How Much Should Your Car Payment Be Compared To Income? Ideally, your car payment should not exceed 10-15% of your monthly take-home pay, ensuring financial stability and flexibility, and this is just a part of overall financial health. At income-partners.net, we help you discover how to strategically manage your car expenses, align them with your income, and explore opportunities for partnership to boost your financial well-being. By optimizing your spending and seeking collaborative ventures, you can achieve a balanced budget and unlock new income streams.

1. Understanding the Golden Ratio: Car Payment vs. Income

What’s the sweet spot for your car payment relative to your income? Your monthly car payment should ideally stay within 10% to 15% of your net monthly income (after taxes), as exceeding this range can strain your budget, limiting your ability to save, invest, or handle unexpected expenses. According to financial experts at the University of Texas at Austin’s McCombs School of Business, a balanced approach to car financing is crucial for long-term financial health. Staying within this range ensures you’re not overextending yourself and allows for a more comfortable financial cushion.

1.1 Why This Ratio Matters

Why is this percentage so important? Sticking to the 10-15% rule ensures you’re not allocating too much of your income to a depreciating asset. This allows you to maintain a healthy financial portfolio, capable of handling emergencies, investments, and other financial goals. Neglecting this balance can lead to financial stress and limited opportunities for wealth-building.

1.2 What to Include in Your Car Payment Calculation

What exactly counts as part of your car payment? Your car payment isn’t just the principal and interest on your loan. It also includes car insurance premiums, fuel costs, and routine maintenance. Factoring in all these expenses provides a more accurate picture of the true cost of owning a vehicle, helping you make a more informed financial decision.

Car payment due date

Car payment due date

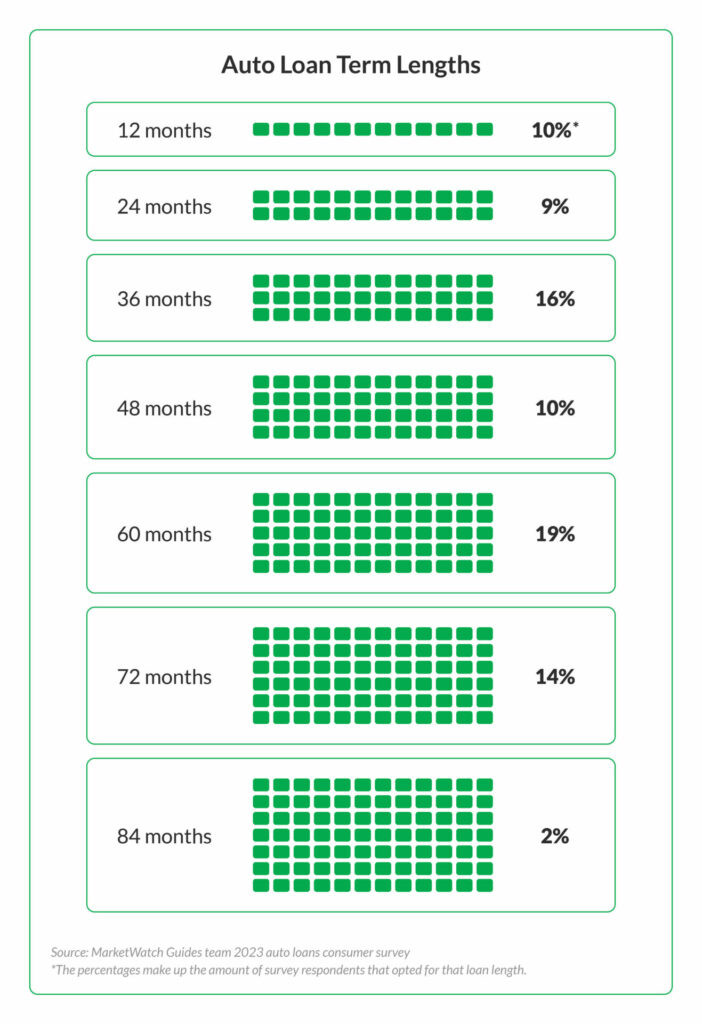

Alt text: Infographic showing the distribution of auto loan term lengths among car owners, highlighting the percentage of individuals opting for various durations.

2. Calculating Your Affordable Car Payment: A Step-by-Step Guide

How can you determine your personal car payment limit? To calculate how much you can comfortably afford for a car payment, start by assessing your monthly take-home pay, then subtract all fixed expenses and savings goals, and finally allocate 10-15% of the remaining amount to your car budget, ensuring you have enough for other financial priorities. This calculation provides a realistic view of your affordability.

2.1 Step 1: Determine Your Net Income

What’s the first step in figuring out your car budget? Start by calculating your net monthly income, which is your income after taxes and other deductions. This figure represents the actual amount you have available to spend each month. Knowing your net income provides a clear foundation for budgeting your car payment.

2.2 Step 2: List Your Monthly Expenses

What expenses should you consider when creating your budget? Account for all fixed monthly expenses, such as rent or mortgage, utilities, groceries, loan payments, and other recurring bills. Identifying these essential expenses will help you determine how much discretionary income you have left for a car payment.

2.3 Step 3: Factor in Savings and Investments

Why is it important to consider savings and investments? Before deciding on a car payment amount, allocate funds for your savings goals (emergency fund, down payment for a house, etc.) and investment contributions. Prioritizing savings and investments ensures you’re building a secure financial future while still addressing your transportation needs.

2.4 Step 4: Calculate Your Car Payment Range

How do you determine the actual car payment amount? After accounting for all expenses and savings, dedicate 10-15% of your remaining net income to your car payment. This range provides a safe and manageable budget for your vehicle, ensuring you can meet your other financial obligations without added stress.

3. Factors Affecting Your Car Affordability

What factors influence how much car you can afford? Several factors influence how much car you can afford, including your credit score, down payment amount, loan term, and interest rate, all of which significantly impact your monthly payments and overall cost of ownership. A better understanding of these factors can lead to smarter purchasing decisions.

3.1 Credit Score

How does your credit score play a role? A higher credit score typically results in lower interest rates on your car loan, reducing your monthly payments and the total amount you pay over the loan term. Improving your credit score can significantly enhance your car-buying power.

3.2 Down Payment

Why is a larger down payment beneficial? Making a larger down payment reduces the amount you need to borrow, resulting in lower monthly payments and less interest paid over the life of the loan. It also demonstrates to lenders that you are a responsible borrower.

3.3 Loan Term

How does the loan term affect your affordability? Opting for a shorter loan term means higher monthly payments but less interest paid overall, whereas a longer loan term reduces monthly payments but increases the total interest. Choosing the right loan term is about balancing affordability and long-term cost.

3.4 Interest Rate

How does the interest rate impact your budget? A lower interest rate can save you thousands of dollars over the life of your loan, making it easier to afford your monthly payments. Shopping around for the best interest rate is crucial for maximizing your affordability.

4. Budgeting for More Than Just the Car Payment

What other expenses should you consider beyond the car payment? When budgeting for a car, remember to factor in additional expenses like insurance, gas, maintenance, and potential repairs, as these costs can significantly impact your overall budget and make it challenging to manage your finances. Being aware of these costs ensures no surprises.

4.1 Car Insurance

How does car insurance factor into your budget? Car insurance premiums can vary widely based on your driving history, location, and the type of vehicle you own. Getting multiple quotes and choosing the right coverage can help you manage this expense effectively.

4.2 Fuel Costs

How can you estimate fuel costs? Use online tools and resources, such as the U.S. Department of Energy’s fuel economy website, to estimate your annual fuel costs based on your driving habits and the fuel efficiency of your vehicle. This helps you factor in a realistic amount for gas each month.

4.3 Maintenance and Repairs

What should you budget for maintenance and repairs? Set aside a portion of your budget each month for routine maintenance, such as oil changes, tire rotations, and other services. Also, be prepared for unexpected repairs by having an emergency fund or a dedicated savings account for vehicle maintenance.

4.4 Registration and Taxes

Are there other fees associated with car ownership? Don’t forget to include registration fees and annual taxes in your car budget, as these costs can add up over time. Check your local DMV for accurate estimates of these expenses.

5. Making Smart Car-Buying Decisions

How can you make the best car-buying choices for your budget? Making smart car-buying decisions involves researching different makes and models, comparing prices, negotiating effectively, and considering the long-term costs of ownership, all of which can help you stay within your budget and avoid financial strain. Informed decisions are the key to car-buying success.

5.1 Research and Comparison

What role does research play in car buying? Before heading to the dealership, research different car models, compare prices, and read reviews to make an informed decision. Websites like Edmunds and Kelley Blue Book offer valuable information and insights.

5.2 Negotiating the Price

How can you negotiate effectively? Negotiate the price of the car with confidence, and be prepared to walk away if the dealer isn’t willing to meet your budget. Knowing the market value of the car and having a target price in mind can give you an advantage.

5.3 Considering Used vs. New

What are the pros and cons of buying used? Buying a used car can save you money on the purchase price and insurance costs, but it may come with higher maintenance expenses. Weigh the pros and cons of both new and used cars to determine the best fit for your needs and budget.

5.4 Avoiding Add-Ons

Are dealer add-ons worth it? Be wary of dealer add-ons, such as extended warranties, paint protection, and other extras that can inflate the price of the car. Determine which add-ons are truly necessary and decline the rest to save money.

6. Strategies to Reduce Your Car Payment

What strategies can help reduce your car payment? To reduce your car payment, consider increasing your down payment, opting for a shorter loan term, improving your credit score, and refinancing your loan, all of which can help lower your monthly expenses and save money over the life of the loan. Small changes can make a big difference.

6.1 Increasing Your Down Payment

How does a larger down payment help? Making a larger down payment reduces the amount you need to finance, lowering your monthly payments and the total interest you’ll pay over the loan term. It’s a simple way to save money in the long run.

6.2 Opting for a Shorter Loan Term

What are the benefits of a shorter loan term? Choosing a shorter loan term results in higher monthly payments, but you’ll pay off the loan faster and save money on interest. It’s a trade-off between short-term affordability and long-term savings.

6.3 Improving Your Credit Score

How does credit improvement lower costs? Improving your credit score can qualify you for lower interest rates on your car loan, reducing your monthly payments and the total cost of borrowing. Take steps to improve your credit before applying for a car loan.

6.4 Refinancing Your Loan

When should you consider refinancing? If interest rates have dropped or your credit score has improved since you took out your car loan, consider refinancing to secure a lower interest rate and reduce your monthly payments. Shop around for the best refinancing offers.

7. The Impact of Car Payments on Your Overall Financial Health

How do car payments affect your broader financial picture? Excessive car payments can negatively impact your overall financial health by limiting your ability to save, invest, and meet other financial goals, potentially leading to debt and financial stress, so maintaining a balanced budget is crucial for long-term stability. Prioritize your financial well-being by keeping car expenses in check.

7.1 Savings and Investments

Why is it important to prioritize savings? High car payments can eat into your savings and investment contributions, hindering your ability to build wealth and achieve financial security. Make sure you’re allocating enough of your income to savings and investments each month.

7.2 Debt Management

How can car payments affect debt levels? Taking on too much debt for a car can increase your overall debt burden and make it harder to manage your finances. Avoid overextending yourself and choose a car that fits comfortably within your budget.

7.3 Emergency Fund

Why is an emergency fund essential? If you have an emergency fund, you are set up to cover unexpected expenses, you do not need to rely on credit cards or loans, which can lead to debt.

7.4 Achieving Financial Goals

How can car payments impact your goals? Excessive car payments can derail your progress toward achieving other financial goals, such as buying a home, starting a business, or retiring early. Keep your car expenses in check to stay on track with your long-term financial objectives.

8. Exploring Alternative Transportation Options

What are some alternatives to owning a car? Consider alternative transportation options such as public transit, biking, walking, or carpooling, as these can reduce or eliminate car payments and related expenses, freeing up more of your income for other financial goals. Exploring different options can lead to significant savings.

8.1 Public Transportation

How can public transit save you money? Using public transportation, such as buses, trains, and subways, can be a cost-effective alternative to owning a car, especially in urban areas with well-developed transit systems. Calculate the cost savings compared to car ownership.

8.2 Biking and Walking

What are the benefits of biking and walking? Biking and walking are not only environmentally friendly and healthy ways to get around, but they can also save you money on transportation costs. Consider biking or walking for short commutes and errands.

8.3 Carpooling

How does carpooling reduce expenses? Carpooling with coworkers, friends, or neighbors can help you share the costs of transportation, such as gas, tolls, and parking fees. It’s a great way to save money and reduce your carbon footprint.

8.4 Ride-Sharing Services

Are ride-sharing services a viable alternative? Ride-sharing services like Uber and Lyft can be a convenient and cost-effective alternative to owning a car, especially for occasional trips or in areas with limited public transportation. Compare the costs of ride-sharing with car ownership.

9. Finding Partnership Opportunities to Boost Income

How can partnerships help you afford your car payment? Exploring partnership opportunities can provide additional income streams to offset car expenses, making your vehicle more affordable, and income-partners.net offers a platform to connect with potential collaborators and ventures. Partnering can lead to financial stability and growth.

9.1 Leveraging Income-Partners.Net

How can income-partners.net help? income-partners.net provides a valuable platform for finding partnership opportunities that can help you increase your income and better manage your car expenses. Explore the site for potential collaborations.

9.2 Types of Partnerships

What kinds of partnerships are available? Consider various partnership options, such as affiliate marketing, joint ventures, and strategic alliances, to find the best fit for your skills and goals. Diversifying your income streams can provide financial stability.

9.3 Real-World Examples

Can you provide examples of successful partnerships? Share success stories of individuals who have used partnerships to increase their income and afford their car payments. Real-world examples can inspire and motivate others.

9.4 Starting Your Partnership Journey

What steps should you take to start? Provide practical tips and advice on how to find and cultivate successful partnerships, including networking, due diligence, and clear communication. A well-planned approach increases your chances of success.

10. Real-Life Examples and Case Studies

How do real people manage their car payments effectively? Explore real-life examples and case studies of individuals who have successfully managed their car payments and maintained financial stability, providing practical insights and inspiration for readers to apply to their own situations. Learn from others’ experiences and strategies.

10.1 Example 1: The Frugal Commuter

What strategies did this individual use? Share the story of someone who reduced their car expenses by using public transportation and biking, highlighting the specific steps they took and the savings they achieved. Showcase the benefits of alternative transportation.

10.2 Example 2: The Smart Negotiator

How did this person negotiate a better deal? Present a case study of someone who negotiated a lower price on their car purchase and secured a favorable interest rate, emphasizing the importance of research and negotiation skills. Demonstrate the power of informed decision-making.

10.3 Example 3: The Partnership Pro

How did this individual leverage partnerships? Tell the story of someone who leveraged partnership opportunities to increase their income and afford their car payments, showcasing the potential of collaborative ventures. Highlight the role of income-partners.net in their success.

10.4 Key Takeaways

What are the main lessons from these examples? Summarize the key takeaways from the real-life examples and case studies, providing actionable advice that readers can apply to their own car-buying and budgeting decisions. Reinforce the importance of smart financial planning.

Navigating the world of car payments doesn’t have to be daunting. By understanding the ideal ratio of car payment to income, calculating your affordable range, and exploring strategies to reduce costs and boost income, you can make informed decisions that support your financial well-being. Visit income-partners.net to discover partnership opportunities and connect with like-minded individuals who can help you achieve your financial goals.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

FAQ: Mastering Your Car Payment

1. What Percentage of My Income Should Go to My Car Payment?

Your car payment should ideally be no more than 10-15% of your net monthly income to ensure financial stability. This percentage allows you to cover other essential expenses and savings.

2. How Do I Calculate My Affordable Car Payment?

Start with your net monthly income, subtract fixed expenses and savings goals, and then allocate 10-15% of the remaining amount to your car budget. This provides a realistic view of your affordability.

3. What Factors Affect My Car Affordability?

Your credit score, down payment amount, loan term, and interest rate all significantly impact your monthly payments and overall cost of ownership. A better understanding of these factors can lead to smarter purchasing decisions.

4. What Expenses Should I Consider Beyond the Car Payment?

Remember to factor in insurance, gas, maintenance, and potential repairs, as these costs can significantly impact your overall budget and make it challenging to manage your finances.

5. How Can I Reduce My Car Payment?

Consider increasing your down payment, opting for a shorter loan term, improving your credit score, and refinancing your loan, all of which can help lower your monthly expenses and save money over the life of the loan.

6. How Do Car Payments Affect My Overall Financial Health?

Excessive car payments can negatively impact your ability to save, invest, and meet other financial goals, potentially leading to debt and financial stress, so maintaining a balanced budget is crucial for long-term stability.

7. What Are Some Alternative Transportation Options?

Consider public transit, biking, walking, or carpooling, as these can reduce or eliminate car payments and related expenses, freeing up more of your income for other financial goals.

8. How Can Partnerships Help Me Afford My Car Payment?

Exploring partnership opportunities can provide additional income streams to offset car expenses, making your vehicle more affordable, and income-partners.net offers a platform to connect with potential collaborators and ventures.

9. What Are the Benefits of a Larger Down Payment?

Making a larger down payment reduces the amount you need to borrow, resulting in lower monthly payments and less interest paid over the life of the loan. It also demonstrates to lenders that you are a responsible borrower.

10. How Can I Improve My Credit Score to Get a Better Car Loan?

Pay your bills on time, reduce your credit card balances, and avoid opening too many new credit accounts. A higher credit score can qualify you for lower interest rates on your car loan.