Figuring out how much of your income a car payment should be is crucial for maintaining financial health while enjoying the convenience of a vehicle. Understanding affordability ensures you’re not overextending yourself financially and allows you to explore partnership opportunities to boost your income with income-partners.net. Let’s explore how to strike the right balance.

1. Determining Your Car Payment Limit

To determine how much of your income should go towards a car payment, start by assessing your overall financial situation. A common rule of thumb is the 20/4/10 rule, where you put down 20%, finance for no more than four years, and keep total car costs below 10% of your gross monthly income.

Understanding the 20/4/10 Rule:

- 20% Down Payment: Paying at least 20% upfront reduces the loan amount and the monthly payments.

- Four-Year Financing: Opting for a loan term of no more than four years helps you pay off the car faster and reduces the total interest paid.

- 10% of Gross Monthly Income: This includes the car payment, insurance, and fuel costs. Staying within this limit ensures that car expenses don’t strain your budget.

This approach ensures that your car expenses are manageable and don’t jeopardize other financial goals. However, this is just a guideline. Let’s dive deeper into how to customize this advice to your specific situation.

2. Calculating Your Car Affordability: A Step-by-Step Guide

Calculating how much car you can afford requires a detailed review of your finances. By following these steps, you can set a realistic budget for your car expenses and avoid overspending.

Step-by-Step Guide:

-

Determine Your Net Income:

- Start with your gross monthly income (total income before taxes and deductions).

- Subtract all taxes, insurance premiums, retirement contributions, and other deductions to find your net monthly income (take-home pay).

-

List Monthly Expenses:

- Include rent or mortgage, utilities, groceries, transportation, debt payments (student loans, credit cards), and entertainment.

- Total these expenses to understand your fixed and variable costs.

-

Calculate Discretionary Income:

- Subtract total monthly expenses from your net monthly income.

- The remaining amount is your discretionary income, which can be used for car payments, savings, and other non-essential spending.

-

Estimate Car-Related Expenses:

- Research the average cost of car insurance in your area.

- Estimate fuel costs based on your driving habits and the fuel efficiency of the car you want.

- Include potential maintenance costs, such as oil changes and tire rotations.

-

Determine Affordable Car Payment Range:

- Calculate 10% of your gross monthly income. This is a general guideline for total car expenses.

- Compare this amount to your discretionary income to ensure your budget can comfortably handle the car payment.

-

Consider Down Payment:

- Determine how much you can put toward a down payment.

- A larger down payment reduces the loan amount and monthly payments.

-

Check Credit Score:

- Review your credit score to understand the interest rates you qualify for.

- A higher credit score typically results in lower interest rates and better loan terms.

-

Use an Online Car Affordability Calculator:

- Input your income, expenses, down payment, and credit score into a car affordability calculator.

- This will provide an estimate of the maximum car price and monthly payment you can afford.

-

Consult Financial Advisor:

- Seek advice from a financial advisor.

- They can provide personalized recommendations based on your financial goals, risk tolerance, and investment plans.

By following these steps, you can create a realistic car budget that aligns with your financial goals and explore partnership opportunities to increase your income with income-partners.net.

3. Monthly Car Payment Calculations

To determine how much you can comfortably allocate to a car payment each month, begin by assessing your net monthly income—the amount you take home after taxes and other deductions. Then, meticulously list all your recurring monthly expenses, including rent, utilities, groceries, insurance, and debt payments. Subtract these expenses from your net income to calculate your discretionary income, which is the amount you have available for non-essential spending.

From your discretionary income, determine how much you can realistically allocate to a car payment without sacrificing other financial goals or necessities. It’s generally recommended that your total car-related expenses, including the car payment, insurance, and fuel, should not exceed 20% of your net monthly income. However, this percentage can vary depending on individual circumstances and financial priorities.

Factors to Consider:

- Income Stability: A reliable, stable income source makes it easier to handle consistent car payments. If your income varies, aim for a lower percentage to accommodate fluctuations.

- Savings Goals: Prioritize your savings, whether for retirement, emergencies, or other long-term goals. Ensure your car payment doesn’t hinder your ability to save adequately.

- Debt Obligations: High debt levels may necessitate a more conservative approach to car payments, freeing up more of your income to tackle existing debts.

4. Calculating Your Monthly Car Payment

To start, calculate your monthly payment potential. Start by gathering your wage or salary information, current bank statements, and records of any monthly or annual expenses. Our team recommends beginning with your post-tax take-home pay, otherwise known as net pay, instead of your annual salary figure or gross pay. Using this reduced figure gives you a more realistic view of what you can afford for a car payment.

Remember to deduct recurring expenses, bills, and other monthly budget items from your take-home pay to reach a low-risk potential monthly payment range. It’s important to be realistic about how long you want to make monthly payments. Most loan companies offer terms between 24 and 84 months for used and new cars. Choosing a longer loan term can help you get lower monthly payments, but you’ll pay more overall because of the additional interest that accumulates.

Longer loan terms also increase your risk of going upside-down on your loan. This happens when borrowers end up owing more on the loan than the vehicle is worth. Since a vehicle’s value decreases over time, weigh your options carefully before choosing which vehicle to purchase.

The table below shows our team’s recommended monthly car payment limits based on your post-tax take home pay per month.

| Monthly Take-Home Pay (Post-Tax) | Monthly Car Payments Should Not Exceed… |

|---|---|

| $1,500 | $150 to $225 per month |

| $3,000 | $300 to $450 per month |

| $4,500 | $450 to $675 per month |

| $6,000 | $600 to $900 per month |

| $7,500 | $750 to $1,125 per month |

| $9,000 | $900 to $1,350 per month |

5. Understanding Fuel and Insurance Costs

Before you purchase or lease a vehicle, consider how much your fuel expenses will be and how much car insurance will cost. Both of these costs depend heavily on your situation, such as your location, driving history, and vehicle type. The U.S. Department of Energy provides a detailed list of fuel economy figures as well as a comparison tool that allows you to check different vehicles’ annual fuel cost estimates.

For auto insurance quotes, reach out to your agent or an insurance company you’re interested in. You can easily get and compare car insurance quotes from companies to get a sense of what you’ll pay. When calculating your monthly car payment and related expenses, try to keep your total costs to less than 20% of your monthly take-home pay.

6. Loan Amount and Term Length

Once you’ve calculated your affordable monthly payment, you can determine how much you can borrow. The amount a lender will let you borrow depends on several factors, including:

- Whether you buy a used or new car: New car loans tend to have lower annual percentage rates (APRs) than used cars.

- Your credit score: This will affect the APR on the loan and how much the bank is willing to lend you.

- Your loan term: This is how many months you’ll have to pay your auto loan off.

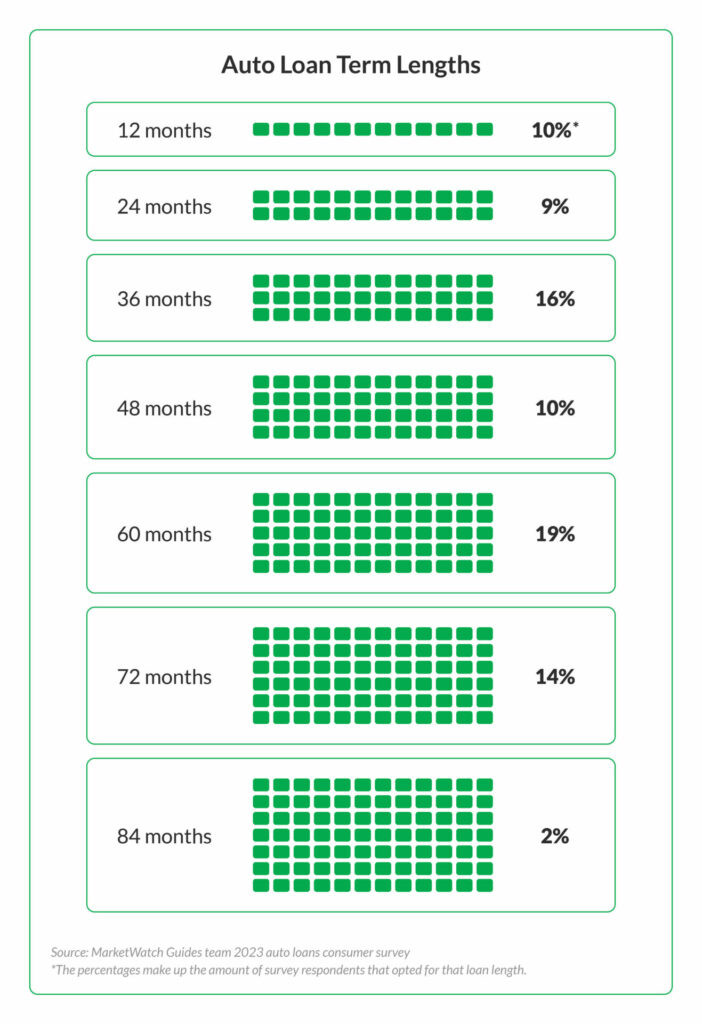

According to our 2023 consumer survey, which questioned 2,000 customers with experiences in auto loans, 19% of respondents had a loan term of 60 months — making 60 months the most popular loan term length in the survey.

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

7. Setting a Purchase Price

The total loan amount you calculated for your car may not be the price you pay. When shopping for a car, pay attention to details other than the sticker price. In most states, you’ll have to pay sales tax and fees whether you buy a new or used car. Making a down payment or trading your old car in can help you borrow less money when purchasing a vehicle.

Here’s a breakdown of how much you can expect to pay in fees or taxes:

- Sales tax: Up to 12.9% and varies by state.

- Registration fees: Typically range from $50 to $300, although some states can be much more expensive.

- Documentation fees: Generally between $100 and $500, depending on your state.

8. Leveraging Partnerships to Increase Affordability

One innovative strategy to enhance your car affordability is through strategic partnerships, which can significantly boost your income. By collaborating with other businesses or individuals, you can create new revenue streams that make your car payments more manageable. Platforms like income-partners.net facilitate these connections, providing opportunities to find partners aligned with your skills and goals.

Types of Partnerships:

- Affiliate Marketing: Partner with companies to promote their products or services, earning a commission for each sale generated through your unique referral link. This can be particularly effective if you have a strong online presence or a niche audience.

- Joint Ventures: Collaborate with another business on a specific project or product, sharing resources and profits. This approach allows you to leverage each other’s expertise and customer base, leading to mutual growth.

- Strategic Alliances: Form a long-term partnership with a complementary business to expand your reach and offer more value to customers. This could involve cross-promotion, shared marketing efforts, or integrating your products or services.

- Referral Programs: Partner with local businesses to refer customers to each other, earning a fee for each successful referral. This can be a simple yet effective way to generate additional income.

- Content Creation Partnerships: Collaborate with other content creators to produce high-quality content that attracts a wider audience. This can involve guest blogging, co-hosting webinars, or creating joint video series.

Finding and Evaluating Potential Partners:

When exploring partnership opportunities, it’s crucial to identify partners whose values, goals, and target market align with yours. Look for businesses that offer complementary products or services and have a solid reputation in their industry. Consider attending industry events, joining online communities, and using professional networking platforms to find potential partners.

Building and Maintaining Successful Partnerships:

Once you’ve identified a suitable partner, establish clear communication channels and set realistic expectations. Define the roles and responsibilities of each party, and create a formal agreement outlining the terms of the partnership. Regularly evaluate the partnership’s performance and make adjustments as needed to ensure mutual benefit and long-term success.

Platforms like income-partners.net can be invaluable in identifying and connecting with potential partners. By leveraging these resources, you can create diverse income streams that not only cover your car payments but also contribute to your overall financial stability and growth.

9. Optimizing Car-Related Expenses

Beyond managing your car payment, there are several ways to optimize your car-related expenses to free up more of your income. These strategies can help you save money on fuel, insurance, and maintenance, making your car more affordable overall.

Strategies for Optimizing Car Expenses:

-

Drive Efficiently:

- Avoid aggressive acceleration and braking, which consume more fuel.

- Maintain a steady speed and use cruise control on highways.

- Combine errands into one trip to reduce unnecessary driving.

-

Maintain Your Vehicle:

- Regularly check tire pressure to improve fuel efficiency.

- Follow the manufacturer’s recommended maintenance schedule, including oil changes and tune-ups.

- Address minor repairs promptly to prevent them from becoming major, costly issues.

-

Shop Around for Insurance:

- Compare quotes from multiple insurance companies to find the best rates.

- Consider increasing your deductible to lower your monthly premiums.

- Inquire about discounts for safe driving, vehicle safety features, or bundling insurance policies.

-

Use Fuel Rewards Programs:

- Join fuel rewards programs offered by gas stations or grocery stores.

- Accumulate points or discounts on fuel purchases to save money over time.

-

Consider Public Transportation:

- Utilize public transportation, such as buses or trains, for commuting or running errands.

- This can significantly reduce your fuel and maintenance costs.

-

Carpool or Rideshare:

- Share rides with colleagues or friends to reduce the number of vehicles on the road.

- Split fuel costs and reduce wear and tear on your car.

-

Refinance Your Auto Loan:

- If interest rates have decreased since you obtained your auto loan, consider refinancing to secure a lower rate.

- This can significantly reduce your monthly payments and overall interest paid.

-

Pay Attention to Fuel Prices:

- Monitor fuel prices in your area.

- Fill up your tank when prices are low to save money.

-

Reduce Vehicle Weight:

- Remove unnecessary items from your car to reduce weight.

- This can improve fuel efficiency and overall performance.

-

Regularly Review Your Car Expenses:

- Review your car-related expenses on a regular basis.

- Identify areas where you can cut back and save money.

10. Making Informed Decisions

Ultimately, determining how much of your income should go towards a car payment requires a holistic assessment of your financial situation, personal priorities, and long-term goals. By considering the guidelines and strategies discussed, you can make informed decisions that align with your financial well-being.

-

Assess Your Financial Situation:

- Begin by evaluating your current financial status.

- Calculate your net monthly income, list your monthly expenses, and assess your debt obligations.

-

Set Clear Financial Goals:

- Define your short-term and long-term financial goals.

- Determine how a car payment fits into your overall financial plan.

-

Consider Your Personal Priorities:

- Reflect on your personal priorities and lifestyle preferences.

- Determine how important having a car is to your daily life.

-

Factor in Unexpected Expenses:

- Account for unexpected expenses.

- This will prevent financial strain.

-

Regularly Review Your Car Budget:

- Review your car budget.

- Adjust as needed.

-

Stay Informed:

- Stay informed about the latest trends in the automotive industry.

- Explore innovative financing options.

-

Seek Professional Advice:

- Consult with a financial advisor.

- Get personalized guidance based on your financial situation and goals.

By making informed decisions and continuously adapting your approach, you can strike a balance between enjoying the convenience of a car and maintaining a healthy financial life.

Search Intent

Here are five search intents for the keyword “How Much Of Your Income Should A Car Payment Be”:

-

Informational: Understanding the recommended percentage of income for car payments. Users want to know the general guidelines or rules of thumb for how much of their income should be allocated to car payments.

-

Budgeting: Finding out how to calculate an affordable car payment based on income. Users are looking for methods or tools to determine a car payment amount that fits within their budget.

-

Financial Planning: Determining the impact of a car payment on overall financial health. Users want to assess how a car payment affects their ability to save, invest, and meet other financial goals.

-

Comparison: Comparing different financial rules or expert advice on car payment affordability. Users are seeking to compare various guidelines or recommendations to make an informed decision.

-

Practical Advice: Getting practical tips for reducing car-related expenses to make payments more manageable. Users are looking for strategies to lower their overall car expenses, such as finding cheaper insurance or saving on fuel.

FAQ: Car Payment Affordability

Here are 10 frequently asked questions (FAQ) related to the keyword “how much of your income should a car payment be”:

-

What percentage of my gross income should I allocate to a car payment?

- A common guideline is the 20/4/10 rule: 20% down payment, finance for no more than four years, and total car costs (including payment, insurance, and fuel) should not exceed 10% of your gross monthly income.

-

How do I calculate an affordable car payment based on my net income?

- Start with your net monthly income (take-home pay) and subtract all monthly expenses. Determine how much of the remaining discretionary income you can comfortably allocate to a car payment without sacrificing other financial goals.

-

Should I include car insurance and fuel costs when determining my car payment budget?

- Yes, it’s essential to include car insurance, fuel costs, and potential maintenance expenses when determining your car budget. Aim for total car-related expenses to be less than 20% of your net monthly income.

-

How does my credit score affect the affordability of my car payment?

- Your credit score significantly impacts the interest rate you’ll receive on an auto loan. A higher credit score typically results in lower interest rates, making your car payment more affordable.

-

What are some strategies to reduce my car-related expenses?

- Strategies include driving efficiently, maintaining your vehicle, shopping around for insurance, using fuel rewards programs, considering public transportation, and refinancing your auto loan.

-

Is it better to buy a new or used car to save money on payments?

- Used cars are typically cheaper upfront and have lower depreciation rates, but new cars may come with better financing options and warranties. Evaluate your budget and long-term needs to make the best decision.

-

How does the length of my auto loan affect my monthly payments?

- Longer loan terms result in lower monthly payments but higher overall interest paid. Shorter loan terms lead to higher monthly payments but lower total interest paid. Choose a loan term that balances affordability and long-term cost.

-

What should I do if I’m struggling to afford my car payment?

- Options include refinancing your auto loan, selling your car and buying a cheaper one, negotiating with your lender, or seeking financial counseling.

-

How can income-partners.net help me afford my car payment?

- income-partners.net can connect you with partnership opportunities to increase your income, making your car payment more manageable. Explore collaborations such as affiliate marketing, joint ventures, or strategic alliances.

-

Are there any online tools or calculators to help me determine an affordable car payment?

- Yes, many online car affordability calculators can estimate the maximum car price and monthly payment you can afford based on your income, expenses, down payment, and credit score.

By addressing these frequently asked questions, you can gain a comprehensive understanding of car payment affordability and make informed decisions that align with your financial goals.