How Much Withholding For Federal Income Tax should you pay? It’s a common question, and understanding how to calculate the correct amount is crucial for avoiding surprises at tax time, and income-partners.net can help. Our site provides resources and strategies to ensure your withholdings align with your tax obligations, potentially freeing up more of your earnings throughout the year. Explore income tax strategies and income tax liability on income-partners.net.

1. Understanding Paycheck Withholding for Federal Income Tax

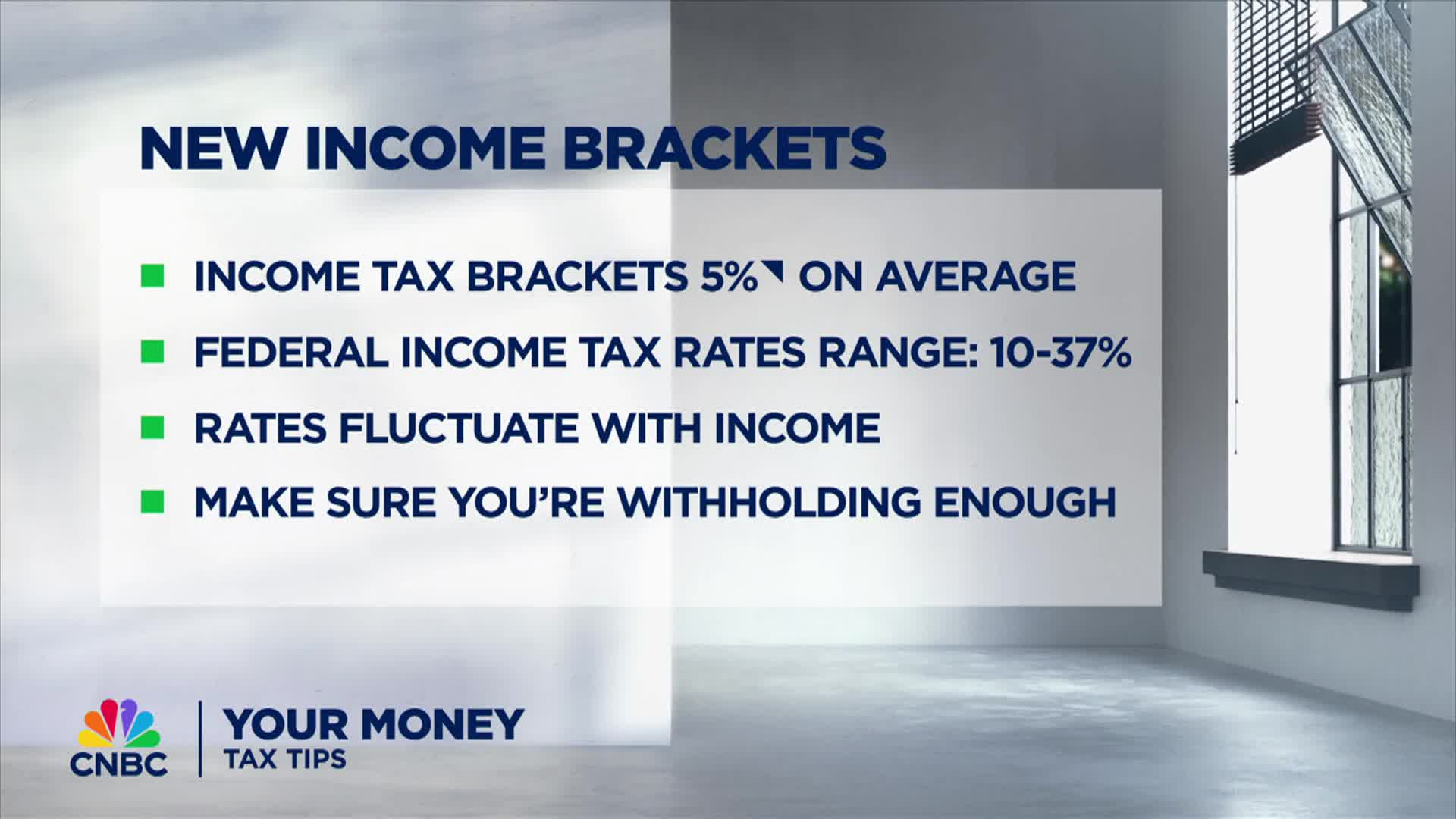

What is paycheck withholding for federal income tax, and why is it important? Paycheck withholding is the amount of federal income tax your employer deducts from each paycheck and remits to the Internal Revenue Service (IRS) on your behalf. Ensuring accurate withholding is essential because it directly impacts your tax liability at the end of the year. Underpaying can result in owing taxes, penalties, and interest, while overpaying leads to a larger refund, which means you’ve essentially given the government an interest-free loan of your money. Proper paycheck withholding helps you align your tax payments with your actual tax obligations, preventing financial surprises. The IRS provides resources and tools like Form W-4 and the Tax Withholding Estimator to help taxpayers determine the appropriate amount to withhold. Understanding the basics of paycheck withholding ensures financial stability and compliance with tax laws, which is a vital aspect of sound financial planning.

Key Factors Influencing Paycheck Withholding:

- Filing Status: Single, married filing jointly, head of household, etc.

- Number of Dependents: Claiming dependents can reduce your withholding.

- Tax Credits: Eligibility for tax credits can affect withholding amounts.

- Other Income: Income from sources other than your primary job.

- Deductions: Itemized deductions can reduce taxable income and withholding.

2. How to Calculate Your Federal Income Tax Withholding

How can you accurately calculate your federal income tax withholding? Calculating your federal income tax withholding involves several steps, starting with IRS Form W-4. This form collects information about your filing status, dependents, and other factors that affect your tax liability. Use the IRS Tax Withholding Estimator, an online tool that helps you estimate your income, deductions, and credits for the year. According to the IRS, using this estimator can significantly improve the accuracy of your withholding. After estimating your tax liability, divide that amount by the number of pay periods in the year to determine the amount to withhold from each paycheck. For example, if your estimated tax liability is $6,000 and you are paid bi-weekly (26 pay periods), you should withhold approximately $230.77 from each paycheck. Regularly review and adjust your withholding, especially when you experience life changes such as marriage, divorce, or the birth of a child. Keeping your withholding accurate prevents surprises at tax time and ensures you are neither underpaying nor overpaying your taxes.

Steps to Calculate Federal Income Tax Withholding:

- Complete Form W-4: Provide accurate information about your filing status, dependents, and other relevant factors.

- Use IRS Tax Withholding Estimator: Estimate your income, deductions, and credits for the year.

- Calculate Total Tax Liability: Determine your estimated total tax liability based on your income and deductions.

- Divide by Pay Periods: Divide your total tax liability by the number of pay periods in the year.

- Review and Adjust Regularly: Review and adjust your withholding as needed, especially when life changes occur.

3. The Importance of Form W-4 in Determining Withholding

Why is Form W-4 important for determining your federal income tax withholding? Form W-4, Employee’s Withholding Certificate, is crucial for determining the correct amount of federal income tax withheld from your paycheck because it provides your employer with the necessary information to calculate your withholding accurately. Completing this form carefully and accurately ensures that your tax withholdings align with your actual tax liability. According to the IRS, employees should review and update their W-4 whenever significant life changes occur, such as marriage, divorce, the birth of a child, or changes in income or deductions. Failing to update your W-4 can result in incorrect withholdings, leading to owing taxes or receiving a larger refund than expected. Accurate completion of Form W-4 helps prevent financial surprises at tax time. The form asks for your filing status, the number of dependents you claim, and any additional withholding you want to request. Using the IRS’s Tax Withholding Estimator in conjunction with Form W-4 can further improve the accuracy of your withholding. Ensuring your W-4 is up-to-date is a fundamental aspect of sound financial planning.

Key Sections of Form W-4:

- Personal Information: Name, address, and Social Security number.

- Filing Status: Single, married filing jointly, head of household, etc.

- Multiple Jobs or Spouse Works: Indicates if you have multiple jobs or if your spouse works.

- Claim Dependents: Information about dependents you plan to claim.

- Other Adjustments: Additional income, deductions, or extra withholding.

4. Common Mistakes to Avoid on Form W-4

What are some common mistakes to avoid when filling out Form W-4? Several common mistakes can lead to incorrect federal income tax withholding when completing Form W-4. One frequent error is failing to update the form after significant life changes, such as marriage, divorce, or the birth of a child. Another mistake is misunderstanding the instructions and incorrectly claiming dependents or deductions. The IRS emphasizes the importance of carefully reading and following the instructions provided with Form W-4 to avoid these errors. A further mistake is not accounting for income from other sources, such as self-employment or investment income, which can lead to underwithholding. To avoid these pitfalls, use the IRS Tax Withholding Estimator to accurately assess your tax liability and adjust your W-4 accordingly. Double-check all entries on the form before submitting it to your employer, and seek professional advice if you are unsure about any section. Avoiding these common mistakes ensures that your federal income tax withholdings accurately reflect your tax obligations.

Common Mistakes on Form W-4:

- Not Updating After Life Changes: Failing to update the form after marriage, divorce, or the birth of a child.

- Incorrectly Claiming Dependents: Misunderstanding the rules for claiming dependents.

- Ignoring Other Income: Not accounting for income from self-employment or investments.

- Misunderstanding Instructions: Failing to read and follow the instructions carefully.

- Not Using the IRS Estimator: Not using the IRS Tax Withholding Estimator to assess tax liability.

5. How Life Changes Impact Your Federal Income Tax Withholding

How do life changes affect your federal income tax withholding needs? Life changes, such as marriage, divorce, the birth of a child, or a new job, significantly impact your federal income tax withholding needs. When you marry, your filing status changes, which affects your tax bracket and standard deduction. A divorce also necessitates updating your filing status and may impact your eligibility for certain tax credits or deductions. The birth of a child introduces new dependents, potentially reducing your tax liability and requiring adjustments to your Form W-4. According to the IRS, updating your W-4 promptly after these life events is crucial to ensure accurate withholding. A new job or changes in income can also affect your tax bracket and overall tax liability. To accurately reflect these changes, use the IRS Tax Withholding Estimator to reassess your tax situation and adjust your W-4 accordingly. Keeping your withholding aligned with your current life circumstances helps avoid surprises at tax time and ensures you are neither underpaying nor overpaying your taxes.

Life Changes That Impact Withholding:

- Marriage: Changes filing status and standard deduction.

- Divorce: Requires updating filing status and may affect tax credits.

- Birth of a Child: Introduces new dependents and potential tax credits.

- New Job: Changes income and may affect tax bracket.

- Change in Income: Affects tax bracket and overall tax liability.

Completing Form W-4 for correct tax withholdings

Completing Form W-4 for correct tax withholdings

6. Strategies for Adjusting Your Federal Income Tax Withholding

What strategies can you use to adjust your federal income tax withholding? Several strategies can help you adjust your federal income tax withholding to better align with your tax liability. One effective approach is to use the IRS Tax Withholding Estimator, which provides personalized recommendations based on your income, deductions, and credits. If you have multiple jobs or sources of income, you may need to increase your withholding to cover your total tax liability. Another strategy is to adjust your itemized deductions or tax credits on Form W-4, which can reduce the amount of tax withheld from your paycheck. For instance, if you anticipate significant medical expenses or charitable contributions, you can include these on your W-4 to lower your withholding. According to financial advisors, regularly reviewing your withholding and making adjustments as needed is a proactive way to manage your tax obligations. Additionally, consider consulting a tax professional for personalized advice on optimizing your withholding strategy. Implementing these strategies ensures that your federal income tax withholdings accurately reflect your tax situation.

Strategies for Adjusting Withholding:

- Use IRS Tax Withholding Estimator: Obtain personalized recommendations.

- Adjust Itemized Deductions: Include anticipated deductions on Form W-4.

- Claim Tax Credits: Factor in tax credits to reduce withholding.

- Increase Withholding for Multiple Jobs: Ensure adequate withholding for all income sources.

- Consult a Tax Professional: Seek personalized advice on optimizing your withholding strategy.

7. Understanding Under Withholding Penalties

What are the penalties for under withholding federal income tax? Under withholding federal income tax can result in penalties imposed by the IRS. Generally, you can avoid penalties if you pay at least 90% of your tax liability for the current year or 100% of the tax shown on your return for the prior year, whichever is smaller. The IRS may also waive penalties for reasonable cause, such as a sudden and unexpected life event that prevented you from accurately estimating your tax liability. If you fail to meet these criteria, you may be subject to an underpayment penalty, which is calculated based on the amount of underpayment, the period during which it remained unpaid, and the applicable interest rate. According to the IRS, the penalty rate is determined quarterly and can vary. To avoid under withholding penalties, regularly review your withholding and adjust your Form W-4 as needed, especially when you experience changes in income or deductions. Using the IRS Tax Withholding Estimator can help you accurately estimate your tax liability and ensure you are withholding enough to avoid penalties. Understanding the rules and taking proactive steps to manage your withholding is essential for tax compliance.

Ways to Avoid Under Withholding Penalties:

- Pay 90% of Current Year Liability: Pay at least 90% of your tax liability for the current year.

- Pay 100% of Prior Year Liability: Pay 100% of the tax shown on your prior year’s return.

- Use IRS Tax Withholding Estimator: Accurately estimate your tax liability.

- Adjust Form W-4 Regularly: Review and update your W-4 as needed.

- Seek Penalty Waiver for Reasonable Cause: Request a waiver if underpayment was due to unforeseen circumstances.

8. The Role of Estimated Taxes for Self-Employed Individuals

How do estimated taxes work for self-employed individuals, and why are they important? Estimated taxes are crucial for self-employed individuals because they are not subject to regular paycheck withholdings like employees. Self-employed individuals must estimate their income and pay taxes on it throughout the year to avoid penalties. Estimated taxes cover not only income tax but also self-employment tax, which includes Social Security and Medicare taxes. The IRS requires self-employed individuals to pay estimated taxes quarterly, typically on April 15, June 15, September 15, and January 15. Accurately estimating your income and deductions is essential for calculating your estimated tax liability. According to the IRS, you can use Form 1040-ES to calculate and pay your estimated taxes. Failing to pay estimated taxes or underpaying them can result in penalties. To avoid these penalties, regularly review your income and expenses and adjust your estimated tax payments as needed. Utilizing accounting software or consulting a tax professional can help you accurately track your income and expenses and ensure you are meeting your estimated tax obligations.

Key Aspects of Estimated Taxes for Self-Employed Individuals:

- Quarterly Payments: Taxes are paid in four installments throughout the year.

- Form 1040-ES: Used to calculate and pay estimated taxes.

- Covers Income and Self-Employment Tax: Includes income tax, Social Security, and Medicare taxes.

- Avoid Penalties: Paying enough estimated tax prevents underpayment penalties.

- Regular Review: Review income and expenses regularly to adjust payments as needed.

9. How Tax Credits Affect Your Federal Income Tax Withholding

How do tax credits influence your federal income tax withholding requirements? Tax credits significantly influence your federal income tax withholding requirements by directly reducing your tax liability. A tax credit is a dollar-for-dollar reduction of the income tax you owe, which can substantially lower the amount you need to have withheld from your paycheck. For example, the Child Tax Credit can reduce your tax liability by up to $2,000 per qualifying child. The IRS allows you to account for tax credits when completing Form W-4, which can lower your withholding and increase your take-home pay. Accurately estimating your eligibility for tax credits and including this information on your W-4 is crucial for aligning your withholding with your actual tax obligations. According to tax experts, failing to account for tax credits can result in over withholding, leading to a larger refund than necessary. Regularly review your eligibility for various tax credits, such as the Earned Income Tax Credit, Child and Dependent Care Credit, and Education Credits, and adjust your W-4 accordingly. Properly accounting for tax credits can optimize your federal income tax withholding and improve your financial situation.

Common Tax Credits That Affect Withholding:

- Child Tax Credit: Reduces tax liability for each qualifying child.

- Earned Income Tax Credit (EITC): Benefits low- to moderate-income individuals and families.

- Child and Dependent Care Credit: Helps with expenses for childcare.

- Education Credits: For eligible students and parents paying for higher education.

- Energy Credits: For investments in energy-efficient home improvements.

10. The Impact of Itemized Deductions on Federal Income Tax Withholding

How do itemized deductions play a role in determining your federal income tax withholding? Itemized deductions play a significant role in determining your federal income tax withholding by reducing your taxable income, which in turn affects the amount of tax you owe. Itemized deductions include expenses such as medical expenses, state and local taxes (SALT), home mortgage interest, and charitable contributions. If your itemized deductions exceed the standard deduction for your filing status, you can reduce your taxable income by claiming these deductions on Schedule A of Form 1040. The IRS allows you to account for itemized deductions when completing Form W-4, which can lower your withholding and increase your take-home pay. Accurately estimating your itemized deductions and including this information on your W-4 is crucial for aligning your withholding with your actual tax obligations. According to financial advisors, failing to account for itemized deductions can result in over withholding, leading to a larger refund than necessary. Regularly review your potential itemized deductions and adjust your W-4 accordingly to optimize your federal income tax withholding and improve your financial situation.

Common Itemized Deductions:

- Medical Expenses: Expenses exceeding 7.5% of adjusted gross income (AGI).

- State and Local Taxes (SALT): Limited to $10,000 per household.

- Home Mortgage Interest: Interest paid on a home mortgage.

- Charitable Contributions: Donations to qualified charitable organizations.

- Casualty and Theft Losses: Losses from federally declared disasters.

By understanding how much withholding for federal income tax you should pay, you can avoid surprises at tax time. Using the IRS resources and consulting with tax professionals can help ensure you are withholding the correct amount.

Are you looking for partners to expand your business and increase your revenue? Visit income-partners.net to discover various partnership opportunities, build effective relationships, and explore strategies to maximize your income. Our platform offers resources to help you find the right partners, negotiate beneficial agreements, and manage long-term relationships. Don’t miss out on potential collaborations—explore income-partners.net today and start building profitable partnerships!

FAQ: Federal Income Tax Withholding

1. What is federal income tax withholding?

Federal income tax withholding is the amount of money your employer deducts from your paycheck to pay your federal income taxes.

2. Why is it important to have accurate federal income tax withholding?

Accurate withholding ensures you neither underpay nor overpay your taxes, avoiding penalties or large refunds.

3. How do I determine the correct amount to withhold?

Use IRS Form W-4 and the IRS Tax Withholding Estimator to calculate your tax liability.

4. What is Form W-4, and how does it affect my withholding?

Form W-4 tells your employer how much to withhold from your paycheck based on your filing status, dependents, and other factors.

5. How often should I review my federal income tax withholding?

Review your withholding annually or whenever significant life changes occur, such as marriage, divorce, or the birth of a child.

6. What are the penalties for under withholding federal income tax?

Penalties may be imposed if you pay less than 90% of your current year’s tax liability or 100% of the prior year’s tax liability.

7. How do tax credits affect my federal income tax withholding?

Tax credits directly reduce your tax liability, lowering the amount you need to withhold from your paycheck.

8. What are estimated taxes, and who needs to pay them?

Estimated taxes are payments made by self-employed individuals who are not subject to regular paycheck withholdings.

9. How do itemized deductions impact my federal income tax withholding?

Itemized deductions reduce your taxable income, which in turn affects the amount of tax you owe and the amount withheld.

10. Where can I find more information about federal income tax withholding?

Visit the IRS website or consult a tax professional for detailed information and personalized advice.