How much income would $1 million generate in the UK? A $1 million nest egg might seem like a fortune, but understanding its income potential in the UK is crucial for retirement planning; income-partners.net can help you navigate the complexities of generating income from your savings and find the best strategies for your financial goals. We’ll explore annuities, drawdown options, and smart investment strategies to maximize your returns and provide financial security. Turn your million into a reliable income stream with expert partnership insights.

1. How Much Income Can $1 Million Generate in the UK Through Annuities?

Annuities can be a solid choice for those seeking a guaranteed income stream. By exchanging your $1 million for an annuity, you essentially receive a lifelong income from an insurance company. The specifics depend on several factors.

Factors Influencing Annuity Rates

- Age: Older individuals generally receive higher annuity rates because the insurer anticipates a shorter payout period.

- Health: If you have health issues, you might qualify for an enhanced annuity, offering a higher income to reflect a potentially shorter life expectancy.

- Inflation Protection: Opting for an annuity that increases with inflation will reduce your initial income but protect your purchasing power over time.

- Survivor Benefits: Choosing to have the income continue to your spouse after your death will also lower the initial payout.

Estimating Annuity Income

Based on current market conditions, a $1 million annuity purchased at age 65 might generate roughly £40,000 to £50,000 per year. However, remember that these figures can fluctuate significantly. For example, interest rates and insurer policies can change. It’s essential to obtain personalized quotes to see precisely how much income your $1 million could produce.

While annuities offer security, they have drawbacks. One major disadvantage is the lack of flexibility. Once set up, you can’t change the income amount, which might be problematic if your needs evolve. Additionally, the default option often doesn’t account for inflation, which means your income’s value decreases over time. Finally, many annuities stop payments upon your death, leaving no inheritance for your beneficiaries unless you specifically opt for survivor benefits, which reduces your income.

2. What Income Can $1 Million Generate in the UK Through Pension Drawdown?

Pension drawdown provides more control and flexibility compared to annuities. With drawdown, your $1 million remains invested, and you can withdraw as much or as little as you need, whenever you need it.

Advantages of Pension Drawdown

- Flexibility: Adjust your income to suit your needs, increasing or decreasing withdrawals as required.

- Investment Growth: Your pension remains invested, offering the potential for growth and a higher income over time.

- Tax Efficiency: Manage withdrawals to minimize your tax liability.

- Death Benefits: Unspent funds can be passed on to your beneficiaries, often tax-free.

Pension Drawdown Tax Efficiency

Pension Drawdown Tax Efficiency

Estimating Drawdown Income

A commonly cited guideline for sustainable withdrawals is the 4% rule. This suggests that you can withdraw 4% of your pension in the first year of retirement and then adjust that amount for inflation in subsequent years without running out of money for at least 30 years. Based on this rule, a $1 million pension pot could generate an initial income of $40,000 per year.

However, drawdown comes with risks. Taking out too much too quickly can deplete your funds prematurely. Investment volatility and the sequence of returns can also impact the longevity of your pension. According to research from the University of Texas at Austin’s McCombs School of Business, a poor sequence of returns early in retirement can significantly reduce your pension’s lifespan, even if average returns are favorable over the long term.

3. How Does the 4% Rule Apply to a $1 Million Pension in the UK?

The 4% rule is a popular guideline for retirement spending, but it’s crucial to understand its limitations. The rule suggests that you can withdraw 4% of your initial retirement pot in the first year and then adjust subsequent withdrawals for inflation.

Calculating Initial Withdrawal

With a $1 million pension, the initial withdrawal would be $40,000. This amount is then adjusted annually to account for inflation, ensuring your purchasing power remains consistent.

Limitations of the 4% Rule

- Sequence of Returns Risk: The order in which your investments generate returns can significantly impact your pension’s sustainability. Poor returns early in retirement can deplete your fund faster.

- Market Volatility: The rule assumes consistent investment performance, which is rarely the case. Market downturns can force you to withdraw a larger percentage of your remaining funds, accelerating depletion.

- Inflation Fluctuations: Unexpectedly high inflation can erode your purchasing power more quickly than anticipated.

Example Scenarios

| Scenario | Year 1 Return | Year 2 Return | Year 3 Return | Year 4 Return | Year 5 Return | Result |

|---|---|---|---|---|---|---|

| Scenario A | 10% | 12% | 8% | -5% | -10% | Pension lasts longer due to strong initial returns. |

| Scenario B | -10% | -5% | 8% | 12% | 10% | Pension depletes faster due to poor initial returns. |

| Scenario C | 5% | 5% | 5% | 5% | 5% | Pension lasts a predictable amount of time due to consistent returns. |

According to BlackRock, the sequence of returns risk is a critical factor in retirement planning. Even with the same average annual returns, the order in which those returns occur can significantly impact the longevity of your pension.

4. What Strategies Can Extend the Life of a $1 Million Pension in the UK?

To mitigate the risks associated with drawdown and the 4% rule, consider implementing strategies designed to extend the life of your pension.

Bucketing Strategy

Divide your assets into three buckets based on your time horizon:

- Short-Term Bucket: Holds one year’s worth of income in cash to cover immediate needs.

- Medium-Term Bucket: Invested in a mix of low- and medium-risk investments to provide income for the next 3-7 years.

- Long-Term Bucket: Invested in higher-growth investments to maximize returns over a longer time horizon.

This strategy helps protect against sequence of returns risk by ensuring you don’t need to sell investments during market downturns.

Dynamic Withdrawal Strategy

Adjust your withdrawal rate based on market conditions and your portfolio’s performance. Withdraw less during downturns and more during periods of strong growth. This approach requires careful monitoring and a willingness to adapt your spending.

Cash Flow Modeling

Develop a detailed cash flow model that projects your income, expenses, and investment returns over your retirement. This allows you to stress-test different scenarios and identify potential shortfalls. According to Professional Paraplanner, cash flow modeling helps clients better understand their finances and make informed decisions.

Diversification

Diversify your investment portfolio across different asset classes, sectors, and geographies to reduce risk. This can help cushion the impact of market volatility and improve your overall returns.

5. What Role Does Investment Volatility Play in a $1 Million Pension’s Longevity?

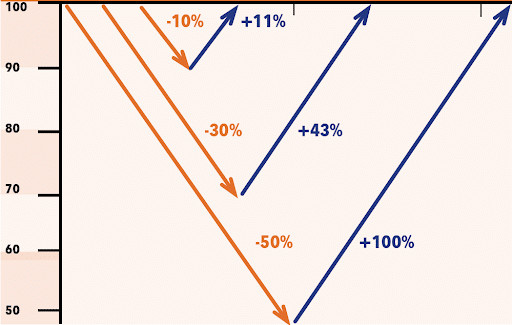

Investment volatility can significantly impact the longevity of your pension. The concept of “volatility drag” illustrates how losses can be more damaging than gains are beneficial.

Understanding Volatility Drag

Imagine your pension falls by 30%. To recover to the original value, it needs to increase by 43%. This is because the base value is lower after the loss.

Impact on Retirement Planning

Volatility drag is particularly problematic in retirement because withdrawals exacerbate the effects of losses. When your investments decline, you need to sell more units to maintain your income, locking in losses and making it harder to recover.

Mitigating Volatility

- Lower-Risk Investments: Allocate a portion of your portfolio to lower-risk assets like bonds and cash.

- Bucketing Strategy: As mentioned earlier, this helps insulate your short-term income needs from market fluctuations.

- Regular Rebalancing: Rebalance your portfolio periodically to maintain your desired asset allocation.

Volatility Drag Illustration

Volatility Drag Illustration

6. How Can Cash Flow Modeling Help Plan for a $1 Million Pension in the UK?

Cash flow modeling is a powerful tool for retirement planning. It provides a comprehensive forecast of your finances, allowing you to see whether you are on track to meet your goals.

Benefits of Cash Flow Modeling

- Realistic Projections: Create realistic projections of your income, expenses, and investment returns.

- Scenario Planning: Stress-test different scenarios, such as market downturns, unexpected expenses, or changes in inflation.

- Informed Decisions: Make informed decisions about your withdrawal rate, investment strategy, and retirement age.

- Visual Representation: See a visual representation of your finances, making it easier to understand your current situation and future prospects.

Example Scenarios

- Early Retirement: See how retiring earlier would impact your pension’s longevity.

- Increased Spending: Evaluate the effect of increasing your spending on travel or hobbies.

- Unexpected Expenses: Assess the impact of unexpected medical bills or home repairs.

By understanding the potential impact of these scenarios, you can make adjustments to your plan and increase your chances of a successful retirement.

7. How Can a Financial Advisor Help Maximize Income from a $1 Million Pension in the UK?

A financial advisor can provide valuable guidance and support in maximizing the income from your $1 million pension.

Benefits of Working with a Financial Advisor

- Personalized Advice: Receive personalized advice tailored to your specific circumstances, goals, and risk tolerance.

- Investment Management: Benefit from professional investment management, including asset allocation, diversification, and rebalancing.

- Withdrawal Strategies: Develop a sustainable withdrawal strategy that balances your income needs with the longevity of your pension.

- Tax Planning: Optimize your withdrawals to minimize your tax liability.

- Ongoing Monitoring: Receive ongoing monitoring and adjustments to your plan as your needs and market conditions change.

Finding the Right Advisor

- Experience: Look for an advisor with experience in retirement planning and pension drawdown.

- Qualifications: Ensure the advisor holds relevant qualifications, such as Chartered Financial Planner.

- Independent: Choose an independent advisor who can provide unbiased advice.

- Fees: Understand the advisor’s fee structure and how they are compensated.

8. What Are the Tax Implications of Drawing Income from a $1 Million Pension in the UK?

Understanding the tax implications of drawing income from your pension is essential for maximizing your returns.

Tax-Free Cash

You can typically withdraw up to 25% of your pension pot tax-free. This lump sum can be used for any purpose, such as paying off debt, making home improvements, or funding a special purchase.

Income Tax

Any income you withdraw above the tax-free cash is subject to income tax at your marginal rate. The amount of tax you pay will depend on your total income and tax bracket.

Tax Planning Strategies

- Phased Withdrawals: Spread your withdrawals over several years to minimize your tax liability.

- Pension Contributions: Continue making pension contributions to reduce your taxable income.

- Utilize Allowances: Take advantage of your personal allowance and other tax-free allowances.

Example Scenario

If you withdraw £50,000 from your pension and have a personal allowance of £12,570, you will pay income tax on £37,430. The tax you pay will depend on your tax bracket.

9. What Are the Alternatives to Annuities and Drawdown for Generating Income from $1 Million in the UK?

While annuities and drawdown are the most common options for generating income from a pension, other alternatives may be suitable for some individuals.

Buy-to-Let Property

Investing in buy-to-let property can provide rental income. However, this requires significant capital, ongoing management, and carries risks such as void periods and tenant issues.

Dividend-Paying Stocks

Investing in dividend-paying stocks can generate a regular income stream. However, dividends are not guaranteed and can fluctuate depending on the company’s performance.

Peer-to-Peer Lending

Peer-to-peer lending involves lending money to individuals or businesses through an online platform. This can offer higher returns than traditional savings accounts, but also carries a higher risk of default.

Commercial Property

Investing in commercial property can provide a higher rental yield than residential property. However, it requires significant capital and carries risks such as longer void periods and higher maintenance costs.

10. How Does Location Impact the Sustainability of a $1 Million Pension in the UK?

Your location within the UK can impact the sustainability of your pension due to variations in the cost of living.

Regional Cost of Living Differences

- London: London has the highest cost of living in the UK, particularly for housing. This means your $1 million pension may not stretch as far in London as it would in other regions.

- Southeast: The Southeast of England also has a relatively high cost of living, particularly for housing.

- Northern England: Northern England generally has a lower cost of living, particularly for housing.

- Scotland, Wales, and Northern Ireland: These regions also tend to have a lower cost of living than London and the Southeast.

Example Scenario

If you plan to retire in London, you may need a larger pension pot to maintain the same standard of living as someone retiring in Northern England.

Mitigating Location Costs

- Downsize: Consider downsizing to a smaller property or moving to a less expensive area.

- Budgeting: Create a detailed budget to track your expenses and identify areas where you can save money.

- Part-Time Work: Consider working part-time to supplement your pension income.

Navigating the complexities of generating income from your savings can be daunting, but with the right strategies and guidance, you can achieve financial security and enjoy a comfortable retirement. Visit income-partners.net today to explore your partnership options and start building a brighter financial future. Our resources can help you connect with potential partners, develop effective relationship strategies, and uncover new opportunities for income growth. Don’t wait—discover the power of partnership today. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

FAQ: Generating Income from $1 Million in the UK

1. Is $1 million enough to retire comfortably in the UK?

It depends on your lifestyle and spending habits. A $1 million pension pot can provide a comfortable retirement for some, but not for others.

2. How much income can I expect from a $1 million annuity?

A $1 million annuity might generate roughly £40,000 to £50,000 per year, but this can vary based on age, health, and other factors.

3. What is the 4% rule?

The 4% rule suggests withdrawing 4% of your initial retirement pot in the first year and then adjusting subsequent withdrawals for inflation.

4. What are the risks of pension drawdown?

Risks include running out of money too soon, investment volatility, and the sequence of returns risk.

5. How can I extend the life of my pension pot?

Strategies include the bucketing strategy, dynamic withdrawal strategy, and cash flow modeling.

6. What is volatility drag?

Volatility drag is the phenomenon where losses can be more damaging than gains are beneficial.

7. How can a financial advisor help me?

A financial advisor can provide personalized advice, investment management, and tax planning.

8. What are the tax implications of drawing income from my pension?

You can typically withdraw up to 25% of your pension pot tax-free, but any income above that is subject to income tax.

9. What are the alternatives to annuities and drawdown?

Alternatives include buy-to-let property, dividend-paying stocks, and peer-to-peer lending.

10. How does location impact the sustainability of my pension?

Your location can impact the sustainability of your pension due to variations in the cost of living.