Calculating cash basis net income is crucial for understanding your business’s profitability; let income-partners.net guide you through the process. By partnering with us, you’ll gain access to strategies that can boost your financial success. Explore valuable resources and partner with confidence, unlocking ways to achieve your financial goals and secure your business’s future in the USA, especially in thriving hubs like Austin, TX.

1. What is Cash Basis Net Income and Why Does It Matter?

Cash basis net income is the difference between the cash inflows and cash outflows of a business over a specific period. It matters because it provides a simple, real-time view of your business’s financial health.

Cash basis net income is a straightforward accounting method where revenue is recognized when cash is received and expenses are recognized when cash is paid out. This method contrasts with accrual accounting, which recognizes revenue when earned and expenses when incurred, regardless of when the cash changes hands. Understanding cash basis net income is crucial for businesses, especially smaller ones, as it offers a clear snapshot of current liquidity and financial health. According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, businesses using cash basis accounting often find it easier to manage their finances due to its simplicity and direct reflection of cash flow.

1.1. Who Benefits Most from Using the Cash Basis Method?

The cash basis method is particularly beneficial for small businesses and startups. These entities often have limited accounting resources and need a simple way to track their finances.

Small businesses and startups benefit most from the cash basis method due to its simplicity and ease of use. This method doesn’t require complex accounting procedures, making it ideal for businesses with limited resources. Cash basis accounting provides an immediate view of available cash, which is crucial for managing day-to-day operations and short-term financial planning. Furthermore, it can simplify tax reporting, as income and expenses are recognized when cash transactions occur, aligning directly with bank statements and minimizing the need for accrual adjustments. This approach is especially useful for businesses that primarily deal in cash or have short operating cycles.

1.2. What Are the Advantages of Tracking Cash Basis Net Income?

Tracking cash basis net income offers several advantages. It provides a clear picture of your current cash flow, simplifies tax reporting, and is easier to understand than accrual accounting.

Tracking cash basis net income provides a straightforward view of a company’s financial standing by focusing solely on cash inflows and outflows. This method offers several key advantages:

- Simplicity: Cash basis accounting is easier to implement and understand compared to accrual accounting, making it ideal for small businesses without extensive accounting expertise.

- Real-Time Cash Flow Insights: It provides an immediate snapshot of available cash, helping businesses manage their short-term liquidity effectively.

- Simplified Tax Reporting: Income and expenses are recognized when cash transactions occur, aligning directly with bank statements and reducing the need for complex adjustments.

- Improved Budgeting: By focusing on actual cash transactions, businesses can create more accurate budgets and financial forecasts.

- Reduced Complexity: It minimizes the need for estimations and accruals, simplifying bookkeeping and reducing the potential for errors.

These advantages make cash basis net income a practical and efficient tool for small businesses to monitor their financial health and make informed decisions.

1.3. Are There Any Disadvantages to Using the Cash Basis Method?

Yes, the cash basis method has limitations. It may not accurately reflect the long-term financial health of a business and can be easily manipulated to defer income or accelerate expenses for tax purposes.

While the cash basis method offers simplicity and immediate insights, it has limitations that can affect a business’s financial accuracy and long-term planning. One significant drawback is its potential to distort the true financial picture by not recognizing revenues and expenses when they are earned or incurred. This can lead to a misrepresentation of profitability, especially for businesses with significant accounts receivable or payable. Additionally, the cash basis method can be easily manipulated to defer income or accelerate expenses, which, while potentially beneficial for short-term tax management, can undermine the integrity of financial reporting. For instance, a business might delay invoicing to push revenue into the next fiscal year or prepay expenses to reduce current taxable income. Furthermore, the cash basis method does not comply with Generally Accepted Accounting Principles (GAAP), which can limit its use for businesses seeking external financing or planning to scale significantly.

Cash Basis Accounting vs Accrual Accounting

Cash Basis Accounting vs Accrual Accounting

2. Key Components for Calculating Cash Basis Net Income

To calculate cash basis net income, you need to identify all cash inflows and outflows. This includes cash received from sales, services, and other sources, as well as cash paid for expenses, such as rent, salaries, and supplies.

Calculating cash basis net income requires a clear understanding of the cash transactions that occur within a business. Here are the key components:

- Cash Inflows:

- Sales Revenue: Cash received from selling goods or services.

- Interest Income: Cash earned from investments or savings accounts.

- Other Income: Any other cash received, such as refunds or rebates.

- Cash Outflows:

- Cost of Goods Sold (COGS): Cash paid for direct costs related to producing goods or services, including raw materials and labor.

- Operating Expenses: Cash spent on day-to-day operations, such as rent, utilities, salaries, and marketing.

- Interest Expense: Cash paid on loans or credit lines.

- Taxes: Cash paid for income taxes and other business taxes.

- Capital Expenditures: Cash spent on purchasing or improving fixed assets, such as equipment and property.

2.1. What Are Cash Inflows?

Cash inflows represent the money coming into your business. This includes revenue from sales, interest income, and any other sources of cash receipts.

Cash inflows refer to all the money coming into a business from various sources. Accurate tracking of these inflows is essential for maintaining a clear understanding of financial health. Here are the primary types of cash inflows:

- Sales Revenue: This is the cash received from the sale of goods or services. It is the most common and significant source of cash inflow for most businesses.

- Interest Income: Cash earned from investments, savings accounts, or loans made by the business.

- Investment Income: Cash received from dividends, capital gains, or other investment returns.

- Loans and Financing: Cash obtained from bank loans, lines of credit, or other financing arrangements.

- Sale of Assets: Cash received from selling assets, such as equipment, property, or investments.

- Refunds and Rebates: Cash received as refunds from suppliers or rebates from manufacturers.

- Grants and Subsidies: Cash received from government grants, subsidies, or other financial assistance programs.

- Rental Income: Cash earned from renting out property or equipment.

- Royalties: Cash received from licensing intellectual property, such as patents or copyrights.

By meticulously tracking these cash inflows, businesses can gain a comprehensive view of their revenue streams and manage their finances more effectively.

2.2. What Are Cash Outflows?

Cash outflows represent the money leaving your business. This includes payments for expenses, such as rent, salaries, and supplies, as well as payments for capital expenditures and debt service.

Cash outflows represent all the money leaving a business, encompassing a wide range of payments necessary for its operation and growth. Accurate tracking of these outflows is crucial for effective financial management. Here are the primary types of cash outflows:

- Cost of Goods Sold (COGS): Cash paid for direct costs related to producing goods or services, including raw materials, labor, and manufacturing overhead.

- Operating Expenses: Cash spent on day-to-day operations, such as rent, utilities, salaries, marketing, and administrative costs.

- Capital Expenditures (CAPEX): Cash invested in purchasing or improving fixed assets, such as equipment, property, and vehicles.

- Debt Payments: Cash paid towards principal and interest on loans, mortgages, and other forms of debt.

- Taxes: Cash paid for income taxes, property taxes, payroll taxes, and other business taxes.

- Inventory Purchases: Cash spent on acquiring inventory for resale or use in production.

- Supplier Payments: Cash paid to suppliers for goods and services purchased on credit.

- Dividends: Cash distributed to shareholders as a return on their investment.

- Insurance Premiums: Cash paid for business insurance policies, such as liability, property, and health insurance.

2.3. How Do You Differentiate Between Cash and Non-Cash Transactions?

Cash transactions involve the actual movement of money, while non-cash transactions do not. For example, a sale on credit is a non-cash transaction until the customer pays, at which point it becomes a cash transaction.

Distinguishing between cash and non-cash transactions is fundamental for accurate financial record-keeping and reporting. Here’s a breakdown of the key differences:

-

Cash Transactions:

- Definition: Cash transactions involve the immediate exchange of money for goods, services, or other assets. The transfer of cash is direct and instantaneous.

- Examples:

- Paying for supplies with cash or a debit card.

- Receiving cash from a customer for a product sold.

- Paying rent with a check.

- Receiving interest income directly into the bank account.

- Impact on Financial Statements:

- Cash transactions directly affect the cash balance on the balance sheet.

- They are immediately recognized on the cash flow statement.

-

Non-Cash Transactions:

- Definition: Non-cash transactions do not involve the immediate exchange of money. Instead, they involve other forms of consideration or accounting adjustments.

- Examples:

- Purchasing supplies on credit (accounts payable).

- Earning revenue that has not yet been collected (accounts receivable).

- Depreciation of assets.

- Amortization of intangible assets.

- Bartering goods or services.

- Impact on Financial Statements:

- Non-cash transactions do not immediately affect the cash balance on the balance sheet.

- They are not recognized on the cash flow statement until cash changes hands.

- They affect other accounts, such as accounts receivable, accounts payable, and accumulated depreciation.

Understanding the difference between these transaction types ensures that financial statements accurately reflect a company’s financial position and performance.

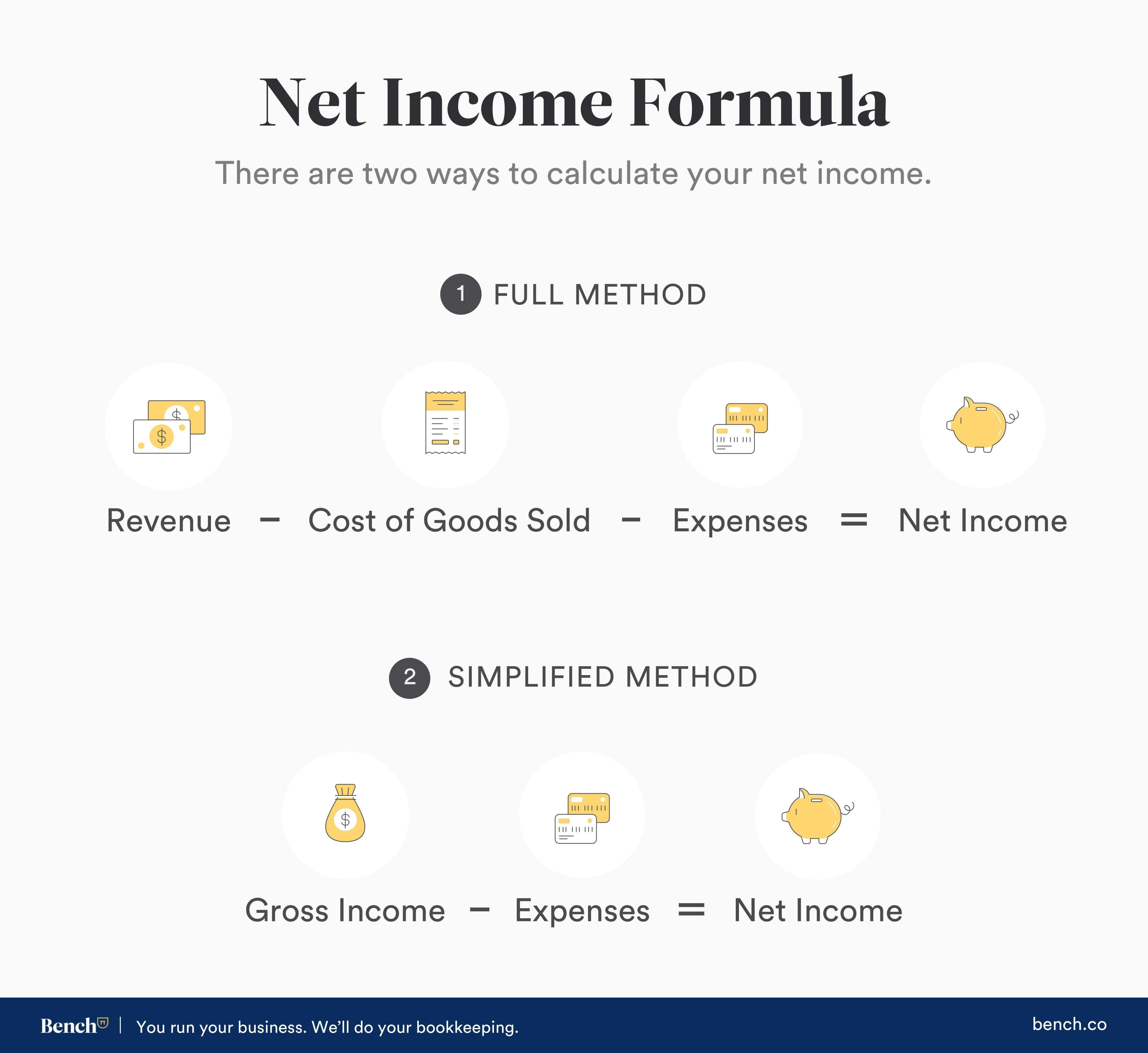

3. Step-by-Step Guide to Calculating Cash Basis Net Income

Calculating cash basis net income involves a few simple steps. First, add up all your cash inflows for the period. Then, add up all your cash outflows. Finally, subtract the total outflows from the total inflows to arrive at your net income.

Calculating cash basis net income involves a straightforward process that provides a clear snapshot of a company’s financial performance based on actual cash transactions. Here’s a step-by-step guide:

Step 1: Identify the Accounting Period

- Determine the specific time frame for which you want to calculate net income. This could be a month, quarter, or year.

Step 2: List All Cash Inflows

- Compile a list of all cash inflows during the accounting period. Common cash inflows include:

- Sales Revenue: Cash received from selling goods or services.

- Interest Income: Cash earned from investments or savings accounts.

- Other Income: Any other cash received, such as refunds or rebates.

Step 3: List All Cash Outflows

- Compile a list of all cash outflows during the accounting period. Common cash outflows include:

- Cost of Goods Sold (COGS): Cash paid for direct costs related to producing goods or services, including raw materials and labor.

- Operating Expenses: Cash spent on day-to-day operations, such as rent, utilities, salaries, and marketing.

- Interest Expense: Cash paid on loans or credit lines.

- Taxes: Cash paid for income taxes and other business taxes.

- Capital Expenditures: Cash spent on purchasing or improving fixed assets, such as equipment and property.

Step 4: Calculate Total Cash Inflows

- Add up all the cash inflows listed in Step 2 to determine the total cash inflows for the period.

Step 5: Calculate Total Cash Outflows

- Add up all the cash outflows listed in Step 3 to determine the total cash outflows for the period.

Step 6: Calculate Net Income

- Subtract the total cash outflows (Step 5) from the total cash inflows (Step 4) to calculate the cash basis net income.

- Formula: Net Income = Total Cash Inflows – Total Cash Outflows

Step 7: Interpret the Result

- If the result is positive, the business has a net income, indicating that it received more cash than it spent during the period.

- If the result is negative, the business has a net loss, indicating that it spent more cash than it received during the period.

3.1. How Do You Account for Sales Revenue?

Under the cash basis method, you only recognize sales revenue when you receive cash from customers. It doesn’t matter when you made the sale; what matters is when the money hits your bank account.

Under the cash basis method, accounting for sales revenue is straightforward: you recognize revenue only when you receive cash from customers. This means that the timing of the cash receipt is the determining factor, regardless of when the sale was made or when the goods or services were provided. Here’s how to account for sales revenue under the cash basis method:

-

Record Revenue When Cash is Received:

- When a customer pays for a product or service, record the revenue at that time.

- For example, if you sell a product in June but receive payment in July, you record the revenue in July.

-

Ignore Accounts Receivable:

- Do not record accounts receivable (money owed to you by customers) as revenue until the cash is actually received.

- If a customer owes you money, it is not considered revenue until they pay.

-

Track Cash Receipts:

- Maintain accurate records of all cash receipts, including dates, amounts, and sources.

- This can be done using accounting software, spreadsheets, or manual ledgers.

-

Example Scenario:

- Suppose a business provides a service in March but does not receive payment until April. Under the cash basis method, the revenue is recorded in April when the cash is received, not in March when the service was provided.

3.2. How Do You Account for Expenses?

Similarly, you only recognize expenses when you pay cash. It doesn’t matter when you incurred the expense; what matters is when you actually paid the bill.

Accounting for expenses under the cash basis method is a straightforward process focused on when cash is actually disbursed. Here’s how to account for expenses:

-

Record Expenses When Cash is Paid:

- Record expenses only when cash is paid out. This means that the timing of the payment is the determining factor, regardless of when the expense was incurred.

- For example, if you receive a utility bill in June but pay it in July, you record the expense in July.

-

Ignore Accounts Payable:

- Do not record accounts payable (money you owe to suppliers or vendors) as expenses until the cash is actually paid.

- If you owe money to a supplier, it is not considered an expense until you pay them.

-

Track Cash Disbursements:

- Maintain accurate records of all cash disbursements, including dates, amounts, and purposes.

- This can be done using accounting software, spreadsheets, or manual ledgers.

-

Example Scenario:

- Suppose a business receives a rent bill in March but does not pay it until April. Under the cash basis method, the rent expense is recorded in April when the cash is paid, not in March when the bill was received.

3.3. What About Depreciation and Amortization?

Depreciation and amortization are non-cash expenses, so they are not included in the calculation of cash basis net income.

Depreciation and amortization are non-cash expenses that are not included in the calculation of cash basis net income. Here’s why:

-

Depreciation:

- Definition: Depreciation is the systematic allocation of the cost of a tangible asset (such as equipment, buildings, or vehicles) over its useful life. It reflects the gradual decline in the asset’s value due to wear and tear, obsolescence, or other factors.

- Non-Cash Nature: Depreciation does not involve an actual cash outflow. Instead, it is an accounting adjustment that reduces the book value of the asset over time.

- Exclusion from Cash Basis: Under the cash basis method, depreciation is not recognized because it does not represent a cash transaction. The full cost of the asset is typically expensed when it is purchased, assuming it is paid for in cash.

-

Amortization:

- Definition: Amortization is the systematic allocation of the cost of an intangible asset (such as patents, copyrights, or goodwill) over its useful life. It is similar to depreciation but applies to intangible assets.

- Non-Cash Nature: Amortization, like depreciation, does not involve a cash outflow. It is an accounting adjustment that reduces the book value of the intangible asset over time.

- Exclusion from Cash Basis: Under the cash basis method, amortization is not recognized because it does not represent a cash transaction.

4. Examples of Calculating Cash Basis Net Income

Let’s look at a couple of examples to illustrate How To Calculate Cash Basis Net Income.

To illustrate how to calculate cash basis net income, let’s examine a couple of practical examples:

4.1. Example 1: Service-Based Business

-

Scenario:

- A freelance graphic designer, Sarah, uses the cash basis method for her accounting. In July, she receives $5,000 in payments from clients for services rendered. She also pays $500 for software subscriptions, $300 for marketing expenses, and $200 for office supplies.

-

Calculation:

- Cash Inflows:

- Client Payments: $5,000

- Cash Outflows:

- Software Subscriptions: $500

- Marketing Expenses: $300

- Office Supplies: $200

- Total Cash Inflows: $5,000

- Total Cash Outflows: $500 + $300 + $200 = $1,000

- Net Income: $5,000 – $1,000 = $4,000

- Cash Inflows:

-

Result:

- Sarah’s cash basis net income for July is $4,000.

4.2. Example 2: Retail Business

-

Scenario:

- A small retail store, “Books & More,” uses the cash basis method. In August, they have the following cash transactions:

- Cash Sales: $10,000

- Payments to Suppliers: $4,000

- Rent Payment: $1,500

- Utilities Payment: $500

- Employee Wages: $2,000

- A small retail store, “Books & More,” uses the cash basis method. In August, they have the following cash transactions:

-

Calculation:

- Cash Inflows:

- Cash Sales: $10,000

- Cash Outflows:

- Payments to Suppliers: $4,000

- Rent Payment: $1,500

- Utilities Payment: $500

- Employee Wages: $2,000

- Total Cash Inflows: $10,000

- Total Cash Outflows: $4,000 + $1,500 + $500 + $2,000 = $8,000

- Net Income: $10,000 – $8,000 = $2,000

- Cash Inflows:

-

Result:

- Books & More’s cash basis net income for August is $2,000.

4.3. What if Expenses Exceed Revenue?

If your expenses exceed your revenue, you have a net loss. This means your business spent more money than it brought in during the period.

When expenses exceed revenue, a business experiences a net loss, indicating that more money was spent than earned during a specific period. This situation can arise from various factors, such as high operating costs, low sales volume, or significant one-time expenses. Understanding and addressing a net loss is crucial for the long-term sustainability of the business. Here are key steps to consider:

-

Identify the Causes:

- Analyze financial statements to pinpoint the specific reasons for the net loss.

- Examine revenue trends to see if sales have declined or if pricing strategies are ineffective.

- Review expenses to identify areas where costs are too high or unnecessary.

-

Implement Cost-Cutting Measures:

- Reduce discretionary spending, such as travel, entertainment, and non-essential supplies.

- Renegotiate contracts with suppliers to lower procurement costs.

- Improve operational efficiency to reduce waste and lower production costs.

-

Increase Revenue:

- Develop and implement marketing strategies to attract new customers and increase sales.

- Explore new product or service offerings to diversify revenue streams.

- Improve customer service to enhance customer loyalty and repeat business.

-

Manage Cash Flow:

- Monitor cash inflows and outflows closely to ensure sufficient liquidity.

- Delay non-essential payments to conserve cash.

- Consider short-term financing options, such as lines of credit, to bridge cash flow gaps.

5. Why is Cash Basis Net Income Important for Partnering?

Understanding your cash basis net income is vital when seeking business partners. It provides a clear view of your financial health, helping potential partners assess the stability and profitability of your business.

Understanding cash basis net income is particularly important when seeking business partners, as it provides a clear and immediate view of a company’s financial health based on actual cash flow. Here’s why it matters:

- Transparency: Cash basis net income offers a straightforward and easily understandable picture of a company’s financial performance. This transparency can build trust with potential partners, as it is less susceptible to accounting complexities and estimations.

- Liquidity Assessment: Partners are keen to understand a company’s ability to meet its short-term obligations. Cash basis net income provides insights into the company’s current liquidity, demonstrating its capacity to manage day-to-day expenses and invest in growth opportunities.

- Profitability Evaluation: While cash basis net income may not provide a complete view of long-term profitability, it does offer a snapshot of how much cash a company is generating over a specific period. Partners can use this information to assess the immediate financial viability of the business.

- Risk Management: Understanding cash basis net income helps partners evaluate the financial risks associated with the business. A consistent positive cash flow indicates stability, while negative cash flow may raise concerns about the company’s ability to sustain operations.

- Decision Making: Potential partners can use cash basis net income to inform their investment decisions. It helps them assess whether the business is a worthwhile venture and how their resources can be best utilized to achieve mutual financial goals.

5.1. How Does it Impact Investor Decisions?

Investors often use cash basis net income as a quick indicator of a company’s financial stability and ability to generate cash. While it’s not a comprehensive measure, it can influence their initial assessment.

Cash basis net income can significantly impact investor decisions by providing a clear, immediate view of a company’s financial health based on actual cash flow. Here’s how:

- Initial Screening: Investors often use cash basis net income as an initial screening tool. A positive cash basis net income indicates that the company is generating more cash than it is spending, suggesting financial stability.

- Liquidity Assessment: Investors assess a company’s ability to meet its short-term obligations. Cash basis net income provides insights into the company’s current liquidity, demonstrating its capacity to manage day-to-day expenses and invest in growth opportunities.

- Risk Evaluation: Understanding cash basis net income helps investors evaluate the financial risks associated with the business. A consistent positive cash flow indicates stability, while negative cash flow may raise concerns about the company’s ability to sustain operations.

- Profitability Snapshot: While cash basis net income may not provide a complete view of long-term profitability, it does offer a snapshot of how much cash a company is generating over a specific period.

- Comparative Analysis: Investors may compare cash basis net income across different periods or against industry benchmarks to identify trends and assess performance relative to competitors.

5.2. What Should You Disclose to Potential Partners?

When seeking partners, be transparent about your accounting method and provide accurate, up-to-date financial information. Highlight both the strengths and limitations of using the cash basis method.

Transparency is crucial when disclosing financial information to potential partners. Here’s what you should disclose:

- Accounting Method: Clearly state that you use the cash basis method of accounting.

- Financial Statements:

- Provide accurate and up-to-date income statements (profit and loss statements) prepared using the cash basis method.

- Include balance sheets showing cash balances, assets, and liabilities.

- Offer cash flow statements detailing cash inflows and outflows.

- Explanation of Cash Basis Method: Explain the key principles of the cash basis method, emphasizing that revenue is recognized when cash is received and expenses are recognized when cash is paid.

- Strengths of Cash Basis Method: Highlight the benefits of using the cash basis method, such as its simplicity, ease of use, and clear reflection of current cash flow.

- Limitations of Cash Basis Method:

- Acknowledge the limitations of the cash basis method, such as its potential to distort the true financial picture by not recognizing revenues and expenses when they are earned or incurred.

- Explain that it may not comply with Generally Accepted Accounting Principles (GAAP).

- Tax Implications: Discuss any tax implications related to using the cash basis method, such as potential strategies for deferring income or accelerating expenses.

- Future Plans: Share any plans to transition to accrual accounting in the future, especially if the business is growing and requires more sophisticated financial reporting.

5.3. How Can Income-Partners.net Help You Find the Right Partners?

Income-partners.net offers a platform to connect with partners who understand and appreciate the financial transparency provided by the cash basis method. We provide resources and tools to help you showcase your financial health effectively.

Income-partners.net can be instrumental in helping you find the right partners by offering a platform that values transparency and financial clarity. Here’s how:

-

Networking Opportunities:

- Income-partners.net provides a robust networking platform where businesses can connect with potential partners who understand and appreciate the financial transparency offered by the cash basis method.

- The platform allows you to showcase your business’s financial health and stability, making it easier to attract partners who align with your values and goals.

-

Resource and Tools:

- The website offers a range of resources and tools to help you effectively present your financial information.

- You can access templates for creating clear and concise financial statements, including income statements, balance sheets, and cash flow statements.

- These tools help you highlight the strengths of your cash basis accounting method, emphasizing its simplicity and direct reflection of cash flow.

-

Educational Content:

- income-partners.net offers educational content that explains the benefits and limitations of the cash basis method.

- This content helps potential partners understand your accounting practices and appreciate the transparency of your financial reporting.

-

Financial Health Showcase:

- The platform allows you to showcase your business’s financial health in a way that is easily understood by potential partners.

- By highlighting your positive cash flow, you can demonstrate your ability to manage day-to-day expenses, invest in growth opportunities, and meet short-term obligations.

6. Common Mistakes to Avoid When Calculating Cash Basis Net Income

Several common mistakes can skew your cash basis net income calculation. These include failing to track all cash transactions, confusing cash and accrual methods, and neglecting to reconcile bank statements.

Several common mistakes can undermine the accuracy of your cash basis net income calculation. Avoiding these pitfalls is essential for maintaining reliable financial records.

-

Failing to Track All Cash Transactions:

- Mistake: Overlooking or failing to record every cash inflow and outflow.

- Solution: Meticulously document all cash transactions, no matter how small. Use accounting software or spreadsheets to keep a comprehensive record of all receipts and payments.

-

Confusing Cash and Accrual Methods:

- Mistake: Mixing up the principles of cash basis and accrual accounting, such as recognizing revenue when earned rather than when cash is received.

- Solution: Stick strictly to the cash basis method. Recognize revenue only when cash is received and expenses only when cash is paid.

-

Neglecting to Reconcile Bank Statements:

- Mistake: Failing to regularly reconcile bank statements with your internal records.

- Solution: Reconcile bank statements monthly to identify any discrepancies and ensure that all transactions are accurately recorded.

-

Ignoring Non-Cash Transactions:

- Mistake: Including non-cash transactions, such as depreciation or amortization, in your cash basis net income calculation.

- Solution: Focus solely on cash transactions. Exclude any non-cash items from your calculation.

-

Improperly Classifying Transactions:

- Mistake: Misclassifying transactions, such as categorizing a capital expenditure as an operating expense.

- Solution: Properly classify each transaction according to its nature. Ensure that capital expenditures are treated as investments rather than immediate expenses.

6.1. What Happens if You Don’t Reconcile Bank Statements?

Failing to reconcile bank statements can lead to inaccurate financial records and missed transactions, skewing your net income calculation.

Failing to reconcile bank statements regularly can lead to significant discrepancies and inaccuracies in your financial records. Here’s what can happen if you neglect this crucial task:

-

Unidentified Errors:

- Problem: Errors in bank transactions, such as incorrect charges or duplicate withdrawals, may go unnoticed.

- Impact: These errors can distort your cash balance and lead to inaccurate financial reporting.

-

Missed Transactions:

- Problem: Transactions that are not properly recorded in your internal records, such as direct deposits or automatic payments, may be missed.

- Impact: This can result in an incomplete picture of your cash inflows and outflows, affecting the accuracy of your net income calculation.

-

Fraudulent Activity:

- Problem: Unauthorized or fraudulent transactions may go undetected, leading to financial losses.

- Impact: Early detection of fraudulent activity can help minimize financial damage and prevent further losses.

-

Inaccurate Cash Balance:

- Problem: The cash balance in your internal records may not match the actual cash balance in your bank account.

- Impact: This can lead to poor financial decision-making, as you may not have a clear understanding of your available funds.

-

Compliance Issues:

- Problem: Failure to reconcile bank statements can raise red flags during audits or tax reviews.

- Impact: It can lead to compliance issues and potential penalties.

6.2. How Can Accounting Software Help?

Accounting software automates many of the tasks involved in calculating cash basis net income, reducing the risk of errors and saving time.

Accounting software can be an invaluable tool for calculating cash basis net income, automating many tasks and reducing the risk of errors. Here’s how it helps:

-

Automated Transaction Tracking:

- Benefit: Automatically records and categorizes cash inflows and outflows from linked bank accounts and credit cards.

- Impact: Reduces manual data entry and ensures that all transactions are captured accurately.

-

Real-Time Financial Data:

- Benefit: Provides real-time access to financial data, allowing you to monitor your cash position and net income at any time.

- Impact: Enables proactive financial management and informed decision-making.

-

Simplified Reporting:

- Benefit: Generates income statements, balance sheets, and cash flow statements with ease.

- Impact: Saves time and effort in preparing financial reports, ensuring accuracy and compliance.

-

Bank Reconciliation:

- Benefit: Automates the bank reconciliation process, matching transactions in your accounting software with those in your bank statements.

- Impact: Helps identify discrepancies and ensures that your cash balance is accurate.

-

Error Reduction:

- Benefit: Minimizes manual errors through automated calculations and data validation.

- Impact: Enhances the reliability of your financial data and reduces the risk of costly mistakes.

-

Tax Compliance:

- Benefit: Helps you stay compliant with tax regulations by accurately tracking income and expenses.

- Impact: Simplifies tax preparation and reduces the risk of audits or penalties.

7. Optimizing Cash Basis Net Income for Growth

Optimizing your cash basis net income involves strategies to increase cash inflows and decrease cash outflows. This can include improving sales, reducing expenses, and managing inventory effectively.

Optimizing cash basis net income is crucial for sustainable growth. It involves implementing strategies to maximize cash inflows and minimize cash outflows, ultimately enhancing profitability and financial stability. Here’s how to optimize your cash basis net income:

-

Increase Cash Inflows:

- Improve Sales Strategies: Implement targeted marketing campaigns, enhance customer service, and offer promotions to drive sales.

- Expand Product/Service Offerings: Introduce new products or services that meet customer needs and generate additional revenue streams.

- Offer Payment Incentives: Provide discounts for early payments or offer flexible payment options to encourage timely cash inflows.

-

Decrease Cash Outflows:

- Negotiate with Suppliers: Renegotiate contracts with suppliers to secure better pricing and payment terms.

- Reduce Operating Expenses: Identify areas where costs can be cut without compromising quality or efficiency.

- Manage Inventory Effectively: Implement inventory management techniques to minimize carrying costs and prevent overstocking.

-

Improve Cash Flow Management:

- Monitor Cash Flow Regularly: Track cash inflows and outflows closely to identify trends and potential issues.

- Create a Budget: Develop a detailed budget to forecast cash flow and manage spending effectively.

- Invoice Promptly: Send invoices promptly and follow up on overdue payments to accelerate cash inflows.

-

Invest in Efficiency:

- Automate Processes: Automate routine tasks to reduce labor costs and improve efficiency.

- Adopt Technology: Invest in technology solutions that streamline operations and enhance productivity.

7.1. How Can You Increase Cash Inflows?

Increasing cash inflows can be achieved through various strategies, such as improving sales and marketing efforts, offering discounts for early payments, and diversifying revenue streams.

Increasing cash inflows is a critical objective for businesses seeking to improve their financial health and fuel growth. Effective strategies include:

-

Enhance Sales and Marketing:

- Targeted Marketing Campaigns: Implement marketing campaigns that focus on specific customer segments and their needs.

- Improve Customer Service: Enhance customer service to build loyalty and generate repeat business.

- Offer Promotions and Discounts: Provide incentives to attract new customers and encourage existing customers to make purchases.

-

Diversify Revenue Streams:

- Introduce New Products/Services: Expand your product or service offerings to cater to a broader customer base.

- Explore New Markets: Enter new geographic or demographic markets to reach untapped customer segments.

- Offer Value-Added Services: Provide additional services that complement your core offerings and generate extra revenue.

-

Improve Pricing Strategies:

- Competitive Pricing: Analyze competitor pricing and adjust your prices accordingly to attract customers.

- Value-Based Pricing: Price your products or services based on the value they provide to customers.

- Dynamic Pricing: Adjust prices based on demand, seasonality, or other market factors.

-

Streamline Sales Processes:

- Simplify Ordering: Make it easy for customers to place orders through online platforms, mobile apps, or other convenient channels.