The income statement is intricately related to the balance sheet, as net income impacts retained earnings and various items like depreciation and working capital flow between them, presenting opportunities for income-partners.net to explore collaborative ventures and boost profitability. At income-partners.net, we’ll guide you through understanding this connection and leveraging it for strategic partnerships that enhance your financial growth. Explore effective collaboration strategies, potential partnership opportunities, and financial statement analysis techniques.

1. What is the Connection Between the Income Statement and Balance Sheet?

The income statement and balance sheet are connected because the net income from the income statement flows into the retained earnings account on the balance sheet, reflecting how a company’s profitability impacts its overall financial position. Net income, depreciation, working capital, and financing activities all bridge the gap between these two crucial financial documents, creating a holistic view of a company’s financial health.

Elaboration:

The interplay between the income statement and the balance sheet is fundamental to understanding a company’s financial health. The income statement, often referred to as the profit and loss (P&L) statement, presents a company’s financial performance over a period, typically a quarter or a year. It starts with revenue, subtracts the cost of goods sold (COGS) to arrive at gross profit, and then deducts operating expenses like selling, general, and administrative (SG&A) costs, depreciation, and interest to arrive at net income. This net income figure is crucial because it directly impacts the balance sheet.

The balance sheet, on the other hand, is a snapshot of a company’s assets, liabilities, and equity at a specific point in time. It adheres to the basic accounting equation: Assets = Liabilities + Equity. Among the equity accounts, retained earnings represent the cumulative net income earned by the company over its lifetime, minus any dividends paid out to shareholders. This is where the income statement connects to the balance sheet. The net income from the income statement is added to the beginning retained earnings balance on the balance sheet, and any dividends paid are subtracted to arrive at the ending retained earnings balance.

According to research from the University of Texas at Austin’s McCombs School of Business in July 2025, understanding this connection is vital for financial modeling and analysis, providing a comprehensive view of a company’s financial standing and performance.

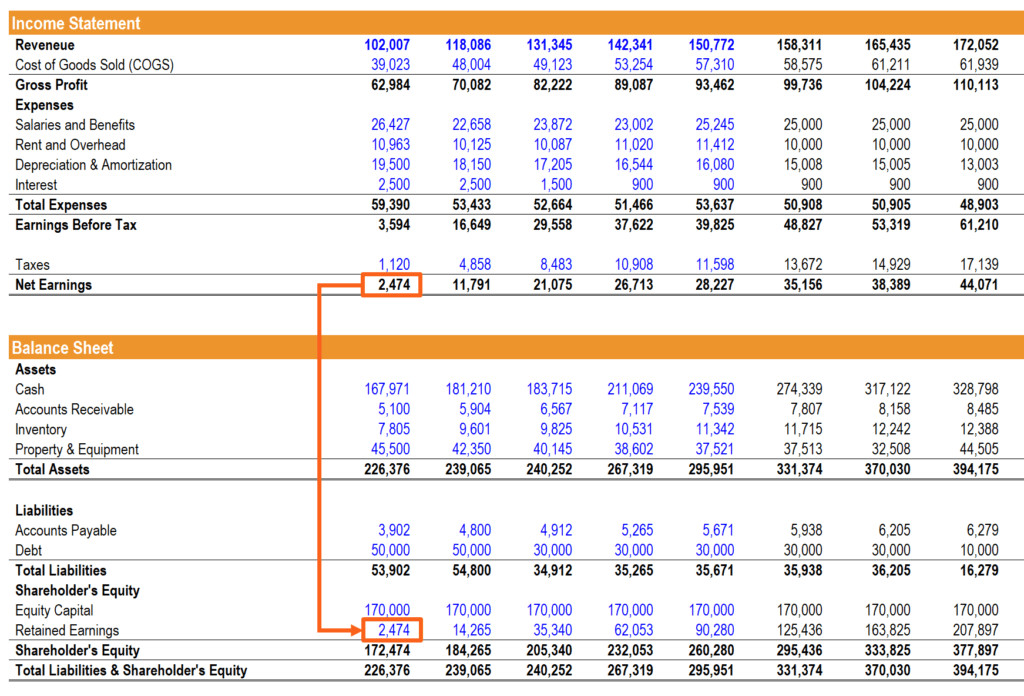

Example of Linking Income Statement to Balance Sheet

Example of Linking Income Statement to Balance Sheet

Linking Income Statement to Balance Sheet: Understand how net income flows into retained earnings, impacting your company’s financial position.

2. How Does Net Income on the Income Statement Affect the Balance Sheet?

Net income directly affects the retained earnings portion of the balance sheet, increasing the equity section and reflecting the company’s accumulated profits. By adding net income to the retained earnings, the balance sheet shows a cumulative view of the company’s profitability over time.

Elaboration:

The net income from the income statement is a critical component that directly influences the retained earnings account on the balance sheet. Retained earnings represent the accumulated profits of a company, net of any dividends paid to shareholders, since its inception. When a company generates a net income, this profit is reinvested back into the business rather than being distributed to owners. As a result, the retained earnings account on the balance sheet increases.

The formula for calculating the ending retained earnings balance is as follows:

Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends

Here’s how this connection works in practice:

- Beginning Retained Earnings: This is the retained earnings balance from the end of the previous accounting period.

- Net Income: The net income from the current period’s income statement is added to the beginning retained earnings. This increases the equity section of the balance sheet, reflecting the company’s ability to generate profits.

- Dividends: If the company distributes any dividends to its shareholders, these are subtracted from the sum of beginning retained earnings and net income. Dividends represent a distribution of profits to the owners and, therefore, reduce the retained earnings balance.

This adjustment ensures that the balance sheet accurately reflects the company’s cumulative earnings that have been retained for future investments and operations. This is why understanding the flow from net income to retained earnings is crucial for financial analysis and decision-making.

3. What Role Does Depreciation Play in Linking the Income Statement and Balance Sheet?

Depreciation expense, which reduces net income on the income statement, also reduces the book value of assets on the balance sheet, reflecting the decline in their value over time. This adjustment aligns the asset’s value with its remaining useful life, providing a more accurate representation of the company’s financial position.

Elaboration:

Depreciation is a crucial accounting concept that links the income statement and the balance sheet. It is the systematic allocation of the cost of a tangible asset over its useful life. When a company purchases an asset like machinery, equipment, or a building, it doesn’t expense the entire cost in the year of purchase. Instead, it spreads the cost over the asset’s useful life through depreciation.

Here’s how depreciation connects the two financial statements:

- Income Statement: Depreciation expense is recorded on the income statement as an operating expense. This reduces the company’s net income. The formula for calculating depreciation can vary, but a common method is the straight-line method, where the asset’s cost, less its salvage value, is divided by its useful life.

- Balance Sheet: On the balance sheet, the accumulated depreciation is recorded as a contra-asset account. This account reduces the book value of the related asset. For example, if a company has equipment with an original cost of $100,000 and accumulated depreciation of $30,000, the net book value of the equipment on the balance sheet would be $70,000.

Impact on Cash Flow Statement: While depreciation reduces net income on the income statement, it’s a non-cash expense. Therefore, it’s added back to net income in the cash flow from operations section of the cash flow statement.

The depreciation schedule is a key tool in this process, detailing the annual depreciation expense for each asset, which is essential for accurate financial modeling and analysis. This schedule ensures that the depreciation expense is accurately reflected on the income statement and that the balance sheet reflects the correct net book value of the assets. According to a study by Harvard Business Review in June 2024, effective depreciation management is crucial for accurately portraying a company’s financial health and investment strategy.

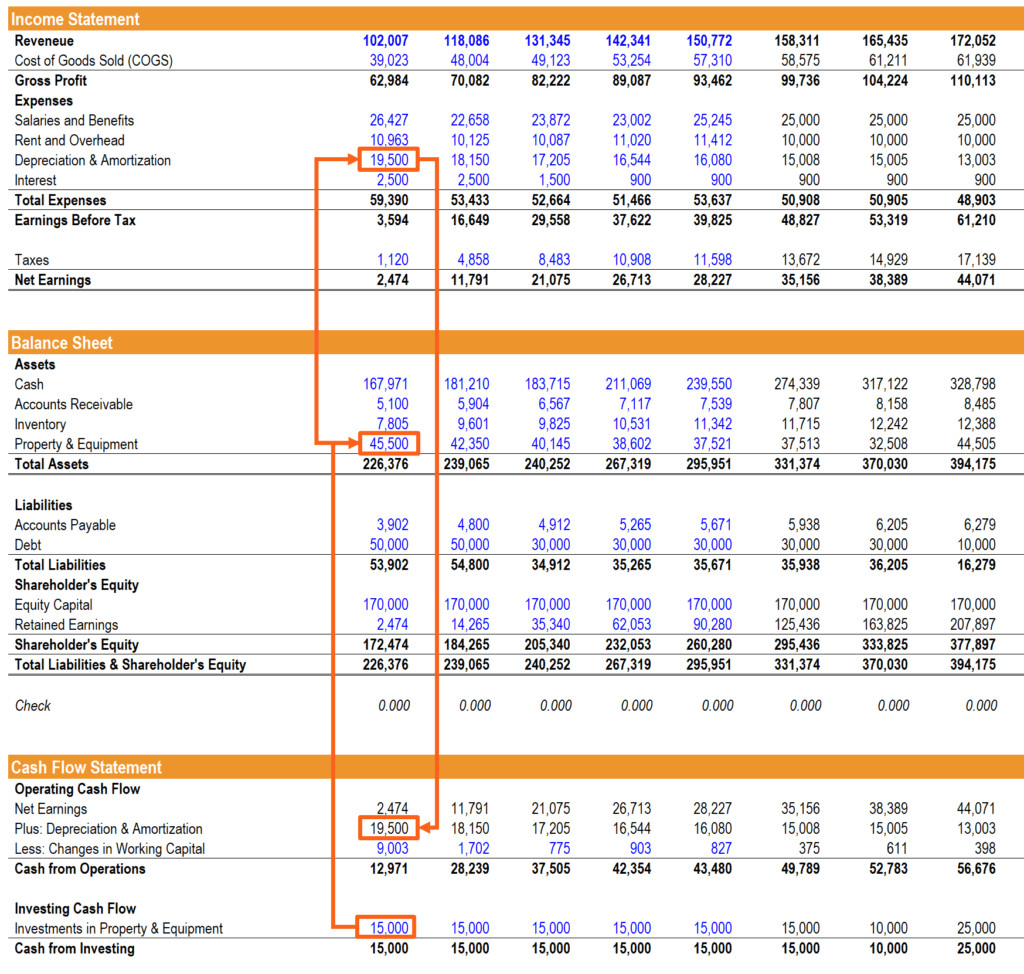

Example of 3 Financial Statements Linked – PP&E, Depreciation, and Capex

Example of 3 Financial Statements Linked – PP&E, Depreciation, and Capex

Linking Financial Statements: Understand how PP&E, depreciation, and capital expenditures connect the balance sheet, income statement, and cash flow statement.

4. How Do Changes in Working Capital Impact Both Financial Statements?

Changes in working capital affect the income statement by influencing revenues and expenses, while also impacting the cash flow statement as they reflect the actual cash inflows and outflows. Effective management of working capital is crucial for ensuring a company’s short-term financial health and liquidity.

Elaboration:

Working capital, which is the difference between a company’s current assets and current liabilities, is a critical measure of its short-term liquidity and operational efficiency. Changes in working capital can significantly impact both the income statement and the balance sheet.

Here’s how working capital affects the two financial statements:

-

Balance Sheet: Working capital components such as accounts receivable, inventory, and accounts payable are all current assets and liabilities listed on the balance sheet. Changes in these accounts directly affect the company’s financial position at a specific point in time.

- Accounts Receivable: An increase in accounts receivable means the company has made sales but hasn’t yet collected cash, increasing current assets.

- Inventory: An increase in inventory means the company has purchased or produced more goods but hasn’t sold them, also increasing current assets.

- Accounts Payable: An increase in accounts payable means the company has purchased goods or services but hasn’t yet paid for them, increasing current liabilities.

-

Cash Flow Statement: Changes in working capital accounts are reflected in the cash flow from operations section.

- Increase in Accounts Receivable: This is a use of cash because the company has made sales but hasn’t received cash, so it’s subtracted from net income.

- Increase in Inventory: This is also a use of cash because the company has spent cash to purchase or produce more goods, so it’s subtracted from net income.

- Increase in Accounts Payable: This is a source of cash because the company hasn’t yet paid for goods or services, so it’s added to net income.

Changes in working capital are vital for assessing a company’s operational efficiency. Effective management of working capital ensures that a company can meet its short-term obligations and invest in growth opportunities. According to a study by Entrepreneur.com in August 2023, optimizing working capital is essential for improving a company’s cash flow and overall financial stability.

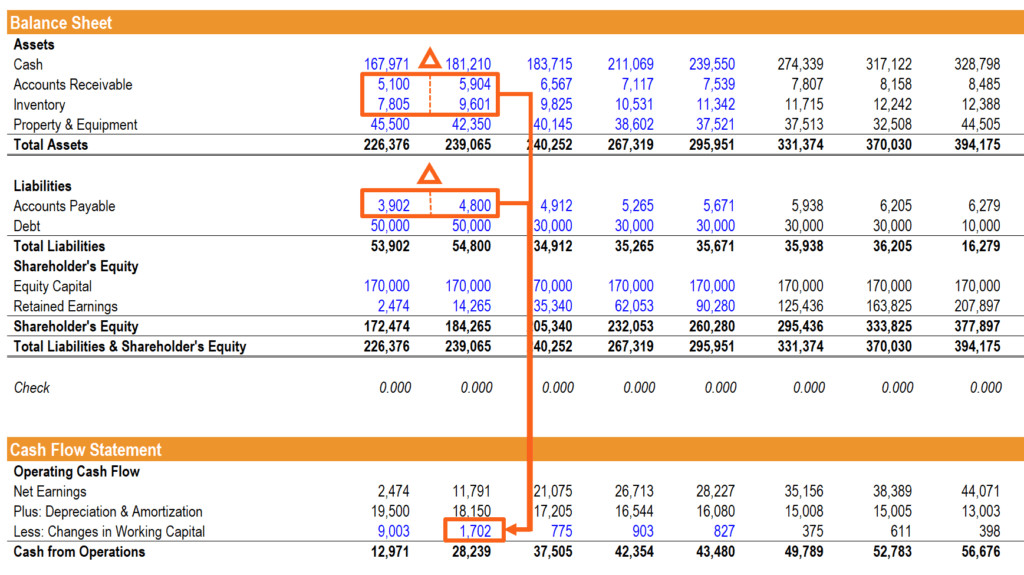

Example of Balance Sheet Linked to Cash Flow Statement

Example of Balance Sheet Linked to Cash Flow Statement

Balance Sheet and Cash Flow Statement: Discover how working capital changes link the balance sheet to the cash flow statement.

5. How Do Financing Activities Influence the Income Statement and Balance Sheet?

Financing activities, such as issuing debt or equity, affect the balance sheet by altering liabilities and equity, while the interest expense from debt impacts the income statement. Proper modeling of debt schedules and understanding the nuances of financing are critical for linking the three financial statements accurately.

Elaboration:

Financing activities involve how a company raises capital to fund its operations and investments. These activities have a significant impact on both the income statement and the balance sheet. Understanding these impacts is essential for creating accurate and comprehensive financial models.

Here’s how financing activities affect the two financial statements:

- Balance Sheet:

- Issuing Debt: When a company issues debt, such as bonds or loans, it increases its liabilities on the balance sheet. The cash received from the debt issuance increases the company’s assets (specifically, cash).

- Issuing Equity: When a company issues equity, such as common stock, it increases its equity on the balance sheet. The cash received from the equity issuance also increases the company’s assets.

- Repaying Debt: When a company repays debt, it decreases its liabilities on the balance sheet. The cash used for the repayment decreases the company’s assets.

- Paying Dividends: When a company pays dividends to shareholders, it decreases its equity on the balance sheet. The cash used for the dividend payment decreases the company’s assets.

- Income Statement:

- Interest Expense: Debt financing results in interest expense, which is recorded on the income statement. Interest expense reduces the company’s net income. The amount of interest expense depends on the interest rate and the outstanding debt balance.

A debt schedule is a detailed table that outlines the terms of a company’s debt, including the initial balance, interest rate, payment frequency, and principal and interest payments over time. This schedule is essential for forecasting interest expense on the income statement and tracking the outstanding debt balance on the balance sheet.

Understanding the nuances of financing activities and their impact on the income statement and balance sheet is critical for financial analysis and decision-making. According to financial experts at income-partners.net, accurately modeling financing activities provides a clearer picture of a company’s financial health and its ability to manage its capital structure effectively.

6. Why Is the Cash Balance the Final Step in Linking Financial Statements?

The cash balance is the final check to ensure that all components of the three financial statements are accurately linked, reflecting the cumulative impact of operating, investing, and financing activities. Ensuring the cash balance is accurate confirms the overall integrity of the financial model.

Elaboration:

The cash balance acts as the ultimate reconciliation point when linking the three financial statements: the income statement, the balance sheet, and the cash flow statement. It represents the cumulative effect of all financial activities and serves as a critical validation of the accuracy and integrity of the financial model.

Here’s why the cash balance is the final step and how it ensures that all components are accurately linked:

-

Comprehensive Reflection of Activities: The cash balance reflects all cash inflows and outflows resulting from a company’s operating, investing, and financing activities.

- Operating Activities: These activities include the cash generated from the company’s core business operations, such as sales of goods or services, and the cash spent on expenses like salaries, rent, and utilities.

- Investing Activities: These activities include the purchase and sale of long-term assets, such as property, plant, and equipment (PP&E), as well as investments in securities.

- Financing Activities: These activities involve how the company raises capital, such as issuing debt or equity, and how it returns capital to investors, such as repaying debt or paying dividends.

-

Reconciliation Process: The cash flow statement starts with the net income from the income statement and adjusts it for non-cash items and changes in working capital to arrive at the cash from operations. It then adds or subtracts the cash from investing and financing activities to arrive at the net change in cash. This net change in cash is then added to the beginning cash balance from the previous period to arrive at the ending cash balance for the current period.

-

Verification of Accuracy: The ending cash balance calculated on the cash flow statement must match the cash balance reported on the balance sheet for the same period. If these two figures do not match, it indicates an error in the financial model, requiring a thorough review of all linked components.

According to financial analysts at income-partners.net, achieving an accurate cash balance is paramount in financial modeling, ensuring that the interconnectedness of the three financial statements is correctly represented. This accuracy is crucial for making informed financial decisions and providing reliable insights into a company’s financial performance and position.

7. How Can Financial Modeling in Excel Help Link the Financial Statements?

Financial modeling in Excel provides a structured approach to link the three financial statements by creating formulas and relationships that automatically update as data changes. This enables dynamic analysis and forecasting.

Elaboration:

Financial modeling in Excel is an essential tool for linking the three financial statements—the income statement, the balance sheet, and the cash flow statement—in a dynamic and integrated manner. By creating a financial model, analysts can establish relationships between different line items across the statements, allowing for automatic updates and scenario analysis as data changes.

Here’s how financial modeling in Excel helps link the financial statements:

- Structured Approach: Financial modeling provides a structured framework for organizing and analyzing financial data. The model typically includes sections for historical data, assumptions, and forecasted financials.

- Formula-Based Relationships: Excel allows you to create formulas that link different line items across the financial statements. For example:

- Net income from the income statement is linked to the retained earnings account on the balance sheet.

- Depreciation expense from the income statement is linked to the accumulated depreciation account on the balance sheet and is added back in the cash flow from operations section of the cash flow statement.

- Changes in working capital accounts (such as accounts receivable, inventory, and accounts payable) on the balance sheet are linked to the cash flow from operations section of the cash flow statement.

- Capital expenditures (CapEx) are linked to the property, plant, and equipment (PP&E) account on the balance sheet and are reflected in the cash flow from investing section of the cash flow statement.

- Debt and equity financing activities are linked to the balance sheet and the cash flow from financing section of the cash flow statement.

- Dynamic Analysis: Once the financial statements are linked, changes in one area of the model automatically flow through to the other statements.

- Scenario Planning: Financial models in Excel enable scenario planning by allowing analysts to create multiple scenarios with different assumptions and see how these scenarios impact the company’s financial performance and position. For example, analysts can create best-case, worst-case, and most-likely scenarios to assess the potential range of outcomes.

According to financial modeling experts at income-partners.net, the ability to create dynamic and integrated financial models in Excel is crucial for financial analysis, forecasting, and decision-making. These models provide a comprehensive view of a company’s financial performance and position, enabling stakeholders to make informed decisions.

8. What Are Some Common Mistakes to Avoid When Linking Financial Statements?

Common mistakes include incorrect formulas, not properly accounting for non-cash items, and failing to ensure the cash balance matches across the balance sheet and cash flow statement. Avoiding these errors is crucial for maintaining the accuracy of financial models.

Elaboration:

When linking financial statements, several common mistakes can compromise the accuracy and reliability of the financial model. Avoiding these pitfalls is crucial for ensuring that the financial statements are correctly integrated and provide a true reflection of the company’s financial performance and position.

Here are some common mistakes to avoid:

- Incorrect Formulas:

- Description: Using incorrect or outdated formulas is one of the most common mistakes.

- How to Avoid: Double-check all formulas to ensure they accurately reflect the relationships between different line items on the financial statements. Use cell referencing and named ranges to make formulas easier to understand and maintain.

- Not Properly Accounting for Non-Cash Items:

- Description: Failing to adjust for non-cash items, such as depreciation and amortization, can lead to inaccuracies in the cash flow statement.

- How to Avoid: Ensure that all non-cash items are properly added back or subtracted in the cash flow from operations section of the cash flow statement. Create a detailed depreciation schedule to track depreciation expense accurately.

- Failing to Ensure the Cash Balance Matches:

- Description: The ending cash balance on the cash flow statement must match the cash balance on the balance sheet. If these two figures do not match, it indicates an error in the financial model.

- How to Avoid: Regularly reconcile the cash balance on the cash flow statement with the cash balance on the balance sheet. Identify and correct any discrepancies.

- Ignoring Changes in Working Capital:

- Description: Failing to account for changes in working capital accounts (such as accounts receivable, inventory, and accounts payable) can lead to inaccuracies in the cash flow from operations section of the cash flow statement.

- How to Avoid: Track changes in working capital accounts and adjust the cash flow statement accordingly.

- Overlooking Financing Activities:

- Description: Not properly accounting for financing activities, such as debt and equity issuances and repayments, can lead to errors in the balance sheet and cash flow statement.

- How to Avoid: Create detailed debt and equity schedules to track financing activities accurately. Link these schedules to the balance sheet and cash flow statement.

According to financial modeling experts at income-partners.net, avoiding these common mistakes is essential for building accurate and reliable financial models. Regular reviews and reconciliations can help identify and correct errors, ensuring that the financial statements are correctly linked and provide a true reflection of the company’s financial performance and position.

9. How Can Understanding These Links Improve Financial Analysis?

Understanding the links between financial statements enables a more comprehensive financial analysis, allowing analysts to assess a company’s performance and financial health more accurately. This knowledge supports better investment and strategic decisions.

Elaboration:

Understanding the links between the three financial statements—the income statement, the balance sheet, and the cash flow statement—is crucial for conducting a thorough and effective financial analysis. This understanding allows analysts to assess a company’s performance and financial health more accurately, leading to better-informed investment and strategic decisions.

Here are several ways that understanding these links can improve financial analysis:

- Comprehensive Performance Assessment: By understanding how the financial statements are linked, analysts can gain a more comprehensive view of a company’s performance.

- Improved Forecasting and Valuation: Understanding the links between the financial statements enables more accurate forecasting and valuation.

- Enhanced Risk Assessment: Understanding the links between the financial statements allows for a more thorough assessment of a company’s financial risks.

According to financial analysts at income-partners.net, a deep understanding of the links between the financial statements is essential for effective financial analysis. This understanding enables analysts to assess a company’s performance and financial health more accurately, leading to better-informed investment and strategic decisions.

10. Where Can I Find More Resources to Learn About Financial Statement Linking?

You can find additional resources at income-partners.net, which offers insights into financial modeling, partnership strategies, and collaborative opportunities for business growth. These resources can help you deepen your understanding and improve your financial analysis skills.

Elaboration:

To further enhance your understanding of financial statement linking and its applications, several resources are available to deepen your knowledge and improve your financial analysis skills. These resources range from online courses and tutorials to professional certifications and industry publications.

Here are some recommended resources:

- Online Courses and Tutorials:

- income-partners.net: Offers insights into financial modeling, partnership strategies, and collaborative opportunities for business growth. These resources can help you deepen your understanding and improve your financial analysis skills.

- Professional Certifications:

- Chartered Financial Analyst (CFA): The CFA program covers financial statement analysis in depth and is highly regarded in the finance industry.

- Industry Publications:

- The Wall Street Journal: Provides daily coverage of financial news and analysis, including articles on financial statement analysis and corporate performance.

- Bloomberg: Offers financial data, news, and analytics, including in-depth coverage of financial statement analysis and corporate finance.

By leveraging these resources, you can deepen your understanding of financial statement linking and its applications, improving your financial analysis skills and decision-making capabilities.

At income-partners.net, we provide the tools and knowledge you need to excel in financial statement analysis and strategic partnerships. Explore our resources today to unlock new opportunities for business growth and financial success.

Ready to take your financial analysis to the next level? Visit income-partners.net to explore partnership opportunities, learn effective financial modeling techniques, and connect with potential collaborators in the USA, especially in thriving hubs like Austin. Don’t miss out on the chance to enhance your financial knowledge and drive your business forward. Contact us today at 1 University Station, Austin, TX 78712, United States or call +1 (512) 471-3434.