Affording a $3 million house requires a strategic approach to income, debt, and financial planning, and income-partners.net is here to guide you. Discover realistic income benchmarks, explore partnership opportunities to boost your earnings, and learn how to confidently navigate the luxury real estate market with financial stability and smart partnerships. Let’s explore the path to homeownership and financial success with sound strategies and potential collaborations.

Table of Contents

- Understanding the $3 Million Home Dream

- The Golden Rule: Income-to-Home Price Ratio

- Minimum Income Threshold: The Bare Necessities

- Factors Influencing Affordability

- The Hidden Costs of Owning a Luxury Home

- Smart Strategies for Boosting Your Income

- Real-Life Scenarios: Family Budgets and Homeownership

- Location Matters: Housing Market Risks and Opportunities

- Alternative Investments: Diversifying Your Portfolio

- Partnering for Success: How Income-Partners.net Can Help

- Frequently Asked Questions (FAQ)

1. Understanding the $3 Million Home Dream

Buying a $3 million house signifies entering the realm of luxury real estate, a milestone reflecting significant financial success and stability. While the median home price in America hovers around $440,000, investing in a $3 million property means acquiring a residence that is more than six times the national average. This leap into luxury real estate requires careful financial planning and a clear understanding of what it takes to maintain such a property.

However, it’s crucial to recognize that in certain high-cost urban centers such as San Francisco, New York, or Los Angeles, a $3 million budget may not secure an extravagant mansion, but rather a comfortable family home. Location profoundly influences the perception of “luxury” and the lifestyle that accompanies it. Before setting your sights on a $3 million home, consider how location aligns with your financial capabilities and lifestyle aspirations.

1.1. The Psychology Behind the Purchase

The decision to purchase a $3 million home often extends beyond mere housing needs; it’s a reflection of personal values, aspirations, and lifestyle preferences. For many, it signifies achieving a certain level of success and stability, providing a tangible symbol of their accomplishments. It’s about creating a sanctuary that reflects their unique taste, offers comfort and convenience, and potentially serves as a gathering place for loved ones.

However, it’s essential to approach this decision with a balanced perspective, ensuring that emotional desires align with financial realities. Avoid getting caught up in the allure of luxury without thoroughly assessing the long-term financial implications. Remember, the goal is to enhance your quality of life, not to burden it with unnecessary financial stress.

1.2. What Does a $3 Million House Offer?

A $3 million property typically boasts an array of features that go beyond basic living requirements. Expect spacious interiors, high-end finishes, gourmet kitchens, luxurious bathrooms, and meticulously landscaped grounds. Many such homes include additional amenities like swimming pools, home theaters, wine cellars, and smart home technology.

Beyond the physical attributes, a $3 million home often provides access to desirable neighborhoods with excellent schools, low crime rates, and convenient access to amenities and services. These factors contribute to an enhanced quality of life and a sense of community.

However, it’s essential to differentiate between needs and wants when evaluating the features of a luxury home. Determine which amenities are essential to your lifestyle and which are merely desirable extras. This will help you prioritize your budget and avoid overspending on features that you may not fully utilize.

1.3. The Role of Partnerships in Achieving the Dream

For many aspiring homeowners, achieving the financial means to purchase a $3 million house may seem like a distant goal. However, strategic partnerships can significantly accelerate your path to homeownership. By collaborating with like-minded individuals or businesses, you can pool resources, share risks, and leverage each other’s strengths to achieve common financial goals.

income-partners.net offers a platform to explore potential partnership opportunities, connecting you with individuals and businesses that can help you increase your income, build your wealth, and ultimately realize your dream of owning a luxury home. Whether you’re seeking investment partners, business collaborators, or mentors, income-partners.net provides the resources and connections you need to succeed.

2. The Golden Rule: Income-to-Home Price Ratio

When considering purchasing a home, particularly one in the luxury category, it’s crucial to adhere to sound financial principles to ensure long-term stability and peace of mind. One such principle is the income-to-home price ratio, a guideline that helps determine how much you can comfortably afford to spend on a home based on your annual income.

2.1. The 3x Rule: A Conservative Approach

A widely recommended guideline is the “3x rule,” which suggests that you should spend no more than three times your gross annual income on a home. This rule is designed to ensure that your housing expenses remain manageable and do not strain your overall financial well-being.

Applying this rule to a $3 million home, you would need to earn at least $1 million per year to comfortably afford the purchase. This may seem like a high hurdle, but it reflects the significant financial commitment involved in owning a luxury property.

Following the 3x rule provides a buffer for unexpected expenses, economic downturns, and other financial challenges. It also allows you to allocate funds towards other important goals, such as retirement savings, education, and investments.

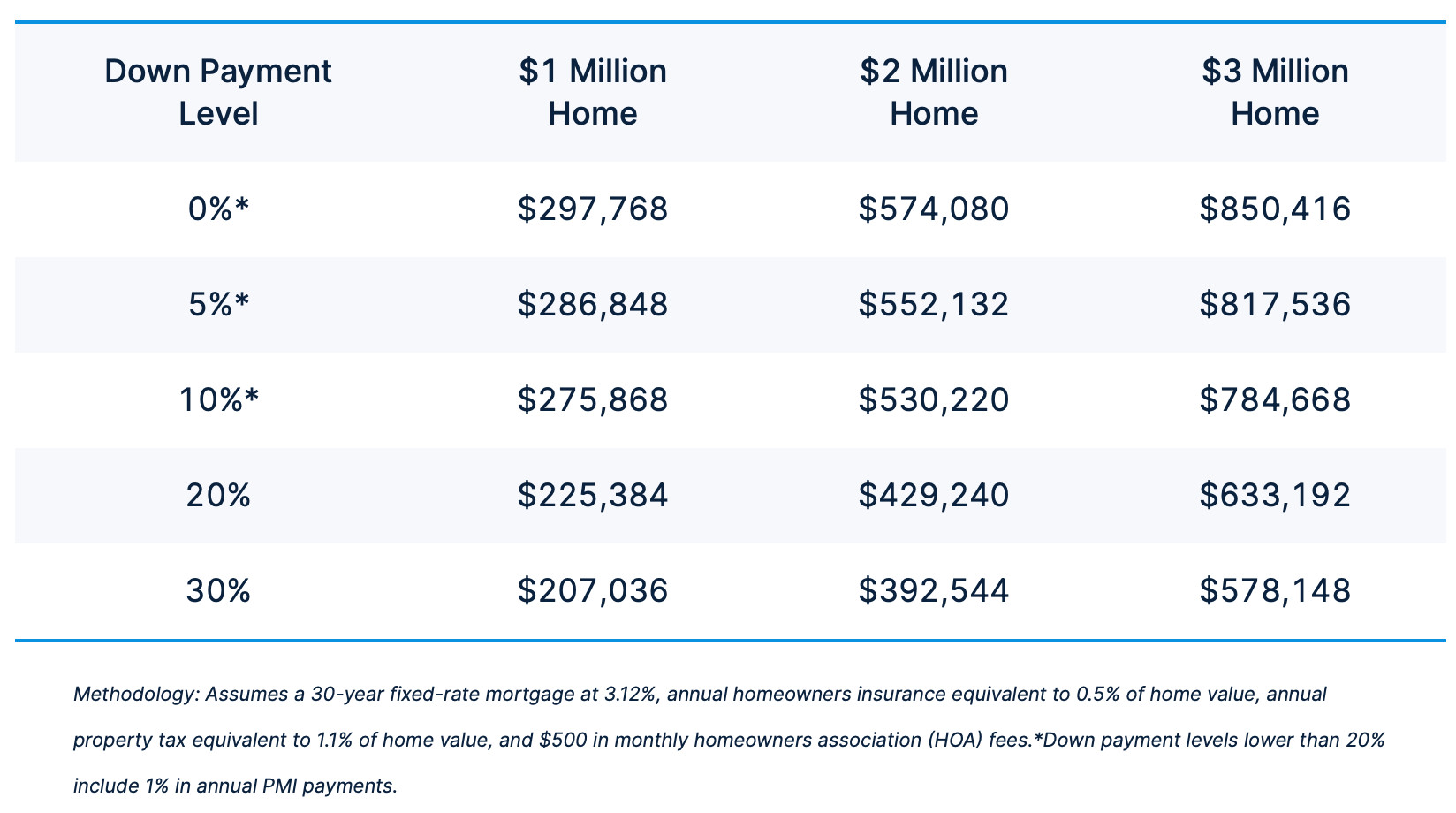

2.2. Down Payment and Cash Buffer: Essential Components

In addition to meeting the income requirements, it’s essential to have a substantial down payment and a cash buffer to comfortably afford a $3 million home. A down payment of at least 20% is typically recommended, which would amount to $600,000 for a $3 million property.

Furthermore, it’s prudent to maintain a cash buffer of at least $300,000 after making the down payment. This buffer can be used to cover unexpected expenses, such as repairs, maintenance, or job loss. It provides a sense of security and prevents you from having to rely on debt during challenging times.

2.3. Stress Testing Your Finances

Before committing to a $3 million home, it’s crucial to stress test your finances to ensure that you can weather potential storms. This involves evaluating how your finances would be affected by various scenarios, such as:

- Job loss: How long could you maintain your mortgage payments and other expenses if you lost your job?

- Interest rate increases: How would your monthly mortgage payments be affected by rising interest rates?

- Unexpected expenses: How would you handle unexpected expenses, such as medical bills or home repairs?

- Economic downturn: How would your income and investments be affected by an economic recession?

By stress testing your finances, you can identify potential vulnerabilities and take steps to mitigate them. This may involve increasing your cash buffer, reducing your debt, or diversifying your income streams.

3 million dollar house affordability with high income

3 million dollar house affordability with high income

3. Minimum Income Threshold: The Bare Necessities

While the 3x rule provides a conservative guideline for home affordability, it’s possible to stretch your finances and purchase a $3 million home with a lower income, particularly in a low-interest-rate environment. However, this requires careful planning, disciplined spending, and a willingness to accept a higher level of financial risk.

3.1. The 5x Rule: A More Aggressive Approach

In certain circumstances, it may be possible to stretch your income to five times the price of the home. With this approach, an individual needs to earn $600,000 annually to buy a $3 million house. With the 5x rule, financial stress is likely to occur.

The 5x rule assumes that you have a strong credit score, a stable job, and a low debt-to-income ratio. It also requires you to make a significant down payment and maintain a substantial cash buffer.

However, it’s important to recognize that stretching your finances to this extent can leave you vulnerable to unexpected expenses, economic downturns, and other financial challenges. It also limits your ability to save for other important goals, such as retirement and education.

3.2. The Importance of a Large Down Payment

Making a large down payment can significantly reduce your monthly mortgage payments and the overall cost of your home. It also reduces your loan-to-value ratio, which can make you eligible for lower interest rates.

For a $3 million home, a down payment of 30% or more is highly recommended if you’re stretching your finances. This would amount to $900,000 or more, which may seem like a significant sum, but it can save you tens of thousands of dollars in interest over the life of the loan.

3.3. Managing a Large Mortgage

Even with a large down payment, a $3 million home will likely require a substantial mortgage. Managing a large mortgage requires careful budgeting, disciplined spending, and a proactive approach to debt management.

- Budgeting: Create a detailed budget that tracks your income, expenses, and savings. Identify areas where you can reduce spending and allocate more funds towards your mortgage payments.

- Debt Management: Avoid taking on additional debt, such as credit card debt or car loans. Focus on paying down existing debt to improve your debt-to-income ratio.

- Refinancing: Consider refinancing your mortgage if interest rates decline. This can lower your monthly payments and save you money over the long term.

- Prepayment: Make extra mortgage payments whenever possible to reduce your principal balance and shorten the term of your loan.

3.4. The Role of Interest Rates

Interest rates play a significant role in home affordability. Lower interest rates can reduce your monthly mortgage payments and make it easier to afford a more expensive home.

However, it’s important to recognize that interest rates can fluctuate over time. Be prepared for the possibility of rising interest rates and factor this into your affordability calculations.

Consider choosing a fixed-rate mortgage to protect yourself from rising interest rates. This will ensure that your monthly payments remain stable over the life of the loan.

4. Factors Influencing Affordability

Several factors beyond income and down payment can influence your ability to afford a $3 million home. These factors include debt, property taxes, insurance, maintenance, and lifestyle expenses.

4.1. Debt-to-Income Ratio (DTI)

Your debt-to-income ratio (DTI) is a key metric that lenders use to assess your creditworthiness. It measures the percentage of your gross monthly income that goes towards debt payments, including your mortgage, credit cards, student loans, and car loans.

A lower DTI indicates that you have more disposable income and are better able to manage your debt obligations. Lenders typically prefer a DTI of 43% or less.

To improve your DTI, focus on paying down existing debt and avoiding new debt. You can also increase your income by seeking a promotion, taking on a side hustle, or starting a business.

4.2. Property Taxes

Property taxes can be a significant expense for homeowners, particularly in high-tax states. Property tax rates vary depending on location and are typically based on the assessed value of your home.

For a $3 million home, property taxes can range from $36,000 to $90,000 per year, depending on the property tax rate in your state. This expense should be factored into your affordability calculations.

Consider researching property tax rates in different locations before deciding where to buy a home. You may be able to save thousands of dollars per year by choosing a location with lower property taxes.

4.3. Homeowners Insurance

Homeowners insurance protects your home and belongings from damage or loss due to fire, theft, natural disasters, and other covered events. The cost of homeowners insurance depends on several factors, including the value of your home, its location, and the coverage limits you choose.

For a $3 million home, homeowners insurance can cost several thousand dollars per year. This expense should be factored into your affordability calculations.

Shop around for homeowners insurance quotes from different providers to find the best rates. You can also save money by increasing your deductible.

4.4. Maintenance and Repairs

Maintaining a $3 million home can be expensive. Luxury homes often require more maintenance and repairs than smaller, less expensive homes.

- Landscaping: Maintaining a large yard can cost thousands of dollars per year.

- Cleaning: Hiring a cleaning service can cost hundreds of dollars per month.

- Repairs: Unexpected repairs, such as plumbing or electrical issues, can cost thousands of dollars.

- Upgrades: Upgrading appliances, fixtures, or finishes can cost tens of thousands of dollars.

Set aside a budget for maintenance and repairs to avoid financial surprises. A good rule of thumb is to budget 1% of your home’s value per year for maintenance.

4.5. Lifestyle Expenses

Owning a $3 million home can lead to increased lifestyle expenses. You may be tempted to spend more money on furniture, décor, entertainment, and travel to match your new lifestyle.

Be mindful of your spending habits and avoid lifestyle inflation. Create a budget that reflects your values and priorities and stick to it.

Consider ways to reduce your lifestyle expenses, such as cooking at home more often, finding free or low-cost entertainment options, and traveling during the off-season.

5. The Hidden Costs of Owning a Luxury Home

Beyond the obvious expenses of mortgage payments, property taxes, and insurance, owning a luxury home comes with a range of hidden costs that can significantly impact your budget.

5.1. Higher Utility Bills

Luxury homes are often larger and more energy-intensive than smaller homes, leading to higher utility bills. Heating, cooling, and lighting a large home can consume a significant amount of energy, resulting in higher monthly expenses.

Consider investing in energy-efficient appliances, windows, and insulation to reduce your utility bills. You can also install solar panels to generate your own electricity.

5.2. Landscaping and Pool Maintenance

Maintaining a large yard and a swimming pool can be expensive. Landscaping costs include mowing, trimming, fertilizing, and pest control. Pool maintenance costs include cleaning, chemicals, and repairs.

Consider hiring a professional landscaping and pool maintenance service to ensure that your property is well-maintained. You can also save money by doing some of the work yourself.

5.3. Home Automation and Security Systems

Luxury homes often feature advanced home automation and security systems. These systems can enhance your comfort, convenience, and security, but they also come with ongoing costs.

Home automation systems require regular maintenance and upgrades. Security systems require monitoring fees and may also require repairs or replacements.

Factor these costs into your budget when considering the purchase of a luxury home.

5.4. HOA Fees

If your luxury home is located in a gated community or a planned development, you may be required to pay homeowners association (HOA) fees. These fees cover the cost of maintaining common areas, such as landscaping, swimming pools, and security.

HOA fees can range from a few hundred dollars to several thousand dollars per month. This expense should be factored into your affordability calculations.

5.5. Opportunity Cost

The opportunity cost of owning a $3 million home is the return you could have earned by investing that money elsewhere. Instead of tying up a large sum of money in a home, you could invest it in stocks, bonds, or real estate.

Consider the potential returns you could earn by investing your money instead of buying a luxury home. This may help you decide whether homeownership is the right choice for you.

Luxury home maintenance and repair costs

Luxury home maintenance and repair costs

6. Smart Strategies for Boosting Your Income

If you’re dreaming of owning a $3 million home but your current income falls short, there are several strategies you can employ to boost your earnings and accelerate your path to homeownership.

6.1. Career Advancement

Pursuing career advancement opportunities is one of the most effective ways to increase your income. This may involve seeking a promotion, taking on additional responsibilities, or acquiring new skills and certifications.

- Negotiate a raise: Research industry salary benchmarks and negotiate a raise with your current employer.

- Seek a promotion: Demonstrate your value to your employer and seek a promotion to a higher-paying role.

- Acquire new skills: Invest in your professional development by acquiring new skills and certifications that are in demand in your industry.

- Change jobs: Consider changing jobs to a company that offers higher pay and better benefits.

6.2. Starting a Side Hustle

Starting a side hustle can provide a supplemental income stream that can help you reach your financial goals faster. There are countless side hustle opportunities available, ranging from freelancing to online businesses.

- Freelancing: Offer your skills and services as a freelancer in areas such as writing, editing, graphic design, web development, or social media marketing.

- Online business: Start an online business selling products or services that you are passionate about.

- Tutoring: Offer tutoring services to students in subjects that you excel in.

- Delivery services: Become a delivery driver for companies like Uber Eats, DoorDash, or Grubhub.

6.3. Investing in Real Estate

Investing in real estate can provide a passive income stream that can help you build wealth and achieve your financial goals. There are several ways to invest in real estate, including:

- Rental properties: Buy rental properties and collect rent from tenants.

- Real estate crowdfunding: Invest in real estate projects through online crowdfunding platforms.

- REITs: Invest in real estate investment trusts (REITs), which are companies that own and operate income-producing real estate.

6.4. Building a Business

Starting a business can be a high-risk, high-reward strategy for increasing your income. If you have a great idea and the drive to succeed, building a business can provide unlimited earning potential.

- Identify a need: Identify a need in the market and create a product or service that fulfills that need.

- Develop a business plan: Develop a detailed business plan that outlines your goals, strategies, and financial projections.

- Secure funding: Secure funding from investors, lenders, or your own savings.

- Market your business: Market your business to potential customers through online and offline channels.

6.5. Partnering with Income-Partners.net

income-partners.net offers a unique platform for connecting with potential business partners, investors, and mentors. By partnering with like-minded individuals, you can leverage each other’s strengths and resources to achieve your financial goals faster.

- Find investment partners: Connect with investors who can provide capital for your business ventures.

- Find business collaborators: Collaborate with other entrepreneurs to develop new products and services.

- Find mentors: Seek guidance and advice from experienced business leaders who can help you navigate the challenges of entrepreneurship.

7. Real-Life Scenarios: Family Budgets and Homeownership

To illustrate the financial realities of owning a $3 million home, let’s examine some real-life scenarios involving family budgets and homeownership.

7.1. Scenario 1: The High-Income Family

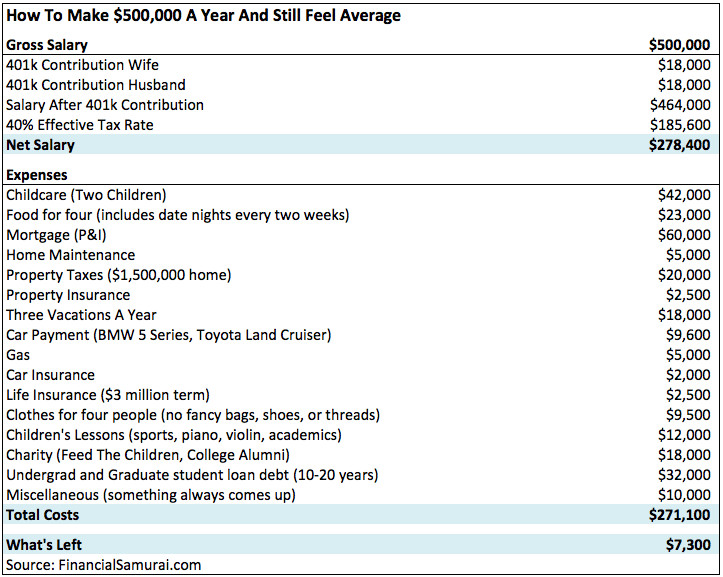

A family of four earns $500,000 per year and owns a $1.5 million home. They save responsibly for retirement and have a comfortable lifestyle. However, they struggle to save enough for a down payment on a $3 million home.

This family could benefit from increasing their income through career advancement or a side hustle. They could also consider reducing their lifestyle expenses to save more for a down payment.

7.2. Scenario 2: The Dual-Income Couple

A dual-income couple earns a combined income of $750,000 per year. They have a large down payment saved but are concerned about the ongoing costs of owning a $3 million home.

This couple should carefully evaluate their budget to ensure that they can comfortably afford the mortgage payments, property taxes, insurance, maintenance, and lifestyle expenses associated with owning a luxury home. They may need to make some adjustments to their spending habits to make it work.

7.3. Scenario 3: The Entrepreneur

An entrepreneur earns a variable income that fluctuates from year to year. They are interested in buying a $3 million home but are concerned about the risks of relying on a variable income to make mortgage payments.

This entrepreneur should build a large cash buffer to cover potential income fluctuations. They should also consider choosing a conservative mortgage option with a fixed interest rate to protect themselves from rising interest rates.

7.4. Scenario 4: The Investor

An investor has a substantial investment portfolio but is hesitant to liquidate their investments to buy a $3 million home. They are concerned about the opportunity cost of tying up a large sum of money in a home.

This investor could consider using a portion of their investment portfolio as collateral for a mortgage. This would allow them to buy the home without liquidating their investments. They could also consider investing in real estate investment trusts (REITs) to gain exposure to the real estate market without directly owning a property.

Family budget considerations for luxury home ownership

Family budget considerations for luxury home ownership

8. Location Matters: Housing Market Risks and Opportunities

The location of your $3 million home can significantly impact its value and your overall financial well-being. It’s essential to be aware of housing market risks and opportunities in different locations before making a purchase.

8.1. Cities at Risk of a Housing Downturn

Some cities are at greater risk of a housing downturn than others. These cities typically have high real estate prices compared to their prior peak and are experiencing an increase in housing supply.

According to Financial Samurai, cities like Austin, Dallas, and Nashville may be at risk of a housing downturn. In these cities, it’s important to be cautious about stretching your finances to buy a $3 million home.

8.2. Cities with Stable Housing Markets

Other cities have more stable housing markets with less risk of a downturn. These cities typically have lower real estate prices compared to their prior peak and are experiencing a limited increase in housing supply.

According to Financial Samurai, cities like San Francisco, San Diego, Miami, Seattle, and Denver have more stable housing markets. In these cities, it may be safer to stretch your finances to buy a $3 million home.

8.3. The Importance of Due Diligence

Regardless of the location you choose, it’s important to conduct thorough due diligence before buying a $3 million home. This includes:

- Researching the local housing market: Understand the current trends, risks, and opportunities in the local housing market.

- Inspecting the property: Hire a qualified home inspector to inspect the property for any potential problems.

- Obtaining a professional appraisal: Obtain a professional appraisal to determine the fair market value of the property.

- Reviewing the title report: Review the title report to ensure that there are no liens or encumbrances on the property.

8.4. Partnering with a Real Estate Professional

Partnering with a knowledgeable and experienced real estate professional can help you navigate the complexities of the luxury home market. A real estate professional can provide valuable insights into the local market, help you find the right property, and negotiate the best possible price.

9. Alternative Investments: Diversifying Your Portfolio

While owning a $3 million home can be a rewarding experience, it’s important to diversify your investment portfolio to mitigate risk and maximize returns.

9.1. Stocks and Bonds

Investing in stocks and bonds can provide long-term growth potential and diversification. Stocks offer higher potential returns but also come with higher risk. Bonds offer lower potential returns but also come with lower risk.

Consider allocating a portion of your investment portfolio to stocks and bonds based on your risk tolerance and investment goals.

9.2. Real Estate Crowdfunding

Real estate crowdfunding allows you to invest in real estate projects with smaller amounts of capital. This can provide diversification and access to real estate investments that you may not otherwise be able to afford.

Platforms like Fundrise and CrowdStreet offer a variety of real estate crowdfunding opportunities.

9.3. REITs

Real estate investment trusts (REITs) are companies that own and operate income-producing real estate. Investing in REITs can provide diversification and exposure to the real estate market without directly owning a property.

REITs are publicly traded and can be bought and sold like stocks.

9.4. Alternative Assets

Alternative assets, such as precious metals, art, and collectibles, can provide diversification and potential inflation protection. However, these assets can be illiquid and difficult to value.

Consider allocating a small portion of your investment portfolio to alternative assets if you have a high risk tolerance and a long-term investment horizon.

10. Partnering for Success: How Income-Partners.net Can Help

income-partners.net is a valuable resource for individuals seeking to increase their income, build wealth, and achieve their financial goals, including owning a $3 million home.

10.1. Connecting with Potential Partners

income-partners.net provides a platform for connecting with potential business partners, investors, and mentors. By partnering with like-minded individuals, you can leverage each other’s strengths and resources to achieve your financial goals faster.

10.2. Accessing Valuable Resources

income-partners.net offers a variety of valuable resources, including articles, guides, and tools, that can help you increase your income, build wealth, and manage your finances.

10.3. Exploring Partnership Opportunities

income-partners.net provides a directory of partnership opportunities in various industries. You can browse these opportunities to find potential collaborations that align with your skills and interests.

10.4. Building a Strong Network

income-partners.net helps you build a strong network of contacts who can support you on your financial journey. Networking with other successful individuals can provide valuable insights, advice, and opportunities.

Ready to take the next step? Visit income-partners.net today to explore partnership opportunities, access valuable resources, and connect with other successful individuals who can help you achieve your financial goals.

11. Frequently Asked Questions (FAQ)

11.1. What is the ideal income-to-home price ratio for buying a $3 million house?

The ideal income-to-home price ratio is 3x, meaning you should earn at least $1 million annually to comfortably afford a $3 million house.

11.2. Can I afford a $3 million house with a lower income?

Yes, it’s possible to stretch your finances and buy a $3 million house with a lower income, but it requires careful planning, a large down payment, and a willingness to accept a higher level of financial risk.

11.3. What is the minimum down payment required for a $3 million house?

A down payment of at least 20% is typically recommended, which would amount to $600,000 for a $3 million property.

11.4. What are some hidden costs of owning a luxury home?

Hidden costs include higher utility bills, landscaping and pool maintenance, home automation and security systems, HOA fees, and opportunity cost.

11.5. How can I boost my income to afford a $3 million house?

Strategies for boosting your income include career advancement, starting a side hustle, investing in real estate, building a business, and partnering with income-partners.net.

11.6. What factors should I consider when choosing a location for my luxury home?

Consider the stability of the local housing market, property tax rates, crime rates, school quality, and access to amenities.

11.7. How can income-partners.net help me achieve my financial goals?

income-partners.net connects you with potential partners, provides valuable resources, and helps you build a strong network of contacts who can support you on your financial journey.

11.8. What are some alternative investments I should consider?

Consider investing in stocks, bonds, real estate crowdfunding, REITs, and alternative assets.

11.9. How important is it to have a cash buffer when owning a $3 million home?

It’s crucial to have a substantial cash buffer to cover unexpected expenses, economic downturns, and other financial challenges.

11.10. What are the risks of stretching my finances to buy a $3 million house?

Stretching your finances can leave you vulnerable to unexpected expenses, economic downturns, and other financial challenges. It also limits your ability to save for other important goals.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net