How Much Tax Should I Pay On Rental Income? Accurately calculating and paying taxes on rental income is crucial for real estate investors looking to optimize their financial strategies and increase profitability. Income-partners.net is here to help you navigate these complexities. We will explore the ins and outs of rental income taxation to help you optimize your financial strategy and explore various tax-saving strategies, including deductions, depreciation, and Qualified Business Income (QBI) to maximize your return on investment. You’ll gain a better understanding of how to report rental income and expenses, minimize your tax liabilities, and make informed financial decisions. Let’s explore the essentials of rental property taxation, including deductions, tax rates, and reporting to help you optimize your financial strategy and explore various tax-saving strategies, including deductions, depreciation, and Qualified Business Income (QBI) to maximize your return on investment and partnership opportunities.

1. Understanding Rental Income Taxation

What is the Basic Principle of Rental Income Tax?

Rental income is generally taxed as ordinary income at the federal level and may also be subject to state income taxes, depending on the state you reside in. This income must be reported in full, with the potential to offset it with eligible deductions, so, the key is to keep detailed records of all rental income and expenses.

According to the IRS, rental income includes all payments received for the use or occupancy of a property. This isn’t limited to just rent; it also encompasses advanced rent payments, tenant fees (like late or pet fees), non-refundable security deposits you keep, and even expenses tenants pay on your behalf.

1.1 What Components Constitute Taxable Rental Income?

Taxable rental income comprises more than just the rent collected, it includes all income streams associated with the rental property.

Here are key components:

- Rent Payments: This is the primary source of income, including all regular rent payments received from tenants.

- Advanced Rent: Any rent received in advance for future periods is also considered taxable income in the year it is received.

- Tenant Fees: Income from late fees, pet fees, and other charges tenants pay.

- Security Deposits: Non-refundable security deposits kept by the landlord are considered income.

- Tenant-Paid Expenses: Payments made by tenants for expenses that would typically be the landlord’s responsibility.

- Services in Lieu of Rent: If a tenant provides services instead of rent, the fair market value of those services is taxable income.

For instance, if a tenant offers gardening services in exchange for reduced rent, the value of those services is considered part of your rental income.

1.2 How Do Federal Income Tax Brackets Impact Rental Income?

The tax bracket you fall into will determine the amount of tax you pay on your rental income. The U.S. has a progressive tax system with seven federal income tax brackets, ranging from 10% to 37%. Your filing status and taxable income determine your tax bracket.

Here’s a look at the 2024 and 2023 income tax brackets:

2024 Income Tax Brackets (Taxes due April 2025)

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 37% | $609,351+ | $731,201+ |

| 35% | $243,726 – $609,350 | $487,451 – $731,200 |

| 32% | $191,951 – $243,725 | $383,901 – $487,450 |

| 24% | $100,526 – $191,950 | $201,051 – $383,900 |

| 22% | $47,151 – $100,525 | $94,301 – $201,050 |

| 12% | $11,601 – $47,150 | $23,201 – $94,300 |

| 10% | Up to $11,600 | Up to $23,200 |

2023 Income Tax Brackets (Taxes due April 2024, extension by October 15th)

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 37% | $578,126+ | $693,751+ |

| 35% | $231,251 – $578,125 | $462,501 – $693,750 |

| 32% | $182,101 – $231,250 | $364,201 – $462,500 |

| 24% | $95,376 – $182,100 | $190,751 – $364,200 |

| 22% | $44,726 – $95,375 | $89,451 – $190,750 |

| 12% | $11,001 – $44,725 | $22,001 – $89,450 |

| 10% | Up to $11,000 | Up to $22,000 |

The tax bracket dictates the percentage of your income that will be taxed. A clear understanding of these brackets is critical for tax planning.

1.3 Do State Taxes on Rental Income Differ?

Yes, state taxes on rental income can vary significantly. Some states have no income tax, while others have progressive or flat tax systems. It’s important to understand the specific tax laws in the state where your rental property is located.

Here’s how different states treat rental income tax:

- States with No Income Tax: States like Texas, Florida, and Nevada do not have state income taxes, which can be a significant advantage for landlords.

- States with Progressive Income Tax: Many states have a progressive income tax system similar to the federal system, where tax rates increase with income. Examples include California and New York.

- States with Flat Income Tax: Some states, like Pennsylvania, have a flat income tax rate, meaning everyone pays the same percentage regardless of income level.

Understanding these state-specific tax laws is essential for accurate tax planning.

1.4 What is Schedule E, and Who Should File It?

Schedule E (Form 1040), Supplemental Income and Loss, is the form used to report rental income and expenses to the IRS. It is used by individuals who receive income from rental properties, royalties, partnerships, S corporations, estates, and trusts.

The key sections of Schedule E include:

- Income Section: Reports all rental income received during the tax year.

- Expense Section: Lists all deductible expenses associated with the rental property.

- Depreciation Section: Calculates and reports depreciation expenses.

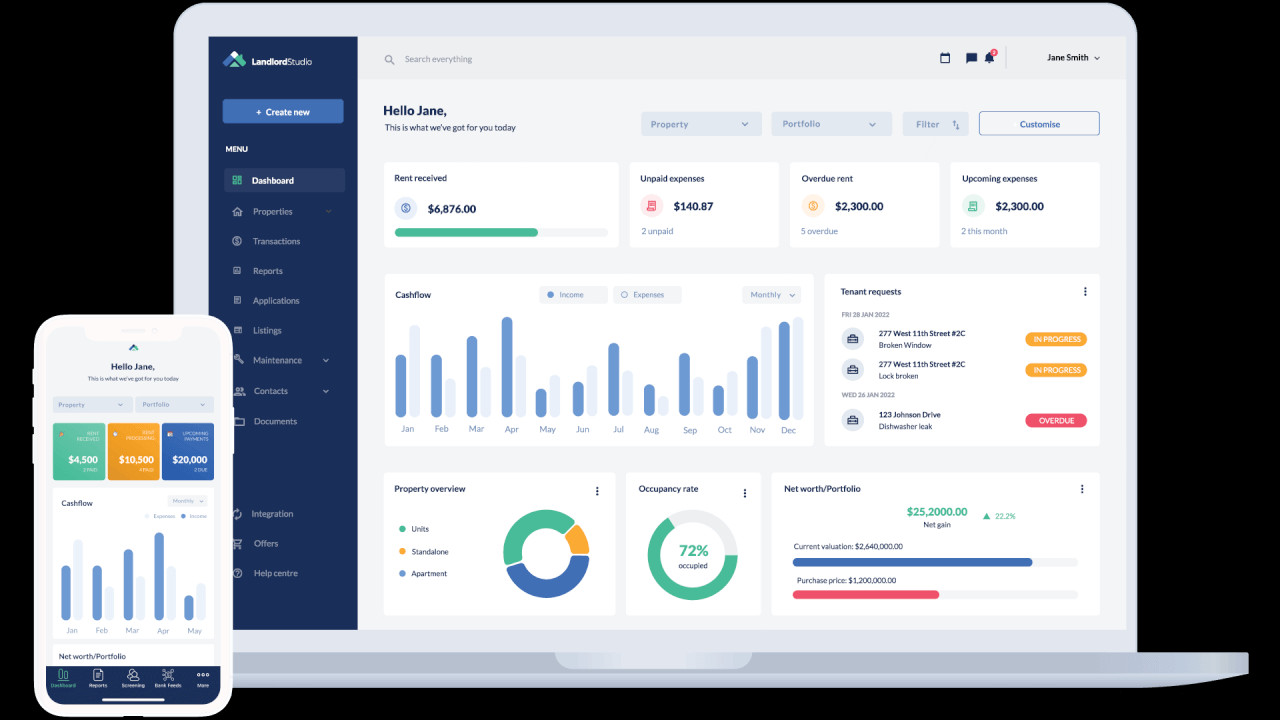

Completing Schedule E accurately requires detailed record-keeping of all income and expenses related to your rental properties. Using property management software like Landlord Studio can greatly simplify this process.

Rental property accounting screenshot

Rental property accounting screenshot

Rental property accounting screenshot

2. Maximizing Deductions for Rental Properties

How Can Deductions Lower My Rental Income Tax?

Deductions are expenses that can be subtracted from your gross rental income to reduce your taxable income. By claiming all eligible deductions, you can significantly lower the amount of tax you owe.

Tracking all expenses throughout the year is crucial to maximize your deductions. Here are some common deductions.

2.1 What Common Rental Property Expenses Are Tax Deductible?

Many expenses related to managing and maintaining your rental property are deductible.

These include:

- Advertising: Costs associated with advertising your rental property.

- Insurance: Premiums paid for property, liability, and other insurance policies.

- Mortgage Interest: Interest paid on the mortgage for the rental property.

- Property Taxes: Real estate taxes paid on the rental property.

- Repairs and Maintenance: Costs for repairs and maintenance to keep the property in good condition.

- Property Management Fees: Fees paid to a property management company.

- Utilities: Costs for utilities paid by the landlord.

- Homeowner Association (HOA) Dues: Fees paid to the HOA.

- Professional Fees: Payments for legal, accounting, and other professional services.

2.2 How Does Mortgage Interest Deduction Work?

Mortgage interest is a significant deductible expense for rental property owners. The interest you pay on your mortgage can be deducted from your rental income, reducing your taxable income.

2.3 What is the Difference Between Repairs and Improvements?

Repairs and improvements are both related to maintaining a rental property, but they are treated differently for tax purposes. Repairs are expenses that maintain the property in its current condition, while improvements add value or extend the life of the property.

- Repairs: Deductible in the year they are incurred. Examples include fixing a leaky faucet or painting a wall.

- Improvements: Must be capitalized and depreciated over several years. Examples include adding a new roof or installing central air conditioning.

2.4 How Can I Deduct Depreciation?

Depreciation is a method of deducting the cost of an asset over its useful life. For residential rental properties, the IRS typically assigns a useful life of 27.5 years. You can deduct a portion of the property’s cost each year.

To calculate the annual depreciation expense:

- Determine the Basis: Calculate the property’s basis, which is typically the purchase price plus any improvements, minus the value of the land.

- Divide by Useful Life: Divide the basis by 27.5 years to determine the annual depreciation expense.

Depreciation allows you to deduct a portion of the property’s cost each year, significantly lowering your taxable income.

2.5 How Does Qualified Business Income (QBI) Deduction Apply to Rental Income?

The Qualified Business Income (QBI) deduction allows eligible self-employed and small business owners to deduct up to 20% of their qualified business income. For rental property owners, this deduction can be a valuable tax-saving tool.

To qualify for the QBI deduction:

- Determine Eligibility: Ensure that your rental activities are classified as business activities.

- Calculate QBI: Determine your qualified business income from the rental property.

- Apply the Deduction: Deduct up to 20% of your QBI, subject to certain limitations based on your total taxable income.

In 2023, the total taxable income must be under $364,200 for those married filing jointly or under $182,10 for single filers. Rental services that constitute business activities include property management, tenant screening, rent collection, and property maintenance.

2.6 What Records Should I Keep to Support My Deductions?

Maintaining detailed and accurate records is crucial to support your deductions and ensure compliance with IRS regulations.

Keep the following records:

- Receipts: Keep receipts for all expenses related to the rental property.

- Invoices: Save invoices for repairs, maintenance, and other services.

- Bank Statements: Retain bank statements showing payments for rental-related expenses.

- Mortgage Statements: Keep mortgage statements showing interest paid.

- Property Tax Records: Save property tax records showing taxes paid.

- Lease Agreements: Maintain copies of lease agreements with tenants.

Keeping these records organized will make tax preparation easier and help you substantiate your deductions if audited.

3. Reporting Rental Income and Expenses

How Do I Accurately Report Rental Income and Expenses?

Accurately reporting rental income and expenses is essential for tax compliance. Use Schedule E (Form 1040) to report all rental income and deductible expenses.

Here’s a step-by-step guide:

3.1 What Forms Do I Need to Report Rental Income?

Several forms may be required to report rental income, depending on your specific circumstances.

The most common forms include:

- Schedule E (Form 1040): Used to report rental income and expenses.

- Schedule A (Form 1040): Used to deduct personal expenses related to the rental property.

- Form 4562: Used to report depreciation and amortization.

- Form 8960: Used to calculate net investment income tax, if applicable.

- Form 1099: Required if you have paid any contractors over $600 during the tax year.

3.2 How to Fill Out Schedule E

Completing Schedule E accurately requires detailed record-keeping and a thorough understanding of rental income and expenses.

Follow these steps:

- Gather Your Records: Collect all records of rental income and expenses, including receipts, invoices, and bank statements.

- Report Rental Income: Enter the total rental income received during the tax year.

- List Deductible Expenses: Itemize all deductible expenses, such as mortgage interest, property taxes, insurance, and repairs.

- Calculate Depreciation: Calculate and report depreciation expenses using Form 4562.

- Determine Net Rental Income: Subtract total expenses from total income to determine your net rental income or loss.

- File with Form 1040: Attach Schedule E to your Form 1040 and submit it with your tax return.

3.3 How Does Passive Activity Loss Rule Affect Rental Income?

The passive activity loss rule limits the amount of losses you can deduct from passive activities, such as rental properties. A passive activity is defined as a business in which you do not materially participate.

Under the passive activity loss rule:

- Losses are Limited: Losses from passive activities can only be deducted up to the amount of income from other passive activities.

- Carryforward Losses: Any losses that cannot be deducted in the current year can be carried forward to future years.

- Real Estate Professionals: Real estate professionals may be exempt from the passive activity loss rule if they meet certain requirements, such as spending more than 750 hours per year on real estate activities.

Consult with a tax professional to determine how the passive activity loss rule affects your rental income.

3.4 Do I Need to Pay Estimated Taxes on Rental Income?

If you expect to owe $1,000 or more in taxes, you may need to pay estimated taxes on your rental income. Estimated taxes are quarterly payments made to the IRS to cover your tax liability.

To determine if you need to pay estimated taxes:

- Calculate Expected Income: Estimate your expected rental income for the year.

- Estimate Deductions: Estimate your deductible expenses.

- Determine Tax Liability: Calculate your expected tax liability based on your income and deductions.

- Make Quarterly Payments: If you expect to owe $1,000 or more, make quarterly estimated tax payments to the IRS.

Paying estimated taxes can help you avoid penalties and interest charges at the end of the tax year.

3.5 What Happens if I Have a Net Rental Loss?

If your deductible expenses exceed your rental income, you may have a net rental loss. This loss can be used to offset other income, subject to certain limitations.

If you have a net rental loss:

- Deductible Up to $25,000: You may be able to deduct up to $25,000 of rental losses if your adjusted gross income is $100,000 or less.

- Phase-Out Range: The $25,000 deduction is phased out for adjusted gross incomes between $100,000 and $150,000.

- Carryforward Losses: Any losses that cannot be deducted in the current year can be carried forward to future years.

The ability to deduct rental losses can provide significant tax relief.

4. Tax Planning Strategies for Rental Property Owners

What Tax Planning Strategies Can I Use to Minimize My Tax Liability?

Effective tax planning can help you minimize your tax liability and maximize your return on investment.

Here are some strategies to consider:

4.1 How Can Cost Segregation Studies Benefit Me?

A cost segregation study is a detailed analysis that identifies and reclassifies property components to shorten their depreciation periods. By accelerating depreciation, you can increase your deductions and reduce your tax liability in the early years of ownership.

Cost segregation studies can:

- Accelerate Depreciation: Identify assets that can be depreciated over shorter periods.

- Increase Deductions: Increase your deductions in the early years of ownership.

- Reduce Tax Liability: Reduce your overall tax liability.

4.2 What is the 1031 Exchange, and How Does It Work?

A 1031 exchange allows you to defer capital gains taxes when selling a rental property and reinvesting the proceeds into a like-kind property. This can be a powerful tool for building wealth through real estate.

To qualify for a 1031 exchange:

- Identify a Replacement Property: Identify a like-kind replacement property within 45 days of selling the relinquished property.

- Complete the Exchange: Complete the exchange within 180 days of selling the relinquished property.

- Reinvest Proceeds: Reinvest all proceeds from the sale into the replacement property.

4.3 How Can I Use a Self-Directed IRA to Invest in Real Estate?

A self-directed IRA allows you to invest in real estate and other alternative assets, providing tax-deferred or tax-free growth. Rental income earned within a self-directed IRA is typically tax-deferred or tax-free.

To invest in real estate with a self-directed IRA:

- Open a Self-Directed IRA: Open a self-directed IRA account with a custodian that allows real estate investments.

- Fund the Account: Transfer funds from an existing IRA or make contributions to the account.

- Purchase Real Estate: Use the funds in the IRA to purchase a rental property.

4.4 What Are the Benefits of Forming an LLC for My Rental Property?

Forming a Limited Liability Company (LLC) can provide several benefits for rental property owners, including liability protection and potential tax advantages.

Benefits of forming an LLC include:

- Liability Protection: Protects your personal assets from lawsuits and liabilities related to the rental property.

- Tax Flexibility: Offers flexibility in how the rental income is taxed.

- Credibility: Enhances your credibility as a business owner.

4.5 How Can I Plan for the Long Term to Minimize Taxes?

Long-term tax planning involves strategies to minimize taxes over the life of your rental property ownership.

These strategies include:

- Regularly Review Your Tax Situation: Review your tax situation annually with a tax professional.

- Keep Accurate Records: Maintain detailed and accurate records of all income and expenses.

- Take Advantage of Tax-Advantaged Accounts: Use tax-advantaged accounts, such as self-directed IRAs, to invest in real estate.

- Consider a 1031 Exchange: Defer capital gains taxes when selling and reinvesting in like-kind properties.

Effective long-term tax planning can help you build wealth and minimize your tax burden.

Rental property investment

Rental property investment

5. Seeking Professional Advice

When Should I Consult a Tax Professional?

Consulting a tax professional is highly recommended to ensure you accurately navigate the complexities of rental income taxation. A tax professional can provide personalized advice based on your financial situation.

Here are scenarios when you should seek professional advice:

5.1 What Questions Should I Ask a Tax Advisor?

When consulting a tax advisor, it’s important to ask specific questions to get the most relevant advice.

Here are key questions to ask:

- What deductions am I eligible for?

- How can I optimize my depreciation deductions?

- How does the passive activity loss rule affect me?

- Do I need to pay estimated taxes?

- What are the tax implications of forming an LLC?

- Can a cost segregation study benefit me?

- What is the 1031 exchange, and how does it work?

- How can I use a self-directed IRA to invest in real estate?

5.2 How to Find a Qualified Tax Professional

Finding a qualified tax professional is essential for accurate tax planning and compliance.

Here are steps to take:

- Seek Referrals: Ask friends, family, or colleagues for referrals.

- Check Credentials: Verify the tax professional’s credentials, such as CPA or Enrolled Agent.

- Review Experience: Review the tax professional’s experience in rental property taxation.

- Consider Specializations: Look for tax professionals who specialize in real estate or small business taxation.

5.3 What are the Benefits of Using Property Management Software for Tax Purposes?

Property management software, such as Landlord Studio, can greatly simplify tax preparation by automating income and expense tracking, generating reports, and providing a clear overview of your financial performance.

Benefits of using property management software include:

- Automated Tracking: Automatically track income and expenses.

- Detailed Reports: Generate detailed reports for tax preparation.

- Easy Record-Keeping: Easily keep records of receipts, invoices, and other documents.

- Time Savings: Save time on tax preparation and reporting.

6. Real-World Examples and Case Studies

Can You Provide Some Examples of How These Concepts Apply in Practice?

Understanding real-world examples and case studies can help illustrate how these concepts apply in practice.

Here are a few examples:

6.1 Case Study: Maximizing Deductions for a Single-Family Rental

- Scenario: John owns a single-family rental property and wants to maximize his deductions.

- Strategy: John diligently tracks all expenses, including mortgage interest, property taxes, insurance, repairs, and property management fees.

- Outcome: By claiming all eligible deductions, John reduces his taxable income by $15,000, resulting in a lower tax liability.

6.2 Example: Using Depreciation to Reduce Taxable Income

- Scenario: Sarah owns a rental property with a basis of $275,000.

- Strategy: Sarah calculates her annual depreciation expense by dividing the basis by 27.5 years.

- Outcome: Sarah deducts $10,000 each year for depreciation, significantly lowering her taxable income.

6.3 Example: Deferring Taxes with a 1031 Exchange

- Scenario: Michael sells a rental property for $500,000 and wants to defer capital gains taxes.

- Strategy: Michael completes a 1031 exchange by reinvesting the proceeds into a like-kind property within 180 days.

- Outcome: Michael defers paying capital gains taxes and continues to build wealth through real estate.

7. Common Mistakes to Avoid

What Common Mistakes Do Landlords Make When Filing Taxes, and How Can I Avoid Them?

Avoiding common mistakes is crucial for accurate tax compliance and minimizing your tax liability.

Here are some mistakes to avoid:

7.1 Not Keeping Accurate Records

- Mistake: Failing to keep accurate records of income and expenses.

- Solution: Use property management software or a detailed spreadsheet to track all transactions.

7.2 Missing Deductions

- Mistake: Overlooking eligible deductions, such as mortgage interest, property taxes, and repairs.

- Solution: Review all eligible deductions and keep receipts for all expenses.

7.3 Incorrectly Classifying Expenses

- Mistake: Misclassifying expenses, such as treating improvements as repairs.

- Solution: Understand the difference between repairs and improvements and classify expenses accordingly.

7.4 Failing to Report All Income

- Mistake: Failing to report all income, including rent payments, late fees, and other charges.

- Solution: Keep detailed records of all income and report it accurately on Schedule E.

7.5 Not Seeking Professional Advice

- Mistake: Not consulting a tax professional for personalized advice.

- Solution: Consult a tax professional to ensure you accurately navigate the complexities of rental income taxation.

8. Staying Updated on Tax Law Changes

How Do I Stay Informed About Changes in Tax Laws That Could Affect My Rental Income?

Staying updated on tax law changes is essential for compliance and effective tax planning.

Here are ways to stay informed:

8.1 Subscribing to IRS Updates

- Strategy: Subscribe to IRS updates and newsletters to receive the latest information on tax law changes.

- Outcome: Stay informed about changes that could affect your rental income.

8.2 Following Industry Publications

- Strategy: Follow industry publications and websites that provide updates on tax laws and regulations.

- Outcome: Stay informed about changes that could affect your rental income.

8.3 Attending Seminars and Webinars

- Strategy: Attend seminars and webinars on tax law changes and strategies for rental property owners.

- Outcome: Gain insights from experts and stay informed about the latest developments.

8.4 Consulting with a Tax Professional

- Strategy: Consult with a tax professional regularly to discuss changes in tax laws and how they affect your situation.

- Outcome: Receive personalized advice and stay compliant with tax regulations.

9. Leveraging Income-Partners.net for Partnership Opportunities

How Can Income-Partners.net Assist in My Rental Income Endeavors?

Income-partners.net can play a pivotal role in enhancing your rental income strategies. It offers a platform to connect with potential partners who can bring diverse skills and resources to your rental property business.

Income-partners.net provides:

- Access to a Network of Professionals: Connect with property managers, contractors, and other real estate professionals who can help you optimize your rental operations.

- Potential Joint Venture Opportunities: Find partners for joint ventures, enabling you to expand your portfolio and share the risks and rewards of rental property ownership.

- Expert Insights and Advice: Access articles, webinars, and other resources that provide valuable insights into rental property management and taxation.

Income-partners.net helps you build a robust network, identify lucrative opportunities, and stay informed about best practices in the rental property industry.

10. Call to Action

Ready to take control of your rental income taxes and unlock new partnership opportunities? Visit income-partners.net today to explore a wealth of resources, connect with potential partners, and discover strategies to maximize your returns. Whether you’re looking for expert tax advice, property management solutions, or joint venture prospects, income-partners.net is your go-to platform for success. Start building your network, optimizing your tax planning, and achieving your rental income goals today.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434

Website: income-partners.net

Frequently Asked Questions (FAQ)

Have Questions About Rental Income Taxes? We’ve Got Answers.

1. What is considered rental income for tax purposes?

Rental income includes all payments you receive for the use or occupancy of a property. This includes regular rent payments, advanced rent, tenant fees, non-refundable security deposits, and expenses paid by tenants on your behalf.

2. How do I report rental income on my tax return?

You report rental income on Schedule E (Form 1040), Supplemental Income and Loss. You list all rental income and deductible expenses on this form and attach it to your Form 1040.

3. What expenses can I deduct from my rental income?

Common deductible expenses include mortgage interest, property taxes, insurance, repairs, maintenance, property management fees, utilities, advertising, and depreciation.

4. How does depreciation work for rental properties?

Depreciation allows you to deduct a portion of the property’s cost each year over its useful life, typically 27.5 years for residential rental properties. You calculate the annual depreciation expense by dividing the property’s basis by 27.5.

5. What is the Qualified Business Income (QBI) deduction, and how does it apply to rental income?

The QBI deduction allows eligible self-employed and small business owners to deduct up to 20% of their qualified business income. For rental property owners, this deduction can be a valuable tax-saving tool if their rental activities are classified as business activities.

6. Do I need to pay estimated taxes on rental income?

If you expect to owe $1,000 or more in taxes, you may need to pay estimated taxes on your rental income. Estimated taxes are quarterly payments made to the IRS to cover your tax liability.

7. What is a 1031 exchange, and how does it work?

A 1031 exchange allows you to defer capital gains taxes when selling a rental property and reinvesting the proceeds into a like-kind property.

8. How can forming an LLC benefit my rental property business?

Forming a Limited Liability Company (LLC) can provide several benefits, including liability protection and potential tax advantages. It protects your personal assets from lawsuits and liabilities related to the rental property.

9. How can property management software help with tax preparation?

Property management software automates income and expense tracking, generates detailed reports, and provides a clear overview of your financial performance, making tax preparation easier and more efficient.

10. When should I consult a tax professional for rental income advice?

Consulting a tax professional is recommended to ensure you accurately navigate the complexities of rental income taxation and receive personalized advice based on your financial situation. They can help you identify eligible deductions, optimize depreciation, and stay compliant with tax laws.