How Much Is A Comfortable Retirement Income, and how can you achieve it? Determining your ideal retirement income involves careful planning and understanding your financial needs. At income-partners.net, we help you explore partnership opportunities and strategies to boost your retirement savings and secure your financial future. Let’s dive in and find out how to make your retirement dreams a reality! Retirement planning, financial security, and income strategies are essential for a comfortable retirement.

1. Understanding the Retirement Income Landscape

The common question isn’t about having a specific amount of savings. It’s about whether you can generate sufficient income to support your desired lifestyle post-retirement. Will a $1 million savings balance create enough income forever?

Financial planners often suggest replacing approximately 80% of your pre-retirement income to maintain your current lifestyle after retirement. For instance, if you currently earn $100,000 annually, you should aim for at least $80,000 in retirement income (in today’s dollars). However, this is a general guideline, and several factors can influence the actual amount you’ll need.

Image illustrating retirement planning with various financial elements

Image illustrating retirement planning with various financial elements

1.1. Why 80% Might Not Always Be Enough

Retiring on 80% of your annual income may not be ideal for everyone. Adjust your goal based on your planned retirement lifestyle and whether your expenses will significantly change. If you plan to travel frequently, you might need 90% to 100% of your pre-retirement income. Conversely, if you pay off your mortgage or downsize, you might live comfortably on less than 80%.

1.2. Estimating Your Retirement Income Needs

Consider a hypothetical couple with a current annual income of $120,000. Following the 80% principle, they can expect to need approximately $96,000 annually or $8,000 per month in retirement income.

2. Factors Influencing Your Retirement Income

Several factors determine how much income you need to retire comfortably.

2.1. Reduced Expenses

One reason you don’t need to replace 100% of your pre-retirement income is that certain expenses typically decrease or disappear altogether:

- Retirement Savings: You no longer need to save for retirement.

- Work-Related Costs: Commuting expenses and other work-related costs are eliminated.

- Mortgage: You may have paid off your mortgage by retirement.

- Life Insurance: If you no longer have dependents, life insurance may not be necessary.

2.2. Lifestyle Choices

Your desired lifestyle significantly impacts your retirement income needs. Those planning extensive travel or luxurious living arrangements will need more income than those preferring a simpler lifestyle.

2.3. Healthcare Costs

Healthcare expenses often increase with age. Plan for potential medical costs, including insurance premiums, co-pays, and long-term care.

2.4. Inflation

Inflation erodes the purchasing power of your savings. Account for inflation to ensure your retirement income maintains its value over time.

2.5. Unexpected Expenses

Prepare for unexpected costs such as home repairs, car maintenance, or unforeseen medical bills.

3. Diversifying Income Sources for Retirement

Relying solely on savings can be risky. Diversifying your income sources ensures a more stable and secure retirement.

3.1. Social Security Benefits

For many, Social Security is a crucial income source. However, the percentage of income replaced by Social Security is typically lower for higher-income retirees. For instance, Fidelity estimates that Social Security may replace 35% of income for someone earning $50,000 per year, but only 11% for someone earning $300,000 per year.

To estimate your benefits, check your Social Security statement or create a my Social Security account

3.2. Pensions

If you have pensions from current or former jobs, factor these into your income projections. Pensions provide a steady, predictable income stream.

3.3. Annuities

Annuities can provide a guaranteed income stream in retirement. Consider both fixed and variable annuities based on your risk tolerance and financial goals.

3.4. Part-Time Work

Working part-time can supplement your retirement income, provide mental stimulation, and keep you socially engaged.

3.5. Investments

A well-diversified investment portfolio can generate income through dividends, interest, and capital gains. Consult a financial advisor to create a portfolio aligned with your risk tolerance and retirement goals.

3.6. Real Estate

Rental income from real estate investments can provide a steady income stream. Consider the responsibilities and potential costs associated with property management.

Continuing with our example, if each spouse anticipates $1,500 monthly from Social Security, and one spouse receives a $1,000 monthly pension, the couple has $4,000 in guaranteed monthly income. The remaining $4,000 must come from savings and investments.

4. Estimating Your Retirement Savings

After determining your income needs, estimate the savings required to generate that income. A retirement calculator can help, or you can use the “4% rule.”

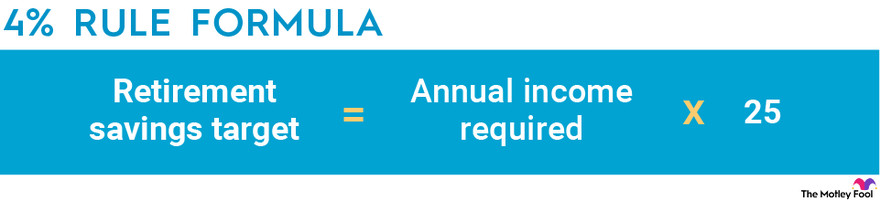

4.1. The 4% Rule

The 4% rule suggests withdrawing 4% of your retirement savings in the first year of retirement. In subsequent years, adjust this amount for cost-of-living increases. This rule aims to ensure your money lasts at least 30 years.

According to research from the University of Texas at Austin’s McCombs School of Business, the 4% rule is a good starting point, but it’s essential to adjust your withdrawal rate based on market conditions and personal circumstances.

Image illustrating the 4% rule with calculations

Image illustrating the 4% rule with calculations

To calculate your retirement savings target using the 4% rule, use this formula:

Retirement Savings Target = Annual Income Needed From Savings / 0.04

If the couple needs $4,000 per month ($48,000 annually) from their savings, they should aim for $1.2 million in retirement savings accounts like a 401(k) or IRA.

4.2. Limitations of the 4% Rule

The 4% rule has flaws. It assumes consistent annual withdrawals adjusted for inflation and a portfolio split between stocks and bonds. You may need to withdraw more or less based on market conditions.

4.3. Market Volatility

Recent market volatility highlights the need for retirees to have cash on hand. This buffer helps avoid cashing out investments during market downturns.

5. Retirement Plans and Taxation

Not all retirement plans are created equal regarding income and taxation.

5.1. Traditional IRA and 401(k)

Withdrawals from a traditional IRA or 401(k) are considered taxable income.

5.2. Roth IRA and 401(k)

Withdrawals from a Roth IRA or Roth 401(k) are generally tax-free, which can significantly impact your retirement income.

5.3. Early Retirement Considerations

Many workers retire earlier than planned due to layoffs, health issues, or caregiving responsibilities. Saving for a longer retirement provides a safety cushion.

5.4. Inflation Impact

Inflation disproportionately affects senior households because they spend a larger portion of their income on healthcare and housing, which tend to increase faster than the overall inflation rate.

6. Partnering for Retirement Success with income-partners.net

To achieve a comfortable retirement income, consider strategic partnerships that can enhance your financial security. income-partners.net offers a platform to explore various partnership opportunities tailored to your goals.

6.1. Strategic Business Partnerships

Partnering with other businesses can create new revenue streams and expand your income potential. This can be particularly beneficial for entrepreneurs and business owners looking to scale their operations.

6.2. Investment Partnerships

Collaborating with investment partners can diversify your portfolio and increase your returns. income-partners.net connects you with potential partners who share your investment philosophy.

6.3. Real Estate Partnerships

Joining forces with real estate partners can help you invest in properties that generate passive income. This can be a valuable addition to your retirement income strategy.

6.4. Financial Planning Partnerships

Working with financial planning partners ensures you have a comprehensive retirement plan tailored to your specific needs. These partnerships offer expert guidance and support to help you navigate the complexities of retirement planning.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

7. Real-Life Examples of Successful Retirement Income Strategies

Several individuals have successfully navigated retirement planning by diversifying their income sources and leveraging strategic partnerships.

7.1. Case Study: Diversified Investment Portfolio

John, a former engineer, retired at 62 with a diversified investment portfolio that included stocks, bonds, and real estate. His portfolio generated a steady income stream that supplemented his Social Security benefits and allowed him to travel extensively.

7.2. Case Study: Part-Time Consulting

Maria, a retired teacher, started a part-time consulting business that provided her with additional income and a sense of purpose. Her consulting work not only supplemented her retirement savings but also kept her mentally and socially engaged.

7.3. Case Study: Real Estate Investments

David and Sarah, a retired couple, invested in rental properties that generated passive income. Their real estate investments provided a stable income stream and helped them achieve their retirement goals.

8. Expert Insights on Retirement Planning

Consulting with financial experts can provide valuable insights and guidance for retirement planning.

8.1. Financial Advisors

Financial advisors can help you create a personalized retirement plan, manage your investments, and navigate the complexities of retirement income.

8.2. Retirement Planning Seminars

Attending retirement planning seminars can provide valuable information and strategies for maximizing your retirement income.

8.3. Online Resources

Numerous online resources offer guidance and tools for retirement planning. Websites like income-partners.net provide valuable information and connect you with potential partners.

9. The Importance of Ongoing Financial Monitoring

Retirement planning is not a one-time event but an ongoing process. Regularly monitor your financial situation, adjust your strategies as needed, and stay informed about market trends and economic conditions.

9.1. Annual Financial Review

Conduct an annual review of your financial situation to assess your progress toward your retirement goals and make any necessary adjustments.

9.2. Investment Portfolio Review

Regularly review your investment portfolio to ensure it aligns with your risk tolerance and retirement goals.

9.3. Stay Informed

Stay informed about changes in tax laws, Social Security benefits, and other factors that may impact your retirement income.

10. Taking Action: Steps to Secure Your Retirement Income

Securing a comfortable retirement income requires proactive planning and action.

10.1. Set Clear Retirement Goals

Define your retirement goals, including your desired lifestyle, expenses, and income needs.

10.2. Create a Retirement Plan

Develop a comprehensive retirement plan that outlines your savings, investments, and income strategies.

10.3. Diversify Your Income Sources

Diversify your income sources to ensure a stable and secure retirement.

10.4. Seek Professional Guidance

Consult with financial advisors and other experts to gain valuable insights and guidance.

10.5. Monitor Your Progress

Regularly monitor your financial situation and adjust your strategies as needed.

10.6. Explore Partnership Opportunities

Explore partnership opportunities on income-partners.net to enhance your financial security and achieve your retirement goals.

11. Understanding the Nuances of Social Security Benefits

Social Security can be a cornerstone of retirement income, but maximizing these benefits requires a strategic approach.

11.1. Factors Affecting Social Security Benefits

The amount you receive from Social Security depends on several factors, including your earnings history, the age at which you begin claiming benefits, and your marital status.

11.2. Claiming Strategies

Deciding when to claim Social Security benefits is a crucial decision. Claiming early (at age 62) reduces your monthly benefit, while delaying until age 70 increases it. According to AARP, delaying benefits can significantly boost your retirement income.

11.3. Spousal Benefits

Spousal benefits allow individuals to claim benefits based on their spouse’s earnings history, even if they have little or no earnings themselves.

11.4. Survivor Benefits

Survivor benefits provide income to surviving spouses and dependents after a worker’s death.

12. Managing Healthcare Costs in Retirement

Healthcare costs are a significant concern for retirees. Planning for these expenses is essential for maintaining financial stability.

12.1. Medicare

Medicare is a federal health insurance program for individuals aged 65 and older. Understanding the different parts of Medicare (A, B, C, and D) is crucial for choosing the right coverage.

12.2. Medigap Policies

Medigap policies, also known as Medicare Supplement Insurance, help cover some of the costs that Original Medicare doesn’t, such as copayments, coinsurance, and deductibles.

12.3. Long-Term Care Insurance

Long-term care insurance helps cover the costs of long-term care services, such as nursing home care, assisted living, and home healthcare.

12.4. Health Savings Accounts (HSAs)

If you have a high-deductible health plan, you can contribute to a Health Savings Account (HSA). These accounts offer tax advantages and can be used to pay for qualified medical expenses.

13. Navigating Estate Planning and Legacy Goals

Estate planning is an essential part of retirement planning. It ensures your assets are distributed according to your wishes and can provide for your loved ones after your death.

13.1. Wills

A will is a legal document that specifies how your assets should be distributed after your death.

13.2. Trusts

Trusts are legal arrangements that allow you to transfer assets to beneficiaries while maintaining control over how those assets are managed.

13.3. Power of Attorney

A power of attorney is a legal document that authorizes someone to act on your behalf in financial or medical matters if you become incapacitated.

13.4. Legacy Planning

Legacy planning involves defining your values and goals and ensuring they are reflected in your estate plan.

14. Addressing Common Retirement Concerns

Many individuals have concerns about retirement, such as outliving their savings, inflation, and healthcare costs. Addressing these concerns requires proactive planning and informed decision-making.

14.1. Outliving Savings

To mitigate the risk of outliving your savings, consider strategies such as delaying retirement, working part-time, and diversifying your income sources.

14.2. Inflation

Protect your retirement income from inflation by investing in assets that tend to increase in value over time, such as stocks and real estate.

14.3. Healthcare Costs

Plan for healthcare costs by enrolling in Medicare, purchasing Medigap insurance, and considering long-term care insurance.

14.4. Market Volatility

Manage market volatility by diversifying your investment portfolio and maintaining a cash reserve.

15. The Role of Financial Technology in Retirement Planning

Financial technology (FinTech) offers numerous tools and resources for retirement planning.

15.1. Online Retirement Calculators

Online retirement calculators can help you estimate your retirement income needs and savings goals.

15.2. Robo-Advisors

Robo-advisors provide automated investment management services based on your risk tolerance and financial goals.

15.3. Budgeting Apps

Budgeting apps can help you track your expenses, manage your budget, and save for retirement.

15.4. Investment Tracking Tools

Investment tracking tools allow you to monitor your portfolio performance and make informed investment decisions.

Securing a comfortable retirement income is achievable with careful planning, diversification, and strategic partnerships. income-partners.net offers resources and connections to help you navigate the complexities of retirement planning and achieve your financial goals.

16. Exploring Government Resources for Retirement Planning

Several government agencies offer resources and information to assist with retirement planning.

16.1. Social Security Administration (SSA)

The SSA provides information about Social Security benefits, eligibility requirements, and claiming strategies.

16.2. Centers for Medicare & Medicaid Services (CMS)

CMS provides information about Medicare, Medicaid, and other healthcare programs.

16.3. Department of Labor (DOL)

The DOL provides information about retirement plans, employee benefits, and retirement savings.

16.4. Internal Revenue Service (IRS)

The IRS provides information about retirement plan tax rules, deductions, and credits.

17. Adapting to Life Changes in Retirement

Retirement is a time of significant life changes. Adapting to these changes is essential for maintaining your well-being and enjoying a fulfilling retirement.

17.1. Maintaining Social Connections

Stay connected with friends, family, and community groups to maintain social connections and combat loneliness.

17.2. Pursuing Hobbies and Interests

Pursue hobbies and interests to stay mentally and physically active.

17.3. Volunteering

Volunteering provides a sense of purpose and allows you to give back to your community.

17.4. Staying Physically Active

Regular exercise is essential for maintaining your physical health and well-being.

18. The Impact of Tax Planning on Retirement Income

Tax planning plays a crucial role in maximizing your retirement income. Understanding the tax implications of different retirement accounts and investment strategies is essential for minimizing your tax burden.

18.1. Tax-Advantaged Retirement Accounts

Take advantage of tax-advantaged retirement accounts, such as 401(k)s, IRAs, and HSAs, to reduce your taxable income and grow your savings.

18.2. Tax-Efficient Investment Strategies

Implement tax-efficient investment strategies, such as tax-loss harvesting and asset location, to minimize your tax liability.

18.3. Roth Conversions

Consider converting traditional retirement accounts to Roth accounts to pay taxes now and avoid paying taxes on future withdrawals.

18.4. Working with a Tax Professional

Consult with a tax professional to develop a comprehensive tax plan that aligns with your retirement goals.

19. Understanding the Different Types of Retirement Plans

Choosing the right retirement plan is crucial for maximizing your savings and achieving your retirement goals.

19.1. 401(k) Plans

401(k) plans are employer-sponsored retirement plans that allow employees to save and invest for retirement.

19.2. Traditional IRAs

Traditional IRAs are individual retirement accounts that allow individuals to save and invest for retirement on a tax-deferred basis.

19.3. Roth IRAs

Roth IRAs are individual retirement accounts that allow individuals to save and invest for retirement on a tax-free basis.

19.4. Simplified Employee Pension (SEP) IRAs

SEP IRAs are retirement plans for self-employed individuals and small business owners.

19.5. Savings Incentive Match Plan for Employees (SIMPLE) IRAs

SIMPLE IRAs are retirement plans for small businesses that offer a simple and cost-effective way to save for retirement.

20. Utilizing income-partners.net for Retirement Success

income-partners.net offers a wealth of resources and opportunities to help you achieve a comfortable and secure retirement.

20.1. Connecting with Financial Experts

income-partners.net connects you with financial advisors and other experts who can provide personalized guidance and support.

20.2. Exploring Partnership Opportunities

income-partners.net offers a platform to explore various partnership opportunities that can enhance your financial security and increase your retirement income.

20.3. Accessing Valuable Resources

income-partners.net provides access to valuable resources, such as articles, guides, and tools, to help you navigate the complexities of retirement planning.

20.4. Building a Supportive Community

income-partners.net fosters a supportive community where you can connect with other individuals who are also planning for retirement.

FAQ: How Much Do I Need to Retire?

How much money do you realistically need to retire?

You realistically need enough money to replace about 80% of your income in retirement. That money does not need to come from savings alone; Social Security income, pensions, and part-time work can supplement your retirement income.

Can I retire at 60 with $500K?

Retiring at 60 with $500,000 is possible but depends on your goals, Social Security income, and debts. The 4% withdrawal rule suggests you could withdraw $20,000 annually from investments. Factor in healthcare costs and potential early Social Security access.

What is the average 401(k) balance for a 65-year-old?

According to Vanguard’s How America Saves 2024 report, the average 401(k) balance for savers 65 and older without an outstanding loan was $282,669.

What is the $1,000-a-month rule for retirement?

The $1,000-a-month rule for retirement means saving $240,000 for every $1,000 of monthly retirement income, assuming a 5% annual withdrawal rate. For $4,000 monthly, aim for $960,000 in savings.

How can I increase my retirement income?

You can increase your retirement income by diversifying income sources, such as Social Security, pensions, investments, part-time work, and real estate. Additionally, partnering with strategic businesses or investment partners can provide new revenue streams.

What are the key factors to consider when planning for retirement income?

Key factors to consider include lifestyle choices, healthcare costs, inflation, and unexpected expenses. Also, plan for market volatility and understand the tax implications of different retirement plans.

How does inflation affect my retirement income?

Inflation erodes the purchasing power of your savings, so it’s crucial to account for inflation to ensure your retirement income maintains its value over time. Senior households often face higher inflation rates due to increased spending on healthcare and housing.

What are the benefits of a Roth IRA compared to a traditional IRA?

A Roth IRA offers tax-free withdrawals in retirement, while traditional IRA withdrawals are taxed as income. Roth IRAs can be beneficial if you anticipate being in a higher tax bracket during retirement.

How can income-partners.net help me plan for retirement?

income-partners.net helps you explore partnership opportunities tailored to your goals, connects you with financial experts, and provides valuable resources for retirement planning. It offers a platform to explore various partnerships that can enhance your financial security and increase your retirement income.

What is the 4% rule, and how does it work?

The 4% rule suggests withdrawing 4% of your retirement savings in the first year of retirement, adjusting this amount for cost-of-living increases in subsequent years. It’s designed to ensure your money lasts at least 30 years, but it’s essential to adjust your withdrawal rate based on market conditions and personal circumstances.

Planning for a comfortable retirement income requires careful consideration of various factors, proactive planning, and a diversified approach. With the right strategies and resources, you can achieve your retirement goals and enjoy a financially secure future. Remember, it’s not just about how much you save, but how effectively you manage your income streams to support your desired lifestyle.