Building wealth with a low income is absolutely achievable and income-partners.net can show you how. It’s about adopting smart money management strategies, focusing on long-term growth, and making informed financial decisions. Discover the strategies and mindset shifts necessary to achieve financial success, including budgeting tips, investment options, and the power of partnership, with a focus on generating passive income and achieving financial freedom.

1. Adopt a Wealth-Building Mindset

Yes, building wealth on a low income is possible, and it all starts with believing it. Many people mistakenly believe they lack the worth, intelligence, or opportunities to achieve financial success.

The quickest way to stop negative thinking is to focus on your own journey and avoid comparing yourself to others. Instead of focusing on what you’re lacking, be enthusiastic about the resources you have and be inspired by success stories of others who have built wealth on a low income.

Examples of People Who Became Wealthy on a Low Income:

- Geoffrey Holt: Despite never earning much money as a mobile home park caretaker, he amassed a secret multi-million dollar fortune through frugal habits. His estate of $3.8 million was left to his hometown to benefit the community.

- Theodore Johnson: A UPS worker who never made more than $14,000 in a single year, Johnson died with $70 million. He was a frugal legend who invested “early and often,” which was the primary driver of his enormous wealth.

- Sarah Wilson (Budget Girl): She is a relatable frugal hero who lives in a small Texas town, earns a single income, and is gradually building wealth. She shares her income, expenses, and budgeting tips on YouTube for others to follow.

Geoffrey Holt secret millionaire

Geoffrey Holt secret millionaire

2. Savings vs. Investing: Understanding the Difference

Understanding the difference between saving and investing money is essential for building wealth with any level of income. Saving and investing serve different but equally important purposes. Investing is necessary for building wealth, while simply saving money is insufficient.

Saving money entails protecting it for a specific savings goal. Any funds not needed for spending or potential emergencies should be invested to grow over time.

For example, you should save money for an emergency fund, a car, weddings, a home down payment, or any other sinking fund goals. However, you should avoid hoarding too much cash beyond saving for specific goals because of inflation.

Inflation Erodes Cash

You cannot save your way to retirement because inflation reduces the value of your savings each year. Investing your money and earning interest on your investments is the only way to combat this.

If you have $100 in your savings account and inflation rises by 3% in a year, that $100 will only have $97 in buying power. While this may not seem significant in one year, its impact on your money compounded over years or decades can be substantial. If inflation averages 3%, your purchasing power will be cut in half in just 23 years.

Compound interest, on the other hand, works in your favor when investing. Compound interest can significantly increase your net worth over time if your money is invested. Investing in highly diversified index funds is a great way to hedge against inflation because the S&P 500 has historically returned an average of 10% over the last 100 years.

However, keep in mind that this is an average return, meaning market returns can vary significantly from year to year. While there is always some risk involved in investing, you can reduce that risk by adopting a long-term investing strategy and committing to keeping your money invested for a longer period.

Can I Save My Way to Retirement?

Compound interest is the most powerful force for building wealth on a small income. When the interest earned on your initial investment begins to earn interest itself, this is known as compound interest. This accelerates the growth of your retirement nest egg over time, making it the secret ingredient to wealth creation.

Here’s a quick example: Suppose you are 20 years old and earn $40,000 per year after taxes. You have approximately $400 per month left over to save or invest after expenses. If you saved that $400 each month for 45 years in a savings account, you would have a total of $216,000 to retire with.

However, if you invested that money instead each month, you could retire with $3,606,180, assuming a 10% average return on investment. That is more than ten times what you could save in plain cash.

Learning to invest is essential for building wealth on a small income. Luckily, it is not as intimidating as it appears.

3. Build an Emergency Fund

An emergency fund can protect you from going into debt or dipping into other savings when shmutz hits the fan. You will also have greater peace of mind knowing that you will be able to weather whatever life throws your way.

While you should ultimately aim to save 3-6 months’ worth of expenses to fully fund your emergency fund, saving just $2,467 can cover most surprises, according to economists.

Pro Tip: Do not keep your emergency savings in a regular bank. Pointless fees can deplete your funds, and you will not earn enough interest to outpace inflation. Instead, open an account with a High Yield Savings Account (HYSA). This will allow you to earn up to ten times the national average in interest and eliminate some of the egregious fees that large banks frequently charge.

chances of losing money in stock market

chances of losing money in stock market

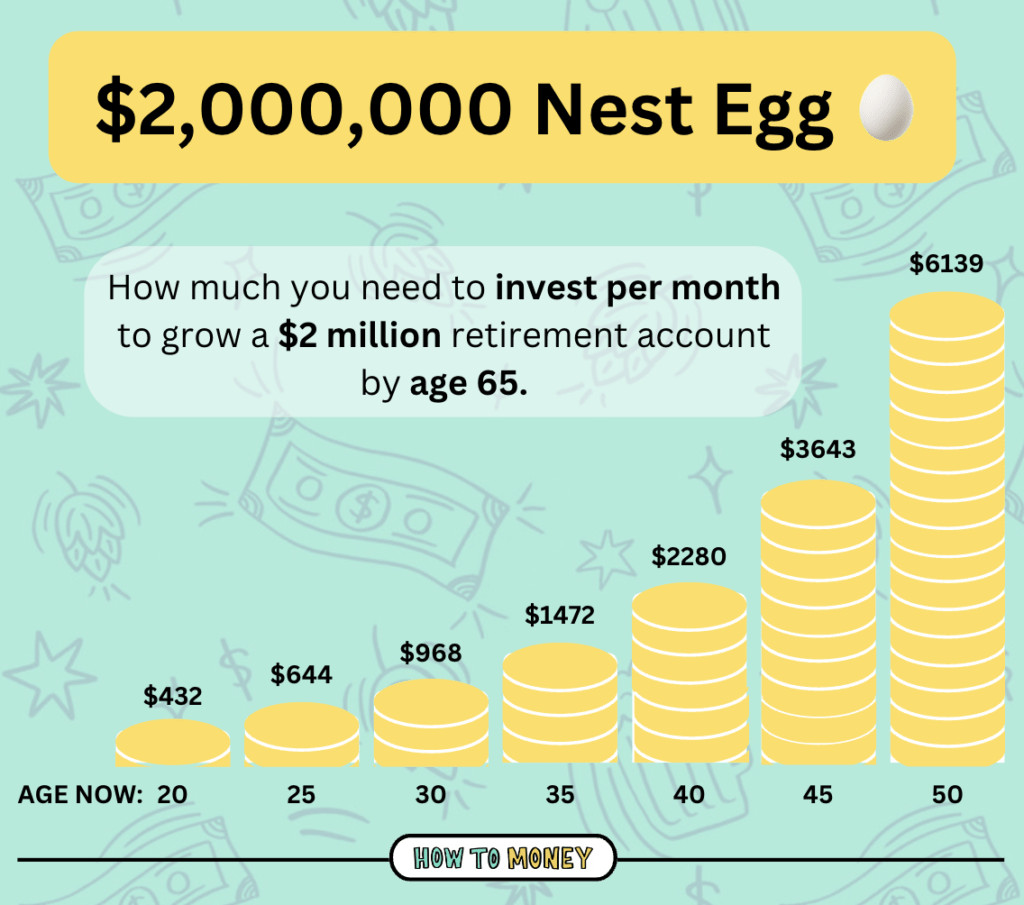

4. Start Investing As Soon As Possible

TIME is your greatest asset when building wealth on a small income. Saving $1 now is more powerful than saving $100 later. The sooner you start and the longer your time horizon, the less money you need to save each month to retire comfortably.

For example, if you start investing at age 20 and want to have approximately $2 million in retirement, you will need to invest approximately $432 per month. However, if you wait until age 40, you will need to invest approximately $2,280 per month to retire with the same amount of money.

No matter your age, you must prioritize investing now. It can be difficult to save a few hundred dollars per month with a small income, but it is easier than saving a few thousand later when playing catch up.

Which Accounts Are Best to Start Investing With?

We always recommend starting with one of the tax-advantaged accounts available to you if you want to start investing. These accounts can provide significant tax benefits that lower your taxes now or in the future.

401(k) Plans

If your employer offers a 401(k), you should take advantage of that investment account first, especially if they offer an employer match. An employer match is essentially free money that your employer will contribute on your behalf toward your retirement.

If you do not contribute to your 401(k) with an employer match, you are committing a cardinal investing sin. You are leaving money on the table, and because we are working with a low income, every penny counts.

You can contribute up to $23,000 per year to your 401(k). Furthermore, contributing to a 401(k) can save you money immediately because your taxable income will be reduced due to the account’s tax-advantaged status. Then, when you withdraw your funds in retirement, you will pay taxes on your withdrawals.

If you do not have a 401(k): Consider asking your boss or business owner to establish one. Human Interest is an excellent fintech service provider that assists businesses in establishing simple and affordable retirement plans for their employees. It never hurts to inquire.

Company-sponsored retirement plans are a win/win for you and your employer because you will likely stay longer if they offer these excellent benefits.

Roth IRA

Not everyone has access to a 401(k). If you fall into this category, you can begin by contributing to a Roth IRA.

Roth IRAs are excellent investment accounts because you contribute with dollars that have already been taxed. Then, when you withdraw your funds in retirement, you will not be taxed on them.

Each year, you can contribute up to $7,000 to a Roth IRA (2024 limits), but if you are over 50, you can take advantage of “catch-up contributions.” This means that you can contribute an additional $1,000 to your Roth IRA each year to compensate for lost time.

Pay Yourself First

While it may be tempting to wait until the end of the month and save whatever is left over, there is a smarter way to save more and improve your financial future. We highly recommend “paying yourself first” when it comes to saving and investing.

This means that as soon as you are paid for the month, you should immediately contribute money to your retirement accounts. Consider retirement investments and savings goals to be bills that must be paid at the beginning of each month.

If you make transfers before paying all of your other bills and before discretionary spending, you will find a way to live off whatever remains in your accounts after your contributions.

Waiting until the end of the month to save is a mistake. If you do not prioritize savings and investing, you will likely have less money to contribute. Instead of simply saving the “scraps” for yourself, prioritize your financial future. We want you to complete these critical tasks at the beginning of each pay period.

Small Amounts Add Up

It is easy to believe that “there is no point in saving or investing right now because I can only spare a few dollars.” However, every dollar counts if you are attempting to build wealth with a small income. When you begin contributing is sometimes more important than how much you invest.

For example, suppose you can only contribute $50 per month between the ages of 18 and 28. Then, at age 28, you change jobs and can contribute $400 per month thereafter. You will be able to retire at age 65 with $1,165,299! (This assumes an 8% annual return on investments).

However, if you waited until age 28 to begin investing, you would only have $1,009,981. Those seemingly paltry $50 per month contributions add up to over $150,000 by the time you retire.

Therefore, it is critical to begin contributing now, even if it is only a small amount. Those few dollars here and there can add up to thousands in retirement.

time to build a m nest egg by age

time to build a m nest egg by age

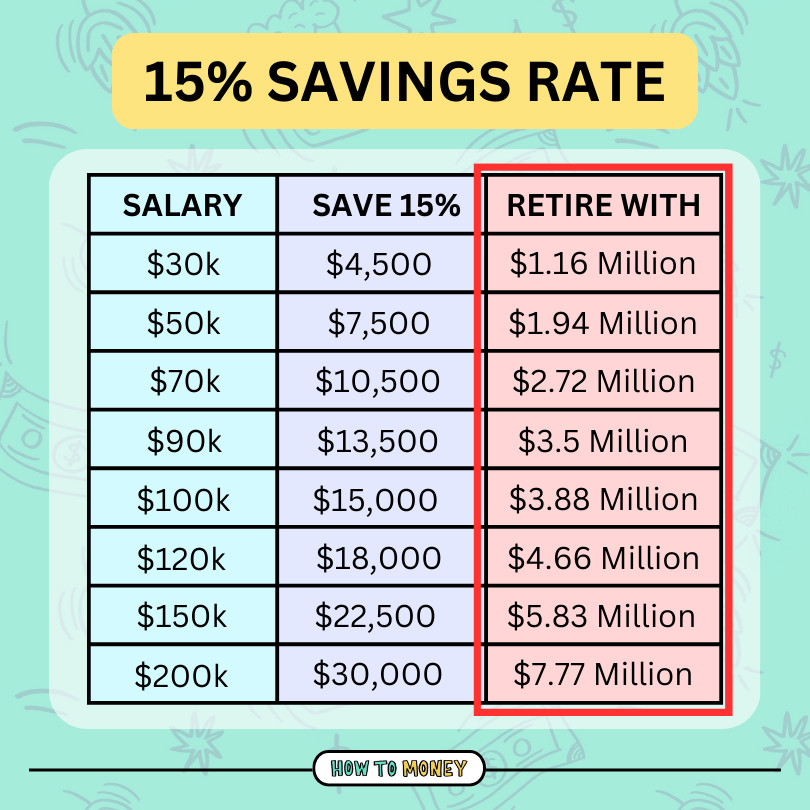

5. Increase Your Savings Rate

The only way to build wealth, regardless of income, is to spend less than you earn and invest the difference each month. You will never be able to increase your net worth if you spend more than you earn.

While it is certainly more difficult on a small income, it is possible to reduce your expenses to maintain a healthy savings rate. If possible, aim to save between 15-20% of your post-tax income each month. Allocate this money to debt payments, retirement contributions, or simply savings!

Here is what a 15% savings rate looks like for various income brackets. This assumes 40 working years and an investment growth rate of 8%.

It is entirely possible to build massive wealth with a small income, as you can see.

Do not worry if you cannot save that much of your income yet. There are numerous steps you can take to increase your savings rate. Remember that every percentage point counts and can make a significant difference over time.

Create A Budget

One of the reasons why most people are unable to save is that they consistently underestimate their expenses. The best way to stay on top of (and hopefully reduce) your expenses is to start budgeting.

If you have a lower income, it may be beneficial to begin with the 50/30/20 budgeting method. You will allocate 50% of your income to needs, 30% to wants, and 20% to savings, including investing, saving, and debt repayment under this budgeting technique.

Budgeting is also an excellent way to track your expenses. It is nearly impossible to manage your money effectively if you are unaware of where it is going. Tracking your expenses will allow you to determine which categories you are spending the most on. Sometimes, this knowledge can assist you in reducing purchases that do not necessarily make you happier.

Negotiate Bills

An easy way to free up more money for investment is to negotiate your bills. Unfortunately, the majority of our service providers do not reward us for being long-term customers.

Instead, they penalize us by raising prices without providing anything in return. That is why it is so important to advocate for yourself by calling and requesting a discount.

Set a date this month to spend an afternoon contacting companies such as your cable, internet, phone, and insurance providers and asking if there are any new customer offers available to you. If the customer service representative on the phone cannot assist you, request to speak with the customer retention department.

Now, here’s the deal. If you call to negotiate your bills, you must be prepared to walk away and switch providers if your requests are denied. While it may seem like a major inconvenience, it is typically less so than you anticipate.

And the savings can be substantial. Switching from a major phone company to one of these budget MVNOs, for example, can save you hundreds of dollars per year, which you can use to increase your savings.

Cancel Subscriptions

I want to preface this by stating that we are NOT one of those blogs that will tell you that you cannot afford a Netflix subscription until you have maxed out your 401(k).

Subscriptions can sometimes add value to our lives. For example, if you watch Netflix every weekend with your partner instead of going to the movie theater, you can save a lot of money. The problem arises when we continue to pay for subscriptions that we do not use regularly.

To put it in perspective, the average consumer spends $219 per month on subscriptions. Again, while we are not entirely opposed to subscriptions, it can be extremely wasteful if you are paying for services that you do not use frequently.

Instead, we propose that you alter the way you think about subscriptions. Instead of paying for them consistently, sign up for them when you actually intend to use them. For example, if a new season of your favorite show premieres on Hulu, subscribe, watch the show, and then cancel it until another show you wish to see premieres.

Limiting your subscriptions to 2-3 at a time can save you hundreds of dollars per year. Conduct a subscription audit every few months to keep track of those sneaky subscriptions that may be draining your bank account.

Change Your Lifestyle

Finally, you can make some significant lifestyle changes if you truly want to make dramatic cuts to your budget. For example, you could save approximately $9,282 per year by ditching one of your family cars. Or you could earn additional money by renting out a room in your home.

While not everyone can make significant changes immediately, it is worth noting that these more significant changes will have the most significant impact on your ability to build wealth.

Here is our master list of frugal hacks! Experiment with some of these this month to see what works for your lifestyle.

Work Towards Earning More

Finally, if you are working with a small income, there are steps you can take to maximize that income. Every small increase in pay can free up funds for wealth accumulation. Even changing jobs to earn 10% more can have a significant impact on your bottom line.

For example, if you currently earn $35,000 per year and change jobs to receive a 10% raise, you will earn an additional $3,500 that year before taxes. Even if you save half of that each year and invest it in a Roth IRA, you could have an additional $453,000 at retirement if you leave it invested for forty years.

If you want to try to earn more money, consider requesting a raise, changing jobs to get a more substantial pay increase, or starting a side hustle. You could also think about switching industries to earn more or furthering your education to advance your career.

Investing 15% of your paycheck

Investing 15% of your paycheck

6. Avoid These Wealth Killers

Now that you are earning more and spending less, you must protect those savings by avoiding these wealth killers at all costs.

High-Interest Debt

Do you recall how we stated that compound interest is the powerful force that can propel your investments to new heights? That same powerful force can also work against you when it comes to high-interest debt.

High-interest rates make it so difficult to escape the grasp of certain types of debt, such as credit card debt, personal loans, and payday loans. That is why it is so important that you pay off these debts as soon as possible and avoid them entirely in the future.

If you want to build wealth on a small income but still have high-interest rate debt, be sure to create a debt payoff plan and stick to it.

If you are drowning in debt, consider contacting a non-profit counseling organization such as Money Management International. They are free, helpful, and can help save your financial life.

Cars Are a Money Pit

We recognize that many people require automobiles to travel from point A to point B. We are not here to tell you that all driving is detrimental. However, you must comprehend the truth about car ownership, including all the hidden costs!

Did you know that the average monthly car payment for a new car is $725?!?!? This can significantly reduce your monthly budget for years. If you can find ways to reduce your car expenses, you can invest those funds in wealth accumulation instead!

The truth is that you do not require a fancy new car with all the bells and whistles, especially if you are attempting to increase your wealth on a low income.

There are numerous affordable and reliable used cars available for less than $10,000. Consider these instead of springing for something new. In addition, I find that purchasing a used car reduces stress over minor dings, dents, and scratches. Win-win situation!

We encourage you to find meaningful ways to reduce your transportation costs, whether that is walking to run errands each week, selling a more expensive car for a more affordable one, or ditching one of your cars entirely!

Living without a car is not difficult if you live in a walkable suburb or work from home.

Big Homes Slow Financial Progress

While homeownership can be a wise investment for many, it is not always the wisest financial choice. If you have a low income, you should exercise extra caution when selecting your housing. Purchasing a home may stretch you too thin financially, resulting in you becoming house poor.

Many homebuyers forget to consider the substantial costs of home maintenance, which can significantly strain your finances if you are unprepared.

If you want to buy a home, house hacking is an excellent way to accomplish that goal. A house hack occurs when you purchase a home to live in and then rent out a portion of it to help offset mortgage costs. You benefit from homeownership while saving more for the future.

Related: Pros and cons of renting vs. buying a home. This guide goes far beyond numbers, but in general, renting is currently less expensive than buying in most of the United States.

Risky Investing

There is a correct and an incorrect method of investing. If you are attempting to build wealth on a small income, you must protect your small flame as much as possible. Risking it all by stock picking or gambling with crypto is a surefire way to lose all of your money.

Stock pickers rarely outperform the S&P 500, one of the most well-known and basic index funds. It consists of the top 500 performing companies. In fact, the New York Times recently reported that not a single one of $2,132 actively managed funds (groups of professional stock-pickers) beat their index benchmark!

I promise you will be unable to do it if professionals on Wall Street cannot. Fortunately, there is a simpler way to invest that will guarantee your fair share of stock market growth, which is by investing in broad, low-cost index funds.

When investing within your 401(k) or IRA, ensure that you do so in low-cost index funds. These funds are comprised of numerous individual companies, allowing you to distribute your wealth across multiple baskets.

Certainly, some of them will fail miserably, resulting in financial loss. However, the others (the majority) will be extremely successful, and you will reap the benefits.

Do you require additional guidance on how to begin investing? Be sure to consult our beginner’s guide here!

Inflation

As previously stated, inflation can significantly impact your purchasing power from year to year, which is why you must take steps to hedge against it. While you may be more comfortable having more cash on hand, it is essential not to hold on to too much cash.

Remember that compound interest is the sidekick you will need to build wealth on a smaller income. Otherwise, inflation will diminish your savings and purchasing power.

Be sure to invest any savings beyond your emergency fund and short-term savings goals, such as a home down payment or automobile.

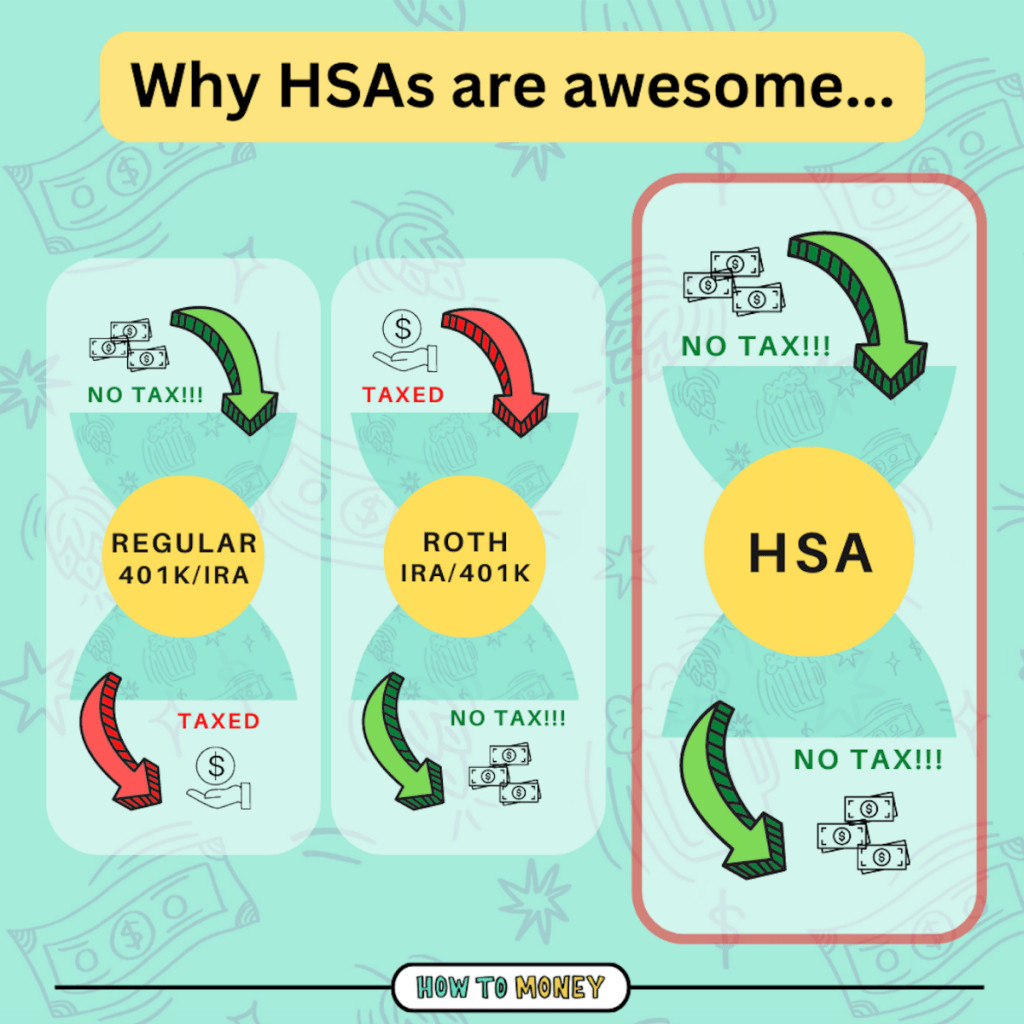

7. Use Tax Advantaged Accounts

We covered some of these earlier, but we cannot overstate the importance of tax-advantaged accounts (here are the ones you will want to prioritize if you do not have access to a 401k). They were created to assist people with lower incomes because the majority of Americans require additional motivation to save for retirement.

Investing in a 401(k) or Traditional IRA can help you lower your upfront taxable income if you want to invest more money now. This means you will have more money to invest now because less of your income will be subject to government taxation.

Deferring taxes allows your money to compound more quickly, resulting in faster growth over time. Just remember that when you withdraw this money in retirement, you will be required to pay taxes because you deferred tax when you contributed that cash.

However, you may want to stick with a Roth IRA if you have a low income and are in the 10% or 12% tax bracket. This means you will pay tax on that income now, but you will be able to withdraw it entirely tax-free in retirement. Because we assume that you will be in a lower tax bracket now than in retirement, you may save money overall when it comes to taxes.

Another excellent account is the Health Savings Account (HSA), which has a triple tax advantage! Contributions are tax-deductible upfront, and there is no tax when you withdraw the funds later for qualified health expenses.

Here is a quick visual overview of taxes in and out of these retirement accounts:

If you have a very low income, you may want to check to see if you qualify for the Savers Tax Credit. If you contribute to your retirement accounts, the government may significantly reduce your taxes for investing!

tax advantages retirement accounts

tax advantages retirement accounts

8. Automate Everything

It is a good idea to automate your finances if you want to accelerate your wealth-building progress, which eliminates the need to physically perform tasks such as transferring money to savings and making contributions to your investment accounts. Out of sight, out of mind!

After addressing all of the low-hanging financial fruit, the next step is automation. The objective is to instill wealth-building habits into your routine, thereby reducing the amount of stress you experience.

We want finances to take up less mental space as you go about your daily life. As long as you put in the hard work upfront and build the consistency, saving for your future and building wealth will become second nature.

A cool tool to consider using is an app called Empower (formerly Personal Capital). This app connects to all of your bank accounts and investment firms, assisting you in charting your financial growth over time.

Checking in every now and then to examine your overall financial situation will help confirm whether you are on track, and you will occasionally need to intervene and make adjustments.

9. Beware of Lifestyle Creep

While you may have a small income now, there is a good chance that your income will increase in the future. As your income increases, it is essential that you do not fall victim to lifestyle creep.

Lifestyle creep describes the phenomenon of spending more as you earn more. In other words, as your income increases, your expenses often rise to meet it.

For example, if someone receives a $5,000 raise, they may believe it is acceptable to spend $5,000 on a vacation that year. Nothing is lost or gained, correct?

Well, the truth is that after taxes, that vacation has just put them in the red. And they may become accustomed to spending that money and taking equally great vacations every year for the remainder of their lives.

Lifestyle creep, however, does not only apply to an increase in income. Sometimes, consumers are more likely to spend more even if their income and expenses remain constant because they feel more financially secure as their wealth increases and their portfolio expands. This is commonly referred to as the “Wealth Effect.”

To combat all of this, continue to track your expenses and note any consecutive months in which spending has increased. It is OK to spend a little more as your income increases, just ensure that you are saving more as well!

The ultimate win is increasing your income while keeping your expenses in check, which will help you build wealth at an accelerated rate.

The Bottom Line

While a great deal of traditional financial advice is geared toward average or high earners, we want to assure you that you do not need to earn six figures per year to accumulate substantial wealth. Money management is far more important than the number of zeros on a person’s paycheck.

By incorporating frugal habits into your daily routine, spending less than you earn, and investing the difference, you can build wealth on a small income. Remember that time, consistency, and compounding returns are your best allies.

Income-partners.net offers resources and tools to help individuals with low incomes find partners, develop strategies, and uncover opportunities to build wealth. Explore our website today to discover how you can begin your journey toward financial independence. Ready to take control of your financial future? Visit income-partners.net now and connect with the resources and partners you need to start building wealth, no matter your current income. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.

FAQ: Building Wealth with Low Income

- Is it truly possible to build wealth on a low income?

- Absolutely. It requires a shift in mindset, disciplined money management, and strategic investing.

- What’s the first step to building wealth on a low income?

- The first step is adopting a wealth-building mindset, believing that it’s possible to achieve financial success regardless of your current income.

- How important is it to understand the difference between saving and investing?

- It’s crucial. Saving protects money for specific goals, while investing grows it over time. Investing is essential to outpace inflation and build long-term wealth.

- Why is an emergency fund necessary, and how much should I save?

- An emergency fund protects against unexpected expenses without incurring debt. Aim to save 3-6 months’ worth of living expenses, but even $2,467 can cover most surprises.

- What’s the significance of starting to invest early?

- Time is a significant advantage. Starting early allows for the power of compounding to work its magic, requiring less monthly investment to reach your financial goals.

- Which investment accounts are best for beginners with a low income?

- Tax-advantaged accounts like 401(k)s (especially with employer matching) and Roth IRAs are excellent starting points.

- What does it mean to “pay yourself first,” and how does it help build wealth?

- It means prioritizing saving and investing by setting aside money at the beginning of each month, treating these as non-negotiable bills.

- How does increasing my savings rate impact wealth building?

- Increasing your savings rate is critical. Even small increases can lead to significant wealth accumulation over time.

- What are some common “wealth killers” to avoid?

- High-interest debt, overspending on cars and homes, risky investments, and ignoring the impact of inflation are common pitfalls to avoid.

- How can income-partners.net help me build wealth on a low income?

- income-partners.net provides resources, strategies, and partnership opportunities tailored for individuals with low incomes seeking to build wealth and achieve financial independence. Visit our website to explore our offerings and connect with potential partners.