How Is Your Social Security Income Determined? Your social security income is determined by your earnings history, the age at which you retire, and a formula used by the Social Security Administration (SSA). Understanding how this income is calculated is crucial for financial planning and partnership opportunities. With insights from income-partners.net, we’ll explore the factors influencing your benefits, offering a clear path to maximizing your income potential and fostering beneficial partnerships. This includes Average Indexed Monthly Earnings (AIME), Primary Insurance Amount (PIA), and retirement age.

1. Key Factors Influencing Social Security Income Determination

Social Security income determination hinges on several interconnected factors. It’s not a one-size-fits-all calculation, but rather a personalized assessment that takes into account your earnings history, the age at which you choose to retire, and a specific formula used by the Social Security Administration (SSA). Let’s delve into each of these key components:

- Earnings History: The cornerstone of your Social Security benefit is your earnings record. The SSA tracks your earnings throughout your working life, primarily through the taxes you pay on your income. The more you earn (up to a certain limit each year), the higher your potential Social Security benefit.

- Retirement Age: The age at which you decide to retire plays a significant role in determining your benefit amount. You can start receiving Social Security retirement benefits as early as age 62, but your benefit will be reduced if you retire before your full retirement age (FRA). The FRA is based on your year of birth and is currently 67 for those born in 1960 or later. If you delay retirement beyond your FRA, you can earn delayed retirement credits, increasing your benefit amount.

- SSA Formula: The SSA uses a complex formula to calculate your Primary Insurance Amount (PIA), which is the benefit you would receive if you retire at your FRA. The formula takes into account your Average Indexed Monthly Earnings (AIME), which is an average of your highest 35 years of earnings, adjusted for inflation.

2. Understanding Average Indexed Monthly Earnings (AIME)

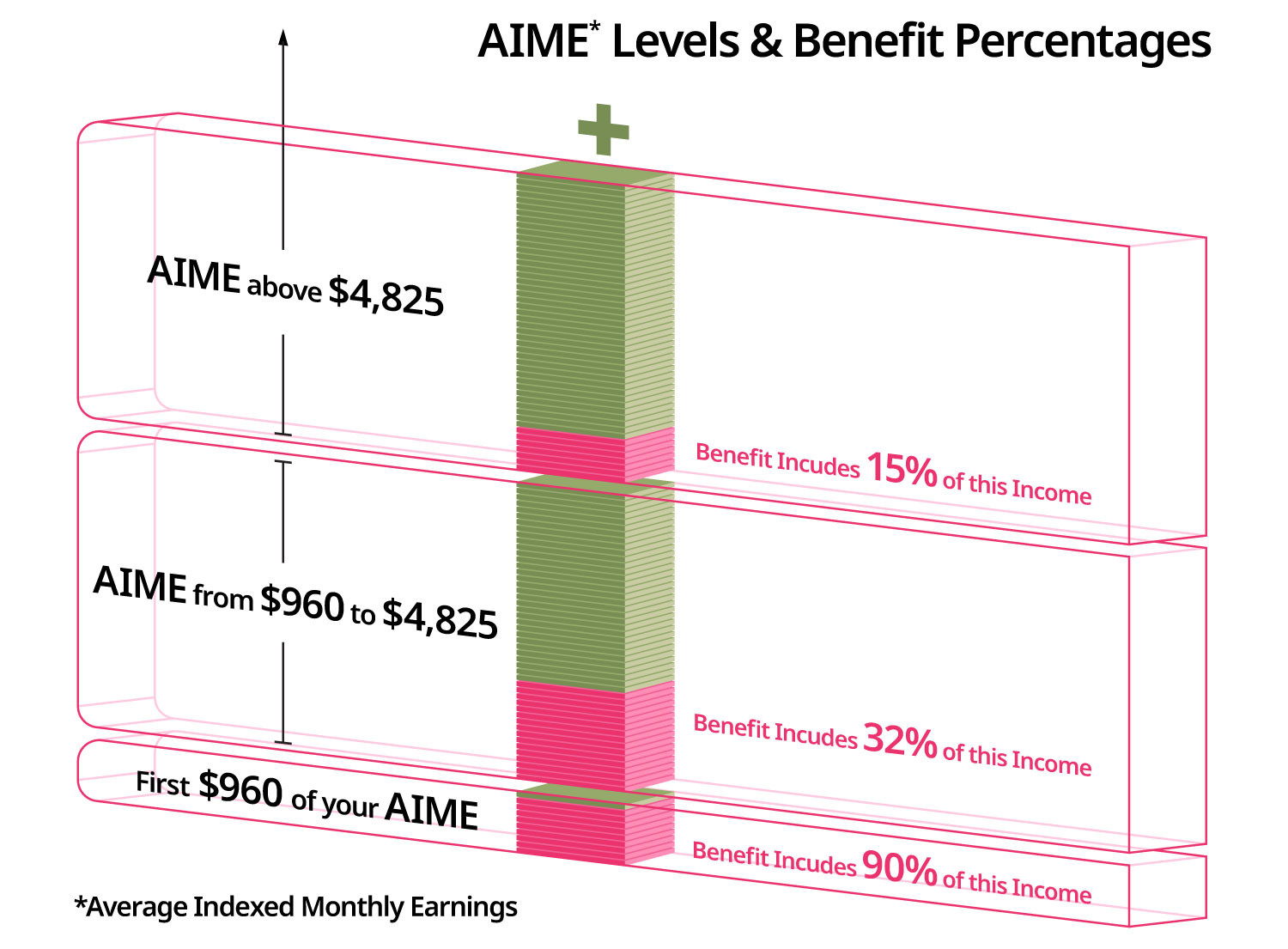

What is AIME, and how does it impact social security income determination? AIME is crucial; it’s your average monthly earnings over your 35 highest-earning years, adjusted for wage inflation.

- Calculation of AIME: The Social Security Administration (SSA) calculates your AIME by first identifying your 35 highest-earning years. These earnings are then adjusted for inflation to reflect their value in current dollars. The adjusted earnings are summed up and divided by 420 (the number of months in 35 years) to arrive at your AIME.

- Impact on Benefits: Your AIME is a key input in the formula used to determine your Primary Insurance Amount (PIA), which is the foundation of your Social Security retirement benefit. A higher AIME generally translates to a higher PIA and, consequently, a larger monthly benefit.

- Importance of Consistent Earnings: The AIME calculation underscores the importance of consistent earnings throughout your career. While high-earning years can significantly boost your AIME, having several years with little or no earnings can negatively impact your average.

3. Deciphering the Primary Insurance Amount (PIA)

What is PIA, and why is it important in social security income determination? PIA is your benefit at full retirement age and is calculated using a formula that considers your AIME.

- PIA Formula Explained: The Social Security Administration (SSA) uses a specific formula to calculate your Primary Insurance Amount (PIA). This formula is designed to provide a progressive benefit structure, meaning that it replaces a higher percentage of pre-retirement earnings for lower-income individuals than for higher-income individuals.

- Bend Points: The PIA formula incorporates “bend points,” which are specific income thresholds that determine the percentage of your AIME used in the calculation. The percentages applied to each segment of your AIME decrease as your income rises, resulting in a progressive benefit structure.

- Impact of Retirement Age on PIA: Your PIA is the benefit you would receive if you retire at your full retirement age (FRA). If you retire earlier than your FRA, your benefit will be reduced. If you delay retirement beyond your FRA, your benefit will be increased due to delayed retirement credits.

4. Retirement Age and Its Effect on Social Security Income Determination

How does retirement age affect social security income determination? Retiring early reduces benefits, while delaying retirement increases them, making it a critical decision.

- Early Retirement: Electing to retire before your full retirement age (FRA) will result in a reduction of your Social Security benefits. The reduction is calculated as a percentage of your Primary Insurance Amount (PIA) and is based on the number of months you retire before your FRA.

- Full Retirement Age: Your FRA is the age at which you are entitled to receive 100% of your PIA. The FRA is 67 for those born in 1960 or later. Retiring at your FRA ensures that you receive your full benefit amount, as calculated based on your earnings history.

- Delayed Retirement: Delaying retirement beyond your FRA can lead to increased Social Security benefits. For each year you delay, you earn delayed retirement credits, which increase your benefit amount by a certain percentage. The maximum delayed retirement credit is earned at age 70.

5. Social Security Benefit Calculation Examples

Can you illustrate social security income determination with examples? Yes, let’s explore hypothetical scenarios to clarify how Social Security benefits are calculated.

- Example 1: High Earner Retiring in 2020:

- Scenario: A high-income earner retires in 2020 with an Average Indexed Monthly Earnings (AIME) of $8,000.

- PIA Calculation: Using the PIA formula, the monthly Social Security benefit is calculated as follows:

- 90% of the first $961 of AIME: 0.90 * $961 = $864.90

- 32% of AIME between $961 and $5,785: 0.32 * ($5,785 – $961) = $1,543.68

- 15% of AIME over $5,785: 0.15 * ($8,000 – $5,785) = $332.25

- Total PIA: $864.90 + $1,543.68 + $332.25 = $2,740.83

- Monthly Benefit: The monthly Social Security benefit at full retirement age would be approximately $2,741.25, subject to annual cost-of-living adjustments.

- Example 2: Retiring Early at Age 62:

- Scenario: An individual chooses to retire at age 62, before their full retirement age.

- Benefit Reduction: Retiring early results in a reduction of benefits. For example, if the full retirement age is 67, retiring at 62 would result in a reduction of approximately 30% in the PIA.

- Example 3: Delaying Retirement Until Age 70:

- Scenario: An individual delays retirement until age 70, beyond their full retirement age.

- Benefit Increase: Delaying retirement leads to an increase in benefits due to delayed retirement credits. The benefit can increase by as much as 24% to 32%, depending on the year of birth.

6. Utilizing Social Security Administration (SSA) Resources

What resources does the SSA offer to help understand social security income determination? The SSA provides various tools and calculators for estimating your benefits.

- Quick Calculator: The SSA’s Quick Calculator is a simple online tool that allows you to estimate your future benefits based on limited information. It provides a rough estimate of your potential retirement benefits without requiring you to create an account or provide detailed earnings information.

- Retirement Calculator: The SSA’s Retirement Calculator is a more comprehensive tool that allows you to estimate your monthly benefit based on your actual earnings history. To use the calculator, you need to create an account with the Social Security Administration. The site updates regularly with new projections for your Social Security benefits as you pay taxes.

- My Social Security Account: Creating a “my Social Security” account on the SSA website provides access to personalized information about your earnings history, estimated benefits, and other important details. This account allows you to track your earnings record, verify its accuracy, and project your future benefits under different retirement scenarios.

7. Strategies to Maximize Your Social Security Income

Are there strategies to increase your social security income? Yes, delaying retirement and understanding spousal benefits can help maximize your income.

- Delaying Retirement: One of the most effective strategies to increase your Social Security income is to delay retirement. For each year you delay retirement beyond your full retirement age (FRA), you earn delayed retirement credits, which increase your benefit amount. The maximum delayed retirement credit is earned at age 70.

- Understanding Spousal Benefits: Spousal benefits can provide additional income for married individuals. If one spouse has a low or no earnings record, they may be eligible to receive a spousal benefit based on their spouse’s earnings record. The spousal benefit can be up to 50% of the worker’s Primary Insurance Amount (PIA).

- Coordinating Benefits With Your Spouse: Married couples can coordinate their Social Security claiming strategies to maximize their combined benefits. This may involve one spouse claiming benefits early while the other delays retirement to earn delayed retirement credits. Consulting with a financial advisor can help determine the optimal claiming strategy for your individual circumstances.

8. How Income-Partners.Net Can Help You Grow Your Income

How can income-partners.net assist in boosting your overall income? Income-partners.net offers partnership opportunities to enhance your financial security.

- Connecting You With Strategic Partners: Income-partners.net specializes in connecting individuals and businesses with strategic partners to create mutually beneficial relationships. These partnerships can lead to increased revenue streams, expanded market reach, and greater financial stability.

- Providing Resources for Financial Growth: Income-partners.net offers a wealth of resources to help you grow your income and achieve your financial goals. This includes articles, guides, and tools on topics such as investing, entrepreneurship, and personal finance.

- Offering Personalized Support and Guidance: Income-partners.net provides personalized support and guidance to help you navigate the complexities of the financial world. Our team of experts can answer your questions, provide advice, and help you develop a customized financial plan.

9. Common Misconceptions About Social Security Income Determination

What are some common myths about social security income determination? Many people misunderstand how their benefits are calculated and what factors influence them.

- Myth 1: Social Security is Going Bankrupt: One common misconception is that Social Security is going bankrupt and will not be able to pay benefits in the future. While the Social Security system does face financial challenges, experts agree that it is highly unlikely to become completely insolvent.

- Myth 2: Your Benefit is Based Solely on Your Last Few Years of Earnings: Another misconception is that your Social Security benefit is based solely on your last few years of earnings. In reality, your benefit is based on your average earnings over your 35 highest-earning years, adjusted for inflation.

- Myth 3: Everyone Receives the Same Benefit Amount: Many people believe that everyone receives the same Social Security benefit amount. However, benefits vary significantly based on individual earnings histories, retirement age, and other factors.

10. Staying Informed About Social Security Changes

How can you stay updated on social security changes that may impact your income? Following official sources and consulting experts are crucial.

- Subscribing to SSA Updates: You can subscribe to email updates from the Social Security Administration (SSA) to stay informed about changes to the program, new regulations, and other important information.

- Following Financial News Outlets: Staying informed about financial news and economic trends can help you understand how Social Security may be affected by broader economic factors.

- Consulting With a Financial Advisor: A financial advisor can provide personalized guidance on how Social Security changes may impact your individual financial situation. They can help you develop a plan to maximize your benefits and achieve your financial goals.

11. Understanding the Impact of Inflation on Social Security Benefits

How does inflation affect social security income determination and purchasing power? Cost-of-living adjustments (COLAs) are designed to protect benefits from inflation.

- Cost-of-Living Adjustments (COLAs): Social Security benefits are subject to annual cost-of-living adjustments (COLAs) to protect their purchasing power against inflation. The COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

- Impact of Inflation on Purchasing Power: Inflation can erode the purchasing power of Social Security benefits over time. If the COLA does not keep pace with inflation, beneficiaries may find that their benefits do not cover their living expenses.

- Strategies to Mitigate Inflation Risk: To mitigate the risk of inflation eroding your Social Security benefits, consider diversifying your income sources and investing in assets that tend to outpace inflation, such as stocks and real estate.

12. Social Security for Self-Employed Individuals

How does social security income determination work for self-employed individuals? Self-employed individuals pay both the employer and employee portions of Social Security taxes.

- Self-Employment Taxes: Self-employed individuals are responsible for paying both the employer and employee portions of Social Security and Medicare taxes, which are collectively known as self-employment taxes. This can be a significant expense, but it also allows self-employed individuals to earn Social Security credits and qualify for retirement, disability, and survivor benefits.

- Deductibility of Self-Employment Taxes: Self-employed individuals can deduct one-half of their self-employment taxes from their gross income. This deduction helps to reduce their overall tax burden and makes the self-employment tax more equitable.

- Planning for Retirement as a Self-Employed Individual: Self-employed individuals need to plan carefully for retirement to ensure they have adequate income to cover their expenses. This may involve saving in retirement accounts, investing in other assets, and coordinating their Social Security claiming strategy.

13. Social Security Disability Benefits

How does disability affect social security income determination? Disability benefits provide income replacement for those unable to work due to a medical condition.

- Eligibility Requirements: To be eligible for Social Security disability benefits, you must have a medical condition that prevents you from engaging in substantial gainful activity (SGA). Your condition must be expected to last for at least 12 months or result in death.

- Application Process: The application process for Social Security disability benefits can be lengthy and complex. It is important to gather all of the necessary documentation and provide accurate information to the Social Security Administration (SSA).

- Coordination With Retirement Benefits: If you are receiving Social Security disability benefits when you reach your full retirement age (FRA), your disability benefits will automatically convert to retirement benefits. The amount of your retirement benefit will be the same as your disability benefit.

14. The Future of Social Security

What are the long-term prospects for social security, and how might they affect your income? Understanding potential changes is crucial for long-term planning.

- Financial Challenges: The Social Security system faces financial challenges due to factors such as an aging population, declining birth rates, and increasing life expectancies. These challenges could lead to benefit cuts or tax increases in the future.

- Potential Reforms: Policymakers are considering various reforms to address the financial challenges facing Social Security. These reforms may include raising the retirement age, increasing the payroll tax rate, or modifying the benefit formula.

- Planning for Uncertainty: Given the uncertainty surrounding the future of Social Security, it is important to plan for a range of potential outcomes. This may involve saving more for retirement, diversifying your income sources, and consulting with a financial advisor.

15. Seeking Professional Financial Advice

When should you seek professional advice regarding social security income determination? A financial advisor can provide personalized guidance based on your specific circumstances.

- Benefits of Working With a Financial Advisor: A financial advisor can help you understand the complexities of Social Security and develop a claiming strategy that is tailored to your individual circumstances. They can also help you plan for retirement, manage your investments, and achieve your financial goals.

- Finding a Qualified Advisor: When choosing a financial advisor, it is important to look for someone who is qualified, experienced, and trustworthy. Ask for referrals, check credentials, and interview several advisors before making a decision.

- Questions to Ask a Financial Advisor: When meeting with a financial advisor, be sure to ask about their experience with Social Security, their fees, and their investment philosophy. Also, ask them to explain how they can help you achieve your financial goals.

16. Estate Planning and Social Security Benefits

How do social security benefits factor into estate planning? Survivor benefits can provide income for your spouse and dependents.

- Survivor Benefits: Social Security survivor benefits can provide income for your spouse and dependents after your death. The amount of the survivor benefit depends on your earnings record and the age of your survivors.

- Planning for Your Survivors: When planning your estate, it is important to consider how Social Security survivor benefits will affect your family’s financial security. You may want to purchase life insurance or make other arrangements to supplement these benefits.

- Working With an Estate Planning Attorney: An estate planning attorney can help you create a comprehensive plan that addresses your needs and the needs of your survivors. They can also help you navigate the complexities of Social Security and other government programs.

17. Social Security and Divorce

How does divorce impact social security income determination? Divorced spouses may be eligible for benefits based on their former spouse’s record.

- Eligibility Requirements for Divorced Spouses: Divorced spouses may be eligible for Social Security benefits based on their former spouse’s earnings record if they meet certain requirements. These requirements include being unmarried, having been married to the former spouse for at least 10 years, and being age 62 or older.

- Benefit Amount for Divorced Spouses: The benefit amount for divorced spouses is typically up to 50% of the former spouse’s Primary Insurance Amount (PIA). However, the benefit may be reduced if the divorced spouse remarries before age 60.

- Impact of Remarriage: Remarriage can affect a divorced spouse’s eligibility for Social Security benefits. If a divorced spouse remarries before age 60, they generally lose their eligibility for benefits based on their former spouse’s earnings record.

18. Social Security and Government Pension Offset (GPO)

What is the government pension offset, and how might it affect your social security income? The GPO can reduce social security benefits for those receiving government pensions.

- How GPO Works: The Government Pension Offset (GPO) can reduce Social Security benefits for individuals who also receive a government pension based on work that was not covered by Social Security. The GPO is designed to prevent individuals from receiving double benefits from both Social Security and a government pension.

- Who is Affected by GPO: The GPO primarily affects individuals who worked for a government agency that did not participate in the Social Security system, such as some teachers, police officers, and firefighters.

- Strategies to Minimize GPO Impact: There are several strategies to minimize the impact of the GPO on your Social Security benefits. These strategies include working in jobs covered by Social Security, delaying retirement, and coordinating your claiming strategy with your spouse.

19. Social Security and Windfall Elimination Provision (WEP)

What is the windfall elimination provision, and how does it relate to social security income determination? The WEP can reduce social security benefits for those with pensions from non-covered employment.

- How WEP Works: The Windfall Elimination Provision (WEP) can reduce Social Security benefits for individuals who also receive a pension from non-covered employment, meaning work that was not subject to Social Security taxes. The WEP is designed to prevent individuals from receiving an unfair advantage by receiving both a Social Security benefit and a pension based on non-covered earnings.

- Who is Affected by WEP: The WEP primarily affects individuals who worked in jobs that were not covered by Social Security, such as some government employees and railroad workers.

- Strategies to Minimize WEP Impact: There are several strategies to minimize the impact of the WEP on your Social Security benefits. These strategies include working in jobs covered by Social Security for a longer period, delaying retirement, and coordinating your claiming strategy with your spouse.

20. Resources for Further Information

Where can you find additional information about social security income determination? Official government websites and financial professionals are valuable resources.

- Social Security Administration (SSA) Website: The SSA website is the primary source of information about Social Security. It provides access to publications, calculators, and other resources to help you understand your benefits.

- Financial Planning Association (FPA): The FPA is a professional organization for financial planners. Its website offers resources and tools to help you find a qualified financial advisor.

- National Association of Personal Financial Advisors (NAPFA): NAPFA is another professional organization for fee-only financial advisors. Its website provides a directory of advisors and resources on financial planning topics.

Understanding how your Social Security income is determined is essential for effective retirement planning and maximizing your financial security. By considering factors like earnings history, retirement age, and utilizing available resources, you can make informed decisions about your future. Don’t forget to explore partnership opportunities on income-partners.net to further enhance your income potential. Ready to take control of your financial future? Visit income-partners.net to explore strategic partnerships, access valuable resources, and connect with experts who can help you maximize your earning potential. Discover the power of collaboration and start building a more secure financial future today.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

AIME Levels & Benefit Percentages

AIME Levels & Benefit Percentages

Alternative text: AIME Levels Benefit Percentages chart illustrating how Average Indexed Monthly Earnings impact Social Security benefits percentages, essential for understanding retirement income.

AIME Example

AIME Example

Alternative text: AIME Example table showcasing how Average Indexed Monthly Earnings are used to calculate monthly Social Security benefits, demonstrating the correlation between earnings and retirement income.

FAQ Section

1. What is Average Indexed Monthly Earnings (AIME) in relation to Social Security?

AIME is your average monthly earnings over your 35 highest-earning years, adjusted for wage inflation, playing a crucial role in determining your Social Security benefits. It’s the foundation upon which your Primary Insurance Amount (PIA) is calculated, directly impacting your monthly income during retirement.

2. How does the Primary Insurance Amount (PIA) affect my Social Security benefits?

PIA is the base figure the Social Security Administration uses to determine your retirement benefits at your full retirement age, calculated using a formula that considers your AIME to ensure fair and progressive payouts. It serves as the benchmark for calculating reduced benefits if you retire early or increased benefits if you delay retirement.

3. At what age should I retire to receive the maximum Social Security benefits?

To receive the maximum Social Security benefits, delay retirement until age 70, as this allows you to accumulate delayed retirement credits, significantly increasing your monthly income. Each year you delay retirement beyond your full retirement age (FRA), your benefit amount increases, making it a strategic move for maximizing your financial security.

4. How does early retirement impact my Social Security income?

Retiring early reduces your Social Security benefits because you’ll receive a smaller percentage of your Primary Insurance Amount (PIA) for each month you retire before your full retirement age. This reduction is permanent, so carefully consider your financial needs and potential income sources before opting for early retirement.

5. Can spousal benefits increase my Social Security income, and how?

Yes, spousal benefits can increase your Social Security income if you have a low or no earnings record, as you may be eligible to receive up to 50% of your spouse’s Primary Insurance Amount (PIA). These benefits are designed to provide financial support to married individuals, ensuring a more secure retirement for both partners.

6. What strategies can I use to maximize my Social Security income?

To maximize your Social Security income, consider delaying retirement until age 70 to earn delayed retirement credits, understanding and utilizing spousal benefits if applicable, and coordinating your claiming strategy with your spouse to optimize your combined benefits. Consulting with a financial advisor can also help tailor a strategy to your specific circumstances.

7. How does self-employment affect my Social Security income determination?

As a self-employed individual, you pay both the employer and employee portions of Social Security taxes, which allows you to earn Social Security credits and qualify for retirement, disability, and survivor benefits. Proper tax planning and consistent contributions are essential to ensure a comfortable retirement income.

8. What is the Social Security Administration’s “Quick Calculator,” and how can it help me?

The SSA’s Quick Calculator is a simple online tool that estimates your future benefits based on limited information, providing a rough idea of your potential retirement income without requiring detailed earnings information or account creation. It’s a useful starting point for understanding your Social Security prospects.

9. How do cost-of-living adjustments (COLAs) protect my Social Security benefits from inflation?

Cost-of-living adjustments (COLAs) are annual adjustments to Social Security benefits based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), designed to ensure that your benefits maintain their purchasing power despite inflation. These adjustments help retirees keep pace with rising living costs.

10. Where can I find reliable resources and personalized support for understanding Social Security income determination?

For reliable resources and personalized support, visit the Social Security Administration (SSA) website, consult with a qualified financial advisor, and explore partnership opportunities on income-partners.net to enhance your income potential and financial security. These resources can provide tailored guidance to help you navigate the complexities of Social Security and achieve your financial goals.