How Much Of Your Income Should Go To Car? A responsible approach to car ownership involves understanding the relationship between your earnings and car-related expenses, and income-partners.net is designed to help you navigate this relationship effectively, providing resources for financial planning and income growth strategies. To find the right balance, carefully assess your budget, consider various financial factors, and explore partnership opportunities to increase your income and manage car expenses wisely, focusing on budgeting strategies, income diversification, and financial planning.

1. Understanding the Golden Rule: The 20/4/10 Rule

Many financial experts recommend the 20/4/10 rule when considering how much of your income should go to your car. This rule provides a simple framework for making informed decisions about car affordability:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price. This reduces the loan amount, lowering monthly payments and the total interest paid over the life of the loan.

- 4-Year Loan Term: Opt for a loan term of no more than four years. This helps you pay off the car faster, minimizing interest costs and reducing the risk of owing more than the car is worth as it depreciates.

- 10% of Gross Income: Limit total car-related expenses (including loan payments, insurance, fuel, and maintenance) to no more than 10% of your gross monthly income. This ensures that car expenses don’t strain your overall budget.

Following the 20/4/10 rule can help you make informed decisions about car affordability, ensuring that you don’t overextend yourself financially.

Why is the 20/4/10 Rule Important?

The 20/4/10 rule is a guideline to help you manage your car expenses responsibly and avoid financial strain. By adhering to this rule, you can:

- Minimize Debt: A larger down payment and shorter loan term reduce the total amount of debt you incur.

- Control Interest Costs: Shorter loan terms and larger down payments mean you’ll pay less interest over the life of the loan.

- Maintain Financial Flexibility: Limiting total car expenses to 10% of your gross income ensures that you have enough money left over for other essential expenses and financial goals.

How to Apply the 20/4/10 Rule in Practice?

Applying the 20/4/10 rule involves some careful planning and budgeting:

- Determine Your Gross Monthly Income: Calculate your total income before taxes and other deductions.

- Calculate Your Maximum Car Expense: Multiply your gross monthly income by 10% to determine the maximum amount you should spend on car-related expenses each month.

- Estimate Insurance, Fuel, and Maintenance Costs: Research insurance rates, fuel costs, and potential maintenance expenses for the car you’re considering.

- Determine Your Maximum Loan Payment: Subtract the estimated insurance, fuel, and maintenance costs from your maximum car expense to determine the maximum amount you can afford to spend on a car loan payment.

- Calculate the Car Price You Can Afford: Use an auto loan calculator to determine the maximum car price you can afford based on your desired down payment, loan term, and interest rate, while keeping your monthly payment within the limit you calculated.

By following these steps, you can make informed decisions about car affordability, ensuring that you don’t overextend yourself financially.

Man calculates monthly car payments

Man calculates monthly car payments

2. Understanding the Factors Influencing Car Affordability

Several factors influence how much of your income should go to your car, and understanding these factors can help you make informed decisions.

Income

Your income is the most important factor in determining car affordability. A general guideline is that your total car-related expenses (including loan payments, insurance, fuel, and maintenance) should not exceed 10-15% of your gross monthly income.

Expenses

Your existing expenses, such as rent, utilities, groceries, and debt payments, play a significant role in determining how much you can afford to spend on a car. It’s essential to create a detailed budget to understand your cash flow and identify areas where you can potentially reduce expenses.

Credit Score

Your credit score affects the interest rate you’ll receive on a car loan. A higher credit score typically results in a lower interest rate, which can save you thousands of dollars over the life of the loan. Check your credit report for errors and take steps to improve your credit score before applying for a car loan.

Down Payment

The amount of your down payment affects the loan amount and monthly payments. A larger down payment reduces the loan amount, lowering monthly payments and the total interest paid over the life of the loan. Aim to put down at least 20% of the car’s purchase price.

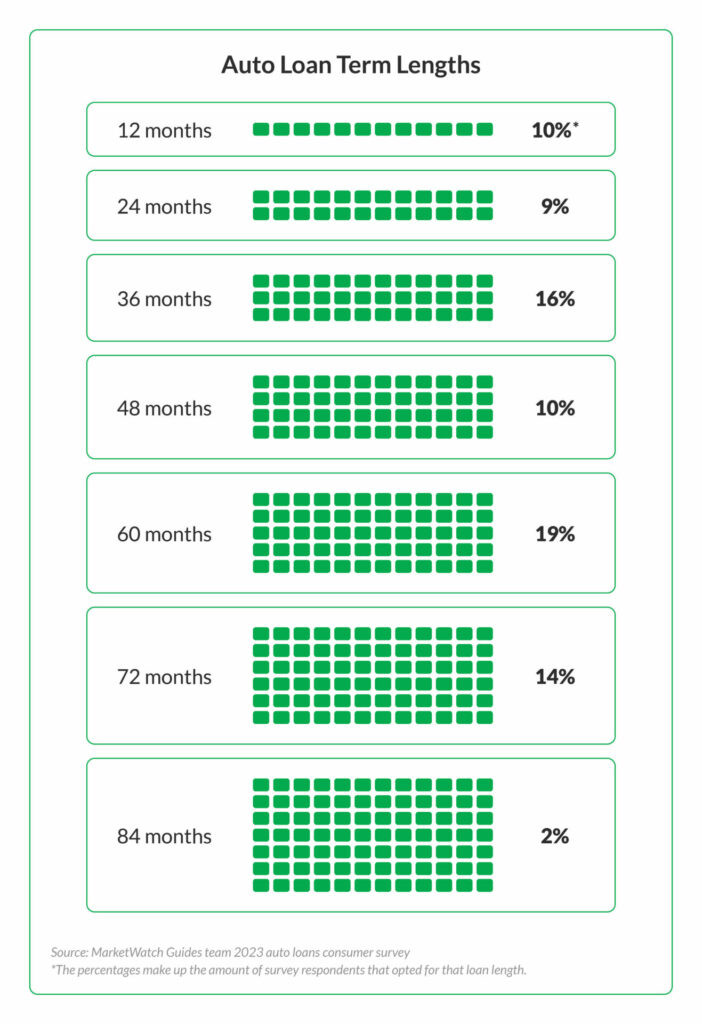

Loan Term

The loan term is the length of time you have to repay the loan. Shorter loan terms result in higher monthly payments but lower total interest paid, while longer loan terms result in lower monthly payments but higher total interest paid. Opt for a loan term of no more than four years to minimize interest costs.

Insurance Costs

Car insurance costs vary depending on factors such as your age, driving history, location, and the type of car you’re insuring. Get quotes from multiple insurance companies to compare rates and find the best deal.

Fuel Costs

Fuel costs depend on the car’s fuel efficiency and how much you drive. Consider buying a fuel-efficient car to save money on gas.

Maintenance Costs

Cars require regular maintenance, such as oil changes, tire rotations, and brake repairs. Set aside money each month to cover these costs.

By considering these factors, you can determine how much of your income should go to your car and make informed decisions about car affordability.

3. How to Calculate Your Car Affordability: A Step-by-Step Guide

Calculating how much car you can afford involves assessing your financial situation and determining how much you can comfortably spend on car-related expenses each month. Here’s a step-by-step guide to help you calculate your car affordability:

Step 1: Determine Your Gross Monthly Income

Start by calculating your total income before taxes and other deductions. This includes your salary, wages, and any other sources of income.

Step 2: Create a Detailed Budget

Create a detailed budget to track your monthly expenses, including rent, utilities, groceries, debt payments, and other recurring costs. This will help you understand your cash flow and identify areas where you can potentially reduce expenses.

Step 3: Estimate Car-Related Expenses

Estimate your car-related expenses, including:

- Loan Payment: Use an auto loan calculator to estimate your monthly loan payment based on the car’s price, down payment, interest rate, and loan term.

- Insurance: Get quotes from multiple insurance companies to estimate your monthly insurance costs.

- Fuel: Estimate your monthly fuel costs based on the car’s fuel efficiency and how much you drive.

- Maintenance: Estimate your monthly maintenance costs based on the car’s make and model and your driving habits.

Step 4: Calculate Your Total Car-Related Expenses

Add up your estimated loan payment, insurance costs, fuel costs, and maintenance costs to determine your total car-related expenses each month.

Step 5: Determine the Percentage of Your Income Going to Car Expenses

Divide your total car-related expenses by your gross monthly income and multiply by 100 to determine the percentage of your income going to car expenses.

Step 6: Assess Your Car Affordability

Assess whether your car expenses are within a reasonable range based on your income and financial situation. As a general guideline, your total car-related expenses should not exceed 10-15% of your gross monthly income.

Step 7: Adjust Your Car Budget as Needed

If your car expenses exceed the recommended range, consider adjusting your car budget by:

- Reducing the Car’s Price: Consider buying a less expensive car or a used car.

- Increasing Your Down Payment: Save up for a larger down payment to reduce the loan amount and monthly payments.

- Choosing a Shorter Loan Term: Opt for a shorter loan term to minimize interest costs.

- Shopping for Cheaper Insurance: Get quotes from multiple insurance companies to find the best deal.

- Reducing Fuel Costs: Consider buying a fuel-efficient car or reducing your driving.

- Reducing Maintenance Costs: Take good care of your car to minimize maintenance costs.

By following these steps, you can calculate your car affordability and make informed decisions about car ownership.

4. The Impact of Car Expenses on Your Financial Health

The amount you spend on your car can significantly impact your financial health. High car expenses can strain your budget, limit your ability to save for other goals, and increase your risk of financial problems.

Reduced Savings

High car expenses can reduce the amount of money you have available to save for other goals, such as retirement, education, or a down payment on a home.

Increased Debt

If you can’t afford your car payments, you may have to take on additional debt to cover the costs. This can lead to a cycle of debt that’s difficult to break.

Limited Financial Flexibility

High car expenses can limit your financial flexibility, making it difficult to cope with unexpected expenses or financial emergencies.

Stress and Anxiety

Financial stress can lead to anxiety, depression, and other mental health problems. Keeping your car expenses within a reasonable range can help you reduce financial stress and improve your overall well-being.

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, maintaining reasonable car expenses is crucial for long-term financial well-being.

Opportunity Cost

The money you spend on your car could be used for other investments or opportunities. For example, you could invest in stocks, bonds, or real estate, which could generate income or appreciate in value over time.

By understanding the impact of car expenses on your financial health, you can make informed decisions about car ownership and prioritize your financial goals.

5. Balancing Car Expenses With Other Financial Goals

Balancing car expenses with other financial goals requires careful planning and prioritization. Here are some tips to help you balance car expenses with other financial goals:

Prioritize Your Financial Goals

Identify your most important financial goals, such as retirement, education, or a down payment on a home. Determine how much you need to save each month to achieve these goals.

Create a Budget

Create a detailed budget to track your income and expenses. This will help you understand your cash flow and identify areas where you can potentially reduce expenses.

Set a Car Budget

Set a car budget based on your income and financial goals. Determine how much you can comfortably spend on car-related expenses each month without sacrificing your other financial goals.

Consider Alternative Transportation Options

Explore alternative transportation options, such as public transportation, biking, or walking, to reduce your car expenses.

Shop Around for Car Insurance

Get quotes from multiple insurance companies to compare rates and find the best deal.

Maintain Your Car

Take good care of your car to minimize maintenance costs.

Negotiate a Lower Car Price

Negotiate a lower car price when purchasing a vehicle.

Consider a Used Car

Consider buying a used car instead of a new car to save money.

By following these tips, you can balance car expenses with other financial goals and achieve your financial objectives.

6. Strategies to Reduce Car Expenses

Reducing car expenses can free up money for other financial goals and improve your overall financial health. Here are some strategies to reduce car expenses:

Buy a Used Car

Used cars are typically less expensive than new cars, and they depreciate more slowly. This can save you thousands of dollars over the life of the car.

Choose a Fuel-Efficient Car

Fuel-efficient cars save money on gas. Consider buying a hybrid or electric car to reduce your fuel costs.

Maintain Your Car

Regular maintenance can prevent costly repairs and extend the life of your car. Follow the manufacturer’s recommended maintenance schedule.

Shop Around for Car Insurance

Car insurance rates vary widely. Get quotes from multiple insurance companies to compare rates and find the best deal.

Drive Less

Drive less to save money on gas and reduce wear and tear on your car. Consider alternative transportation options, such as public transportation, biking, or walking.

Carpool

Carpool with coworkers or friends to save money on gas and reduce traffic congestion.

Negotiate a Lower Car Price

Negotiate a lower car price when purchasing a vehicle.

Refinance Your Car Loan

If you have a high-interest car loan, consider refinancing to a lower interest rate. This can save you hundreds or even thousands of dollars over the life of the loan.

Pay Off Your Car Loan Early

Paying off your car loan early can save you money on interest and free up cash flow for other financial goals.

By implementing these strategies, you can reduce your car expenses and improve your overall financial health.

Man calculates monthly car payments

7. The Role of Partnerships in Managing Car-Related Costs

Exploring partnership opportunities can be a strategic approach to managing and even offsetting car-related expenses. Partnerships can take various forms, each offering unique benefits.

Ridesharing Partnerships

- Description: Partnering with ridesharing services like Uber or Lyft to use your vehicle for income generation during your free time.

- Benefits: Earn extra income to cover car payments, insurance, and fuel costs. Flexible hours allow you to work around your schedule.

- Considerations: Requires a reliable vehicle, good driving record, and willingness to work during peak hours.

Delivery Partnerships

- Description: Partnering with food delivery services or courier companies to use your vehicle for delivering goods.

- Benefits: Generate income based on deliveries made. Can be a good option if you prefer driving but not necessarily transporting passengers.

- Considerations: Requires a vehicle suitable for deliveries, knowledge of the area, and ability to meet delivery deadlines.

Advertising Partnerships

- Description: Partnering with local businesses or advertising agencies to display advertisements on your vehicle.

- Benefits: Earn passive income for simply driving your car as usual. Minimal effort required once the advertisement is placed.

- Considerations: May require driving in specific areas or meeting certain mileage requirements.

Carpooling Partnerships

- Description: Partnering with coworkers or neighbors to share rides to work or other destinations.

- Benefits: Save on fuel costs, reduce wear and tear on your vehicle, and decrease traffic congestion.

- Considerations: Requires coordination and communication with partners.

Rental Partnerships

- Description: Partnering with car rental platforms to rent out your vehicle when you’re not using it.

- Benefits: Generate income from your vehicle while it’s sitting idle. Can be a good option if you have a second car or travel frequently.

- Considerations: Requires a reliable vehicle, willingness to share your car with others, and managing rental logistics.

According to Entrepreneur.com, strategic partnerships can significantly reduce the financial burden of car ownership.

How to Find Partnership Opportunities?

- Online Platforms: Explore online platforms that connect drivers with ridesharing, delivery, or advertising opportunities.

- Local Businesses: Reach out to local businesses to inquire about advertising partnerships.

- Community Networks: Connect with coworkers, neighbors, or community groups to explore carpooling opportunities.

By exploring these partnership opportunities, you can find creative ways to manage and offset car-related expenses, improving your financial health and achieving your financial goals.

8. Maximizing Your Income to Afford a Car

If your income is a limiting factor in affording a car, there are several strategies you can implement to increase your income and improve your car affordability:

Get a Raise

- Description: Negotiate a raise with your current employer based on your performance and contributions to the company.

- Benefits: Increase your base salary, providing more disposable income for car-related expenses.

- Considerations: Requires demonstrating your value to the company and negotiating effectively.

Find a Higher-Paying Job

- Description: Look for a higher-paying job in your field or industry.

- Benefits: Significantly increase your income, making it easier to afford a car and other financial goals.

- Considerations: Requires updating your resume, networking, and interviewing skills.

Start a Side Hustle

- Description: Start a side hustle or freelance business to generate additional income.

- Benefits: Flexible hours, potential for high earnings, and opportunity to pursue your passions.

- Considerations: Requires time management, self-discipline, and marketing skills.

Invest in Yourself

- Description: Invest in education, training, or certifications to improve your skills and increase your earning potential.

- Benefits: Long-term career advancement, higher salary, and greater job security.

- Considerations: Requires time and financial investment.

Rent Out Your Assets

- Description: Rent out your spare room, apartment, or other assets to generate passive income.

- Benefits: Relatively passive income stream with minimal effort required.

- Considerations: Requires managing rental logistics and adhering to local regulations.

Sell Unwanted Items

- Description: Sell unwanted items online or at a garage sale to generate quick cash.

- Benefits: Easy way to declutter your home and earn extra money.

- Considerations: Requires time and effort to list and sell items.

Participate in Surveys or Focus Groups

- Description: Participate in online surveys or focus groups to earn small amounts of money.

- Benefits: Easy way to earn extra money in your spare time.

- Considerations: Earnings are typically low.

By implementing these strategies, you can maximize your income and improve your car affordability, making it easier to achieve your financial goals.

9. How to Use Online Tools and Resources for Car Affordability

Online tools and resources can help you make informed decisions about car affordability. These tools can help you estimate loan payments, compare insurance rates, and find deals on cars.

Auto Loan Calculators

Auto loan calculators can help you estimate your monthly loan payment based on the car’s price, down payment, interest rate, and loan term. These calculators can help you determine how much you can afford to spend on a car loan.

Car Insurance Comparison Websites

Car insurance comparison websites can help you compare rates from multiple insurance companies and find the best deal. These websites can save you time and money on car insurance.

Car Price Comparison Websites

Car price comparison websites can help you find deals on new and used cars. These websites can help you compare prices from multiple dealerships and find the best price on the car you want.

Fuel Efficiency Websites

Fuel efficiency websites can help you compare the fuel efficiency of different cars. These websites can help you choose a fuel-efficient car that will save you money on gas.

Credit Score Websites

Credit score websites can help you check your credit score and identify ways to improve it. A higher credit score can help you get a lower interest rate on a car loan.

Budgeting Apps

Budgeting apps can help you track your income and expenses and create a budget. These apps can help you identify areas where you can reduce expenses and save money for a car.

Financial Planning Websites

Financial planning websites can provide information and resources on car affordability and other financial topics. These websites can help you make informed decisions about your finances.

By using these online tools and resources, you can make informed decisions about car affordability and improve your overall financial health.

10. Case Studies: Real-Life Examples of Managing Car Expenses Wisely

Examining real-life examples can provide valuable insights into how others have successfully managed their car expenses wisely.

Case Study 1: The Frugal Commuter

- Background: Sarah, a 28-year-old marketing professional, wanted to buy a car but was concerned about the cost.

- Strategy: Sarah opted for a used car, negotiated a lower price, and shopped around for car insurance. She also carpooled with a coworker to save money on gas.

- Results: Sarah was able to buy a car without straining her budget. She saved money on gas and insurance, and she was able to achieve her other financial goals.

Case Study 2: The Side Hustler

- Background: John, a 35-year-old teacher, needed a car for his commute but had a limited budget.

- Strategy: John started a side hustle delivering pizzas in his spare time. He used the extra income to cover his car payments and insurance costs.

- Results: John was able to afford a car without sacrificing his other financial goals. He also enjoyed the flexibility of his side hustle.

Case Study 3: The Public Transportation Advocate

- Background: Maria, a 40-year-old accountant, lived in a city with good public transportation.

- Strategy: Maria decided to sell her car and use public transportation instead. She saved money on car payments, insurance, gas, and maintenance.

- Results: Maria was able to save a significant amount of money by using public transportation. She also enjoyed the convenience of not having to drive.

Case Study 4: The Car Rental Entrepreneur

- Background: David, a 45-year-old consultant, owned a car that he only used occasionally.

- Strategy: David listed his car on a car rental platform and rented it out when he wasn’t using it. He used the rental income to cover his car payments and insurance costs.

- Results: David was able to offset his car expenses by renting out his car. He also enjoyed the flexibility of being able to use his car when he needed it.

These case studies illustrate that there are many ways to manage car expenses wisely. By considering your individual circumstances and implementing the right strategies, you can afford a car without sacrificing your other financial goals.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Ready to take control of your finances and explore partnership opportunities to boost your income? Visit income-partners.net today to discover strategies for building successful partnerships and achieving your financial goals. Don’t wait—start your journey towards financial freedom now.

FAQ: Navigating Car Affordability

1. What is the 20/4/10 rule?

The 20/4/10 rule is a guideline that recommends making a 20% down payment, financing for no more than four years, and keeping total car expenses below 10% of your gross monthly income. This rule helps manage car costs effectively.

2. Why is my credit score important when buying a car?

Your credit score affects the interest rate you’ll receive on a car loan. A higher score typically means a lower interest rate, saving you money over the loan term.

3. How can I reduce my car insurance costs?

You can reduce car insurance costs by shopping around for quotes, increasing your deductible, and bundling your insurance policies.

4. What are some alternative transportation options to consider?

Alternative transportation options include public transportation, biking, walking, and carpooling.

5. What is the best way to estimate my monthly fuel costs?

Estimate your monthly fuel costs by checking the car’s fuel efficiency rating and multiplying it by your average monthly mileage.

6. How can I negotiate a lower car price?

You can negotiate a lower car price by researching the car’s market value, shopping around for quotes, and being willing to walk away from the deal.

7. What are the benefits of buying a used car?

The benefits of buying a used car include lower purchase price, slower depreciation, and lower insurance costs.

8. How can I increase my income to afford a car?

You can increase your income by getting a raise, finding a higher-paying job, starting a side hustle, or investing in your skills.

9. What is the best way to track my car expenses?

The best way to track your car expenses is to create a budget and use a budgeting app or spreadsheet to track your income and expenses.

10. How can income-partners.net help me manage car expenses?

income-partners.net offers resources and strategies for building successful partnerships, increasing your income, and achieving your financial goals, helping you better manage car expenses.