Determining how much your car payment should be based on income is crucial for maintaining financial stability and avoiding unnecessary debt, and income-partners.net is here to help you navigate this important decision. By understanding the relationship between your income, expenses, and car payment, you can make informed choices that align with your financial goals. We’ll explore practical guidelines, financial advice, and resources to help you manage your car expenses effectively.

1. Understanding the Golden Rule for Car Payments

Is there a rule of thumb when deciding on car payments? Yes, a well-regarded financial guideline suggests that your total monthly car expenses, including the car payment, insurance, and fuel, should not exceed 20% of your monthly take-home pay. This is a crucial rule to safeguard your budget and ensure you’re not overextending yourself. Sticking to this guideline can help you maintain financial stability and avoid unnecessary debt. For example, if your monthly take-home pay is $4,000, your total car-related expenses should ideally stay below $800. This approach, also known as the 20% rule, allows you to have a manageable and sustainable car payment.

Why is this 20% rule so effective?

- Financial Stability: According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, adhering to the 20% rule allows for consistent savings and investment, improving financial stability.

- Budget Management: Following this guideline helps in better budget allocation, ensuring other financial obligations are met without strain.

- Debt Avoidance: By limiting the car payment to 20% of income, individuals are less likely to accumulate excessive debt and can maintain a healthier financial profile.

car payment based on income

car payment based on income

2. Calculating Your Ideal Car Payment

How do you figure out the sweet spot for your car payment? First, you need a clear understanding of your financial landscape. Start by determining your monthly net income, which is your take-home pay after taxes and other deductions. Once you have that figure, subtract all your monthly expenses, including rent or mortgage, utilities, groceries, and any other recurring bills. The remaining amount is what you have available for discretionary spending, including your car payment. Aim for a car payment that fits comfortably within this discretionary budget without compromising your ability to save and invest.

Here’s a step-by-step guide to calculate your ideal car payment:

- Calculate Net Income:

- Net Income = Gross Income – Taxes – Deductions

- Total Monthly Expenses:

- List all fixed and variable monthly expenses.

- Determine Discretionary Income:

- Discretionary Income = Net Income – Total Monthly Expenses

- Apply the 20% Rule:

- Ideal Car Payment = 20% of Net Income (This includes car payment, insurance, and fuel.)

By following these steps, you can determine a car payment that aligns with your financial situation and helps you avoid financial strain.

3. Factors Influencing Car Affordability

What other factors besides income should you consider? Beyond your income, several factors influence how much car you can realistically afford. Your credit score plays a significant role, as it affects the interest rate you’ll receive on your auto loan. A higher credit score typically results in a lower interest rate, which can significantly reduce your monthly payments. Your down payment amount also impacts your loan amount and monthly payments. The larger your down payment, the less you’ll need to borrow, resulting in lower monthly payments and less interest paid over the life of the loan.

Key factors to consider:

- Credit Score: A higher score means lower interest rates.

- Down Payment: A larger down payment reduces the loan amount.

- Loan Term: Shorter terms mean higher monthly payments but less interest paid overall.

- Interest Rate: Compare rates from different lenders to secure the best deal.

Taking these factors into account will help you make a more informed decision about the car you can afford.

4. Budgeting for Car-Related Expenses

Are there other costs besides the car payment that I should budget for? Absolutely. Owning a car involves more than just the monthly payment. You also need to factor in expenses such as car insurance, fuel costs, maintenance, and potential repairs. Car insurance premiums can vary widely depending on your age, driving history, location, and the type of vehicle you own. Fuel costs depend on the fuel efficiency of your car and how much you drive. Maintenance includes routine services like oil changes, tire rotations, and inspections. Setting aside a portion of your budget for these expenses can help you avoid unexpected financial surprises.

To effectively budget for car-related expenses, consider the following:

- Car Insurance:

- Obtain quotes from multiple insurers.

- Consider higher deductibles to lower premiums.

- Fuel Costs:

- Calculate average monthly mileage.

- Factor in current gas prices.

- Maintenance and Repairs:

- Set aside a monthly amount for routine maintenance.

- Create an emergency fund for unexpected repairs.

By carefully budgeting for these expenses, you can ensure that you’re prepared for the full cost of car ownership.

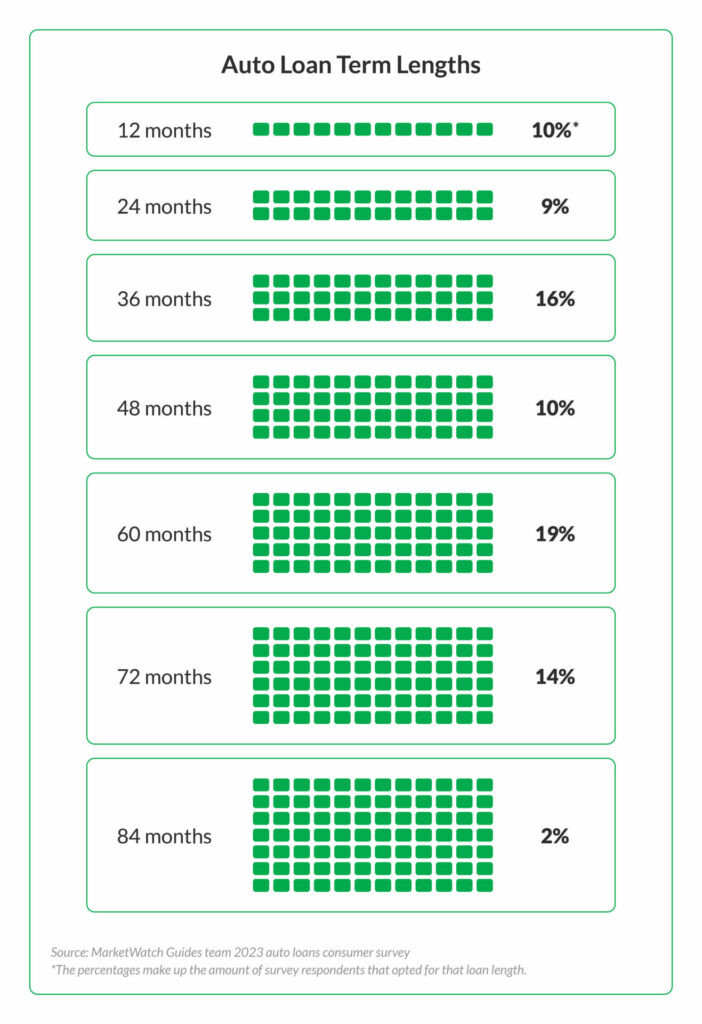

5. Understanding Loan Terms and Interest Rates

What’s the difference between a 36-month loan and a 72-month loan? The loan term and interest rate significantly affect your car payment and the total cost of the vehicle. A shorter loan term, such as 36 months, will result in higher monthly payments but lower overall interest paid. A longer loan term, such as 72 months, will lower your monthly payments but increase the total interest paid over the life of the loan. It’s essential to strike a balance between affordable monthly payments and the total cost of the loan. Additionally, the interest rate you receive depends on your credit score and the prevailing market rates. Shop around for the best interest rates to minimize the cost of borrowing.

Here’s a breakdown of the impact of loan terms and interest rates:

| Loan Term | Monthly Payment | Total Interest Paid | Pros | Cons |

|---|---|---|---|---|

| 36 Months | Higher | Lower | Pay off loan faster, save on interest | Higher monthly payments |

| 72 Months | Lower | Higher | Lower monthly payments, easier to budget | Pay more interest overall, longer debt term |

Choosing the right loan term and securing a competitive interest rate can save you thousands of dollars over the life of the loan.

6. The Impact of Credit Score on Car Payments

How does my credit score affect my car payment? Your credit score is a major determinant of the interest rate you’ll receive on your auto loan. Lenders use your credit score to assess your creditworthiness and the risk of lending you money. A higher credit score demonstrates a history of responsible credit management, making you a less risky borrower. As a result, lenders offer lower interest rates to borrowers with good to excellent credit scores. Conversely, a lower credit score indicates a higher risk, leading to higher interest rates. Improving your credit score before applying for an auto loan can significantly reduce your monthly payments and save you money in the long run.

Strategies to improve your credit score:

- Pay Bills on Time: Consistent on-time payments are crucial.

- Reduce Credit Card Balances: High balances can negatively impact your score.

- Avoid Opening Too Many New Accounts: Opening multiple accounts in a short period can lower your score.

- Check Your Credit Report: Review your credit report for errors and dispute any inaccuracies.

By taking these steps, you can improve your credit score and secure a better interest rate on your auto loan.

7. Leasing vs. Buying: Which Is More Affordable?

Is it better to lease or buy a car? Leasing and buying are two different ways to acquire a vehicle, each with its own set of pros and cons. Leasing typically involves lower monthly payments and requires little to no down payment, making it an attractive option for those on a tight budget. However, at the end of the lease term, you don’t own the car and have to return it. Buying, on the other hand, requires a larger down payment and higher monthly payments, but you own the car outright once the loan is paid off. The best option depends on your financial situation and long-term goals.

Here’s a comparison of leasing and buying:

| Feature | Leasing | Buying |

|---|---|---|

| Monthly Payment | Lower | Higher |

| Down Payment | Lower or None | Higher |

| Ownership | No Ownership | Full Ownership |

| Maintenance | Often Covered by Warranty | Owner’s Responsibility |

| Mileage Limits | Strict Mileage Limits | No Limits |

| Long-Term Costs | Can Be Higher if Always Leasing | Lower Over Time if Car is Kept |

Consider your driving habits, budget, and long-term financial goals when deciding whether to lease or buy.

8. Negotiating the Best Car Deal

How do I negotiate a lower price on a car? Negotiating the price of a car can save you a significant amount of money. Start by researching the fair market value of the car you’re interested in. Use online resources like Kelley Blue Book and Edmunds to get an idea of the average price paid for the vehicle in your area. When negotiating with the dealer, focus on the out-the-door price, which includes all taxes and fees. Be prepared to walk away if the dealer isn’t willing to meet your price. You can also negotiate the interest rate on your auto loan. Get pre-approved for a loan from your bank or credit union to have a baseline interest rate to compare against the dealer’s offer.

Tips for successful negotiation:

- Research Fair Market Value: Know the average price of the car.

- Focus on Out-the-Door Price: Include all taxes and fees.

- Get Pre-Approved for a Loan: Have a baseline interest rate.

- Be Prepared to Walk Away: Don’t be afraid to leave if the deal isn’t right.

With a little preparation and negotiation, you can secure a better deal on your next car.

9. Automating Savings for Your Car Payment

How can I make sure I have enough money for my car payment each month? Automating your savings can help ensure you have enough money for your car payment each month. Set up automatic transfers from your checking account to a dedicated savings account specifically for car-related expenses. Schedule the transfers to coincide with your paydays to ensure the money is available when you need it. Automating your savings eliminates the temptation to spend the money on other things and helps you stay on track with your financial goals.

Steps to automate your savings:

- Open a Dedicated Savings Account: Use a separate account for car-related expenses.

- Set Up Automatic Transfers: Schedule transfers from your checking account.

- Coincide Transfers With Paydays: Ensure funds are available when needed.

- Monitor Your Savings: Regularly check your savings progress.

By automating your savings, you can build a financial cushion for your car payment and other car-related expenses.

10. Refinancing Your Auto Loan

Can I lower my car payment by refinancing my auto loan? Yes, refinancing your auto loan can potentially lower your monthly payments and save you money. Refinancing involves taking out a new loan with a lower interest rate or a longer loan term to pay off your existing auto loan. If interest rates have dropped since you took out your original loan or if your credit score has improved, you may be able to qualify for a lower interest rate. A longer loan term will lower your monthly payments but increase the total interest paid over the life of the loan.

When considering refinancing, keep the following in mind:

- Check Your Credit Score: A higher score can qualify you for better rates.

- Compare Offers: Shop around for the best interest rates and terms.

- Calculate Total Savings: Determine if the savings outweigh any fees associated with refinancing.

- Consider Loan Term: Balance lower payments with total interest paid.

Refinancing can be a smart move if it lowers your overall cost of car ownership.

11. The Role of Location in Car Affordability

Does where I live affect how much I can afford for a car? Yes, your location can significantly impact how much car you can afford. Factors such as insurance rates, fuel costs, and registration fees vary by state and even by city. Urban areas often have higher insurance rates due to increased traffic and a higher risk of accidents. Fuel costs can vary depending on local taxes and the availability of public transportation. Registration fees also differ from state to state. Consider these location-specific factors when calculating your car budget.

Examples of location-related costs:

- Insurance Rates: Higher in urban areas due to traffic density.

- Fuel Costs: Vary based on local taxes and gas prices.

- Registration Fees: Differ from state to state.

Being aware of these factors can help you make a more accurate assessment of your car affordability.

12. How to Find Car Partnership Opportunities at Income-Partners.Net

Are there ways to offset the cost of a car through partnerships? At income-partners.net, we provide numerous opportunities to explore partnerships that can help offset the cost of car ownership. One option is to look for partnerships in the transportation or automotive industry, where you can collaborate with companies on marketing campaigns or product development. Another approach is to find partners who are willing to share transportation costs in exchange for your services or expertise. These partnerships can provide additional income streams, making your car more affordable.

To find such opportunities at income-partners.net:

- Explore Partnership Categories: Look for categories related to transportation, automotive, or local services.

- Network With Other Members: Connect with members who may have partnership ideas or needs.

- Post Your Partnership Ideas: Share your own ideas and expertise to attract potential partners.

- Participate in Forums and Discussions: Engage in conversations to discover new opportunities.

By leveraging income-partners.net, you can find innovative ways to make car ownership more affordable.

13. Exploring Side Hustles to Fund Your Car Payment

What can I do in my spare time to earn extra money for my car? Exploring side hustles is a great way to supplement your income and make your car payment more manageable. Consider options such as driving for ride-sharing services, delivering food, or offering freelance services like writing, design, or virtual assistance. These side hustles can provide a flexible income stream that you can dedicate specifically to your car payment. Additionally, they can help you develop new skills and expand your professional network.

Popular side hustle options:

- Ride-Sharing Services: Drive for companies like Uber or Lyft.

- Food Delivery Services: Deliver food for companies like DoorDash or Uber Eats.

- Freelance Services: Offer writing, design, or virtual assistance services.

- Online Tutoring: Tutor students online in subjects you’re knowledgeable in.

By dedicating a portion of your side hustle income to your car payment, you can significantly reduce the financial strain of car ownership.

14. Using Auto Loan Calculators Effectively

How can an auto loan calculator help me figure out what I can afford? An auto loan calculator is a valuable tool for estimating your monthly car payment and determining how much you can afford. These calculators allow you to input variables such as the loan amount, interest rate, and loan term to see how they impact your monthly payments. You can also use the calculator to experiment with different scenarios, such as increasing your down payment or shortening the loan term, to see how they affect your affordability.

Key benefits of using an auto loan calculator:

- Estimate Monthly Payments: See how different loan terms and interest rates affect your payments.

- Experiment With Scenarios: Explore the impact of changing variables like down payment and loan term.

- Determine Affordability: Find a car payment that fits within your budget.

- Plan Your Finances: Make informed decisions about your car purchase.

By using an auto loan calculator, you can make more informed decisions about your car purchase and ensure it aligns with your financial goals.

15. The Long-Term Financial Implications of Car Debt

What are the consequences of having too much car debt? Taking on too much car debt can have significant long-term financial implications. High monthly car payments can strain your budget, making it difficult to save for other important goals such as retirement, education, or homeownership. Additionally, excessive car debt can limit your ability to invest and build wealth over time. It’s essential to strike a balance between your transportation needs and your financial well-being.

Potential consequences of excessive car debt:

- Strained Budget: Difficulty covering other essential expenses.

- Limited Savings: Reduced ability to save for long-term goals.

- Reduced Investment Opportunities: Limited funds for investing and building wealth.

- Stress and Anxiety: Financial stress can negatively impact your overall well-being.

By being mindful of the long-term financial implications of car debt, you can make more responsible decisions about your car purchase.

16. How to Track Your Car Expenses

What’s the best way to keep track of my car expenses? Keeping track of your car expenses is essential for managing your budget and identifying areas where you can save money. Use budgeting apps like Mint, YNAB (You Need A Budget), or Personal Capital to track your income and expenses. These apps allow you to categorize your expenses, set budgets, and monitor your spending habits. Regularly reviewing your car expenses can help you identify opportunities to reduce costs, such as finding cheaper gas, negotiating lower insurance rates, or reducing unnecessary trips.

Methods for tracking car expenses:

- Budgeting Apps: Use apps like Mint, YNAB, or Personal Capital.

- Spreadsheets: Create a spreadsheet to manually track income and expenses.

- Expense Tracking Apps: Use apps specifically designed for tracking expenses.

- Regular Reviews: Review your expenses regularly to identify savings opportunities.

By tracking your car expenses, you can gain better control over your finances and make more informed decisions about your car ownership.

17. Understanding the Total Cost of Car Ownership

What’s included in the total cost of owning a car? Understanding the total cost of car ownership involves considering all expenses associated with owning and operating a vehicle over its lifespan. This includes the purchase price, financing costs, insurance, fuel, maintenance, repairs, registration fees, and depreciation. Depreciation, the decline in the car’s value over time, is often one of the most significant costs of car ownership. By understanding the total cost of car ownership, you can make more informed decisions about your car purchase and budget accordingly.

Components of the total cost of car ownership:

- Purchase Price: The initial cost of the vehicle.

- Financing Costs: Interest paid on the auto loan.

- Insurance: Premiums for car insurance coverage.

- Fuel: Costs of gasoline or electricity.

- Maintenance: Routine services like oil changes and tire rotations.

- Repairs: Costs of unexpected repairs.

- Registration Fees: Annual fees for registering the vehicle.

- Depreciation: Decline in the car’s value over time.

By considering all these factors, you can get a more accurate picture of the true cost of car ownership.

18. The Importance of Regular Car Maintenance

Why is it important to keep up with car maintenance? Regular car maintenance is crucial for preserving the reliability, safety, and value of your vehicle. Following the manufacturer’s recommended maintenance schedule can help prevent costly repairs and extend the lifespan of your car. Regular maintenance includes oil changes, tire rotations, brake inspections, fluid checks, and tune-ups. Neglecting maintenance can lead to more significant problems down the road, potentially resulting in expensive repairs or even a breakdown.

Benefits of regular car maintenance:

- Improved Reliability: Reduces the risk of breakdowns and unexpected repairs.

- Enhanced Safety: Ensures critical components like brakes and tires are in good working order.

- Extended Lifespan: Prolongs the life of the vehicle.

- Maintained Value: Helps preserve the car’s resale value.

By prioritizing regular car maintenance, you can ensure your car remains reliable, safe, and valuable.

19. Saving Money on Car Insurance

What are some ways to lower my car insurance rates? There are several strategies you can use to lower your car insurance rates. Start by comparing quotes from multiple insurance companies to find the best rates. Consider increasing your deductible, the amount you pay out of pocket before your insurance coverage kicks in. A higher deductible typically results in lower premiums. You can also qualify for discounts by bundling your car insurance with other insurance policies, such as home or renters insurance. Additionally, maintaining a clean driving record and taking a defensive driving course can help you qualify for lower rates.

Tips for saving money on car insurance:

- Compare Quotes: Shop around for the best rates.

- Increase Deductible: Choose a higher deductible to lower premiums.

- Bundle Policies: Combine car insurance with other policies.

- Maintain Clean Driving Record: Avoid accidents and traffic violations.

- Take Defensive Driving Course: Qualify for discounts by completing a course.

By implementing these strategies, you can significantly reduce your car insurance costs.

20. Finding the Right Balance Between Car Needs and Financial Health

How do I know when I’m spending too much on a car? Finding the right balance between your car needs and your financial health is essential for long-term financial stability. If your car payment and related expenses are consuming a significant portion of your income, it may be time to re-evaluate your car situation. Consider whether you can downsize to a more affordable vehicle, refinance your auto loan, or explore alternative transportation options like public transportation, biking, or walking. Prioritize your financial goals and make sure your car payment isn’t hindering your ability to save, invest, and achieve your financial dreams.

Signs you may be spending too much on a car:

- High Car Payment: Consumes a significant portion of your income.

- Difficulty Saving: Struggling to save for other financial goals.

- Limited Investment Opportunities: Unable to invest and build wealth.

- Financial Stress: Feeling stressed or anxious about your car expenses.

By regularly assessing your car expenses and prioritizing your financial health, you can ensure your car ownership aligns with your long-term financial goals.

Managing your car payments effectively is vital for your financial well-being, and income-partners.net is dedicated to providing you with the strategies and resources you need to make informed decisions. Remember to adhere to the 20% rule, calculate your ideal car payment, and consider all related expenses, including insurance, fuel, and maintenance.

Ready to take control of your financial future and find the perfect car payment solution? Visit income-partners.net today! Explore our resources, connect with financial experts, and discover partnership opportunities that can help you manage your car expenses and achieve your financial goals. Don’t wait – start your journey to financial freedom now! You can visit us at 1 University Station, Austin, TX 78712, United States, or call us at +1 (512) 471-3434.

FAQ: Car Payments and Affordability

1. What is the 20% rule for car payments?

The 20% rule suggests that your total monthly car expenses, including the car payment, insurance, and fuel, should not exceed 20% of your monthly take-home pay to maintain financial stability.

2. How does my credit score affect my car payment?

A higher credit score typically results in a lower interest rate on your auto loan, reducing your monthly payments and the total cost of the vehicle.

3. What factors influence car affordability besides income?

Other factors include your credit score, down payment amount, loan term, and interest rate.

4. Should I lease or buy a car?

Leasing usually has lower monthly payments but no ownership. Buying requires a larger down payment and higher monthly payments but you own the car. The best option depends on your financial situation and long-term goals.

5. How can I negotiate a better car deal?

Research the fair market value, focus on the out-the-door price, get pre-approved for a loan, and be prepared to walk away if the deal isn’t right.

6. What are some side hustles to help fund my car payment?

Consider driving for ride-sharing services, delivering food, or offering freelance services to supplement your income.

7. What is the total cost of car ownership?

The total cost includes the purchase price, financing costs, insurance, fuel, maintenance, repairs, registration fees, and depreciation.

8. How can automating savings help with my car payment?

Automating transfers to a dedicated savings account ensures you have enough money for car-related expenses and helps you stay on track with your financial goals.

9. Can I refinance my auto loan to lower my payment?

Yes, refinancing can potentially lower your monthly payments by securing a lower interest rate or a longer loan term.

10. Why is regular car maintenance important?

Regular maintenance ensures reliability, enhances safety, extends the car’s lifespan, and maintains its resale value.