Determining how much car you can afford with your income is a crucial step toward financial stability and smart money management. How much car can I afford with my income involves evaluating your financial situation and setting realistic expectations for car ownership. At income-partners.net, we provide the resources and strategies you need to make informed decisions that align with your financial goals and discover partnership opportunities to boost your income. This includes understanding vehicle affordability, budget management, and leveraging partnership opportunities for financial growth.

1. Assess Your Financial Landscape

To accurately determine how much car you can afford, you must first take a comprehensive look at your current financial situation. Knowing where your money goes each month is essential for effective budgeting and financial planning.

1.1 Calculate Your Net Monthly Income

Start by determining your total monthly take-home pay, also known as your net pay. This is the amount you receive after taxes, insurance, and other deductions. This figure provides a realistic view of your available funds for car-related expenses.

1.2 Itemize Your Monthly Expenses

List all your monthly expenses, including rent or mortgage payments, utilities, groceries, loan payments, credit card bills, and entertainment costs. Be thorough and accurate to get a clear picture of your spending habits.

1.3 Determine Your Savings Rate

Calculate how much you save each month. Ideally, you should be saving at least 10-15% of your income for future goals, such as retirement, emergencies, or investments.

1.4 Calculate Your Debt-to-Income Ratio (DTI)

Your DTI is the percentage of your gross monthly income that goes toward paying debts. To calculate your DTI, divide your total monthly debt payments by your gross monthly income. A lower DTI indicates better financial health. Lenders typically prefer a DTI of 43% or less.

2. The 20/4/10 Rule for Car Affordability

A widely recognized guideline for car affordability is the 20/4/10 rule. This rule suggests the following:

- 20% Down Payment: Make a down payment of at least 20% of the car’s purchase price.

- 4-Year Loan Term: Finance the car with a loan term of no more than four years.

- 10% of Gross Income: Keep your total monthly car costs (including loan payment, insurance, and fuel) below 10% of your gross monthly income.

2.1 Advantages of Following the 20/4/10 Rule

- Reduced Financial Strain: By adhering to these guidelines, you minimize the risk of overextending your budget.

- Faster Loan Payoff: A shorter loan term helps you pay off the car faster, reducing the total interest paid.

- Lower Interest Costs: A larger down payment can lead to better loan terms and lower interest rates.

- Protection Against Depreciation: A significant down payment protects you against owing more than the car is worth as it depreciates.

2.2 Flexibility and Adjustments to the Rule

While the 20/4/10 rule provides a solid foundation, it’s important to adjust it based on your specific circumstances. For instance, if you have a lower income or higher living expenses, you may need to aim for a smaller percentage of your income for car-related costs.

3. Factors Influencing Car Affordability

Several factors influence how much car you can realistically afford. Understanding these factors will help you make a more informed decision.

3.1 Credit Score and Interest Rates

Your credit score plays a significant role in determining the interest rate you’ll receive on an auto loan. A higher credit score typically results in a lower interest rate, which can save you thousands of dollars over the life of the loan.

According to Experian, the average interest rates for auto loans in the fourth quarter of 2023 were:

- Super Prime (781-850): 6.61% for new cars, 9.15% for used cars

- Prime (661-780): 8.63% for new cars, 11.91% for used cars

- Nonprime (601-660): 11.68% for new cars, 15.97% for used cars

- Subprime (501-600): 14.05% for new cars, 19.67% for used cars

- Deep Subprime (300-500): 16.28% for new cars, 21.18% for used cars

Maintaining a good credit score is essential for securing favorable loan terms.

3.2 Down Payment Amount

The amount of your down payment significantly impacts the total cost of the car. A larger down payment reduces the loan amount, lowering your monthly payments and the total interest paid over the life of the loan. Aim for at least 20% of the car’s purchase price as a down payment, if possible.

3.3 Loan Term Length

The loan term is the amount of time you have to repay the loan. Shorter loan terms result in higher monthly payments but lower overall interest costs. Longer loan terms offer lower monthly payments but increase the total interest paid. Balance your budget with your long-term financial goals when choosing a loan term.

3.4 Insurance Costs

Car insurance is a necessary expense for car ownership. The cost of insurance varies depending on factors such as your age, driving history, location, and the type of car you drive. Obtain insurance quotes from multiple providers to find the best rates.

3.5 Fuel Costs

Fuel costs can significantly impact your monthly budget, especially if you drive a long distance or own a vehicle with poor fuel efficiency. Consider the fuel economy of the car you’re considering and factor in estimated fuel costs when determining affordability. The U.S. Department of Energy provides detailed fuel economy figures and comparison tools on its website.

3.6 Maintenance and Repair Costs

Cars require regular maintenance and occasional repairs. Budget for these costs to avoid unexpected financial strain. Research the typical maintenance costs for the car you’re considering to get a realistic estimate.

3.7 Registration and Taxes

Car registration fees and sales taxes can add to the initial cost of purchasing a car. These fees vary by state, so research the specific costs in your area. Edmunds.com provides a breakdown of fees and taxes by state.

4. Budgeting Strategies for Car Ownership

Creating a budget is essential for managing your car-related expenses and ensuring you can afford the vehicle without financial stress.

4.1 The 50/30/20 Budget Rule

The 50/30/20 budget rule allocates your after-tax income as follows:

- 50% for Needs: Essential expenses such as housing, utilities, transportation, and groceries.

- 30% for Wants: Non-essential expenses such as dining out, entertainment, and hobbies.

- 20% for Savings and Debt Repayment: Savings, investments, and debt repayment.

Adjust this rule to fit your circumstances.

4.2 Tracking Your Expenses

Track your expenses to identify areas where you can cut back and save money. Use budgeting apps, spreadsheets, or notebooks to monitor your spending.

4.3 Creating a Sinking Fund for Car Expenses

A sinking fund is a savings account dedicated to specific expenses, such as car maintenance, repairs, or a future down payment. Set aside a small amount each month to build your sinking fund.

4.4 Automating Your Savings

Automate your savings by setting up regular transfers from your checking account to your savings account. This ensures you consistently save money without having to think about it.

5. Practical Examples of Car Affordability

To illustrate how to determine car affordability, let’s consider a few practical examples.

5.1 Example 1: Moderate Income

- Monthly Take-Home Pay: $4,500

- Recommended Car Payment (10% of Gross Income): $450

In this scenario, you can afford a car with a monthly payment of up to $450, including loan payment, insurance, and fuel.

5.2 Example 2: Higher Income

- Monthly Take-Home Pay: $7,500

- Recommended Car Payment (10% of Gross Income): $750

With a higher income, you can afford a car with a monthly payment of up to $750.

5.3 Example 3: Adjusting for High Living Expenses

- Monthly Take-Home Pay: $6,000

- High Living Expenses (Rent, Utilities, etc.): $4,000

- Remaining Income: $2,000

- Adjusted Car Payment (10% of Gross Income): $600

Even with a decent income, high living expenses may require you to adjust your car budget accordingly.

6. New vs. Used Cars: Which Is More Affordable?

When determining how much car you can afford, consider whether to buy a new or used car.

6.1 New Cars

- Pros:

- Latest features and technology

- Manufacturer warranty

- Lower maintenance costs initially

- Cons:

- Higher purchase price

- Rapid depreciation

6.2 Used Cars

- Pros:

- Lower purchase price

- Slower depreciation

- Cons:

- Higher maintenance costs

- Limited or no warranty

- Fewer features

6.3 Certified Pre-Owned (CPO) Cars

CPO cars offer a middle ground between new and used cars. They come with a manufacturer-backed warranty and have been inspected and reconditioned to meet certain standards.

6.4 Making the Decision

Choose between a new or used car based on your budget and priorities. If you value the latest features and reliability, a new car may be worth the higher price. If you’re looking to save money, a used car can be a great option.

7. Leasing vs. Buying: What Makes Sense for Your Budget?

Another important consideration is whether to lease or buy a car.

7.1 Leasing

- Pros:

- Lower monthly payments

- Opportunity to drive a new car every few years

- Maintenance often covered by warranty

- Cons:

- Mileage restrictions

- No ownership

- Potential for fees for excess wear and tear

7.2 Buying

- Pros:

- Ownership

- No mileage restrictions

- Ability to customize

- Cons:

- Higher monthly payments

- Depreciation

- Responsibility for maintenance

7.3 Making the Decision

Decide whether to lease or buy based on your lifestyle and financial goals. If you like driving a new car every few years and don’t drive long distances, leasing may be a good option. If you prefer ownership and want to avoid mileage restrictions, buying may be better.

8. Negotiating the Best Deal

Negotiating the price of a car can save you money and help you stay within your budget.

8.1 Researching Prices

Before you start negotiating, research the market value of the car you’re interested in. Use online resources such as Kelley Blue Book and Edmunds to get an idea of the fair price.

8.2 Getting Pre-Approved for a Loan

Get pre-approved for an auto loan before you visit the dealership. This gives you leverage during negotiations and helps you secure a better interest rate.

8.3 Negotiating Strategies

- Start Low: Make an initial offer that is lower than the price you’re willing to pay.

- Focus on the Out-the-Door Price: Negotiate the total price, including taxes and fees.

- Be Willing to Walk Away: If the dealer isn’t willing to meet your price, be prepared to walk away.

8.4 Leveraging Online Tools

Use online tools to compare prices and find the best deals. Many dealerships offer online quotes and allow you to negotiate prices online.

9. Exploring Partnership Opportunities to Increase Income

To afford a car without stretching your budget, consider exploring partnership opportunities to increase your income. income-partners.net offers resources and connections to help you find the right partnerships.

9.1 Identifying Partnership Opportunities

Look for businesses or individuals with complementary skills or resources. Consider partnering with companies that offer products or services that align with your interests or expertise.

9.2 Types of Partnerships

- Strategic Alliances: Partnering with other businesses to achieve common goals.

- Joint Ventures: Collaborating on a specific project or venture.

- Affiliate Marketing: Earning commissions by promoting other companies’ products or services.

9.3 Maximizing Partnership Benefits

To maximize the benefits of your partnerships, establish clear goals, define roles and responsibilities, and maintain open communication.

9.4 Success Stories of Income Partnerships

Many individuals and businesses have successfully increased their income through strategic partnerships. For example, a marketing consultant might partner with a web developer to offer comprehensive digital marketing solutions to clients.

10. Real-World Case Studies

Let’s examine some real-world case studies to illustrate how individuals have successfully navigated car affordability.

10.1 Case Study 1: Sarah, a Young Professional

Sarah is a 28-year-old marketing specialist with a monthly take-home pay of $4,000. She wants to buy a reliable car for commuting to work. After assessing her finances, Sarah determines that she can comfortably afford a monthly car payment of $400. She researches used cars and finds a certified pre-owned Honda Civic for $18,000. She makes a down payment of $4,000 and finances the remaining $14,000 with a four-year loan at 5% interest. Her monthly payment is $322, which fits well within her budget.

10.2 Case Study 2: John, an Entrepreneur

John is a 45-year-old entrepreneur with a fluctuating monthly income. He wants to lease a luxury car to project a professional image. John partners with other businesses to increase his income. After analyzing his finances, John decides to lease a BMW 3 Series for $600 per month. He leverages his partnerships to increase his monthly income.

10.3 Case Study 3: Maria, a Freelancer

Maria is a 35-year-old freelancer with a variable monthly income. She needs a car for client visits and errands. Maria identifies a partnership opportunity with a local business to increase her income. She saves diligently for a down payment and finances the remainder with a reasonable loan.

11. Tools and Resources for Car Affordability

Several tools and resources can help you determine car affordability and manage your car-related expenses.

11.1 Online Car Affordability Calculators

Online car affordability calculators can help you estimate how much car you can afford based on your income, expenses, and credit score. MarketWatch provides a comprehensive auto loan calculator.

11.2 Budgeting Apps

Budgeting apps such as Mint, YNAB (You Need A Budget), and Personal Capital can help you track your expenses and create a budget.

11.3 Credit Score Monitoring Services

Credit score monitoring services such as Credit Karma and Experian can help you track your credit score and identify areas for improvement.

11.4 Car Loan Comparison Websites

Car loan comparison websites such as LendingTree and Auto Credit Express can help you compare interest rates and loan terms from multiple lenders.

11.5 Government Resources

Government resources such as the U.S. Department of Energy provide information on fuel economy and vehicle costs.

12. Common Pitfalls to Avoid

When determining car affordability, avoid these common pitfalls:

12.1 Overestimating Income

Be realistic about your income and avoid overestimating how much you earn.

12.2 Underestimating Expenses

Account for all car-related expenses, including insurance, fuel, maintenance, and repairs.

12.3 Ignoring Credit Score

Your credit score plays a significant role in determining the interest rate you’ll receive on an auto loan.

12.4 Skipping Research

Research the market value of the car you’re interested in and compare prices from multiple dealerships.

12.5 Falling for Add-Ons

Avoid unnecessary add-ons such as extended warranties or paint protection packages.

13. The Future of Car Ownership

The future of car ownership is evolving with the rise of electric vehicles, autonomous driving technology, and ride-sharing services.

13.1 Electric Vehicles (EVs)

EVs are becoming more affordable and offer lower operating costs compared to gasoline-powered cars. Government incentives and tax credits can further reduce the cost of EV ownership.

13.2 Autonomous Driving Technology

Autonomous driving technology has the potential to revolutionize transportation and reduce the need for car ownership.

13.3 Ride-Sharing Services

Ride-sharing services such as Uber and Lyft provide an alternative to car ownership for individuals who don’t drive frequently.

13.4 Car Subscription Services

Car subscription services offer a flexible alternative to traditional car ownership, allowing you to access a variety of vehicles for a monthly fee.

14. Embracing Financial Wellness

Determining how much car you can afford is an important step toward financial wellness.

14.1 Setting Financial Goals

Set clear financial goals, such as saving for retirement, paying off debt, or buying a home.

14.2 Creating a Financial Plan

Create a comprehensive financial plan that outlines your income, expenses, savings, and investments.

14.3 Seeking Professional Advice

Consider seeking advice from a financial advisor who can help you create a personalized financial plan and make informed decisions.

14.4 Continuous Learning

Stay informed about personal finance topics and continuously educate yourself about managing money.

15. Connecting With Partners to Achieve Financial Goals

income-partners.net provides resources and connections to help you find partners and achieve your financial goals.

15.1 The Power of Partnerships

Partnerships can provide access to new markets, technologies, and resources.

15.2 Building Strong Relationships

Building strong relationships with your partners is essential for long-term success.

15.3 Overcoming Challenges

Be prepared to overcome challenges and resolve conflicts that may arise in your partnerships.

15.4 Celebrating Successes

Celebrate your successes with your partners and recognize their contributions.

Calculating how much car you can afford involves careful consideration of your financial situation, budgeting strategies, and partnership opportunities. By following the guidelines outlined in this article and leveraging the resources available at income-partners.net, you can make informed decisions that align with your financial goals and drive toward financial success.

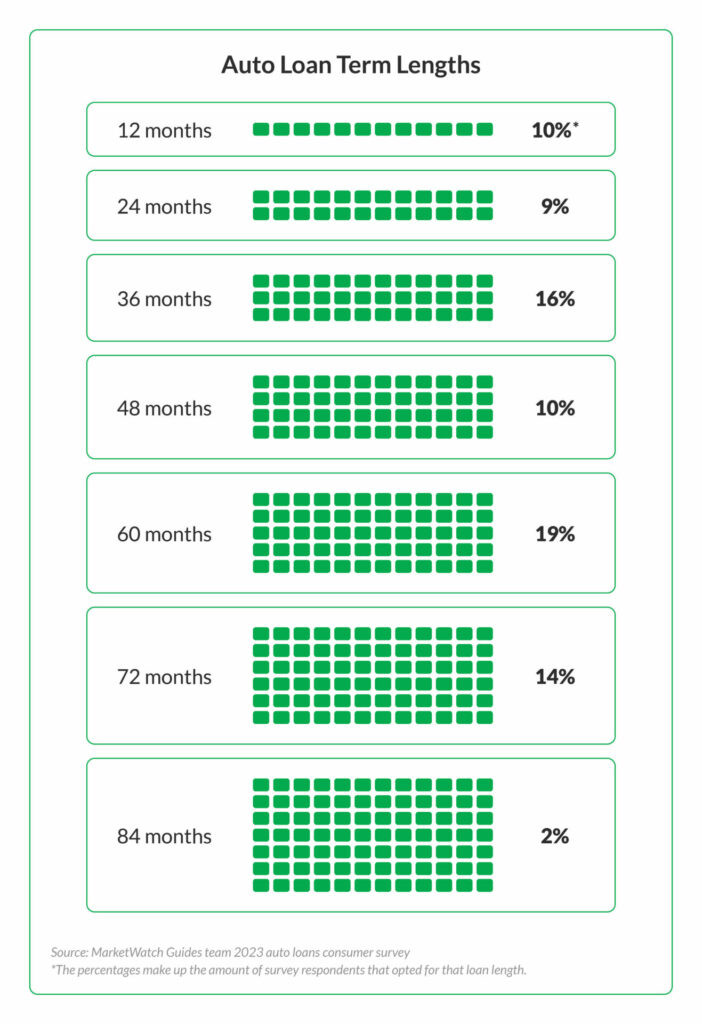

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Partner with Income-Partners.Net for Financial Success

Ready to take control of your finances and drive toward financial success? Visit income-partners.net today to discover a wealth of resources and partnership opportunities. Whether you’re looking to increase your income, manage your budget, or connect with strategic partners, we have the tools and connections you need to achieve your financial goals. Explore our website, connect with our community, and start building a brighter financial future.

By focusing on your financial landscape, applying the 20/4/10 rule, and exploring partnership opportunities, you can confidently navigate the path to car ownership and achieve your financial aspirations. Financial planning and partnership strategies will help you drive toward a more secure and prosperous future.

FAQ: Car Affordability

1. How do I determine how much car I can afford with my income?

Start by calculating your net monthly income, itemizing your monthly expenses, and determining your savings rate. Use the 20/4/10 rule as a guideline: a 20% down payment, a 4-year loan term, and total monthly car costs below 10% of your gross monthly income. Adjust the rule based on your circumstances.

2. What is the 20/4/10 rule for car affordability?

The 20/4/10 rule suggests making a 20% down payment, financing the car with a loan term of no more than four years, and keeping total monthly car costs below 10% of your gross monthly income.

3. How does my credit score affect car affordability?

Your credit score affects the interest rate you’ll receive on an auto loan. A higher credit score typically results in a lower interest rate, saving you money over the life of the loan.

4. Should I buy a new or used car?

Choose between a new or used car based on your budget and priorities. New cars offer the latest features and a warranty, while used cars are more affordable. Certified pre-owned cars provide a middle ground.

5. What are the pros and cons of leasing vs. buying a car?

Leasing offers lower monthly payments and the opportunity to drive a new car every few years, but you don’t own the car and face mileage restrictions. Buying allows ownership and no mileage restrictions, but involves higher monthly payments and depreciation.

6. How can I negotiate the best deal on a car?

Research prices, get pre-approved for a loan, start low in negotiations, focus on the out-the-door price, and be willing to walk away if the dealer doesn’t meet your price.

7. What are some common pitfalls to avoid when determining car affordability?

Avoid overestimating income, underestimating expenses, ignoring your credit score, skipping research, and falling for add-ons.

8. How can I increase my income to afford a car?

Explore partnership opportunities, such as strategic alliances, joint ventures, or affiliate marketing, to increase your income. income-partners.net can help you find the right partnerships.

9. What tools and resources can help me determine car affordability?

Use online car affordability calculators, budgeting apps, credit score monitoring services, and car loan comparison websites.

10. What is the future of car ownership?

The future of car ownership is evolving with the rise of electric vehicles, autonomous driving technology, ride-sharing services, and car subscription services.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net