How Much Of Your Income Should Go To Car Payment? Determining the ideal portion of your income for car payments is crucial for maintaining financial health and avoiding unnecessary stress, and income-partners.net can help you find strategic alliances to boost your income. To determine the appropriate amount, let’s explore this topic in detail and help you make a smart choice. This article will explore factors such as monthly income, expenses, and loan terms, as well as providing strategies for improving your income.

1. Understanding the Foundation: Calculating Your Car Payment Potential

What’s the first step in figuring out your monthly car payment potential? Start by accurately determining how much you can realistically allocate each month without straining your financial situation. Begin by gathering data on your wages, salaries, current bank statements, and records of any monthly or annual expenses.

1.1 Net Pay vs. Gross Pay: Which Should You Consider?

Why is using your net pay better than using your gross pay? Our team strongly advises beginning with your post-tax take-home pay, often known as net pay, rather than your annual salary figure or gross pay because it gives you a more realistic view of what you can afford for a car payment. Using your net pay provides a more accurate reflection of your actual disposable income.

1.2 Deducting Expenses: How Does This Affect Your Car Budget?

Why is it important to deduct recurring expenses? Remember to deduct recurring expenses, bills, and other monthly budget items from your take-home pay to reach a low-risk potential monthly payment range. This ensures you’re only allocating funds you can truly afford.

2. Expert Advice: MarketWatch Guidance on Staying Within Budget

What does MarketWatch suggest for staying within your car budget? MarketWatch advises that you shouldn’t max out your budget, and it’s important to keep your anticipated monthly car payments within reasonable ranges to stay prepared for unexpected financial strain. This provides you with a safety net for unforeseen financial challenges.

2.1 The Importance of Realistic Loan Terms

Why should you be realistic about loan terms? Being realistic about how long you want to make monthly payments is essential because most loan companies offer terms between 24 and 84 months for used and new cars. This decision directly impacts your financial health.

2.2 Longer Loan Terms: Pros and Cons

What are the advantages and disadvantages of choosing a longer loan term? Choosing a longer loan term can help you get lower monthly payments, but you’ll pay more overall because of the additional interest that accumulates. While it eases the immediate financial burden, it increases the total cost over time.

2.3 Avoiding the Upside-Down Loan Scenario

What does it mean to be upside-down on a car loan? Longer loan terms also increase your risk of going upside-down on your loan, which happens when borrowers end up owing more on the loan than the vehicle is worth. Since a vehicle’s value decreases over time, weigh your options carefully before choosing which vehicle to purchase.

3. Salary-Based Car Payment Guidelines

What kind of car payment can you afford based on your salary? Here’s a helpful guideline based on your post-tax monthly take-home pay:

| Monthly Take-Home Pay (Post-Tax) | Monthly Car Payments Should Not Exceed… |

|---|---|

| $1,500 | $150 to $225 per month |

| $3,000 | $300 to $450 per month |

| $4,500 | $450 to $675 per month |

| $6,000 | $600 to $900 per month |

| $7,500 | $750 to $1,125 per month |

| $9,000 | $900 to $1,350 per month |

4. The Hidden Costs: Fuel and Insurance

What hidden costs should you consider when buying a car? Before you purchase or lease a vehicle, factor in fuel expenses and car insurance costs, which can vary widely based on your location, driving history, and vehicle type.

4.1 Estimating Fuel Costs

How can you estimate fuel costs? The U.S. Department of Energy provides a detailed list of fuel economy figures as well as a comparison tool that allows you to check different vehicles’ annual fuel cost estimates. This allows for a more informed decision.

4.2 Comparing Car Insurance Quotes

How do you find affordable car insurance? For auto insurance quotes, reach out to your agent or an insurance company you’re interested in. You can easily get and compare car insurance quotes from companies to get a sense of what you’ll pay.

4.3 Total Costs: Aiming for 20% of Take-Home Pay

What percentage of your take-home pay should cover total car costs? When calculating your monthly car payment and related expenses, try to keep your total costs to less than 20% of your monthly take-home pay. This ensures you maintain financial stability.

5. Navigating Loan Amounts and Terms

How do you calculate the loan amount you can afford? Once you’ve calculated your affordable monthly payment, you can determine how much you can borrow. The amount a lender will let you borrow depends on several factors, including:

- Buying a Used or New Car: New car loans tend to have lower annual percentage rates (APRs) than used cars.

- Your Credit Score: This will affect the APR on the loan and how much the bank is willing to lend you.

- Your Loan Term: This is how many months you’ll have to pay your auto loan off.

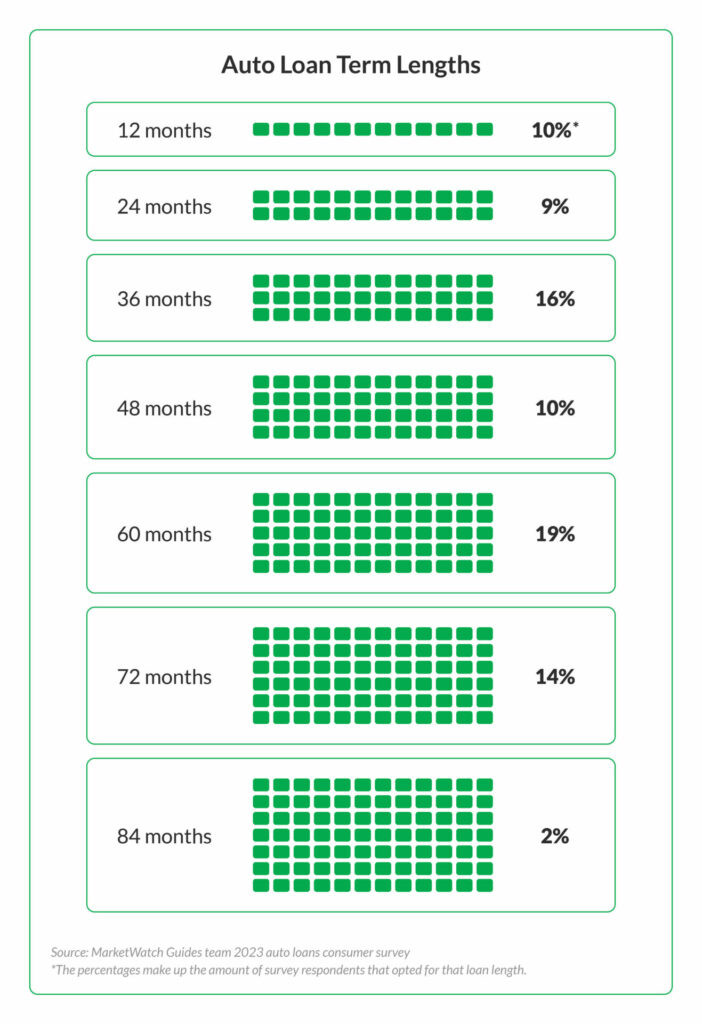

5.1 Survey Insights: Popular Loan Terms

What is the most popular auto loan term length? According to our 2023 consumer survey, which questioned 2,000 customers with experiences in auto loans, nineteen percent of respondents had a loan term of 60 months, making it the most popular.

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

6. The Real Price Tag: Setting a Purchase Price

Why is the sticker price not the only factor to consider? The total loan amount you calculated for your car may not be the price you pay. When shopping for a car, pay attention to details other than the sticker price because sales tax and fees can significantly increase the total cost.

6.1 Understanding Additional Fees and Taxes

What additional fees and taxes should you expect when buying a car? Here’s a breakdown of what you can expect to pay in fees or taxes:

- Sales Tax: Up to 12.9% and varies by state.

- Registration Fees: Typically range from $50 to $300, although some states can be much more expensive.

- Documentation Fees: Generally between $100 and $500, depending on your state.

6.2 Reducing the Loan Amount

How can you reduce the amount you need to borrow? Making a down payment or trading in your old car can help you borrow less money when purchasing a vehicle. Both options reduce the overall financial burden.

7. Leveraging Tools: Car Affordability Calculators

How can an auto loan calculator help you? An auto loan calculator can help you determine the monthly payment and total cost of an auto loan you may qualify for. It uses factors such as your loan term, down payment, and interest rate. Some calculators may also incorporate sales tax, fees, and your current vehicle’s trade-in value.

7.1 Maximizing Calculator Benefits

What information should you input into a car affordability calculator? Enter your projected loan amount, term, and interest rate to see your estimated monthly payments and the total interest you can expect to pay. This offers a clear picture of your financial commitment.

8. Partnering for Prosperity: Enhancing Income to Manage Car Payments

How can strategic partnerships help manage car payments? Managing car payments effectively isn’t just about budgeting; it’s also about increasing your income. income-partners.net offers opportunities to connect with strategic alliances that can significantly boost your earnings. These partnerships can provide the financial flexibility needed to comfortably afford your car payments and other financial goals.

8.1 The Power of Strategic Alliances

What types of strategic alliances are available? Strategic alliances can take many forms, including joint ventures, marketing partnerships, and collaborative projects. These alliances allow you to leverage the resources and expertise of others, opening doors to new revenue streams.

8.2 Finding the Right Partners

How do you find the right partners for income growth? Finding the right partners involves identifying businesses or individuals who complement your skills and resources. income-partners.net provides a platform to explore potential collaborations, assess compatibility, and establish mutually beneficial relationships.

8.3 Success Stories: Partnerships in Action

Can you provide examples of successful income-boosting partnerships? Consider a marketing agency partnering with a software company to offer bundled services, or a freelancer collaborating with a consulting firm to tackle larger projects. These partnerships not only increase revenue but also expand your professional network and skill set.

8.4 Building a Collaborative Ecosystem

How does collaboration lead to long-term financial stability? Building a collaborative ecosystem is key to sustained financial stability. By continuously seeking out and nurturing strategic alliances, you can create a diversified income portfolio that mitigates financial risks and enhances your ability to meet financial obligations, including car payments.

9. Real-World Examples: Scenarios and Solutions

How can different financial situations affect car payment decisions? Let’s explore a few scenarios to illustrate how different income levels and financial situations can influence the decision-making process:

9.1 Scenario 1: The Recent Graduate

What car payment is feasible for a recent graduate with a starting salary? A recent graduate earning $3,000 per month after taxes should aim for car payments between $300 and $450. They should also prioritize building credit and saving for a down payment to secure better loan terms.

9.2 Scenario 2: The Growing Family

How should a family with increasing expenses manage car payments? A family earning $6,000 per month after taxes might consider car payments between $600 and $900. They should focus on finding a reliable and fuel-efficient vehicle while managing other household expenses.

9.3 Scenario 3: The Entrepreneur

What is a reasonable car payment for an entrepreneur with fluctuating income? An entrepreneur with a variable monthly income averaging $7,500 after taxes can consider car payments between $750 and $1,125. They should maintain a financial cushion to cover payments during leaner months and explore tax deductions for business-related vehicle expenses.

10. Expert Insights: Financial Advisors’ Perspectives

What do financial advisors recommend regarding car affordability? Financial advisors often recommend adhering to the 20/4/10 rule: 20% down payment, finance the car for no more than 4 years, and ensure that total transportation costs (including insurance and fuel) do not exceed 10% of your gross monthly income.

10.1 Aligning Car Payments with Financial Goals

How do car payments fit into broader financial planning? Integrating car payments into your overall financial plan involves setting clear financial goals, creating a budget, and regularly reviewing your progress. This ensures that your car expenses align with your long-term financial objectives.

10.2 Common Mistakes to Avoid

What are the common pitfalls when financing a car? Common mistakes include not shopping around for the best interest rates, underestimating the total cost of ownership, and choosing a vehicle that exceeds your budget. Avoiding these pitfalls can save you significant money and stress.

11. Strategies for Improving Your Income

How can you proactively increase your income to better afford car payments? Improving your income provides more financial flexibility and reduces the strain of car payments. Consider these strategies:

11.1 Seeking Additional Income Streams

What are some options for generating extra income? Explore part-time jobs, freelance work, or side businesses that align with your skills and interests. Platforms like Upwork and Fiverr offer numerous opportunities to earn additional income.

11.2 Negotiating Salary Increases

How can you effectively negotiate a higher salary? Research industry benchmarks, document your accomplishments, and confidently present your case to your employer. Demonstrating your value can lead to a higher salary, providing more room for car payments.

11.3 Investing in Skill Development

Why is continuous learning essential for income growth? Investing in skill development can increase your earning potential. Take courses, attend workshops, or pursue certifications that enhance your expertise and make you more valuable in the job market.

12. Harnessing Technology: Apps and Tools for Budgeting

What digital tools can aid in managing car expenses? Several apps and tools can help you track your spending, create budgets, and manage your car expenses:

12.1 Budgeting Apps Overview

Which budgeting apps are most effective for car payment management? Apps like Mint, YNAB (You Need A Budget), and Personal Capital offer features for tracking expenses, setting budgets, and monitoring your financial health. These tools can help you stay on top of your car payments and overall financial goals.

12.2 Utilizing Car Maintenance Trackers

How do car maintenance trackers help with budgeting? Car maintenance trackers like Carfax Car Care and AutoCare can help you monitor your vehicle’s maintenance schedule and anticipate upcoming expenses. This allows you to budget for repairs and maintenance, preventing unexpected financial strain.

12.3 Financial Planning Software

What are the benefits of using financial planning software? Financial planning software like Quicken and TurboTax can provide a comprehensive overview of your financial situation, including car payments, investments, and retirement savings. This holistic approach helps you make informed decisions and optimize your financial strategy.

13. The Future of Car Ownership: Trends and Predictions

What trends are shaping the future of car ownership? Several trends are influencing the future of car ownership, including the rise of electric vehicles, car-sharing services, and autonomous driving technologies.

13.1 The Rise of Electric Vehicles

How do electric vehicles impact car affordability? Electric vehicles (EVs) can offer long-term cost savings due to lower fuel and maintenance expenses. Government incentives and tax credits can also make EVs more affordable, reducing the overall financial burden of car ownership.

13.2 Car-Sharing and Subscription Services

What are the alternatives to traditional car ownership? Car-sharing services like Zipcar and car subscription services offer alternatives to traditional car ownership. These options can be more cost-effective for individuals who don’t need a car full-time, providing flexibility and reducing financial commitments.

13.3 Autonomous Driving Technology

How might autonomous vehicles change transportation costs? Autonomous driving technology has the potential to revolutionize transportation costs by reducing accidents, optimizing fuel efficiency, and lowering insurance rates. While still in development, autonomous vehicles could significantly impact the affordability of transportation in the future.

14. Legal and Financial Considerations

What legal and financial aspects should you be aware of when buying a car? Understanding the legal and financial implications of car ownership is crucial for making informed decisions and protecting your interests.

14.1 Understanding Loan Agreements

What should you look for in a car loan agreement? Carefully review the terms of your car loan agreement, including the interest rate, loan term, payment schedule, and any fees or penalties. Understanding these details can help you avoid surprises and manage your financial obligations effectively.

14.2 Insurance Requirements

What types of insurance coverage are necessary? Most states require minimum levels of auto insurance coverage, including liability insurance. Consider purchasing additional coverage, such as collision and comprehensive insurance, to protect yourself against financial losses in the event of an accident or damage to your vehicle.

14.3 Tax Implications

Are there any tax benefits associated with car ownership? Depending on your situation, you may be able to deduct certain car-related expenses on your taxes, such as vehicle registration fees and business-related mileage. Consult with a tax professional to determine which deductions you qualify for.

15. Success Stories: Managing Car Payments Effectively

Can you share examples of individuals who have successfully managed their car payments? Numerous individuals have successfully managed their car payments by employing smart budgeting, income-boosting strategies, and informed decision-making.

15.1 Case Study 1: The Budget-Savvy Professional

How did one professional manage their car payments while paying off debt? A young professional successfully managed her car payments by creating a detailed budget, tracking her expenses, and automating her savings. She also negotiated a lower interest rate on her car loan and paid it off ahead of schedule, saving thousands of dollars in interest.

15.2 Case Study 2: The Entrepreneurial Driver

How did an entrepreneur use their car to boost their income? An entrepreneur leveraged his car to start a delivery service, generating additional income to cover his car payments and other expenses. He also took advantage of tax deductions for business-related vehicle expenses, further reducing his financial burden.

15.3 Case Study 3: The Frugal Family

How did a family balance car payments with other financial responsibilities? A family balanced their car payments with other financial responsibilities by prioritizing their needs, cutting unnecessary expenses, and seeking out discounts and savings opportunities. They also maintained their car well to minimize maintenance costs and extend its lifespan.

16. Avoiding Common Mistakes

What are the most frequent errors people make when financing a car? Many people make common mistakes when financing a car, leading to financial strain and regret. Avoiding these errors can save you money and stress.

16.1 Not Shopping Around for Loans

Why is it essential to compare loan options from multiple lenders? Not shopping around for loans can result in paying a higher interest rate than necessary. Comparing offers from multiple lenders can help you secure the best terms and save money over the life of the loan.

16.2 Underestimating Total Cost of Ownership

What costs beyond the car payment should you factor in? Underestimating the total cost of ownership can lead to budget shortfalls. Remember to factor in expenses such as insurance, fuel, maintenance, and repairs when determining your car affordability.

16.3 Overspending on Features and Upgrades

How can you avoid overspending on unnecessary car features? Overspending on features and upgrades can quickly inflate the price of your car. Prioritize your needs and choose features that provide genuine value without breaking the bank.

17. The Role of Credit Score in Car Financing

How does your credit score influence car loan terms and interest rates? Your credit score plays a significant role in determining the terms and interest rates you qualify for on a car loan. A higher credit score typically results in lower interest rates and more favorable loan terms, saving you money over time.

17.1 Improving Your Credit Score

What steps can you take to improve your credit score? Improving your credit score can enhance your car financing options. Strategies include paying bills on time, reducing debt, and monitoring your credit report for errors.

17.2 Monitoring Your Credit Report

Why is it important to regularly check your credit report? Regularly checking your credit report can help you identify and correct errors that may be negatively impacting your credit score. You can obtain free copies of your credit report from the three major credit bureaus: Experian, Equifax, and TransUnion.

17.3 Addressing Credit Issues

How can you resolve negative entries on your credit report? Addressing credit issues promptly can improve your credit score. Dispute errors with the credit bureaus and work with creditors to resolve outstanding debts or payment issues.

18. The Impact of Lifestyle Choices

How do lifestyle choices affect car affordability? Your lifestyle choices can significantly impact your car affordability. Consider how your spending habits, transportation needs, and personal preferences influence your ability to manage car payments.

18.1 Prioritizing Transportation Needs

How do you assess your actual transportation requirements? Prioritizing your transportation needs can help you make informed decisions about car ownership. Evaluate how often you use your car, the distance you typically drive, and any specific requirements you have for a vehicle.

18.2 Balancing Wants and Needs

How do you differentiate between essential and non-essential car features? Balancing wants and needs can help you avoid overspending on unnecessary car features. Focus on essential features that meet your transportation requirements and consider forgoing luxury options that strain your budget.

18.3 Reducing Transportation Costs

What strategies can you employ to lower your overall transportation expenses? Reducing transportation costs can free up more money for car payments. Strategies include carpooling, using public transportation, biking, or walking whenever possible.

19. Future-Proofing Your Finances

How can you ensure long-term financial stability while managing car payments? Future-proofing your finances involves creating a comprehensive financial plan that addresses both current and future needs.

19.1 Building an Emergency Fund

Why is an emergency fund crucial for managing unexpected expenses? Building an emergency fund can help you weather unexpected expenses, such as car repairs or job loss, without derailing your financial plan. Aim to save at least three to six months’ worth of living expenses in an easily accessible account.

19.2 Investing for the Future

How can investing contribute to long-term financial security? Investing for the future can help you grow your wealth and achieve your financial goals. Consider investing in stocks, bonds, or real estate to diversify your portfolio and generate long-term returns.

19.3 Planning for Retirement

Why is it important to start saving for retirement early? Planning for retirement early can ensure you have adequate funds to support your lifestyle in your later years. Take advantage of employer-sponsored retirement plans and consider opening a Roth IRA or traditional IRA to save for retirement.

20. Leveraging Professional Advice

When should you seek advice from a financial advisor? Seeking advice from a financial advisor can provide valuable guidance and support in managing your car payments and overall financial plan.

20.1 Benefits of Consulting a Financial Advisor

How can a financial advisor assist with car payment management? A financial advisor can help you create a budget, assess your car affordability, and develop a financial plan that aligns with your goals. They can also provide expert advice on managing debt, investing, and saving for the future.

20.2 Finding a Qualified Financial Advisor

How do you identify a trustworthy and competent financial advisor? Finding a qualified financial advisor involves researching their credentials, experience, and reputation. Look for advisors who are certified and have a track record of success in helping clients achieve their financial goals.

20.3 The Value of Ongoing Financial Planning

Why is continuous financial planning important for long-term success? Ongoing financial planning can help you stay on track with your financial goals, adapt to changing circumstances, and make informed decisions about your money. Regular check-ins with a financial advisor can provide valuable support and guidance throughout your financial journey.

Conclusion: Making Informed Car Payment Decisions

How can you make informed decisions about your car payment? By understanding your financial situation, exploring different options, and seeking expert advice, you can make informed decisions about your car payment and ensure your long-term financial stability.

Ready to take control of your financial future and explore strategic partnerships to boost your income? Visit income-partners.net today to discover opportunities for collaboration, growth, and financial success. Let’s build a partnership that drives us forward together. Don’t wait—the road to financial empowerment starts now. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

FAQ: Addressing Your Car Payment Questions

Q1: What is the ideal percentage of my income to spend on a car payment?

The ideal percentage of your income to spend on a car payment should be no more than 10-15% of your monthly take-home pay to maintain financial stability.

Q2: How can I calculate how much car I can afford?

Calculate how much car you can afford by assessing your monthly income, deducting expenses, and using online car affordability calculators to determine a reasonable monthly payment.

Q3: What are the key factors to consider when determining car affordability?

Key factors to consider when determining car affordability include your income, monthly expenses, credit score, down payment, loan term, and the total cost of ownership (including insurance and fuel).

Q4: Should I consider leasing a car instead of buying one?

Consider leasing a car if you prefer lower monthly payments and enjoy driving a new car every few years. However, keep in mind that you won’t own the car at the end of the lease term.

Q5: How does my credit score impact my car loan interest rate?

Your credit score significantly impacts your car loan interest rate; a higher credit score typically results in lower interest rates and more favorable loan terms.

Q6: What are some strategies to lower my car payment?

Strategies to lower your car payment include making a larger down payment, opting for a shorter loan term, improving your credit score, and shopping around for the best interest rates.

Q7: How can I increase my income to afford a more expensive car?

Increase your income to afford a more expensive car by seeking additional income streams, negotiating salary increases, investing in skill development, or starting a side business. Platforms like income-partners.net can help you find strategic alliances to boost your earnings.

Q8: What should I do if I’m struggling to make my car payments?

If you’re struggling to make your car payments, contact your lender to explore options such as refinancing or loan modification. Also, reassess your budget and consider selling the car if necessary.

Q9: Are there any tax benefits associated with car ownership?

Depending on your situation, you may be able to deduct certain car-related expenses on your taxes, such as vehicle registration fees and business-related mileage.

Q10: How can financial planning help me manage my car payments effectively?

Financial planning can help you manage your car payments effectively by creating a budget, setting financial goals, and developing a comprehensive plan that aligns with your needs and priorities. Seeking advice from a financial advisor can provide valuable support and guidance.