiency. Understanding this metric enables businesses to make informed decisions, optimize operations, and enhance financial performance.

2.1. Understanding Profitability

The cost of sales directly impacts a company’s gross profit, which is calculated as total revenue less the cost of sales. According to a study by Harvard Business Review, companies that closely monitor and manage their cost of sales tend to have higher gross profit margins, leading to increased overall profitability.

2.2. Inventory Management

Calculating the cost of sales helps in better inventory management. By understanding how quickly inventory is sold, businesses can optimize their purchasing and production schedules, reducing waste and storage costs.

2.3. Pricing Strategies

Knowing the cost of sales is essential for setting competitive and profitable prices. Businesses must understand their costs to ensure that their pricing strategies cover expenses and generate a reasonable profit margin.

2.4. Financial Reporting

The cost of sales is a key component of the income statement, which is a fundamental financial report. Accurate calculation and reporting of the cost of sales are necessary for compliance with accounting standards and for providing stakeholders with a clear picture of the company’s financial performance.

2.5. Performance Benchmarking

Calculating and tracking the cost of sales over time allows businesses to benchmark their performance against industry standards and competitors. This comparison can highlight areas where the company excels or needs improvement.

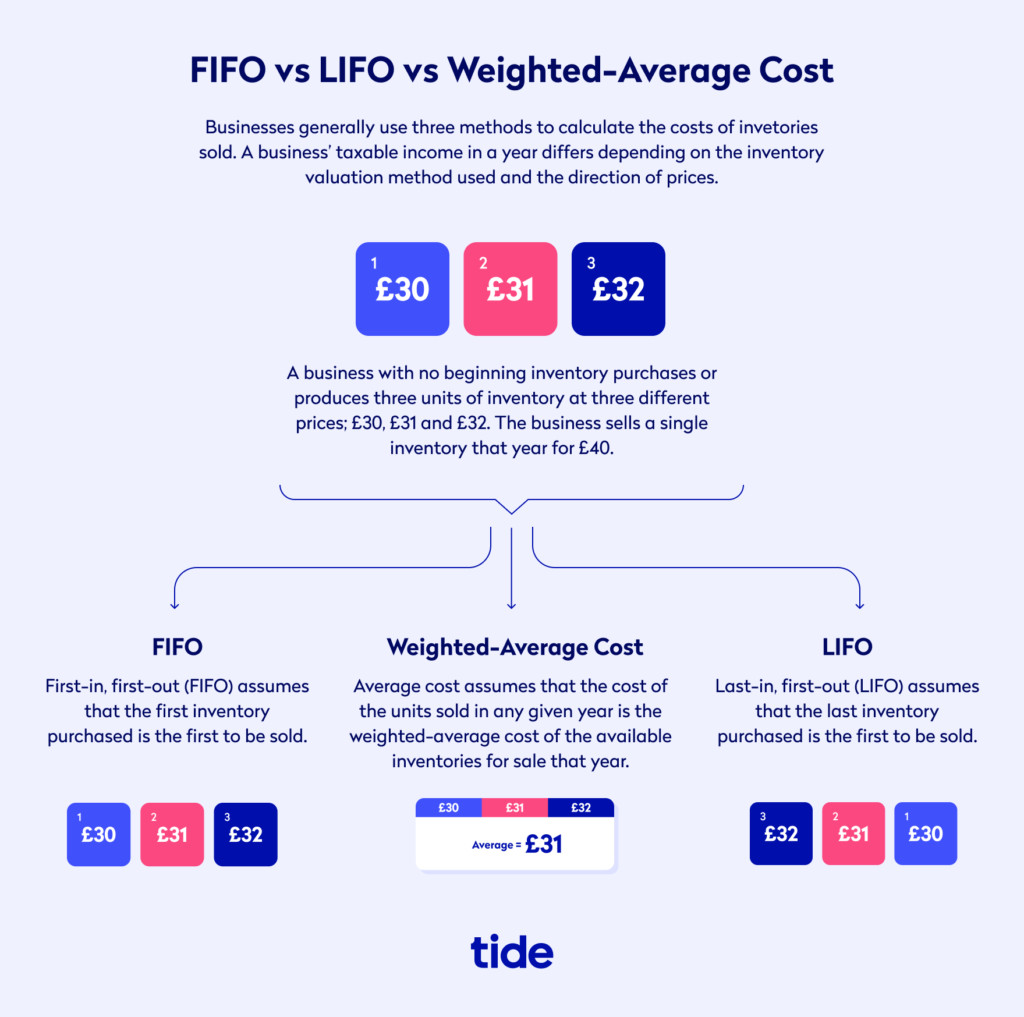

3. Inventory Cost Methods: FIFO, LIFO, and Weighted Average

When calculating the cost of sales, the inventory cost method you choose can significantly impact your financial statements. The three main methods are FIFO (First-In, First-Out), LIFO (Last-In, First-Out), and the weighted average cost method. Let’s explore each method with examples to illustrate their effects.

3.1. FIFO (First-In, First-Out)

FIFO assumes that the first units purchased are the first ones sold. This method is widely used because it often aligns with the actual flow of inventory, especially for perishable goods or items with a short shelf life.

Example:

“Fresh Flowers Inc.” purchased the following roses:

- January 1: 100 roses at $1 each = $100

- February 1: 150 roses at $1.20 each = $180

In March, they sold 200 roses. Under FIFO, the cost of sales is calculated as:

- 100 roses from January at $1 = $100

- 100 roses from February at $1.20 = $120

- Total Cost of Sales = $100 + $120 = $220

Impact: FIFO typically results in a higher net income during periods of rising prices because the cost of sales reflects older, lower prices.

3.2. LIFO (Last-In, First-Out)

LIFO assumes that the last units purchased are the first ones sold. While LIFO can provide tax advantages during inflationary periods, it is not permitted under IFRS (International Financial Reporting Standards) and is less commonly used.

Example:

Using the same data for “Fresh Flowers Inc.”:

- January 1: 100 roses at $1 each = $100

- February 1: 150 roses at $1.20 each = $180

In March, they sold 200 roses. Under LIFO, the cost of sales is calculated as:

- 150 roses from February at $1.20 = $180

- 50 roses from January at $1 = $50

- Total Cost of Sales = $180 + $50 = $230

Impact: LIFO can result in a lower net income during periods of rising prices because the cost of sales reflects the more recent, higher prices.

3.3. Weighted Average Cost Method

The weighted average cost method calculates the average cost of all units available for sale during a period and uses that average to determine the cost of sales.

Example:

Using the same data for “Fresh Flowers Inc.”:

- January 1: 100 roses at $1 each = $100

- February 1: 150 roses at $1.20 each = $180

- Total Cost = $100 + $180 = $280

- Total Units = 100 + 150 = 250 roses

- Weighted Average Cost = Total Cost / Total Units = $280 / 250 = $1.12 per rose

In March, they sold 200 roses. The cost of sales is calculated as:

- 200 roses at $1.12 each = $224

Impact: The weighted average cost method smooths out price fluctuations, providing a cost of sales figure that falls between FIFO and LIFO.

3.4. Comparative Analysis

Here’s a table summarizing the cost of sales under each method for “Fresh Flowers Inc.”:

| Method | Cost of Sales |

|---|---|

| FIFO | $220 |

| LIFO | $230 |

| Weighted Average | $224 |

As you can see, the choice of inventory cost method can significantly impact the reported cost of sales and, consequently, the net income. Businesses should carefully consider which method best reflects their inventory flow and financial strategy.

4. What is Included and Excluded in the Cost of Sales?

To accurately calculate your cost of sales, it’s essential to know what to include and exclude. Generally Accepted Accounting Principles (GAAP) provide guidelines on what constitutes the cost of sales, focusing on the direct costs associated with producing goods or services. However, certain expenses are classified differently.

4.1. What to Include in the Cost of Sales

- Direct Materials: These are the raw materials and components that directly go into producing the final product.

- Direct Labor: This includes the wages and benefits of workers directly involved in the manufacturing process.

- Manufacturing Overhead: These are the indirect costs associated with production, such as factory rent, utilities, and depreciation of manufacturing equipment.

- Freight In: This includes the transportation costs of bringing raw materials to your production facility.

- Purchase Discounts: Reductions in the purchase price offered by suppliers for prompt payment or bulk orders.

Example:

Consider “TechGadgets Inc.,” a manufacturer of electronic devices. The following costs would be included in the cost of sales:

- Cost of microchips and circuit boards

- Wages of assembly line workers

- Factory rent and utilities

- Depreciation of manufacturing machinery

- Shipping costs for receiving components

4.2. What to Exclude from the Cost of Sales

- Operating Expenses: These are the costs associated with running your business but not directly related to production.

- Marketing and Advertising Expenses: These costs are incurred to promote and sell your products or services.

- Administrative Expenses: These include costs related to managing the business, such as executive salaries, office rent, and administrative staff wages.

- Selling Expenses: These costs are incurred to sell and distribute your products, such as sales commissions and outbound shipping.

- Interest Expense: This is the cost of borrowing money.

Example:

For TechGadgets Inc., the following expenses would be excluded from the cost of sales and classified as operating expenses:

- Salaries of marketing staff

- Advertising campaign costs

- Office rent and utilities

- Salaries of administrative staff

- Sales commissions

- Interest on loans

4.3. Cost of Revenue vs. Cost of Sales

It’s important to distinguish between the cost of revenue and the cost of sales. The cost of revenue is a broader term that includes all expenses incurred to deliver a product or service. It extends beyond the direct manufacturing costs covered by the cost of sales to include marketing and distribution expenses.

Example:

Consider “ServiceSolutions LLC,” a consulting firm. The cost of revenue would include:

- Salaries of consultants

- Travel expenses for client meetings

- Software and tools used to deliver consulting services

- Marketing expenses to attract new clients

- Cost of Sales would be only the direct cost

4.4. Impact of Exclusions on Financial Statements

Excluding certain expenses from the cost of sales can significantly impact a company’s financial statements:

- Gross Profit: By excluding operating expenses from the cost of sales, a company can present a higher gross profit, which may appeal to investors.

- Net Income: However, these expenses will still be reflected in the operating expenses section of the income statement, reducing the net income.

- Financial Ratios: Financial ratios such as the gross profit margin and operating profit margin will be affected by how expenses are classified.

Understanding what to include and exclude in the cost of sales is essential for accurate financial reporting and analysis. Businesses should follow GAAP guidelines and carefully consider the nature of each expense to ensure proper classification.

5. Cost of Sales for Service-Based Businesses

Service-based businesses, unlike product-based companies, do not have physical inventory. As such, the cost of sales for these businesses includes direct costs related to providing their services. Understanding how to calculate the cost of sales for service-based businesses is essential for accurate financial reporting and profitability analysis.

5.1. Identifying Direct Costs

The first step in calculating the cost of sales for a service-based business is to identify the direct costs associated with delivering the service. These costs typically include:

- Direct Labor: This includes wages, salaries, and benefits for employees directly involved in providing the service.

- Materials and Supplies: These are the costs of any materials or supplies directly used in providing the service.

- Subcontractor Costs: If a service-based business hires subcontractors to perform part of the service, the costs paid to those subcontractors are included.

- Travel Expenses: These are the costs of transportation, lodging, and meals incurred while providing services at a client’s location.

- Software and Tools: The costs of software, tools, and equipment directly used in providing the service.

Example:

Consider “ConsultingSolutions Inc.,” a management consulting firm. The direct costs of providing consulting services include:

- Salaries of consultants

- Travel expenses for client meetings

- Software licenses for analytical tools

- Fees paid to expert advisors

5.2. Cost of Sales Formula for Service-Based Businesses

The formula for calculating the cost of sales for service-based businesses is:

Cost of Sales = Direct Labor + Materials and Supplies + Subcontractor Costs + Travel Expenses + Software and Tools

Example:

Using the data for ConsultingSolutions Inc.:

- Direct Labor (Salaries of consultants): $500,000

- Travel Expenses: $50,000

- Software Licenses: $20,000

- Subcontractor Costs: $30,000

Cost of Sales = $500,000 + $50,000 + $20,000 + $30,000 = $600,000

5.3. Differentiating from Operating Expenses

It is crucial to differentiate between the cost of sales and operating expenses in service-based businesses. Operating expenses are costs not directly related to providing the service, such as administrative salaries, rent, utilities, and marketing expenses.

Example:

For ConsultingSolutions Inc., operating expenses include:

- Salaries of administrative staff

- Office rent and utilities

- Marketing and advertising expenses

- Depreciation of office equipment

These operating expenses are reported separately on the income statement and are not included in the cost of sales.

5.4. Impact on Financial Statements

Calculating the cost of sales accurately is essential for determining the gross profit of service-based businesses. Gross profit is calculated as total revenue less the cost of sales. A higher gross profit indicates that the business is efficiently delivering its services and managing its direct costs.

Example:

If ConsultingSolutions Inc. generated total revenue of $1,000,000, the gross profit would be:

Gross Profit = Total Revenue – Cost of Sales

$1,000,000 – $600,000 = $400,000

The gross profit margin, calculated as (Gross Profit / Total Revenue) x 100, provides further insight into the profitability of the business.

In conclusion, calculating the cost of sales for service-based businesses involves identifying and summing the direct costs associated with delivering the service.

6. How Cost of Sales Impacts the Income Statement

The cost of sales plays a pivotal role in shaping the income statement, providing key insights into a company’s profitability and operational efficiency. The income statement, also known as the profit and loss (P&L) statement, summarizes a company’s financial performance over a specific period. Understanding how the cost of sales affects this statement is crucial for financial analysis and decision-making.

6.1. Structure of the Income Statement

To understand the impact of the cost of sales, let’s first outline the basic structure of the income statement:

- Revenue (Sales): The total amount of money earned from selling goods or services.

- Cost of Sales (COGS): The direct costs associated with producing and selling those goods or services.

- Gross Profit: Calculated as Revenue – Cost of Sales.

- Operating Expenses: Costs incurred in running the business, such as administrative, marketing, and research expenses.

- Operating Income: Calculated as Gross Profit – Operating Expenses.

- Interest and Taxes: Expenses related to interest on debt and income taxes.

- Net Income: The final profit after deducting all expenses, interest, and taxes.

6.2. Direct Impact on Gross Profit

The cost of sales has a direct and significant impact on a company’s gross profit. By deducting the cost of sales from revenue, the gross profit indicates how efficiently a company is managing its production costs.

Example:

Consider “FashionForward Inc.,” a clothing retailer.

- Revenue: $2,000,000

- Cost of Sales: $800,000

Gross Profit = Revenue – Cost of Sales

$2,000,000 – $800,000 = $1,200,000

The gross profit of $1,200,000 indicates the profit FashionForward Inc. earned from its sales after accounting for the direct costs of the goods sold.

6.3. Impact on Profit Margins

The cost of sales also affects key profitability metrics such as the gross profit margin. The gross profit margin is calculated as (Gross Profit / Revenue) x 100, and it measures the percentage of revenue remaining after accounting for the cost of sales.

Example:

Using the data for FashionForward Inc.:

Gross Profit Margin = (Gross Profit / Revenue) x 100

($1,200,000 / $2,000,000) x 100 = 60%

A gross profit margin of 60% means that FashionForward Inc. retains 60 cents of every dollar of revenue after covering the cost of sales.

6.4. Influencing Net Income

While the cost of sales directly affects gross profit, it indirectly influences net income by impacting the funds available to cover operating expenses, interest, and taxes. Efficiently managing the cost of sales can lead to a higher gross profit, providing more resources to cover these other expenses and ultimately increase net income.

Example:

Continuing with FashionForward Inc.:

- Gross Profit: $1,200,000

- Operating Expenses: $500,000

- Operating Income: $700,000

- Interest and Taxes: $200,000

- Net Income: $500,000

If FashionForward Inc. could reduce its cost of sales by $100,000, the gross profit would increase to $1,300,000, and the net income would rise to $600,000, assuming all other factors remain constant.

6.5. Implications for Financial Analysis

The cost of sales is a critical component in financial analysis, providing insights into a company’s operational efficiency and profitability. Investors and analysts use the cost of sales to assess:

- Cost Management: The ability of a company to control its production costs.

- Pricing Strategy: Whether a company’s pricing strategy is effectively covering its costs.

- Industry Comparisons: How a company’s cost of sales compares to industry peers.

7. Key Ratios Using Cost of Sales

The cost of sales is a vital component in several financial ratios that help assess a company’s profitability, efficiency, and overall financial health. These ratios provide insights into how well a company manages its production and sales processes.

7.1. Gross Profit Margin

The gross profit margin, as discussed earlier, is a key profitability ratio that measures the percentage of revenue remaining after accounting for the cost of sales.

Formula:

Gross Profit Margin = (Gross Profit / Revenue) x 100

Interpretation:

A higher gross profit margin indicates that a company is efficiently managing its production costs and has a strong pricing strategy.

Example:

Consider “Electronics Emporium,” an electronics retailer with:

- Revenue: $1,500,000

- Cost of Sales: $900,000

- Gross Profit: $600,000

Gross Profit Margin = ($600,000 / $1,500,000) x 100 = 40%

This means Electronics Emporium retains 40 cents of every dollar of revenue after covering the cost of sales.

7.2. Cost of Sales Ratio

The cost of sales ratio measures the percentage of revenue used to cover the direct costs of producing and selling goods or services.

Formula:

Cost of Sales Ratio = (Cost of Sales / Revenue) x 100

Interpretation:

A lower cost of sales ratio indicates that a company is efficiently managing its production costs.

Example:

Using the data for Electronics Emporium:

Cost of Sales Ratio = ($900,000 / $1,500,000) x 100 = 60%

This means 60% of Electronics Emporium’s revenue is used to cover the cost of sales, leaving 40% for other expenses and profit

electronics-cost-sales-ratio.

electronics-cost-sales-ratio.

7.3. Inventory Turnover Ratio

The inventory turnover ratio measures how efficiently a company is managing its inventory by indicating how many times inventory is sold and replaced over a period.

Formula:

Inventory Turnover Ratio = Cost of Sales / Average Inventory

Interpretation:

A higher inventory turnover ratio indicates that a company is efficiently managing its inventory and has strong sales.

Example:

Electronics Emporium has:

- Cost of Sales: $900,000

- Beginning Inventory: $200,000

- Ending Inventory: $250,000

- Average Inventory: ($200,000 + $250,000) / 2 = $225,000

Inventory Turnover Ratio = $900,000 / $225,000 = 4

This means Electronics Emporium sells and replaces its inventory four times a year.

7.4. Days Sales of Inventory (DSI)

Days Sales of Inventory (DSI) measures the average number of days it takes for a company to sell its inventory.

Formula:

DSI = (Average Inventory / Cost of Sales) x 365

Interpretation:

A lower DSI indicates that a company is efficiently managing its inventory and has strong sales.

Example:

Using the data for Electronics Emporium:

DSI = ($225,000 / $900,000) x 365 = 91.25 days

This means it takes Electronics Emporium approximately 91 days to sell its inventory.

7.5. Return on Sales (ROS)

Return on Sales (ROS) measures how efficiently a company is generating profit from its revenue.

Formula:

ROS = (Net Income / Revenue) x 100

Interpretation:

A higher ROS indicates that a company is efficiently converting revenue into profit.

Example:

Electronics Emporium has:

- Net Income: $300,000

- Revenue: $1,500,000

ROS = ($300,000 / $1,500,000) x 100 = 20%

This means Electronics Emporium generates 20 cents of profit for every dollar of revenue.

8. Strategies to Reduce the Cost of Sales

Reducing the cost of sales is crucial for improving a company’s profitability and financial health. By implementing effective strategies, businesses can optimize their production processes, manage inventory efficiently, and negotiate better terms with suppliers.

8.1. Streamlining Production Processes

Improving the efficiency of production processes can significantly reduce the cost of sales. This involves identifying and eliminating bottlenecks, reducing waste, and implementing lean manufacturing principles.

- Process Analysis: Conduct a thorough analysis of the production process to identify areas for improvement.

- Automation: Implement automation technologies to reduce labor costs and increase efficiency.

- Waste Reduction: Minimize waste through better inventory management, quality control, and recycling programs.

Example:

Consider “AutoTech Manufacturing,” an automotive parts manufacturer. By implementing automation in its assembly line, AutoTech Manufacturing reduced labor costs by 20% and decreased production time by 15%.

8.2. Efficient Inventory Management

Effective inventory management can reduce storage costs, minimize waste, and prevent stockouts. This involves implementing inventory management techniques such as just-in-time (JIT) inventory and economic order quantity (EOQ).

- Just-In-Time (JIT) Inventory: Receive materials and produce goods only when needed to minimize inventory holding costs.

- Economic Order Quantity (EOQ): Determine the optimal order quantity to minimize total inventory costs, including ordering and holding costs.

- Inventory Tracking: Use inventory management software to track inventory levels, monitor sales trends, and forecast demand.

Example:

“RetailChic,” a fashion retailer, implemented a JIT inventory system to reduce storage costs and minimize the risk of obsolescence. This resulted in a 10% reduction in inventory holding costs and improved cash flow.

8.3. Negotiating Better Supplier Terms

Negotiating favorable terms with suppliers can significantly reduce the cost of materials and supplies. This involves building strong relationships with suppliers, leveraging purchasing power, and exploring alternative sourcing options.

- Volume Discounts: Negotiate discounts for purchasing materials in bulk.

- Early Payment Discounts: Take advantage of discounts offered for paying invoices early.

- Long-Term Contracts: Establish long-term contracts with suppliers to secure favorable pricing and supply availability.

Example:

“FoodCorp,” a food processing company, negotiated volume discounts with its suppliers by committing to long-term contracts. This resulted in a 5% reduction in the cost of raw materials and improved profit margins.

8.4. Reducing Direct Labor Costs

Reducing direct labor costs can significantly lower the cost of sales. This involves improving workforce productivity, providing training and development opportunities, and optimizing staffing levels.

- Productivity Improvements: Implement strategies to improve workforce productivity, such as process optimization and employee incentives.

- Training and Development: Provide training and development opportunities to enhance employee skills and efficiency.

- Staffing Optimization: Optimize staffing levels to match production needs and reduce unnecessary labor costs.

Example:

“ServiceMaster Solutions,” a service-based company, invested in training and development programs to improve employee skills and productivity. This resulted in a 15% reduction in direct labor costs and improved service quality.

8.5. Optimizing Supply Chain Management

Efficient supply chain management can reduce transportation costs, minimize delays, and improve overall efficiency. This involves streamlining logistics, using technology to track shipments, and diversifying sourcing options.

- Logistics Optimization: Streamline logistics operations to reduce transportation costs and delivery times.

- Technology Integration: Use technology to track shipments, monitor inventory levels, and improve communication with suppliers.

- Sourcing Diversification: Diversify sourcing options to reduce reliance on single suppliers and mitigate supply chain risks.

Example:

“GlobalTech Distributors,” a technology distributor, optimized its supply chain management by implementing a tracking system and diversifying its sourcing options. This resulted in a 10% reduction in transportation costs and improved supply chain resilience.

9. Examples of Cost of Sales Calculations

To illustrate how to calculate the cost of sales, let’s consider a few examples across different types of businesses.

9.1. Manufacturing Company

Scenario:

“PrecisionTech,” a manufacturing company, produces electronic components. At the beginning of the year, PrecisionTech had $50,000 worth of raw materials in inventory. During the year, they purchased an additional $200,000 worth of raw materials. At the end of the year, $30,000 worth of raw materials remained in inventory. Direct labor costs were $150,000, and manufacturing overhead costs were $70,000.

Calculation:

- Beginning Inventory: $50,000

- Additional Inventory Purchased: $200,000

- Ending Inventory: $30,000

- Cost of Raw Materials Used: $50,000 + $200,000 – $30,000 = $220,000

- Direct Labor Costs: $150,000

- Manufacturing Overhead Costs: $70,000

- Cost of Sales: $220,000 + $150,000 + $70,000 = $440,000

Interpretation:

The cost of sales for PrecisionTech is $440,000, representing the total direct costs associated with producing electronic components during the year.

9.2. Retail Company

Scenario:

“StyleHub,” a retail company, sells clothing and accessories. At the beginning of the year, StyleHub had $80,000 worth of merchandise inventory. During the year, they purchased an additional $300,000 worth of merchandise. At the end of the year, $60,000 worth of merchandise remained in inventory. Freight-in costs were $10,000.

Calculation:

- Beginning Inventory: $80,000

- Additional Inventory Purchased: $300,000

- Ending Inventory: $60,000

- Freight-In Costs: $10,000

- Cost of Sales: $80,000 + $300,000 – $60,000 + $10,000 = $330,000

Interpretation:

The cost of sales for StyleHub is $330,000, representing the total cost of merchandise sold during the year, including freight-in costs.

9.3. Service-Based Company

Scenario:

“ConsultPro,” a service-based company, provides consulting services. During the year, direct labor costs (salaries of consultants) were $250,000, travel expenses were $20,000, and software costs directly related to client projects were $10,000.

Calculation:

- Direct Labor Costs: $250,000

- Travel Expenses: $20,000

- Software Costs: $10,000

- Cost of Sales: $250,000 + $20,000 + $10,000 = $280,000

Interpretation:

The cost of sales for ConsultPro is $280,000, representing the total direct costs associated with providing consulting services during the year.

9.4. Restaurant

Scenario:

“FlavorPlate,” a restaurant, had $5,000 worth of food inventory at the beginning of the month. During the month, they purchased an additional $15,000 worth of food. At the end of the month, $3,000 worth of food remained in inventory.

Calculation:

- Beginning Inventory: $5,000

- Additional Inventory Purchased: $15,000

- Ending Inventory: $3,000

- Cost of Sales: $5,000 + $15,000 – $3,000 = $17,000

Interpretation:

The cost of sales for FlavorPlate is $17,000, representing the total cost of food sold during the month.

9.5. Software Company

Scenario:

“CodeCrafters,” a software company, provides software development services. Direct labor costs (salaries of developers) were $400,000, software licenses used for projects were $30,000, and cloud computing costs directly related to client projects were $20,000.

Calculation:

- Direct Labor Costs: $400,000

- Software Licenses: $30,000

- Cloud Computing Costs: $20,000

- Cost of Sales: $400,000 + $30,000 + $20,000 = $450,000

Interpretation:

The cost of sales for CodeCrafters is $450,000, representing the total direct costs associated with providing software development services during the year.

10. Latest Trends in Cost of Sales Management

In today’s dynamic business environment, staying ahead of the latest trends in the cost of sales management is essential for maintaining profitability and competitive advantage. Here are some emerging trends that businesses should consider:

10.1. Digital Transformation

Digital transformation is revolutionizing the way businesses manage their cost of sales. By implementing digital technologies, companies can automate processes, improve efficiency, and gain better visibility into their supply chains.

- Cloud Computing: Moving to the cloud can reduce IT infrastructure costs and improve scalability.

- Data Analytics: Using data analytics to identify cost-saving opportunities and optimize pricing strategies.

- E-Commerce: Expanding into e-commerce can reduce overhead costs and reach a broader customer base.

Example:

“TechForward Solutions,” a technology company, implemented cloud-based solutions for its operations and used data analytics to optimize its pricing strategies. This resulted in a 15% reduction in overhead costs and a 10% increase in revenue.

10.2. Sustainability and Ethical Sourcing

Consumers are increasingly demanding sustainable and ethically sourced products, which is impacting the cost of sales management. Businesses must consider the environmental and social impact of their sourcing decisions and invest in sustainable practices.

- Sustainable Sourcing: Prioritizing suppliers with sustainable practices and certifications.

- Ethical Labor Practices: Ensuring fair labor practices throughout the supply chain.

- Environmental Impact Reduction: Implementing measures to reduce waste, emissions, and energy consumption.

Example:

“EcoStyle Apparel,” a sustainable fashion brand, prioritized suppliers with ethical labor practices and sustainable materials. This not only appealed to environmentally conscious consumers but also reduced long-term costs associated with waste and environmental impact.

10.3. Supply Chain Resilience

Recent global events have highlighted the importance of supply chain resilience. Businesses must diversify their sourcing options, build stronger relationships with suppliers, and implement risk management strategies to mitigate disruptions.

- Diversification of Suppliers: Reduce reliance on single suppliers by diversifying sourcing options.

- Stronger Supplier Relationships: Build strong, collaborative relationships with key suppliers.

- Risk Management: Implement risk management strategies to identify and mitigate potential supply chain disruptions.

Example:

“GlobalTech Electronics,” a global electronics distributor, diversified its sourcing options and built stronger relationships with key suppliers to mitigate supply chain disruptions. This ensured business continuity and reduced the impact of disruptions on the cost of sales.

10.4. Automation and AI

Automation and artificial intelligence (AI) are transforming various aspects of the cost of sales management, from inventory management to customer service.

- Automated Inventory Management: Using AI-powered inventory management systems to optimize inventory levels and reduce stockouts.

- AI-Powered Customer Service: Implementing AI-powered chatbots to improve customer service and reduce labor costs.

- Robotic Process Automation (RPA): Automating repetitive tasks to improve efficiency and reduce errors.

Example:

“RetailAI Solutions,” a retail company, implemented AI-powered inventory management and customer service solutions. This resulted in a 20% reduction in inventory costs and a 15% improvement in customer satisfaction.

10.5. Focus on Customer Experience

In today’s competitive market, customer experience is a key differentiator. Businesses are focusing on improving the customer experience to drive sales and reduce customer acquisition costs.

- Personalization: Personalizing the customer experience to improve engagement and loyalty.

- Omnichannel Strategy: Providing a seamless customer experience across all channels, including online, in-store, and mobile.

- Customer Feedback: Actively seeking and responding to customer feedback to improve products and services.

Example:

“ServiceFirst Solutions,” a service-based company, implemented a personalized customer experience strategy and actively sought customer feedback to improve its services. This resulted in a 25% increase in customer retention and a 20% reduction in customer acquisition costs.

By staying informed about these latest trends and adapting their cost of sales management strategies accordingly, businesses can enhance their profitability, improve efficiency, and gain a competitive advantage in the market.

Visit income-partners.net today to explore how strategic partnerships can further optimize your cost of sales and boost your bottom line. Discover the power of collaboration and take your business to new heights. Our Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.

FAQ: Calculating Cost of Sales

-

What is the cost of sales (COGS)?

The cost of sales, also known as the cost of goods sold (COGS), includes the direct costs associated with producing and selling goods or services.

-

Why is calculating the cost of sales important?

Calculating the cost of sales is important for determining gross profit, managing inventory, setting prices, and making informed business decisions.

-

What is included in the cost of sales?

The cost of sales typically includes direct materials, direct labor, and manufacturing overhead.

-

What is excluded from the cost of sales?

Operating expenses, marketing expenses, and administrative expenses are typically excluded from the cost of sales.

-

How do I calculate the cost of sales?

The cost of sales is calculated using the formula: Cost of Sales = (Beginning Inventory + Purchases) – Ending Inventory.

-

What is the difference between FIFO and LIFO inventory methods?

FIFO (First-In, First-Out) assumes that the first units purchased are the first ones sold, while LIFO (Last-In, First-Out) assumes that the last units purchased are the first ones sold.

-

How does the inventory method affect the cost of sales?

The inventory method can significantly impact the cost of sales and net income, especially during periods of rising or falling prices.

-

What is the cost of revenue?

Cost of revenue is a broader term that includes all expenses incurred to deliver a product or service, including the cost of sales.

-

How can I reduce the cost of sales?

Strategies to reduce the cost of sales include streamlining production processes, improving inventory management, and negotiating better supplier terms.

-

What is the gross profit margin?

The gross profit margin is calculated as (Gross Profit / Revenue) x 100 and measures the percentage of revenue remaining after accounting for the cost of sales.