Understanding the landscape of federal income taxes in the U.S. is crucial, especially for entrepreneurs and business owners seeking partnership opportunities to boost their income. At income-partners.net, we provide insights and connections to navigate this complex financial environment, ensuring you’re well-informed and ready to maximize your financial strategies. Discover how strategic partnerships can lead to financial growth and success through effective tax planning and income optimization.

1. What Percentage Of Americans Pay Federal Income Taxes?

While the exact percentage fluctuates annually, typically, around half to two-thirds of Americans pay federal income taxes. This variability depends on factors like income levels, deductions, and tax credits available each year.

To understand the extent of Americans contributing to federal income taxes, it’s essential to consider various factors influencing tax liabilities. These factors include income levels, eligibility for deductions and credits, and changes in tax laws. Let’s delve deeper into each aspect:

- Income Levels: The amount of income earned by an individual or household is a primary determinant of their federal income tax liability. Higher-income earners generally contribute a larger share of overall tax revenue.

- Deductions and Credits: Tax deductions and credits play a significant role in reducing taxable income and, consequently, the amount of taxes owed. Common deductions include those for mortgage interest, charitable contributions, and state and local taxes. Credits like the Child Tax Credit and Earned Income Tax Credit can further offset tax liabilities, particularly for low-to-moderate income families.

- Changes in Tax Laws: Federal tax laws undergo periodic revisions that can significantly impact who pays federal income taxes and how much they owe. For example, the Tax Cuts and Jobs Act of 2017 brought about substantial changes to individual income tax rates, deductions, and credits, affecting taxpayers across different income brackets.

1.1. How Tax Laws Impact the Number of Americans Paying Federal Income Taxes?

Tax laws significantly shape the number of Americans who pay federal income taxes. Legislation like the Tax Cuts and Jobs Act of 2017 altered tax brackets, deductions, and credits, influencing who owes taxes and how much.

Tax laws can have a profound impact on the distribution of tax burdens among different segments of the population. Changes to tax rates, deductions, and credits can shift the composition of taxpayers who contribute to federal income tax revenue. For instance:

- Tax Rate Adjustments: Lowering income tax rates across the board may result in a larger proportion of Americans owing federal income taxes, as individuals who were previously below the taxable income threshold may now find themselves subject to taxation.

- Expansion of Deductions and Credits: Conversely, expanding eligibility for tax deductions and credits can reduce the number of Americans paying federal income taxes, as more individuals become eligible to offset their tax liabilities.

- Targeted Tax Incentives: Tax laws may also include targeted tax incentives aimed at specific industries, activities, or demographic groups. These incentives can influence economic behavior and investment decisions, potentially affecting the overall tax landscape.

1.2. How Tax Credits Impact the Number of Americans Paying Federal Income Taxes?

Tax credits directly reduce the amount of tax an individual owes, and refundable tax credits can even result in a taxpayer receiving money back from the IRS. The Earned Income Tax Credit (EITC) and Child Tax Credit are examples of how credits can significantly decrease the number of Americans who ultimately pay federal income taxes.

Tax credits are powerful tools for incentivizing certain behaviors, supporting low-income individuals, and stimulating economic activity. These credits can have a substantial impact on the number of Americans who pay federal income taxes. Key effects include:

- Reducing Tax Liabilities: Tax credits directly reduce the amount of tax owed by eligible individuals and families. This can lower the effective tax rate and, in some cases, eliminate tax liabilities altogether.

- Promoting Economic Equity: Refundable tax credits, such as the EITC and Child Tax Credit, provide financial assistance to low-to-moderate income households. These credits can help alleviate poverty, improve financial stability, and promote economic equity.

- Encouraging Work and Investment: Some tax credits are designed to incentivize specific activities, such as investing in renewable energy or hiring workers from disadvantaged groups. By reducing the after-tax cost of these activities, tax credits can encourage greater participation and investment.

- Stimulating Economic Growth: Tax credits can also stimulate economic growth by boosting consumer spending and business investment. For example, tax credits for energy-efficient home improvements can increase demand for these products and services, creating jobs and supporting local economies.

- Simplifying Tax Filing: While tax laws can be complex, certain tax credits can simplify the filing process for eligible individuals. For example, the Saver’s Credit, which provides a tax break for low-to-moderate income individuals who contribute to retirement accounts, can encourage retirement savings while also making it easier to claim a tax benefit.

1.3. What Role Do Deductions Play in Determining the Number of Taxpayers?

Deductions lower the amount of income subject to tax, which can lead to fewer people paying federal income taxes. Standard deductions and itemized deductions for expenses like healthcare costs and mortgage interest reduce taxable income, potentially bringing more individuals below the threshold where they owe taxes.

Tax deductions play a crucial role in determining the number of taxpayers in the United States by directly influencing the amount of income that is subject to taxation. Several key points illustrate this role:

- Reduction of Taxable Income: Deductions allow taxpayers to reduce their taxable income by subtracting certain expenses or amounts from their gross income. This reduction in taxable income can lower the overall tax liability of individuals and businesses.

- Encouragement of Specific Behaviors: Many deductions are designed to incentivize specific behaviors or activities that are deemed beneficial to society or the economy. For example, deductions for charitable contributions encourage individuals to donate to charitable organizations, while deductions for mortgage interest promote homeownership.

- Offsetting Economic Burdens: Some deductions are intended to offset economic burdens or hardships faced by taxpayers. For instance, deductions for medical expenses help individuals and families cope with the costs of healthcare, while deductions for student loan interest assist borrowers in managing their educational debt.

- Simplification of Tax Filing: The standard deduction, which is a fixed amount that taxpayers can deduct from their income without itemizing, simplifies the tax filing process for many individuals. By providing a uniform deduction amount, the standard deduction reduces the need for taxpayers to track and document various expenses.

- Impact on Tax Revenue: The availability and utilization of deductions can significantly impact the amount of tax revenue collected by the government. Changes in deduction rules or amounts can affect the overall tax burden on individuals and businesses, influencing their economic behavior and investment decisions.

Tax preparer helping customer at H&R Block office in Brooklyn, NYC.

Tax preparer helping customer at H&R Block office in Brooklyn, NYC.

1.4. What Are the Income Thresholds That Determine Tax Liability?

Income thresholds, such as the standard deduction and tax bracket cutoffs, determine tax liability. These thresholds dictate who must pay federal income taxes based on their earnings. For example, individuals whose income falls below the standard deduction amount typically owe no federal income tax.

Income thresholds play a pivotal role in determining tax liability for individuals and businesses in the United States. These thresholds are key figures that dictate when and how taxes are applied to income. Here’s a detailed examination of their significance:

- Tax Brackets: Tax brackets define the income ranges at which different tax rates apply. The U.S. federal income tax system employs a progressive tax structure, meaning that higher income levels are taxed at higher rates. Income thresholds determine which portion of a taxpayer’s income falls into each tax bracket, thereby influencing their overall tax liability.

- Standard Deduction: The standard deduction is a fixed amount that taxpayers can deduct from their adjusted gross income (AGI) to reduce their taxable income. Income thresholds related to the standard deduction determine whether taxpayers should opt for the standard deduction or itemize deductions. Taxpayers with deductions exceeding the standard deduction threshold may choose to itemize to minimize their tax burden.

- Exemptions: Although personal and dependent exemptions have been suspended under recent tax law changes, they historically played a role in determining tax liability. Exemption thresholds specified the amount that taxpayers could deduct for themselves, their spouses, and their dependents, thereby reducing their taxable income.

- Eligibility for Tax Credits: Income thresholds also govern eligibility for various tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit. These credits are designed to provide financial assistance to low-to-moderate income individuals and families. Income thresholds determine whether taxpayers meet the criteria to claim these valuable tax benefits.

- Phase-Out Ranges: Certain tax deductions and credits are subject to phase-out ranges, meaning that their value decreases as a taxpayer’s income rises. Income thresholds establish the levels at which these phase-outs begin and end, affecting the amount of tax relief available to taxpayers at different income levels.

2. Who Doesn’t Pay Federal Income Taxes in the U.S.?

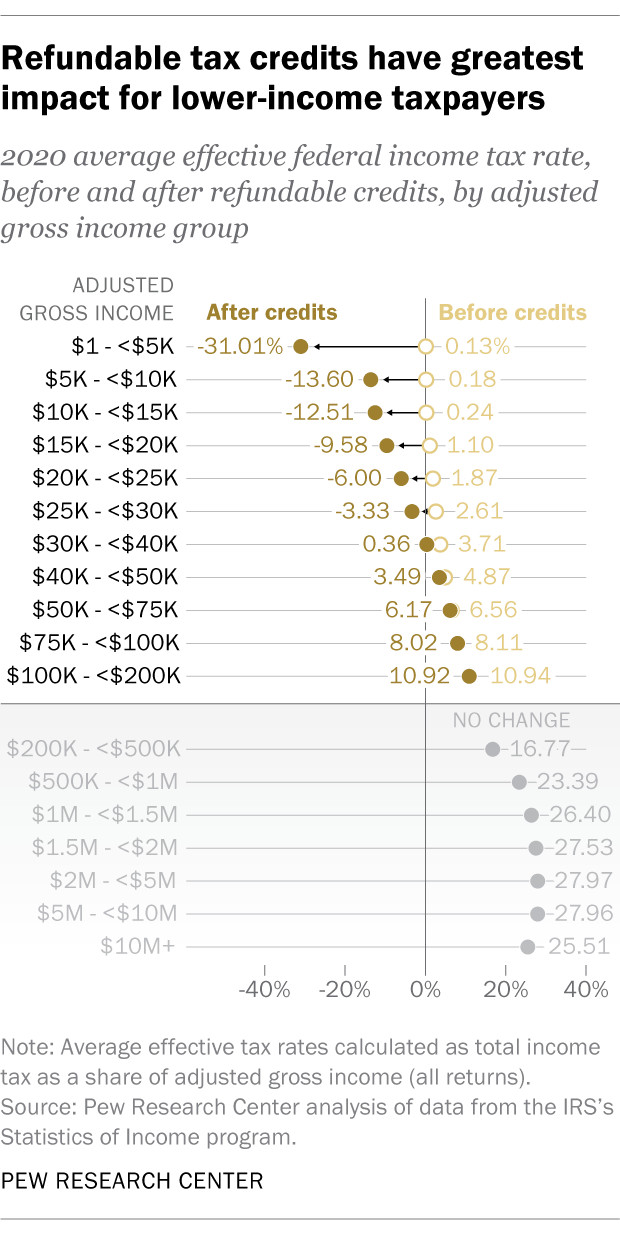

Millions of Americans owe little to no federal income tax. This includes those with low incomes and those who benefit from refundable tax credits like the Earned Income Tax Credit and the Child Tax Credit. According to IRS data, a significant portion of returns show no adjusted gross income (AGI) or AGIs below certain thresholds, leading to minimal or no tax liability.

Several key factors contribute to this phenomenon:

- Low Income Levels: Individuals with low incomes may not owe federal income taxes because their earnings fall below the standard deduction threshold. The standard deduction is a fixed amount that taxpayers can deduct from their adjusted gross income (AGI) to reduce their taxable income.

- Refundable Tax Credits: Refundable tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit, can provide financial assistance to low-to-moderate income individuals and families. These credits can reduce tax liabilities and, in some cases, result in a refund even if the taxpayer doesn’t owe any taxes.

- Deductions: Taxpayers can reduce their taxable income by claiming various deductions, such as the standard deduction, itemized deductions (e.g., medical expenses, charitable contributions), and deductions for certain expenses (e.g., student loan interest, IRA contributions). Deductions lower the amount of income subject to taxation, potentially resulting in lower tax liabilities.

- Tax Laws and Policies: Government tax laws and policies play a crucial role in shaping the tax landscape and determining who pays federal income taxes. Changes to tax rates, deductions, credits, and exemptions can impact the tax burden on individuals and families across different income levels.

2.1. What Is Adjusted Gross Income (AGI) and How Does It Affect Tax Liability?

Adjusted Gross Income (AGI) is your gross income minus certain deductions, like student loan interest or IRA contributions. AGI is a critical figure because it is used to calculate eligibility for many deductions and credits. Lower AGI can lead to reduced tax liability or even eligibility for tax refunds through refundable credits.

Adjusted Gross Income (AGI) holds significant importance in determining tax liability for individuals and businesses in the United States. It serves as a crucial intermediate step in calculating taxable income and is used to assess eligibility for various tax deductions, credits, and other tax benefits.

- Definition of AGI: Adjusted Gross Income (AGI) is calculated by subtracting certain deductions from an individual’s or business’s gross income. Gross income includes all sources of income, such as wages, salaries, business profits, investment income, and retirement distributions. Deductions subtracted from gross income to arrive at AGI may include expenses like student loan interest, contributions to retirement accounts (e.g., IRA, 401(k)), and certain self-employment expenses.

- Impact on Taxable Income: AGI serves as the starting point for calculating taxable income, which is the amount of income subject to federal income tax. By reducing gross income through allowable deductions, AGI lowers the amount of income that is ultimately taxed. This can result in lower overall tax liabilities for individuals and businesses.

- Eligibility for Tax Benefits: AGI is often used as a threshold for determining eligibility for various tax deductions, credits, and other tax benefits. Many tax provisions have income limitations or phase-out ranges based on AGI. For example, certain tax credits may only be available to individuals with AGI below a certain level, while others may phase out as AGI increases.

- Complexity of Tax Laws: The computation of AGI and its role in determining eligibility for tax benefits contribute to the complexity of the U.S. tax system. Taxpayers must navigate numerous rules and regulations to accurately calculate their AGI and determine which deductions and credits they are eligible to claim.

- Tax Planning Strategies: Understanding the implications of AGI is essential for effective tax planning. Taxpayers can strategically manage their income and deductions to minimize their AGI and maximize their eligibility for tax benefits. This may involve making contributions to retirement accounts, managing investment income, and taking advantage of eligible deductions and credits.

2.2. How Do Refundable Tax Credits Work?

Refundable tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC), can reduce a taxpayer’s tax liability to zero. If the credit amount exceeds the tax liability, the taxpayer receives the difference as a refund. This feature significantly benefits lower-income individuals and families.

Refundable tax credits serve as valuable tools for providing financial assistance to low-to-moderate income individuals and families in the United States. Unlike non-refundable tax credits, which can only reduce a taxpayer’s tax liability to zero, refundable tax credits can result in a refund even if the taxpayer doesn’t owe any taxes.

- Mechanism of Refundable Tax Credits: Refundable tax credits operate by reducing a taxpayer’s tax liability dollar-for-dollar. If the amount of the refundable tax credit exceeds the taxpayer’s tax liability, the excess amount is refunded to the taxpayer as a direct payment from the government. This means that eligible individuals and families can receive a financial benefit from the credit, even if they don’t owe any taxes.

- Targeting Low-Income Individuals and Families: Refundable tax credits are often designed to target low-to-moderate income individuals and families who may be struggling to make ends meet. These credits provide a financial safety net for those who need it most, helping them afford basic necessities such as food, housing, and healthcare.

- Promoting Work and Economic Security: Refundable tax credits like the Earned Income Tax Credit (EITC) incentivize work by providing a financial reward to low-income workers. The EITC encourages individuals to enter or remain in the workforce, as it provides a larger benefit to those who earn more income from employment.

- Complexity of Eligibility Rules: While refundable tax credits offer valuable financial assistance, they can also be complex to navigate due to their eligibility rules and requirements. Taxpayers must meet certain income thresholds, residency requirements, and other criteria to qualify for these credits.

- Impact on Poverty Reduction: Refundable tax credits have been shown to be effective in reducing poverty and improving economic security for low-income families. By providing a financial boost to those who need it most, these credits can help lift families out of poverty and provide them with greater opportunities for economic advancement.

2.3. What Are the Most Common Reasons People Owe No Federal Income Tax?

The most common reasons people owe no federal income tax include low income, claiming the standard deduction, utilizing tax credits (especially refundable ones), and taking advantage of deductions for expenses like student loan interest, IRA contributions, or healthcare costs.

There are several common reasons why individuals in the United States may owe no federal income tax. These reasons often stem from factors related to income level, tax deductions, tax credits, and tax law provisions.

- Low Income: One of the most prevalent reasons people owe no federal income tax is having a low income. Individuals whose income falls below the standard deduction threshold may not owe any federal income tax. The standard deduction is a fixed amount that taxpayers can deduct from their adjusted gross income (AGI) to reduce their taxable income.

- Standard Deduction: The standard deduction is a fixed amount that taxpayers can deduct from their AGI to reduce their taxable income. The amount of the standard deduction varies depending on filing status (e.g., single, married filing jointly, head of household) and is adjusted annually for inflation.

- Tax Credits: Tax credits directly reduce a taxpayer’s tax liability, dollar for dollar. Certain tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC), are refundable, meaning that taxpayers can receive a refund even if they don’t owe any taxes.

- Tax Deductions: Tax deductions reduce a taxpayer’s taxable income, which can lower their overall tax liability. There are various types of tax deductions available to individuals, including itemized deductions (e.g., medical expenses, charitable contributions), deductions for certain expenses (e.g., student loan interest, IRA contributions), and deductions for self-employment taxes.

- Tax Law Provisions: Government tax laws and provisions play a crucial role in determining who pays federal income taxes and how much they owe. Changes to tax rates, deductions, credits, and exemptions can impact the tax burden on individuals and families across different income levels.

IRS Individual Income Tax Returns.

IRS Individual Income Tax Returns.

2.4. How Does the Alternative Minimum Tax (AMT) Affect Tax Liabilities?

The Alternative Minimum Tax (AMT) is a separate tax system designed to prevent high-income taxpayers from avoiding taxes through excessive deductions and credits. A small number of individuals with no AGI may end up paying taxes due to the AMT.

The Alternative Minimum Tax (AMT) is a parallel tax system in the United States designed to ensure that high-income individuals and corporations pay their fair share of taxes, even if they take advantage of various deductions, credits, and exemptions that are allowed under the regular tax system.

- Purpose of the AMT: The AMT was originally enacted in 1969 in response to concerns that some wealthy individuals were using loopholes and tax shelters to avoid paying income taxes altogether. The AMT aims to prevent taxpayers from excessively reducing their tax liability through the use of tax preferences.

- Calculation of the AMT: Under the AMT, taxpayers calculate their income and deductions under a different set of rules than those used for the regular tax system. The AMT disallows or limits certain deductions and credits that are allowed under the regular tax system, such as the deduction for state and local taxes and certain itemized deductions.

- AMT Exemption: Taxpayers are allowed an exemption amount under the AMT, which reduces the amount of income subject to the AMT. The AMT exemption amount varies depending on filing status and is adjusted annually for inflation.

- AMT Rates: The AMT uses a different set of tax rates than the regular tax system. The AMT rates are generally lower than the regular tax rates, but they apply to a broader base of income due to the disallowance of certain deductions and credits.

- Impact on Taxpayers: The AMT can impact taxpayers in different ways depending on their income, deductions, and credits. High-income individuals and families who take advantage of various tax preferences are more likely to be subject to the AMT.

- Complexity and Controversy: The AMT has been criticized for its complexity and its potential to unfairly burden middle-income taxpayers. The AMT rules can be difficult to understand and comply with, and the AMT can sometimes result in taxpayers paying more in taxes than they would under the regular tax system.

3. How Does Income Bracket Affect Federal Income Tax Payments?

The federal income tax system is progressive, meaning that higher income brackets pay taxes at higher rates. As income increases, the percentage paid in taxes also generally increases, although effective tax rates can vary based on deductions and credits.

Income brackets play a fundamental role in determining how federal income tax payments are calculated in the United States. The U.S. federal income tax system operates on a progressive tax structure, where different income levels are subject to varying tax rates.

- Progressive Tax System: The U.S. federal income tax system is designed as a progressive tax system, meaning that higher income earners pay a larger percentage of their income in taxes compared to lower income earners. This progressivity is achieved through the use of income brackets, which divide taxable income into different ranges, each taxed at a specific rate.

- Tax Brackets: Tax brackets define the income ranges at which different tax rates apply. The tax rates associated with each bracket typically increase as income rises. For example, in 2023, there are seven federal income tax brackets, ranging from 10% to 37%.

- Marginal Tax Rates: The tax rate applied to each income bracket is known as the marginal tax rate. This means that the tax rate only applies to the portion of income that falls within that specific bracket. For example, if a taxpayer’s income falls into the 22% tax bracket, only the income within that bracket is taxed at 22%, while income in lower brackets is taxed at lower rates.

- Effective Tax Rate: The effective tax rate represents the actual percentage of income that a taxpayer pays in taxes after considering all deductions, credits, and other tax benefits. The effective tax rate is typically lower than the marginal tax rate due to the availability of various tax breaks that reduce taxable income.

- Impact on Tax Liabilities: Income brackets have a direct impact on the amount of federal income taxes that individuals and families owe. Higher income earners who fall into higher tax brackets will generally pay more in taxes compared to lower income earners who fall into lower tax brackets.

- Tax Planning Considerations: Income brackets are an important consideration in tax planning strategies. Taxpayers may seek to minimize their tax liabilities by managing their income and deductions to stay within lower tax brackets or to qualify for tax credits and other benefits that are phased out at higher income levels.

3.1. How Do Tax Brackets Work in the U.S.?

Tax brackets in the U.S. define the income ranges taxed at different rates, increasing as income rises. The progressive system ensures higher earners pay a higher percentage of their income in taxes.

Tax brackets are a fundamental component of the United States federal income tax system. They play a critical role in determining how much tax individuals and households owe to the government each year.

- Definition of Tax Brackets: Tax brackets are income ranges that are subject to different tax rates. The U.S. federal income tax system is progressive, meaning that higher income earners pay a larger percentage of their income in taxes compared to lower income earners. Tax brackets facilitate this progressivity by dividing taxable income into different levels, each taxed at a specific rate.

- Marginal Tax Rates: Each tax bracket is associated with a specific tax rate, known as the marginal tax rate. The marginal tax rate is the rate at which the next dollar of income is taxed. It’s important to understand that the marginal tax rate only applies to the income that falls within that particular bracket.

- Taxable Income: Tax brackets are applied to taxable income, which is the amount of income that is subject to federal income tax. Taxable income is calculated by subtracting deductions, such as the standard deduction or itemized deductions, from adjusted gross income (AGI).

- Annual Adjustments: The income thresholds for tax brackets are typically adjusted annually to account for inflation. This helps prevent bracket creep, which occurs when inflation pushes individuals into higher tax brackets even though their real income has not increased.

- Tax Planning Implications: Tax brackets have significant implications for tax planning. Individuals and households may seek to minimize their tax liabilities by managing their income and deductions to stay within lower tax brackets or to qualify for tax credits and other benefits that are phased out at higher income levels.

- Changes to Tax Brackets: Tax brackets and their associated tax rates can be subject to change through legislation. Tax laws, such as the Tax Cuts and Jobs Act of 2017, can alter the income thresholds for tax brackets and the corresponding tax rates, which can have a significant impact on taxpayers’ tax liabilities.

3.2. What Are the Current Federal Income Tax Brackets?

For the 2023 tax year, the federal income tax brackets range from 10% to 37%, with different income thresholds for single filers, married filing jointly, and other filing statuses. These brackets are adjusted annually for inflation.

The federal income tax brackets are adjusted annually to account for inflation, which helps to prevent bracket creep and ensures that taxpayers are not unfairly pushed into higher tax brackets simply due to rising prices.

- Tax Rate Structure: The federal income tax system in the United States employs a progressive tax rate structure, which means that higher income earners pay a larger percentage of their income in taxes compared to lower income earners. This progressivity is achieved through the use of tax brackets, which divide taxable income into different ranges, each taxed at a specific rate.

- Number of Tax Brackets: The number of federal income tax brackets has varied over time, but typically ranges from six to eight brackets. The specific income thresholds for each bracket are adjusted annually to account for inflation.

- Tax Rates: The tax rates associated with each income bracket range from a low of 10% to a high of 37% for the 2023 tax year. These rates are applied to the portion of a taxpayer’s income that falls within each respective bracket.

- Filing Status: The income thresholds for the federal income tax brackets vary depending on a taxpayer’s filing status. The filing status options include single, married filing jointly, married filing separately, head of household, and qualifying widow(er). Each filing status has its own set of income thresholds for the tax brackets.

- Tax Planning Implications: Understanding the federal income tax brackets is crucial for effective tax planning. Taxpayers can strategically manage their income and deductions to stay within lower tax brackets and minimize their tax liabilities.

- Legislative Changes: The federal income tax brackets and their associated tax rates are subject to change through legislation. Tax laws, such as the Tax Cuts and Jobs Act of 2017, can alter the income thresholds for tax brackets and the corresponding tax rates, which can have a significant impact on taxpayers’ tax liabilities.

3.3. How Does Filing Status Affect Tax Liability?

Filing status impacts tax liability by determining which tax brackets, standard deductions, and credits apply. Options include single, married filing jointly, married filing separately, head of household, and qualifying widow(er), each with different tax implications.

Filing status plays a pivotal role in determining tax liability for individuals and couples in the United States. It dictates which tax rates, standard deductions, and credits apply, ultimately impacting the amount of taxes owed or refunded.

- Definition of Filing Status: Filing status refers to the category that taxpayers use to classify themselves when filing their federal income tax return. The IRS offers several filing status options, including single, married filing jointly, married filing separately, head of household, and qualifying widow(er).

- Impact on Tax Brackets: Filing status affects the income thresholds for tax brackets, which determine the tax rates applied to different levels of income. For example, the income thresholds for tax brackets are generally higher for married filing jointly status compared to single status, allowing couples to earn more income before being subject to higher tax rates.

- Standard Deduction Amount: Filing status also influences the standard deduction amount, which is a fixed amount that taxpayers can deduct from their adjusted gross income (AGI) to reduce their taxable income. The standard deduction amount varies depending on filing status and is adjusted annually for inflation.

- Eligibility for Tax Credits: Filing status can affect eligibility for certain tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit. Some tax credits have income limitations that vary depending on filing status, making certain credits more accessible to taxpayers in specific filing status categories.

- Tax Planning Considerations: Choosing the appropriate filing status is a crucial aspect of tax planning. Taxpayers should carefully consider their marital status, family situation, and other factors to determine which filing status will result in the lowest tax liability.

- Rules and Requirements: The IRS has specific rules and requirements that taxpayers must meet to qualify for each filing status. Taxpayers should familiarize themselves with these rules to ensure that they are using the correct filing status on their tax return.

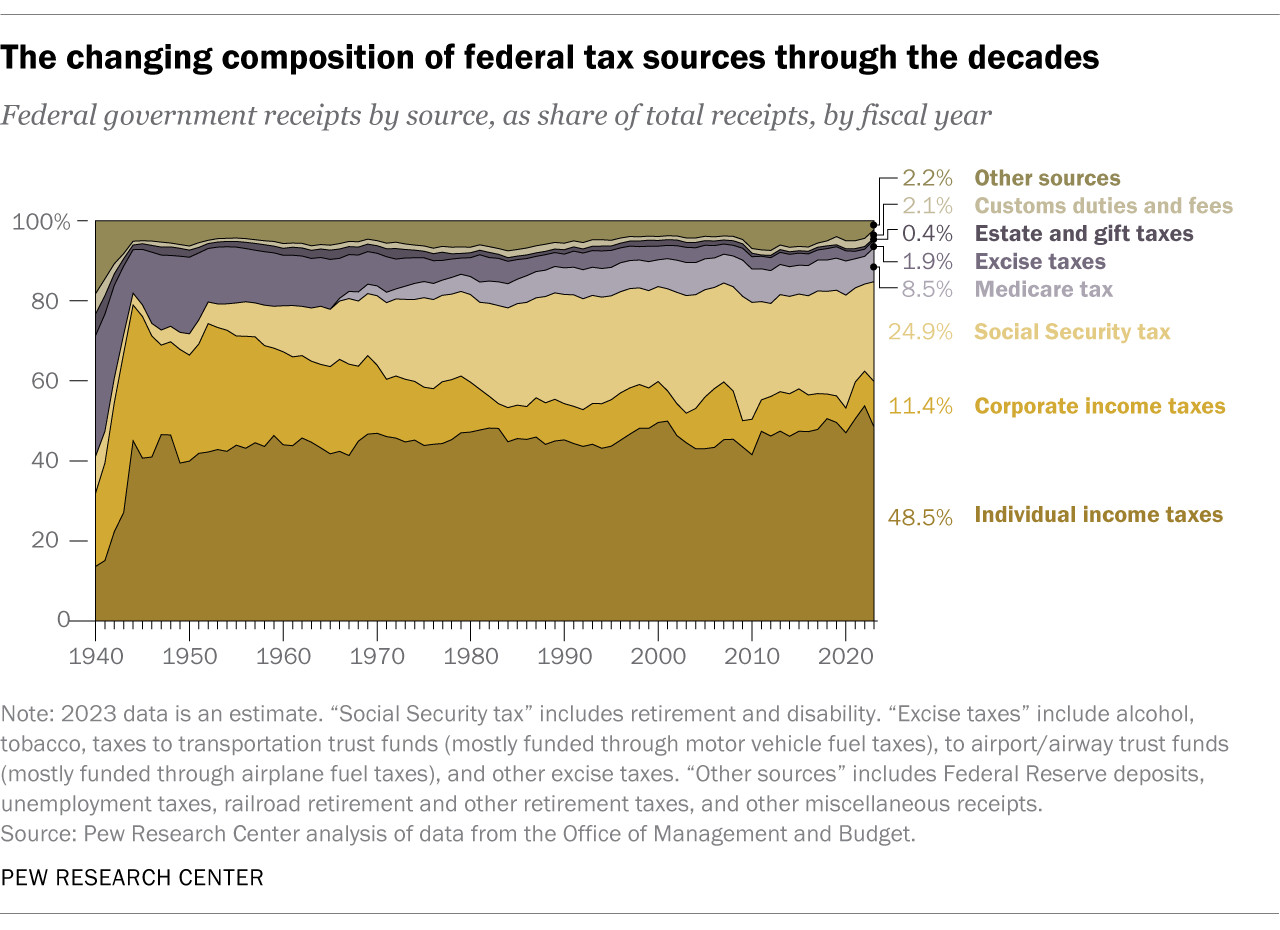

4. How Do Corporate Taxes Compare to Individual Income Taxes?

Corporate income taxes and individual income taxes differ significantly. Corporate taxes are levied on company profits, while individual taxes are on personal income. Corporate taxes account for a smaller share of federal revenue compared to individual income taxes.

Corporate income taxes and individual income taxes represent two distinct components of the U.S. federal tax system, each with its own set of rules, rates, and implications.

- Tax Base: Corporate income taxes are levied on the profits of corporations, which are legal entities separate from their owners. Individual income taxes, on the other hand, are levied on the income earned by individuals, including wages, salaries, business profits, investment income, and retirement distributions.

- Tax Rates: Corporate income tax rates are generally lower than individual income tax rates. The corporate tax rate in the United States is a flat rate of 21%, while individual income tax rates range from 10% to 37% for the 2023 tax year.

- Tax Treatment of Business Income: The tax treatment of business income depends on the type of business entity. Corporations are subject to corporate income tax on their profits, while pass-through entities, such as sole proprietorships, partnerships, and S corporations, pass their income through to their owners, who report it on their individual income tax returns.

- Tax Planning Strategies: Taxpayers employ different tax planning strategies depending on whether they are subject to corporate income tax or individual income tax. Corporations may seek to minimize their tax liabilities by taking advantage of various deductions, credits, and tax incentives, while individuals may focus on managing their income and deductions to stay within lower tax brackets and qualify for tax credits and other benefits.

- Impact on the Economy: Corporate income taxes and individual income taxes both have significant impacts on the economy. Corporate taxes affect business investment, hiring, and competitiveness, while individual taxes influence consumer spending, savings, and labor supply.

- Tax Policy Considerations: Policymakers often debate the merits of different approaches to corporate and individual income taxation, weighing the potential effects on economic growth, income distribution, and government revenue.

Corporate tax share of federal revenues.

Corporate tax share of federal revenues.

4.1. What Are the Differences Between Corporate and Individual Tax Returns?

Corporate and individual tax returns differ in their structures, schedules, and the types of income and deductions reported. Corporations use forms like Form 1120 to report income, deductions, and calculate tax liabilities, while individuals use Form 1040.

Corporate and individual tax returns are distinct documents used to report income, deductions, and tax liabilities to the government. While both types of returns serve the purpose of calculating and remitting taxes, they differ significantly in terms of structure, content, and the specific rules and regulations that apply.

- Taxpayer Identification: Corporate tax returns require the corporation’s Employer Identification Number (EIN) for identification purposes, while individual tax returns use the taxpayer’s Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Income Reporting: Corporate tax returns report various sources of income, including gross receipts, sales, and investment income. Individual tax returns report income from wages, salaries, self-employment, investments, and other sources.

- Deductions and Expenses: Corporate tax returns include deductions for business expenses, such as salaries, rent, advertising, and depreciation. Individual tax returns include deductions for personal expenses, such as mortgage interest, state and local taxes, and charitable contributions.

- Tax Credits: Both corporate and individual tax returns may include various tax credits designed to incentivize certain behaviors or provide tax relief. However, the specific tax credits available to corporations and individuals may differ.

- Schedules and Forms: Corporate tax returns often involve a variety of schedules and forms to report specific types of income, deductions, and credits. Individual tax returns also use schedules and forms to provide additional details on various aspects of the taxpayer’s financial situation.

- Complexity: Corporate tax returns are generally more complex than individual tax returns due to the intricacies of corporate accounting, tax laws, and regulations. Corporations may require the assistance of tax professionals to navigate the complexities of corporate taxation.

4.2. How Do Pass-Through Entities Affect Tax Revenue?

Pass-through entities, like S corporations and partnerships, pass their income to their owners, who then report it on their individual tax returns. This affects tax revenue by blending business income with individual income, influencing the total amount of tax collected.

Pass-through entities play a significant role in the landscape of tax revenue in the United States. These entities, which include sole proprietorships, partnerships, S corporations, and limited liability companies (LLCs), are characterized by their unique tax treatment, wherein their profits and losses are “passed through” to their owners or members, who then report them on their individual income tax returns.

- Definition of Pass-Through Entities: Pass-through entities are business structures in which the profits and losses of the business are not taxed at the entity level. Instead, the income is passed through to the owners or members, who report it on their individual income tax returns.

- Tax Treatment: Pass-through entities are not subject to corporate income tax. Instead, the owners or members report their share of the entity’s income on their individual income tax returns and pay tax at their individual income tax rates.

- Impact on Tax Revenue: Pass-through entities have a significant impact on tax revenue because they represent a large portion of the U.S. business landscape. The tax revenue generated from pass-through entities is reported on individual income tax returns, rather than corporate income tax returns.

- Tax Planning Considerations: Pass-through entities offer various tax planning opportunities for business owners. They can choose to structure their businesses as pass-through entities to avoid double taxation, which occurs when profits are taxed at both the corporate level and the individual level.

- Changes in Tax Law: Changes in tax law can have a significant impact on pass-through entities and their owners. For example, the Tax Cuts and Jobs Act of 2017 introduced a qualified business income (QBI) deduction for owners of pass-through entities, which allows them to deduct up to 20% of their qualified business income.

- Complexity: Pass-through entities can be complex to navigate from a tax perspective. Business owners must understand the rules and regulations that apply to their specific type of pass-through entity to ensure that they are complying with all applicable tax laws.

Business and Individual Income Tax.

Business and Individual Income Tax.

4.3. How Does Business Structure Influence Tax Obligations?

Business structure significantly influences tax obligations. Sole proprietorships, partnerships, S corporations, and C corporations each have distinct tax implications, affecting how profits are taxed and reported.

The structure of a business entity has a profound impact on its tax obligations in the United States. The choice of business structure determines how the business is taxed, as well as the extent to which the business owners are personally liable for the debts and obligations of the business.

- Sole Proprietorship: A sole proprietorship is the simplest form of business structure, in which the business is owned and operated by one person. The profits and losses of the business are reported on the owner’s individual income tax return.

- Partnership: A partnership is a business structure in which two or more individuals agree to share in the profits or losses of a business. Partnerships are pass-through entities, meaning that the profits and losses of the partnership are passed through to the partners, who report them on their individual income tax returns.

- S Corporation: An S corporation is a business structure that combines the benefits of a corporation with the pass-through taxation of a partnership. S corporations are not subject to corporate income tax. Instead, the profits and losses of the S corporation are passed through to the shareholders, who report them on their individual income tax returns.

- C Corporation: A C corporation is a business structure that is treated as a separate legal entity from its owners. C corporations are subject to corporate income tax on their profits. In addition, when profits are distributed to shareholders as dividends, the dividends are taxed again at the individual level.

- Limited Liability Company (LLC): A limited liability company (LLC) is a business structure that offers the limited liability of a corporation with the flexibility of a partnership or sole proprietorship. LLCs can choose to be taxed as a sole proprietorship, partnership, S corporation, or C corporation, depending on their specific circumstances and tax planning goals.

- Tax Planning Considerations: The choice of business structure is a crucial consideration for business owners. The business structure should be carefully selected to minimize tax liabilities, protect personal assets, and achieve other financial and business goals.

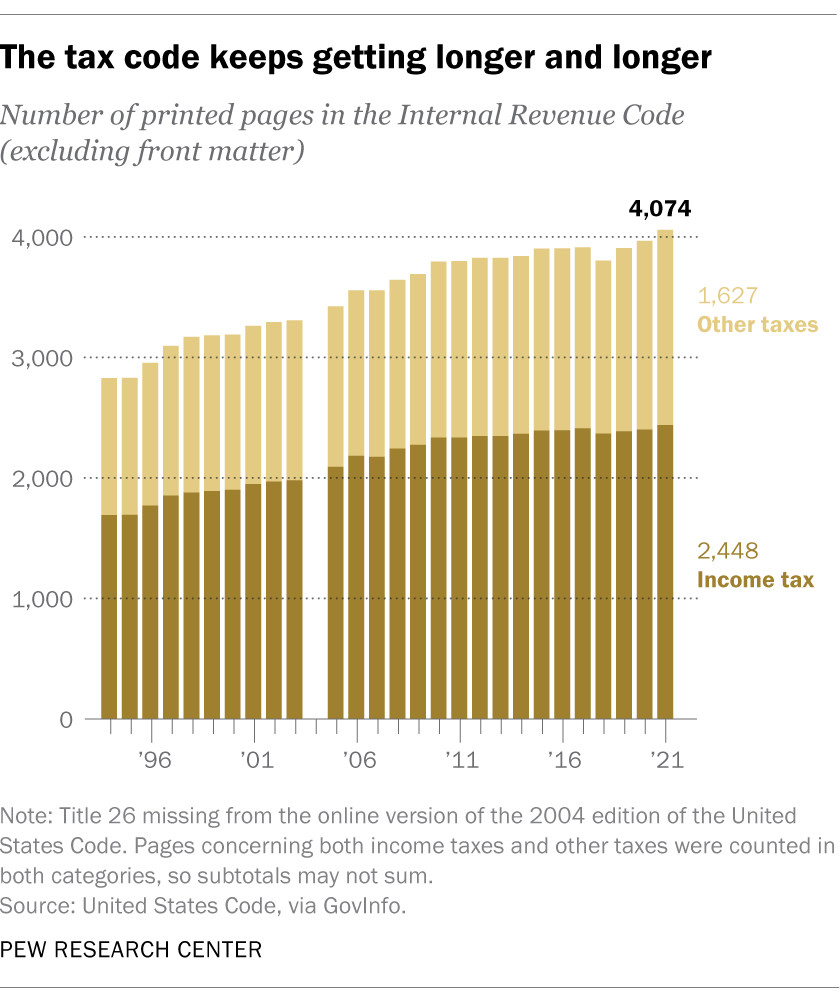

5. What Is the Tax Code’s Complexity and Why Is It a Concern?

The U.S. tax code is notoriously complex, spanning thousands of pages with intricate rules and regulations. This complexity burdens taxpayers, increases compliance costs, and raises concerns about fairness and equity.

The complexity of the tax code has numerous implications for individuals, businesses, and the overall economy. Here are some key concerns associated