Are you looking to get a clearer picture of your business’s financial health? Calculating accrual basis net income is key, and at income-partners.net, we’re here to help you understand how to do it right. Accrual accounting offers a more accurate view of profitability by matching revenues with related expenses, helping you make informed partnership decisions and drive revenue growth. We’ll cover everything you need to know, from understanding the accrual method to applying practical examples, ensuring you can confidently navigate financial reporting. Let’s dive into the concepts of revenue recognition, expense matching, and financial partnerships.

1. What is Accrual Basis Net Income?

Accrual basis net income is a financial metric that reflects a company’s profitability by recognizing revenue when it’s earned and expenses when they’re incurred, regardless of when cash changes hands. This method provides a more accurate picture of a business’s financial performance over a specific period.

1.1 The Core Principles of Accrual Accounting

Accrual accounting relies on two key principles:

- Revenue Recognition Principle: Revenue is recognized when it’s earned, not necessarily when cash is received.

- Matching Principle: Expenses are recognized in the same period as the revenue they helped generate.

These principles ensure that financial statements accurately reflect the economic reality of a business, as reported by the Harvard Business Review.

1.2 Why Accrual Basis Matters for Net Income

Unlike cash basis accounting, which only records transactions when cash is exchanged, accrual accounting provides a more comprehensive view of a company’s financial health. This is especially important for businesses with significant accounts receivable or accounts payable. Accrual accounting provides a more accurate picture of profitability by matching revenues with related expenses.

2. Understanding the Formula for Accrual Basis Net Income

The formula for calculating accrual basis net income is straightforward:

Accrual Basis Net Income = Total Accrued Revenues – Total Accrued Expenses

This formula accounts for all revenues earned and expenses incurred during a specific period, regardless of whether cash has been exchanged.

2.1 Breaking Down Accrued Revenues

Accrued revenues are revenues that have been earned but not yet received in cash. This can include sales on credit, services provided but not yet billed, and other similar transactions.

2.2 Breaking Down Accrued Expenses

Accrued expenses are expenses that have been incurred but not yet paid in cash. This can include salaries owed to employees, rent for the current period that hasn’t been paid, and other similar obligations.

2.3 Practical Example of the Calculation

Let’s say a company has total accrued revenues of $500,000 and total accrued expenses of $300,000 for the year. The accrual basis net income would be:

Accrual Basis Net Income = $500,000 – $300,000 = $200,000

Accrual Basis Net Income Calculation

Accrual Basis Net Income Calculation

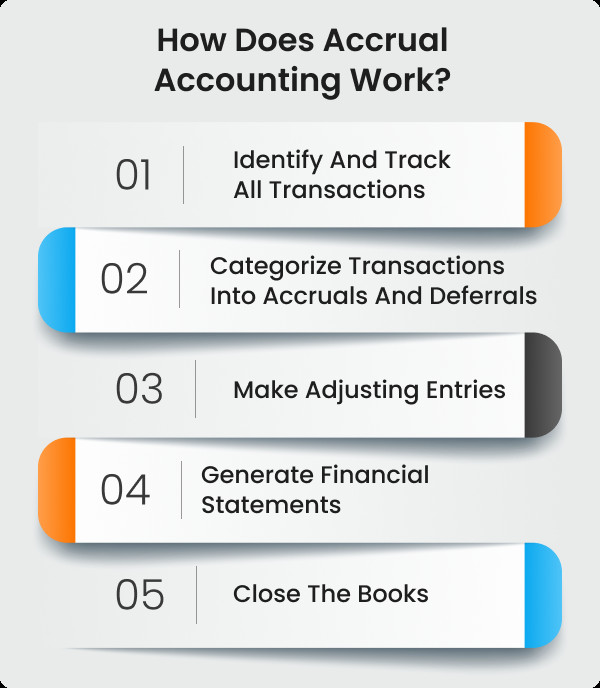

3. Step-by-Step Guide to Calculating Accrual Basis Net Income

Calculating accrual basis net income involves several key steps:

- Identify All Revenues: Determine all revenues earned during the accounting period, regardless of when cash was received.

- Identify All Expenses: Determine all expenses incurred during the accounting period, regardless of when cash was paid.

- Adjust for Accruals and Deferrals: Make necessary adjustments for accrued revenues, accrued expenses, deferred revenues, and deferred expenses.

- Calculate Net Income: Subtract total expenses from total revenues to arrive at accrual basis net income.

3.1 Identifying and Recording Revenues

Start by identifying all sources of revenue for your business. This includes sales revenue, service revenue, and any other income earned during the accounting period.

3.2 Identifying and Recording Expenses

Next, identify all expenses incurred during the accounting period. This includes cost of goods sold, salaries, rent, utilities, and any other costs associated with running your business.

3.3 Adjusting Entries: Accruals and Deferrals

Adjusting entries are crucial for accurately reflecting the economic reality of your business. These entries account for revenues and expenses that have been earned or incurred but not yet recorded.

3.3.1 Accrued Revenues

Accrued revenues are revenues that have been earned but not yet received in cash. For example, if you provide services to a client in December but don’t bill them until January, you would need to make an adjusting entry to recognize the revenue in December.

3.3.2 Accrued Expenses

Accrued expenses are expenses that have been incurred but not yet paid in cash. For example, if you owe your employees salaries for the last week of December but don’t pay them until January, you would need to make an adjusting entry to recognize the expense in December.

3.3.3 Deferred Revenues

Deferred revenues are revenues that have been received in cash but not yet earned. For example, if you receive a prepayment from a customer for services to be provided in the future, you would need to make an adjusting entry to defer the revenue until it is earned.

3.3.4 Deferred Expenses

Deferred expenses are expenses that have been paid in cash but not yet incurred. For example, if you pay for insurance coverage for the next six months, you would need to make an adjusting entry to defer the expense until it is incurred.

3.4 Calculating the Final Net Income Figure

Once you’ve made all necessary adjusting entries, you can calculate the final net income figure by subtracting total expenses from total revenues.

4. Accrual Basis vs. Cash Basis Accounting: What’s the Difference?

The main difference between accrual basis and cash basis accounting lies in the timing of when revenues and expenses are recognized.

- Accrual Basis: Recognizes revenues when earned and expenses when incurred, regardless of when cash changes hands.

- Cash Basis: Recognizes revenues when cash is received and expenses when cash is paid.

4.1 Timing of Revenue Recognition

Under accrual accounting, revenue is recognized when it’s earned, not necessarily when cash is received. Under cash basis accounting, revenue is recognized only when cash is received.

4.2 Timing of Expense Recognition

Under accrual accounting, expenses are recognized when they’re incurred, not necessarily when cash is paid. Under cash basis accounting, expenses are recognized only when cash is paid.

4.3 Which Method is Right for Your Business?

The choice between accrual and cash basis accounting depends on several factors, including the size and complexity of your business, as well as any regulatory requirements.

- Small Businesses: Cash basis accounting may be simpler and more appropriate for very small businesses with few transactions.

- Larger Businesses: Accrual basis accounting is generally required for larger businesses and those that need to comply with GAAP (Generally Accepted Accounting Principles).

According to Entrepreneur.com, accrual accounting provides a more accurate picture of a company’s financial health, making it the preferred method for most businesses.

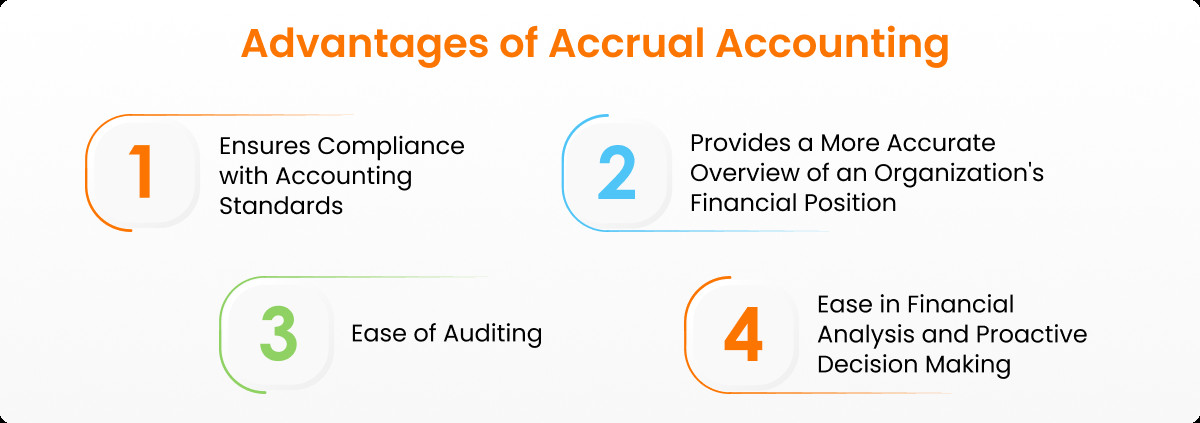

5. Benefits of Using Accrual Basis Accounting

Accrual basis accounting offers several key benefits:

- More Accurate Financial Picture: Provides a more accurate representation of a company’s financial performance over time.

- Better Matching of Revenues and Expenses: Matches revenues with the expenses that helped generate them, providing a more complete picture of profitability.

- Compliance with GAAP: Required for companies that need to comply with GAAP.

- Improved Decision-Making: Provides better information for making informed business decisions.

5.1 Enhanced Financial Reporting

Accrual accounting provides more detailed and accurate financial reports, which can be used to track performance, identify trends, and make informed decisions.

5.2 Improved Financial Analysis

Accrual accounting allows for more sophisticated financial analysis, such as ratio analysis and trend analysis, which can provide valuable insights into a company’s financial health.

5.3 Better Decision-Making for Partnerships

Accrual accounting provides a clearer picture of profitability, which is essential for evaluating potential partnerships and making informed decisions about business growth.

Accrual Accounting Benefits

Accrual Accounting Benefits

6. Common Mistakes to Avoid When Calculating Accrual Basis Net Income

Calculating accrual basis net income can be complex, and it’s easy to make mistakes. Here are some common errors to avoid:

- Incorrectly Recognizing Revenue: Recognizing revenue too early or too late can distort your financial statements.

- Incorrectly Recognizing Expenses: Failing to match expenses with the related revenue can also lead to inaccurate financial reporting.

- Not Making Adjusting Entries: Failing to make necessary adjusting entries for accruals and deferrals can result in an incomplete picture of your business’s financial health.

- Not Following GAAP: Failing to comply with GAAP can lead to non-compliance issues and inaccurate financial reporting.

6.1 Revenue Recognition Errors

Ensure that you are following the revenue recognition principle and recognizing revenue only when it has been earned.

6.2 Expense Matching Errors

Make sure that you are matching expenses with the revenue they helped generate. For example, if you sell a product in December but incur the cost of goods sold in November, you should recognize the expense in December.

6.3 Overlooking Accruals and Deferrals

Don’t forget to make adjusting entries for accruals and deferrals. These entries are essential for accurately reflecting the economic reality of your business.

7. Tools and Software for Accrual Accounting

There are many tools and software programs available to help you with accrual accounting. Some popular options include:

- QuickBooks: A popular accounting software for small businesses.

- Xero: Another popular accounting software with a focus on ease of use.

- NetSuite: A comprehensive ERP (Enterprise Resource Planning) system for larger businesses.

- Sage Intacct: A cloud-based accounting software for mid-sized businesses.

7.1 Popular Accounting Software

These software programs can help you automate many of the tasks associated with accrual accounting, such as recording transactions, making adjusting entries, and generating financial reports.

7.2 Features to Look for in Accounting Software

When choosing accounting software, look for features such as:

- Accrual Accounting Capabilities: The software should support accrual accounting methods.

- Adjusting Entry Functionality: The software should allow you to easily make adjusting entries for accruals and deferrals.

- Reporting Capabilities: The software should be able to generate accurate and detailed financial reports.

- Integration with Other Systems: The software should be able to integrate with other systems, such as your bank account and CRM (Customer Relationship Management) system.

8. How Accrual Basis Net Income Affects Business Partnerships

Accrual basis net income plays a crucial role in business partnerships, as it provides a more accurate and comprehensive view of a company’s financial performance. This is especially important when evaluating potential partnerships and making decisions about profit sharing and resource allocation.

8.1 Evaluating Partnership Opportunities

When considering a partnership, it’s essential to understand the financial health of the potential partner. Accrual basis net income provides a more accurate picture of profitability than cash basis accounting, allowing you to make informed decisions about whether to proceed with the partnership.

8.2 Determining Profit Sharing

Accrual basis net income can be used to determine how profits will be shared among partners. By using a more accurate measure of profitability, partners can ensure that they are being fairly compensated for their contributions to the business.

8.3 Strategic Decision-Making

Accrual basis net income provides valuable information for making strategic decisions about business growth and resource allocation. By understanding the true profitability of your business, you can make informed decisions about where to invest your resources and how to grow your business.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

9. Real-World Examples of Accrual Basis Net Income in Action

To illustrate the importance of accrual basis net income, let’s look at some real-world examples:

- Consulting Firm: A consulting firm provides services to a client in December but doesn’t bill them until January. Under accrual accounting, the revenue is recognized in December, providing a more accurate picture of the firm’s performance for that year.

- Retail Business: A retail business purchases inventory in November but doesn’t sell it until December. Under accrual accounting, the cost of goods sold is recognized in December, matching the expense with the related revenue.

- Subscription Service: A subscription service receives a prepayment from a customer for a year’s worth of service. Under accrual accounting, the revenue is recognized over the course of the year, as the service is provided.

9.1 Case Study: Consulting Firm

A consulting firm provides services to a client in December but doesn’t bill them until January. Under cash basis accounting, the revenue would be recognized in January, when the cash is received. However, under accrual accounting, the revenue is recognized in December, providing a more accurate picture of the firm’s performance for that year.

9.2 Case Study: Retail Business

A retail business purchases inventory in November but doesn’t sell it until December. Under cash basis accounting, the cost of goods sold would be recognized in November, when the cash is paid. However, under accrual accounting, the cost of goods sold is recognized in December, matching the expense with the related revenue.

9.3 Case Study: Subscription Service

A subscription service receives a prepayment from a customer for a year’s worth of service. Under cash basis accounting, the revenue would be recognized immediately, when the cash is received. However, under accrual accounting, the revenue is recognized over the course of the year, as the service is provided.

10. Expert Tips for Accurate Accrual Basis Net Income Calculation

To ensure that you are accurately calculating accrual basis net income, follow these expert tips:

- Maintain Accurate Records: Keep detailed records of all revenues and expenses, including supporting documentation.

- Make Adjusting Entries Regularly: Make adjusting entries for accruals and deferrals at the end of each accounting period.

- Consult with a Professional: If you are unsure about any aspect of accrual accounting, consult with a qualified accountant or financial advisor.

- Use Accounting Software: Use accounting software to automate many of the tasks associated with accrual accounting.

10.1 Importance of Detailed Record-Keeping

Accurate accrual accounting relies on detailed and accurate record-keeping. Keep track of all revenues and expenses, including invoices, receipts, and other supporting documentation.

10.2 Regular Reconciliation

Reconcile your accounts regularly to ensure that your records are accurate and up-to-date. This can help you identify and correct any errors or discrepancies.

10.3 Seeking Professional Advice

If you are unsure about any aspect of accrual accounting, consult with a qualified accountant or financial advisor. They can provide valuable guidance and help you ensure that you are accurately calculating your accrual basis net income.

At income-partners.net, we understand the importance of accurate financial reporting for successful business partnerships. That’s why we provide resources and support to help you navigate the complexities of accrual accounting. Contact us today to learn more about how we can help you find the perfect partner to grow your business and improve your financial performance. Don’t miss out on the opportunity to explore our strategic partnership options and revenue-boosting strategies at income-partners.net.

Frequently Asked Questions (FAQs)

1. What is the difference between accrual and cash basis accounting?

Accrual accounting recognizes revenues when earned and expenses when incurred, regardless of when cash changes hands. Cash basis accounting recognizes revenues when cash is received and expenses when cash is paid.

2. Is accrual accounting required for all businesses?

No, accrual accounting is generally required for larger businesses and those that need to comply with GAAP. Small businesses may be able to use cash basis accounting.

3. How do I calculate accrual basis net income?

Accrual basis net income is calculated by subtracting total accrued expenses from total accrued revenues.

4. What are accrued revenues?

Accrued revenues are revenues that have been earned but not yet received in cash.

5. What are accrued expenses?

Accrued expenses are expenses that have been incurred but not yet paid in cash.

6. What are deferred revenues?

Deferred revenues are revenues that have been received in cash but not yet earned.

7. What are deferred expenses?

Deferred expenses are expenses that have been paid in cash but not yet incurred.

8. What are some common mistakes to avoid when calculating accrual basis net income?

Common mistakes include incorrectly recognizing revenue, incorrectly recognizing expenses, not making adjusting entries, and not following GAAP.

9. What tools and software can help with accrual accounting?

Popular accounting software programs include QuickBooks, Xero, NetSuite, and Sage Intacct.

10. How does accrual basis net income affect business partnerships?

Accrual basis net income provides a more accurate picture of profitability, which is essential for evaluating potential partnerships and making informed decisions about profit sharing and resource allocation.