How is a mortgage calculator based on income? It’s a powerful tool for anyone looking to buy a home, and here at income-partners.net, we’re dedicated to helping you understand how it works and how you can leverage it to make informed financial decisions that drive income potential. Understanding the nuances of mortgage calculations can pave the way for strategic partnerships and lucrative ventures. Mortgage calculations rely on multiple elements that determine your eligibility, including income verification, debt-to-income ratio, and credit history.

Table of Contents

1. Understanding the Basics of Mortgage Calculators

- 1.1 What is a Mortgage Calculator?

- 1.2 Key Factors in Mortgage Calculations

- 1.3 The Role of Income in Mortgage Approval

2. How Income Affects Mortgage Affordability

- 2.1 Debt-to-Income Ratio (DTI) Explained

- 2.2 Different Types of Income Considered

- 2.3 Income Stability and Mortgage Approval

3. The Impact of Credit Score and Down Payment

- 3.1 Credit Score’s Role in Interest Rates

- 3.2 How Down Payment Affects Loan Amount and Terms

- 3.3 Combining Income, Credit, and Down Payment for Optimal Results

4. Exploring Different Mortgage Types and Income Requirements

- 4.1 Conventional Mortgages: Income and Credit Standards

- 4.2 FHA Loans: Lower Income and Credit Options

- 4.3 VA Loans: Benefits for Veterans and Income Considerations

- 4.4 USDA Loans: Rural Housing and Income Limits

5. Strategies to Increase Mortgage Affordability

- 5.1 Improving Your Debt-to-Income Ratio

- 5.2 Boosting Your Credit Score

- 5.3 Increasing Your Down Payment

6. Advanced Mortgage Calculation Concepts

- 6.1 Understanding APR vs. Interest Rate

- 6.2 The Impact of Loan Term on Monthly Payments

- 6.3 Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages

7. Common Mistakes to Avoid When Using a Mortgage Calculator

- 7.1 Overestimating Income

- 7.2 Ignoring Additional Expenses

- 7.3 Neglecting to Shop Around for the Best Rates

8. Leveraging Income-Partners.net for Mortgage and Partnership Opportunities

- 8.1 Finding Strategic Partners for Real Estate Ventures

- 8.2 Accessing Resources for Income Growth and Financial Planning

- 8.3 Connecting with Experts in the Mortgage Industry

9. Real-Life Examples and Case Studies

- 9.1 Case Study 1: First-Time Homebuyer with Limited Income

- 9.2 Case Study 2: Self-Employed Borrower Navigating Mortgage Approval

- 9.3 Case Study 3: Optimizing DTI for a Larger Mortgage

10. Future Trends in Mortgage Lending and Income Verification

- 10.1 The Rise of Automated Underwriting Systems

- 10.2 Alternative Income Verification Methods

- 10.3 The Impact of Economic Changes on Mortgage Rates

11. Frequently Asked Questions (FAQs)

1. Understanding the Basics of Mortgage Calculators

1.1 What is a Mortgage Calculator?

A mortgage calculator is a financial tool that estimates the monthly payments, interest, and other costs associated with a home loan. It requires inputs like loan amount, interest rate, loan term, and down payment to provide an estimated breakdown of your mortgage expenses. These calculators offer insights into how much you can afford and plan your budget effectively.

1.2 Key Factors in Mortgage Calculations

Mortgage calculations depend on several key factors. The loan amount is the total sum you borrow to purchase the home. The interest rate is the percentage charged by the lender for borrowing the money. The loan term is the length of time you have to repay the loan, typically 15, 20, or 30 years. The down payment is the initial amount you pay upfront, expressed as a percentage of the home’s purchase price.

1.3 The Role of Income in Mortgage Approval

Income plays a vital role in mortgage approval. Lenders assess your income to determine your ability to repay the loan. They look for stable and verifiable income sources, such as salary, wages, and self-employment income. According to a study by the University of Texas at Austin’s McCombs School of Business, borrowers with stable income are more likely to be approved for a mortgage with favorable terms. Income verification is a critical step in the mortgage application process, ensuring that you can comfortably manage your monthly payments.

2. How Income Affects Mortgage Affordability

2.1 Debt-to-Income Ratio (DTI) Explained

The debt-to-income ratio (DTI) is a crucial metric lenders use to assess your ability to manage monthly payments. DTI is calculated by dividing your total monthly debt payments by your gross monthly income. For example, if you have $2,000 in monthly debt payments and a gross monthly income of $6,000, your DTI is 33%. Lenders prefer lower DTI ratios, as they indicate you have more disposable income and are less likely to default on your loan.

2.2 Different Types of Income Considered

Lenders consider various types of income when assessing mortgage affordability. Salary and wages are the most common forms of income. Self-employment income, including profits from a business, is also considered but often requires more documentation, such as tax returns and profit and loss statements. Other income sources, such as alimony, child support, and investment income, can also be included if they are stable and verifiable. Each income source is evaluated to ensure consistency and reliability.

2.3 Income Stability and Mortgage Approval

Income stability is a significant factor in mortgage approval. Lenders prefer borrowers with a consistent employment history and stable income. Fluctuating or inconsistent income can raise concerns about your ability to make timely payments. If you have recently changed jobs or have gaps in your employment history, lenders may require additional documentation or have stricter requirements. Demonstrating a stable income history increases your chances of mortgage approval and favorable terms.

3. The Impact of Credit Score and Down Payment

3.1 Credit Score’s Role in Interest Rates

Your credit score significantly impacts the interest rate you receive on your mortgage. A higher credit score indicates a lower risk to the lender, resulting in a lower interest rate. Conversely, a lower credit score signals a higher risk and leads to a higher interest rate. According to Experian, borrowers with excellent credit scores (750+) typically receive the best interest rates, saving them thousands of dollars over the life of the loan. Monitoring and improving your credit score is crucial for securing a favorable mortgage rate.

3.2 How Down Payment Affects Loan Amount and Terms

The down payment you make affects both the loan amount and the terms of your mortgage. A larger down payment reduces the loan amount, which means you’ll pay less interest over the life of the loan. It can also help you avoid private mortgage insurance (PMI) if you put down at least 20% of the home’s purchase price. Additionally, a larger down payment may qualify you for better interest rates and loan terms.

3.3 Combining Income, Credit, and Down Payment for Optimal Results

Combining a strong income, excellent credit score, and substantial down payment is the key to securing the best mortgage terms. When you demonstrate financial stability and a low-risk profile, lenders are more likely to offer favorable interest rates and loan conditions. According to a study by the Harvard Business Review, borrowers who optimize these three factors can save significantly on their mortgage payments and build equity faster.

4. Exploring Different Mortgage Types and Income Requirements

4.1 Conventional Mortgages: Income and Credit Standards

Conventional mortgages are loans not insured or guaranteed by the government. They typically require higher credit scores and down payments than government-backed loans. Lenders look for a stable income history and a low DTI. According to Fannie Mae, borrowers generally need a credit score of 620 or higher to qualify for a conventional mortgage. Verifying income through W-2s, tax returns, and bank statements is standard practice.

4.2 FHA Loans: Lower Income and Credit Options

FHA loans are insured by the Federal Housing Administration and designed to help borrowers with lower credit scores and smaller down payments. FHA loans often have more flexible income requirements than conventional mortgages. The FHA considers borrowers with credit scores as low as 500 with a 10% down payment or 580 with a 3.5% down payment. FHA loans can be an excellent option for first-time homebuyers or those with limited income.

4.3 VA Loans: Benefits for Veterans and Income Considerations

VA loans are guaranteed by the Department of Veterans Affairs and offer significant benefits to eligible veterans, active-duty service members, and their families. VA loans typically do not require a down payment or private mortgage insurance (PMI). While there is no minimum credit score requirement, lenders generally look for a score of 620 or higher. Income requirements are assessed to ensure borrowers can comfortably afford the monthly payments. VA loans are a valuable resource for veterans looking to purchase a home.

4.4 USDA Loans: Rural Housing and Income Limits

USDA loans are offered by the U.S. Department of Agriculture to help low- and moderate-income borrowers purchase homes in rural areas. USDA loans do not require a down payment and offer competitive interest rates. However, there are income limits that vary by location. Borrowers must meet specific income criteria to qualify for a USDA loan, making it an affordable option for those living in eligible rural areas.

5. Strategies to Increase Mortgage Affordability

5.1 Improving Your Debt-to-Income Ratio

Improving your debt-to-income ratio (DTI) can significantly increase your mortgage affordability. One strategy is to pay down existing debts, such as credit card balances and student loans. Reducing your monthly debt payments lowers your DTI and makes you a more attractive borrower. Another approach is to increase your income through a raise, promotion, or side hustle. A higher income also lowers your DTI and improves your chances of mortgage approval.

5.2 Boosting Your Credit Score

Boosting your credit score can lead to better interest rates and loan terms. Start by checking your credit report for errors and disputing any inaccuracies. Make timely payments on all your bills to avoid late fees and negative marks on your credit report. Keep your credit utilization low by using only a small portion of your available credit. A higher credit score demonstrates financial responsibility and makes you a more appealing borrower.

5.3 Increasing Your Down Payment

Increasing your down payment can lower your loan amount, reduce your monthly payments, and potentially eliminate the need for private mortgage insurance (PMI). Save aggressively by setting aside a portion of each paycheck and cutting unnecessary expenses. Consider selling assets or seeking assistance from down payment assistance programs. A larger down payment not only saves you money in the long run but also increases your chances of mortgage approval.

6. Advanced Mortgage Calculation Concepts

6.1 Understanding APR vs. Interest Rate

It’s important to understand the difference between the annual percentage rate (APR) and the interest rate. The interest rate is the percentage charged by the lender for borrowing money, while the APR includes the interest rate plus other fees and charges, such as origination fees, discount points, and closing costs. The APR provides a more comprehensive view of the total cost of the mortgage and is useful for comparing different loan offers.

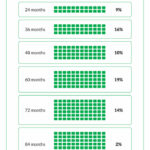

6.2 The Impact of Loan Term on Monthly Payments

The loan term significantly impacts your monthly payments and the total interest you pay over the life of the loan. A shorter loan term, such as 15 years, results in higher monthly payments but lower total interest. A longer loan term, such as 30 years, leads to lower monthly payments but higher total interest. Carefully consider your budget and financial goals when choosing a loan term.

6.3 Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages

Adjustable-rate mortgages (ARMs) have an interest rate that can change over time, while fixed-rate mortgages have a consistent interest rate for the life of the loan. ARMs typically start with a lower interest rate than fixed-rate mortgages, but the rate can increase if market interest rates rise. Fixed-rate mortgages provide stability and predictability in your monthly payments. Consider your risk tolerance and long-term financial plans when choosing between an ARM and a fixed-rate mortgage.

7. Common Mistakes to Avoid When Using a Mortgage Calculator

7.1 Overestimating Income

One common mistake is overestimating your income. Be realistic and accurate when calculating your gross monthly income. Only include income that is stable and verifiable, such as salary, wages, and self-employment income. Avoid including income that is inconsistent or unreliable. Accurate income information ensures that the mortgage calculator provides a realistic estimate of your affordability.

7.2 Ignoring Additional Expenses

Another mistake is ignoring additional expenses associated with homeownership. In addition to your monthly mortgage payment, you’ll need to budget for property taxes, homeowners insurance, maintenance, and potential homeowner association (HOA) fees. Failing to account for these expenses can lead to financial strain and make it difficult to manage your monthly payments.

7.3 Neglecting to Shop Around for the Best Rates

Neglecting to shop around for the best rates is a costly mistake. Interest rates can vary significantly between lenders, so it’s essential to compare offers from multiple sources. Get pre-approved by several lenders and compare their interest rates, fees, and loan terms. Shopping around ensures you get the most favorable mortgage terms and save money over the life of the loan.

8. Leveraging Income-Partners.net for Mortgage and Partnership Opportunities

8.1 Finding Strategic Partners for Real Estate Ventures

Income-partners.net provides a platform to find strategic partners for real estate ventures. Connect with investors, developers, and other professionals who can help you expand your business and increase your income. Building strong partnerships is essential for success in the competitive real estate market. Our platform facilitates connections that drive growth and profitability.

8.2 Accessing Resources for Income Growth and Financial Planning

Access a wealth of resources for income growth and financial planning on income-partners.net. Our articles, guides, and tools can help you improve your financial literacy and make informed decisions about mortgages, investments, and other financial matters. We are committed to empowering you with the knowledge and resources you need to achieve your financial goals.

8.3 Connecting with Experts in the Mortgage Industry

Connect with experts in the mortgage industry through income-partners.net. Our network includes lenders, brokers, and financial advisors who can provide personalized guidance and support. Whether you’re a first-time homebuyer or an experienced investor, our experts can help you navigate the complexities of the mortgage process and secure the best possible terms.

Contact Information:

- Address: 1 University Station, Austin, TX 78712, United States

- Phone: +1 (512) 471-3434

- Website: income-partners.net

9. Real-Life Examples and Case Studies

9.1 Case Study 1: First-Time Homebuyer with Limited Income

Sarah, a first-time homebuyer with a limited income, struggled to qualify for a mortgage. By improving her credit score and increasing her down payment, she was able to secure an FHA loan with favorable terms. Sarah also leveraged resources from income-partners.net to improve her financial literacy and find a strategic partner who provided additional financial support.

9.2 Case Study 2: Self-Employed Borrower Navigating Mortgage Approval

John, a self-employed borrower, faced challenges in verifying his income. By providing detailed tax returns and profit and loss statements, he demonstrated his income stability to the lender. John also worked with a financial advisor from income-partners.net to optimize his financial planning and secure a conventional mortgage.

9.3 Case Study 3: Optimizing DTI for a Larger Mortgage

Emily wanted to purchase a larger home but needed to optimize her DTI to qualify for a larger mortgage. By paying down existing debts and increasing her income through a side hustle, she lowered her DTI and successfully secured the mortgage. Emily also utilized the partnership opportunities on income-partners.net to find a real estate investor who helped her expand her property portfolio.

10. Future Trends in Mortgage Lending and Income Verification

10.1 The Rise of Automated Underwriting Systems

Automated underwriting systems are becoming increasingly prevalent in mortgage lending. These systems use algorithms to assess risk and streamline the approval process. According to a report by McKinsey, automated underwriting can reduce loan processing times and improve efficiency. However, it’s important to ensure that these systems are fair and do not perpetuate bias.

10.2 Alternative Income Verification Methods

Alternative income verification methods are emerging to address the challenges faced by self-employed borrowers and those with non-traditional income sources. These methods may include using bank statements, cash flow analysis, and other alternative forms of documentation to verify income. These innovative approaches can help more borrowers qualify for mortgages.

10.3 The Impact of Economic Changes on Mortgage Rates

Economic changes, such as inflation, interest rate hikes, and economic recessions, can significantly impact mortgage rates. Monitoring economic trends and staying informed about market conditions is essential for making smart mortgage decisions. Income-partners.net provides up-to-date information and analysis to help you navigate these changes.

11. Frequently Asked Questions (FAQs)

1. How does a mortgage calculator use my income to determine affordability?

A mortgage calculator uses your income to determine affordability by calculating your debt-to-income ratio (DTI). Lenders use this ratio to assess whether you have enough income to manage your monthly debt obligations, including the mortgage payment.

2. What types of income do mortgage lenders typically consider?

Mortgage lenders typically consider stable and verifiable income sources such as salary, wages, self-employment income, alimony, child support, and investment income. They look for consistency and reliability in these income sources.

3. How does my credit score affect the interest rate I’ll receive on a mortgage?

Your credit score significantly impacts the interest rate you’ll receive on a mortgage. A higher credit score indicates a lower risk to the lender, resulting in a lower interest rate. Conversely, a lower credit score signals a higher risk and leads to a higher interest rate.

4. What is the difference between the interest rate and the APR on a mortgage?

The interest rate is the percentage charged by the lender for borrowing money, while the APR (Annual Percentage Rate) includes the interest rate plus other fees and charges, such as origination fees, discount points, and closing costs. The APR provides a more comprehensive view of the total cost of the mortgage.

5. How does the down payment amount affect my mortgage?

The down payment amount affects your mortgage by reducing the loan amount, which means you’ll pay less interest over the life of the loan. It can also help you avoid private mortgage insurance (PMI) if you put down at least 20% of the home’s purchase price, and may qualify you for better interest rates.

6. What is a debt-to-income ratio (DTI) and why is it important?

The debt-to-income ratio (DTI) is calculated by dividing your total monthly debt payments by your gross monthly income. It’s important because lenders use it to assess your ability to manage monthly payments. A lower DTI indicates you have more disposable income and are less likely to default on your loan.

7. What are some strategies to improve my debt-to-income ratio?

Strategies to improve your debt-to-income ratio include paying down existing debts, such as credit card balances and student loans, and increasing your income through a raise, promotion, or side hustle.

8. What are the income requirements for FHA, VA, and USDA loans compared to conventional loans?

FHA loans often have more flexible income requirements than conventional mortgages and are designed to help borrowers with lower credit scores and smaller down payments. VA loans, guaranteed by the Department of Veterans Affairs, offer significant benefits to eligible veterans and typically do not require a down payment or private mortgage insurance (PMI). USDA loans, offered by the U.S. Department of Agriculture, help low- and moderate-income borrowers purchase homes in rural areas but have income limits that vary by location.

9. How can I use Income-Partners.net to find strategic partners for real estate ventures?

Income-partners.net provides a platform to connect with investors, developers, and other professionals who can help you expand your business and increase your income in the real estate market.

10. What are some common mistakes to avoid when using a mortgage calculator?

Common mistakes to avoid when using a mortgage calculator include overestimating your income, ignoring additional expenses associated with homeownership (such as property taxes and insurance), and neglecting to shop around for the best mortgage rates.

By understanding how mortgage calculators use your income and other financial factors, you can make informed decisions and secure the best possible mortgage terms. income-partners.net is here to support you with resources, expert connections, and partnership opportunities to help you achieve your financial goals and realize your dream of homeownership. Explore income growth strategies and find reliable partners to enhance your financial journey today.