Did you know that not all Americans pay federal income taxes? At income-partners.net, we help you understand the complexities of the tax system and explore opportunities to increase your income through strategic partnerships. Understanding the dynamics of who pays federal income taxes can reveal valuable insights for business and investment strategies.

1. Who Actually Pays Federal Income Taxes in the U.S.?

While the idea of taxes might seem universal, not every American contributes to the federal income tax system. The number of Americans who actually pay federal income taxes fluctuates depending on factors like income level, tax laws, and economic conditions. While most Americans file a tax return, a significant portion ends up owing little to no federal income tax. According to IRS data, in 2020, millions of Americans paid little to no federal income tax due to various deductions, credits, and low-income thresholds. Understanding this landscape is crucial for making informed financial and partnership decisions.

1.1. Factors Determining Who Pays Federal Income Taxes

Several factors determine whether an American pays federal income taxes:

- Adjusted Gross Income (AGI): AGI is a key determinant. Individuals with lower AGIs often qualify for deductions and credits that reduce their tax liability.

- Tax Deductions: Standard and itemized deductions significantly lower taxable income. Common deductions include those for state and local taxes, mortgage interest, and charitable contributions.

- Tax Credits: Tax credits, such as the Child Tax Credit and Earned Income Tax Credit (EITC), directly reduce the amount of tax owed and can even result in a refund.

- Filing Status: Whether a person files as single, married filing jointly, head of household, or qualifying widow(er) affects their tax bracket and standard deduction.

- Tax Laws and Policies: Changes in tax laws, like the Tax Cuts and Jobs Act of 2017, can significantly alter who pays taxes and how much they pay.

1.2. Impact of Tax Laws and Policies on Tax Payments

Tax laws and policies have a significant impact on who pays federal income taxes. According to the Pew Research Center, changes to tax laws over the past two decades have affected different classes of taxpayers differently.

For example, the Tax Cuts and Jobs Act of 2017 reduced the corporate tax rate from 35% to 21% and made changes to individual income tax rates, deductions, and credits. These changes generally reduced the tax burden for corporations and some high-income individuals but had varying effects on other income groups. Staying informed about these changes is essential for optimizing your financial strategies and partnership opportunities.

Tax season at H&R Block in Brooklyn, NYC

Tax season at H&R Block in Brooklyn, NYC

1.3. How Income-partners.net Helps You Navigate Tax and Partnership Opportunities

Income-partners.net provides resources and insights to help you navigate the complexities of the tax system and identify strategic partnership opportunities. By understanding who pays taxes and how tax laws impact different income groups, you can make better-informed decisions about your business and investment strategies.

2. What Percentage of Americans Pay Federal Income Taxes?

While it’s not a fixed number, typically around 50% to 60% of Americans actually pay federal income taxes in any given year. This percentage varies based on economic conditions and changes in tax laws. The Tax Policy Center estimates that for 2023, around 57% of tax filers will have positive income tax liability. This means that a significant portion of the population either owes no income tax or receives money back from the government through refundable tax credits. For entrepreneurs and investors, understanding this distribution is key to identifying potential markets and partnership opportunities.

2.1. Examining Effective Tax Rates Across Income Levels

Effective tax rates, which represent the actual percentage of income paid in taxes, vary significantly across different income levels. The tax system is designed to be progressive, meaning that higher-income earners pay a larger percentage of their income in taxes. However, various deductions, credits, and tax preferences can alter this progressivity.

According to the IRS data from 2020:

- Taxpayers with AGIs below $30,000 had an average effective tax rate of 1.5% before refundable tax credits were applied.

- Taxpayers with AGIs between $2 million and $10 million had the highest average effective tax rate, nearly 28%.

- Taxpayers with AGIs of $10 million or more had a slightly lower average effective tax rate of 25.5%, due to a larger share of income from dividends and capital gains, which are taxed at lower rates.

Understanding these effective tax rates can help you identify the most tax-efficient strategies for your business and investments, enhancing your profitability and attractiveness as a partner.

2.2. How Refundable Tax Credits Affect Tax Liabilities

Refundable tax credits play a significant role in reducing tax liabilities, especially for lower-income individuals and families. These credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit, can result in taxpayers receiving money back from the IRS, even if they owe no income tax.

In 2020, taxpayers with AGIs below $30,000 collectively received over $78.6 billion from the IRS due to refundable tax credits. For those with AGIs between $1 and $15,000, the average effective tax rate fell to -14.8% after refundable credits were applied.

These credits can significantly impact the financial well-being of lower-income individuals and families, making them an important consideration for businesses and organizations seeking to create partnerships that support economic empowerment.

Tax effective rates and income

Tax effective rates and income

2.3. Leveraging Income-partners.net for Strategic Partnerships

Income-partners.net helps you explore how tax policies and credits can inform strategic partnership opportunities. By understanding the financial incentives available to different segments of the population, you can identify areas where collaboration can lead to mutual benefits and increased income.

3. How Does the U.S. Federal Income Tax System Work?

The U.S. federal income tax system operates on a progressive tax structure, where higher income levels are taxed at higher rates. This system involves several key steps, including calculating gross income, determining adjusted gross income (AGI), and applying deductions and credits to arrive at taxable income. Understanding these steps is crucial for tax planning and identifying opportunities for strategic partnerships.

3.1. Key Components of the Federal Income Tax System

The federal income tax system is comprised of several key components:

- Gross Income: This includes all income received during the year, such as wages, salaries, tips, interest, dividends, and business income.

- Adjusted Gross Income (AGI): AGI is calculated by subtracting certain deductions from gross income, such as contributions to traditional IRAs, student loan interest payments, and self-employment taxes.

- Taxable Income: Taxable income is calculated by subtracting either the standard deduction or itemized deductions (whichever is greater) from AGI.

- Tax Rates: The U.S. has a progressive tax system, with different income brackets taxed at different rates. For 2023, there are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

- Tax Credits: Tax credits directly reduce the amount of tax owed. They can be either refundable (resulting in a refund if the credit exceeds the tax liability) or non-refundable.

3.2. Understanding Progressive Tax Brackets and Their Impact

The progressive tax system means that as income increases, it is taxed at higher rates. This system is designed to ensure that higher-income earners contribute a larger share of their income to support government programs and services. Understanding these brackets is important for income planning and strategic partnerships.

For example, in 2023, a single individual might face the following tax brackets:

| Tax Rate | Income Range |

|---|---|

| 10% | $0 to $11,000 |

| 12% | $11,001 to $44,725 |

| 22% | $44,726 to $95,375 |

| 24% | $95,376 to $182,100 |

| 32% | $182,101 to $231,250 |

| 35% | $231,251 to $578,125 |

| 37% | Over $578,125 |

This means that only the portion of income that falls within each bracket is taxed at that rate. Taxpayers can reduce their taxable income through deductions and credits, potentially lowering their overall tax liability.

3.3. Utilizing Income-partners.net for Tax-Efficient Partnerships

Income-partners.net provides resources for structuring partnerships that take advantage of tax-efficient strategies. By understanding how different business structures and investment vehicles are taxed, you can optimize your partnership agreements to maximize after-tax income for all parties involved.

4. What Are the Common Tax Deductions and Credits Available?

Tax deductions and credits are essential for reducing your tax liability. Common deductions include the standard deduction, itemized deductions (such as those for mortgage interest and charitable contributions), and deductions for business expenses. Credits like the Child Tax Credit, Earned Income Tax Credit, and education credits can significantly lower the amount of tax you owe. Entrepreneurs and investors can leverage these deductions and credits to minimize their tax burden and free up capital for reinvestment or partnership ventures.

4.1. Exploring Itemized vs. Standard Deductions

Taxpayers can choose to take either the standard deduction or itemize their deductions, depending on which results in a lower tax liability. The standard deduction is a fixed amount that varies based on filing status and is adjusted annually for inflation. For 2023, the standard deduction amounts are:

- Single: $13,850

- Married Filing Jointly: $27,700

- Head of Household: $20,800

Itemized deductions, on the other hand, are specific expenses that taxpayers can deduct from their income. Common itemized deductions include:

- State and Local Taxes (SALT): Limited to $10,000 per household.

- Mortgage Interest: Deductible on the first $750,000 of mortgage debt.

- Charitable Contributions: Deductible up to 60% of adjusted gross income for cash contributions and 30% for property contributions.

- Medical Expenses: Deductible to the extent they exceed 7.5% of adjusted gross income.

Taxpayers should calculate both their standard deduction and itemized deductions to determine which method results in the lowest taxable income.

4.2. Key Tax Credits for Individuals and Families

Tax credits directly reduce the amount of tax owed and can be particularly beneficial for individuals and families. Some key tax credits include:

- Child Tax Credit: For 2023, the Child Tax Credit is worth up to $2,000 per qualifying child.

- Earned Income Tax Credit (EITC): The EITC is a refundable tax credit for low- to moderate-income workers and families. The amount of the credit varies based on income, filing status, and the number of qualifying children.

- Education Credits: The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit can help offset the costs of higher education.

- Saver’s Credit: This credit is for low- to moderate-income taxpayers who contribute to retirement accounts.

4.3. Connecting with Income-partners.net for Maximizing Tax Benefits

Income-partners.net provides resources to help you identify and maximize available tax deductions and credits. By understanding how these tax benefits can reduce your overall tax liability, you can free up more capital for business ventures and strategic partnerships.

Tax rates and revenues

Tax rates and revenues

5. How Does Corporate Tax Fit Into the Overall Picture?

While individual income taxes are a significant source of federal revenue, corporate taxes also play a crucial role. However, the share of federal revenues from corporate taxes has declined over the decades. Understanding the dynamics of corporate tax and its impact on businesses is essential for making informed partnership decisions. According to the Office of Management and Budget, corporate taxes are projected to account for 11.4% of total federal receipts this year, less than half the share in the 1950s.

5.1. The Role of Corporate Tax in Federal Revenue

Corporate income taxes are a significant source of federal revenue, although their contribution has declined over the years. In 2023, the federal government expects to collect $546 billion in corporate taxes, representing 11.4% of total receipts.

The decline in the corporate tax share of federal revenue can be attributed to several factors, including:

- Lower Tax Rates: The corporate tax rate has been reduced over time, most recently from 35% to 21% by the Tax Cuts and Jobs Act of 2017.

- Increased Deductions and Credits: Corporations have access to various deductions and credits that can reduce their taxable income.

- Shifting Business Structures: More businesses are structured as pass-through entities, such as S corporations and partnerships, where income is taxed at the individual level rather than the corporate level.

5.2. Pass-Through Entities and Their Tax Implications

Pass-through entities, such as S corporations, partnerships, and sole proprietorships, pass their income (or loss) through to their owner or owners, who then include it on their individual tax returns. This means that the income is taxed at the individual income tax rates rather than the corporate income tax rate.

In 2020, 9 million taxpayers reported income or losses from partnerships and S corporations, and 27.7 million reported income or losses as sole proprietors or self-employed professionals. The rise of pass-through entities has reduced the share of federal revenue collected through corporate income taxes.

5.3. Partnering with Income-partners.net for Corporate Tax Insights

Income-partners.net provides valuable insights into the corporate tax landscape, helping you understand the implications of different business structures and tax strategies. By leveraging our resources, you can make informed decisions about your business and partnership opportunities, optimizing your tax position and maximizing your profitability.

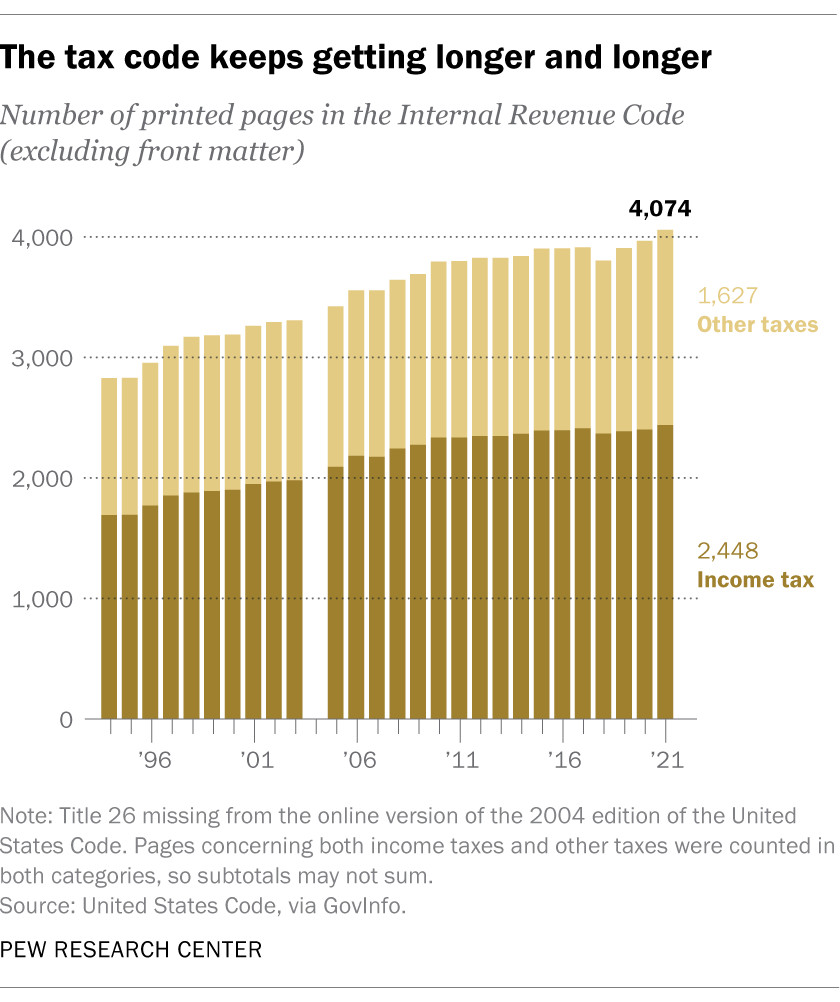

6. What Makes the U.S. Tax Code So Complex?

The U.S. tax code is notoriously complex, with numerous rules, regulations, and exceptions that can be challenging to navigate. This complexity arises from various factors, including the need to address diverse economic activities, social policies, and political considerations. The complexity of the tax code not only affects individual taxpayers but also influences how businesses structure their operations and partnerships.

6.1. Key Factors Contributing to Tax Code Complexity

Several key factors contribute to the complexity of the U.S. tax code:

- Numerous Provisions: The tax code contains a vast number of provisions, covering everything from income exclusions and deductions to credits and special rules for specific industries and activities.

- Frequent Changes: Tax laws are subject to frequent changes, making it difficult for taxpayers to stay up-to-date and comply with the latest requirements.

- Ambiguous Language: The language used in the tax code is often ambiguous and subject to interpretation, leading to confusion and disputes between taxpayers and the IRS.

- Economic and Social Policies: The tax code is used to achieve various economic and social policy goals, such as encouraging investment, promoting homeownership, and supporting charitable activities, adding to its complexity.

- Political Considerations: Political considerations often influence the drafting of tax laws, resulting in compromises and special provisions that further complicate the code.

According to the Pew Research Center, in a recent survey, 53% of U.S. adults said the system’s complexity bothered them a lot.

6.2. Impact of Complexity on Taxpayers and Businesses

The complexity of the tax code has several negative consequences for taxpayers and businesses:

- Increased Compliance Costs: Taxpayers and businesses must spend time and money to comply with the complex tax rules, including hiring tax professionals, purchasing tax software, and maintaining detailed records.

- Reduced Economic Efficiency: The complexity of the tax code can distort economic decisions, as taxpayers and businesses may make choices based on tax considerations rather than economic fundamentals.

- Erosion of Trust: The complexity of the tax code can erode trust in the tax system, as taxpayers may feel that it is unfair and difficult to understand.

6.3. Partnering with Income-partners.net for Simplifying Tax Compliance

Income-partners.net offers resources and support to help you navigate the complexities of the tax code and simplify your tax compliance efforts. By partnering with us, you can access expert guidance and insights, ensuring that you are taking advantage of all available tax benefits and minimizing your tax liability.

The complexity of the U.S. tax code

The complexity of the U.S. tax code

7. Who Bears the Burden of Federal Income Taxes?

The burden of federal income taxes is not evenly distributed across the population. While the tax system is designed to be progressive, various factors can affect who ultimately pays the most taxes. Understanding the tax burden distribution is crucial for businesses and investors looking to create fair and equitable partnerships.

7.1. Examining the Distribution of Tax Burden Across Income Groups

The distribution of the tax burden varies significantly across different income groups. Higher-income earners generally pay a larger share of their income in taxes, but the effective tax rates can differ due to deductions, credits, and tax preferences.

According to the IRS data from 2020:

- Taxpayers with AGIs between $100,000 and $1 million paid close to 54% of the total individual income taxes collected.

- Taxpayers with AGIs of $10 million or more paid 12.6% of the total individual income tax collections.

These figures highlight the progressive nature of the tax system, with higher-income earners contributing a larger share of the overall tax revenue.

7.2. Impact of Tax Policies on Different Taxpayer Classes

Tax policies can have different effects on different classes of taxpayers. Changes to tax rates, deductions, and credits can shift the tax burden, benefiting some groups while disadvantaging others.

For example, the Tax Cuts and Jobs Act of 2017 reduced the corporate tax rate and made changes to individual income tax rates, deductions, and credits. These changes generally reduced the tax burden for corporations and some high-income individuals but had varying effects on other income groups.

7.3. Collaborating with Income-partners.net for Equitable Partnerships

Income-partners.net helps you understand the distribution of the tax burden and its implications for creating equitable partnerships. By considering the tax implications for all parties involved, you can structure partnerships that are fair, sustainable, and mutually beneficial.

8. How Can Strategic Partnerships Help in Managing Tax Liabilities?

Strategic partnerships can offer numerous benefits in managing tax liabilities. By collaborating with other businesses or individuals, you can access new deductions, credits, and tax planning strategies that may not be available on your own. These partnerships can help you optimize your tax position and reduce your overall tax burden.

8.1. Tax Benefits of Forming Strategic Alliances

Forming strategic alliances can provide access to various tax benefits, including:

- Increased Deductions: Partnerships may be able to deduct expenses that are not deductible for individual businesses, such as certain fringe benefits and organizational costs.

- Tax Credits: Partnerships may qualify for tax credits that are not available to individual businesses, such as the research and development tax credit.

- Loss Sharing: Partnerships can share losses among partners, allowing them to offset income and reduce their overall tax liability.

- Tax Planning Strategies: Partnerships can implement tax planning strategies that are not available to individual businesses, such as deferring income and accelerating deductions.

8.2. Case Studies of Successful Tax-Efficient Partnerships

Several case studies illustrate how strategic partnerships can effectively manage tax liabilities:

- Real Estate Partnerships: Real estate partnerships can take advantage of depreciation deductions, which allow them to deduct a portion of the cost of their properties over time.

- Research and Development Partnerships: These partnerships can claim the research and development tax credit, which incentivizes investment in innovation.

- Energy Partnerships: Energy partnerships can benefit from tax credits for renewable energy projects, such as solar and wind power.

8.3. Income-partners.net: Your Gateway to Tax-Advantaged Collaborations

Income-partners.net provides a platform for finding and forming strategic partnerships that can help you manage your tax liabilities effectively. By connecting with other businesses and individuals, you can access new tax benefits and optimize your overall tax position.

9. What Are the Biggest Frustrations With the Current Tax System?

The U.S. tax system is a source of frustration for many Americans. Common complaints include the complexity of the tax code, the feeling that some corporations and wealthy individuals don’t pay their fair share, and the amount of taxes they personally pay. Addressing these frustrations is essential for maintaining trust in the tax system and fostering economic equity.

9.1. Common Complaints About the Tax System

According to a recent Pew Research Center survey, the biggest frustrations with the tax system include:

- Complexity: 53% of U.S. adults said the system’s complexity bothered them a lot.

- Fairness: 61% said they were bothered a lot by the feeling that some corporations don’t pay their fair share, and 60% felt the same about wealthy people.

- Tax Burden: 38% said they were bothered a lot by the amount they personally paid.

These frustrations highlight the need for tax reform that simplifies the tax code, ensures fairness, and addresses concerns about the tax burden on individuals and businesses.

9.2. Addressing Perceptions of Fairness and Equity

Addressing perceptions of fairness and equity is crucial for maintaining trust in the tax system. Tax reforms that close loopholes, eliminate tax shelters, and ensure that all taxpayers pay their fair share can help alleviate concerns about the distribution of the tax burden.

9.3. Partner with Income-partners.net for a Fairer Financial Future

Income-partners.net is committed to promoting fairness and equity in the tax system. By providing resources and support for businesses and individuals, we help you navigate the tax code, optimize your tax position, and contribute to a more equitable financial future.

10. How Can I Find the Right Financial Partner to Optimize My Tax Strategy?

Finding the right financial partner is crucial for optimizing your tax strategy and maximizing your financial success. Look for partners who bring complementary skills, resources, and expertise to the table. Effective partnerships can unlock new opportunities for tax planning, investment, and business growth.

10.1. Qualities to Look for in a Financial Partner

When seeking a financial partner, consider the following qualities:

- Expertise: Look for partners with expertise in tax law, financial planning, and business strategy.

- Resources: Choose partners who can provide access to capital, technology, and other resources that can help you achieve your financial goals.

- Compatibility: Select partners who share your values, vision, and commitment to success.

- Communication: Ensure that your partner is a good communicator and is willing to collaborate effectively.

- Trustworthiness: Choose partners who are trustworthy, ethical, and committed to acting in your best interest.

10.2. Utilizing Income-partners.net to Discover Partnership Opportunities

Income-partners.net provides a platform for discovering partnership opportunities that can help you optimize your tax strategy and achieve your financial goals. Our network includes businesses, investors, and financial professionals who are looking to collaborate and create mutually beneficial partnerships.

10.3. Contacting Income-partners.net for Personalized Partnership Guidance

At income-partners.net, we understand that finding the right financial partner can be a complex and time-consuming process. That’s why we offer personalized partnership guidance to help you identify and connect with potential partners who are a good fit for your needs and goals.

Contact us today to learn more about how we can help you find the right financial partner to optimize your tax strategy and maximize your financial success.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

Navigating the complexities of the U.S. tax system requires knowledge and strategic partnerships. With income-partners.net, you gain access to valuable insights, resources, and a network of potential partners to help you optimize your tax strategy and grow your income.

FAQ: Federal Income Taxes in the U.S.

1. What is adjusted gross income (AGI)?

AGI is gross income minus certain deductions, such as contributions to traditional IRAs and student loan interest.

2. What are the standard deduction amounts for 2023?

For 2023, the standard deduction is $13,850 for single filers, $27,700 for married filing jointly, and $20,800 for head of household.

3. What is the Earned Income Tax Credit (EITC)?

The EITC is a refundable tax credit for low- to moderate-income workers and families.

4. How do refundable tax credits affect tax liabilities?

Refundable tax credits can reduce tax liabilities to zero and result in a refund if the credit exceeds the tax owed.

5. What are pass-through entities?

Pass-through entities are businesses like S corporations and partnerships that pass income through to their owners for tax purposes.

6. What is the corporate tax rate in the U.S.?

The corporate tax rate is 21%.

7. How does the U.S. tax system work?

The U.S. tax system is progressive, meaning higher incomes are taxed at higher rates.

8. What are common tax deductions?

Common tax deductions include the standard deduction, itemized deductions, and deductions for business expenses.

9. Why is the U.S. tax code so complex?

The U.S. tax code is complex due to numerous provisions, frequent changes, and its use for economic and social policies.

10. How can I find a financial partner to optimize my tax strategy?

Look for partners with expertise, resources, compatibility, and trustworthiness. Utilize income-partners.net to discover partnership opportunities.