How Is Bad Debt Expense Reported On The Income Statement, and what does it mean for your business? Bad debt expense represents the portion of accounts receivable that a company deems uncollectible, directly impacting profitability; income-partners.net provides expert insights and strategies to manage and minimize this expense. Understanding how to report bad debt accurately is crucial for financial transparency and attracting potential partners; learn about allowance for doubtful accounts and accounts receivable aging to improve your business’s financial health, optimizing partnership potential.

1. Understanding Bad Debt Expense

Bad debt expense represents the estimated amount of credit sales that a business does not expect to collect. It is a crucial accounting concept, especially for businesses that offer credit to their customers. Recognizing and accurately reporting bad debt expense is vital for maintaining a transparent and realistic financial picture.

1.1. What is Bad Debt Expense?

Bad debt expense (BDE) is the portion of a company’s accounts receivable that is considered uncollectible. It reflects the risk inherent in extending credit to customers and is an inevitable part of doing business for many companies. This expense is recorded on the income statement, reducing the company’s profit.

1.2. Why is Bad Debt Expense Important?

Recognizing and managing bad debt expense is important for several reasons:

- Accurate Financial Reporting: It provides a more realistic view of a company’s financial health by recognizing potential losses from uncollectible accounts.

- Decision Making: It helps management make informed decisions about credit policies, sales strategies, and risk management.

- Investor Confidence: It enhances investor confidence by demonstrating a company’s awareness and management of credit risks.

1.3. Accrual vs. Cash Accounting

The method of accounting a company uses—accrual or cash—determines how bad debt expense is handled.

- Accrual Accounting: This method recognizes revenue when earned, regardless of when cash is received. Bad debt expense is necessary to adjust for uncollectible accounts.

- Cash Accounting: This method recognizes revenue only when cash is received. Bad debt expense is not typically used because revenue is not recorded until payment is made.

2. Methods for Recording Bad Debt Expense

There are two primary methods for recording bad debt expense: the direct write-off method and the allowance method. Each has its own advantages and disadvantages, and the choice depends on the company’s accounting policies and the nature of its receivables.

2.1. The Direct Write-Off Method

The direct write-off method recognizes bad debt expense only when an account is deemed uncollectible. When a specific invoice is determined to be uncollectible, it is written off directly to bad debt expense.

2.1.1. How it Works

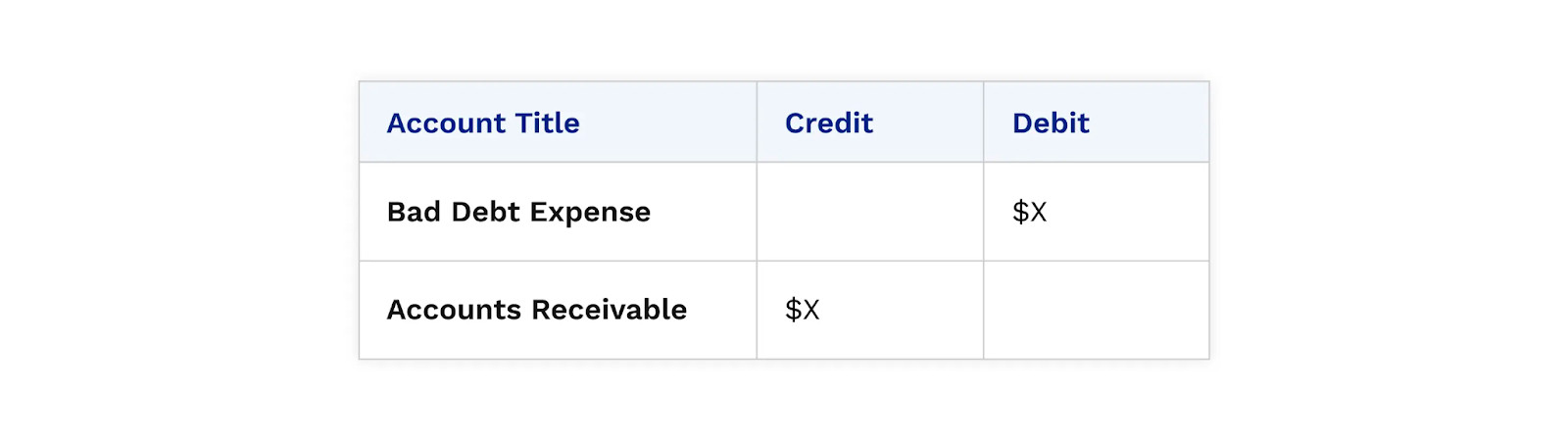

When an account is deemed uncollectible, the following journal entry is made:

- Debit: Bad Debt Expense

- Credit: Accounts Receivable

2.1.2. Advantages and Disadvantages

- Advantages: Simple to implement and understand.

- Disadvantages: It does not adhere to the matching principle (matching revenues with associated expenses in the same period) and can distort financial statements if bad debts are material.

2.1.3. When to Use

The direct write-off method is suitable for small businesses with immaterial bad debts or those using cash accounting. However, it is not generally accepted under GAAP (Generally Accepted Accounting Principles) for companies with significant receivables.

2.2. The Allowance Method

The allowance method is a more sophisticated approach that estimates bad debt expense and creates an allowance for doubtful accounts. This method aligns with the matching principle and provides a more accurate representation of a company’s financial position.

2.2.1. How it Works

- Estimate Bad Debt Expense: At the end of each accounting period, estimate the amount of accounts receivable that are likely to be uncollectible.

- Create Allowance for Doubtful Accounts (AFDA): Establish a contra-asset account called “Allowance for Doubtful Accounts” to reduce the carrying value of accounts receivable.

- Record Bad Debt Expense: Debit Bad Debt Expense and credit AFDA for the estimated amount.

- Write-Off Uncollectible Accounts: When a specific account is deemed uncollectible, debit AFDA and credit Accounts Receivable.

2.2.2. Advantages and Disadvantages

- Advantages: Adheres to the matching principle, provides a more accurate picture of financial health, and smooths out income fluctuations.

- Disadvantages: Requires estimation, which can be subjective and complex.

2.2.3. When to Use

The allowance method is required by GAAP for companies with material accounts receivable balances because it provides a more accurate and reliable representation of the company’s financial condition.

3. Estimating Bad Debt Expense Under the Allowance Method

Estimating bad debt expense under the allowance method involves several techniques, each with its own nuances. The most common methods are the percentage of sales method, the percentage of accounts receivable method, and the aging of accounts receivable method.

3.1. Percentage of Sales Method

The percentage of sales method estimates bad debt expense as a percentage of credit sales. This method is straightforward and focuses on the relationship between sales and potential uncollectible accounts.

3.1.1. How it Works

- Determine Historical Percentage: Calculate the historical percentage of uncollectible sales by dividing total bad debt losses by total credit sales over a period of time.

- Apply Percentage to Current Sales: Multiply the current period’s credit sales by the historical percentage to estimate bad debt expense.

- Record Adjustment: Record the resulting amount as an adjustment to the AFDA balance; when recording bad debt expense on the income statement, record the adjustment value.

3.1.2. Example

Suppose a company has historical average annual credit sales of $1,000,000 and historical average uncollected credit sales of $20,000. The historical percentage of uncollected credit sales is 2% ($20,000 / $1,000,000).

If the current period’s credit sales are $1,200,000, the estimated bad debt expense would be 2% of $1,200,000, which equals $24,000.

3.1.3. Pros and Cons

- Pros: Simple and easy to calculate, directly related to sales volume.

- Cons: May not accurately reflect the current collectability of accounts receivable, ignores existing AFDA balances.

3.2. Percentage of Accounts Receivable Method

The percentage of accounts receivable method estimates bad debt expense as a percentage of the outstanding accounts receivable balance. This method focuses on the collectability of the receivables at a specific point in time.

3.2.1. How it Works

- Determine Historical Percentage: Calculate the historical percentage of uncollectible receivables by dividing total bad debt losses by total accounts receivable over a period of time.

- Apply Percentage to Current Receivables: Multiply the current period’s accounts receivable balance by the historical percentage to estimate the required AFDA balance.

- Calculate Adjustment: Determine the necessary adjustment to the AFDA balance by comparing the required balance to the existing balance.

3.2.2. Example

Suppose a company has historical average accounts receivable of $500,000 and historical average uncollected receivables of $30,000. The historical percentage of uncollected receivables is 6% ($30,000 / $500,000).

If the current period’s accounts receivable balance is $600,000, the estimated required AFDA balance would be 6% of $600,000, which equals $36,000. If the existing AFDA balance is $10,000, the adjustment to bad debt expense would be $26,000 ($36,000 – $10,000).

3.2.3. Pros and Cons

- Pros: More accurate reflection of the current collectability of accounts receivable.

- Cons: Relies on historical data, which may not accurately predict future collectability, requires careful monitoring of AFDA balance.

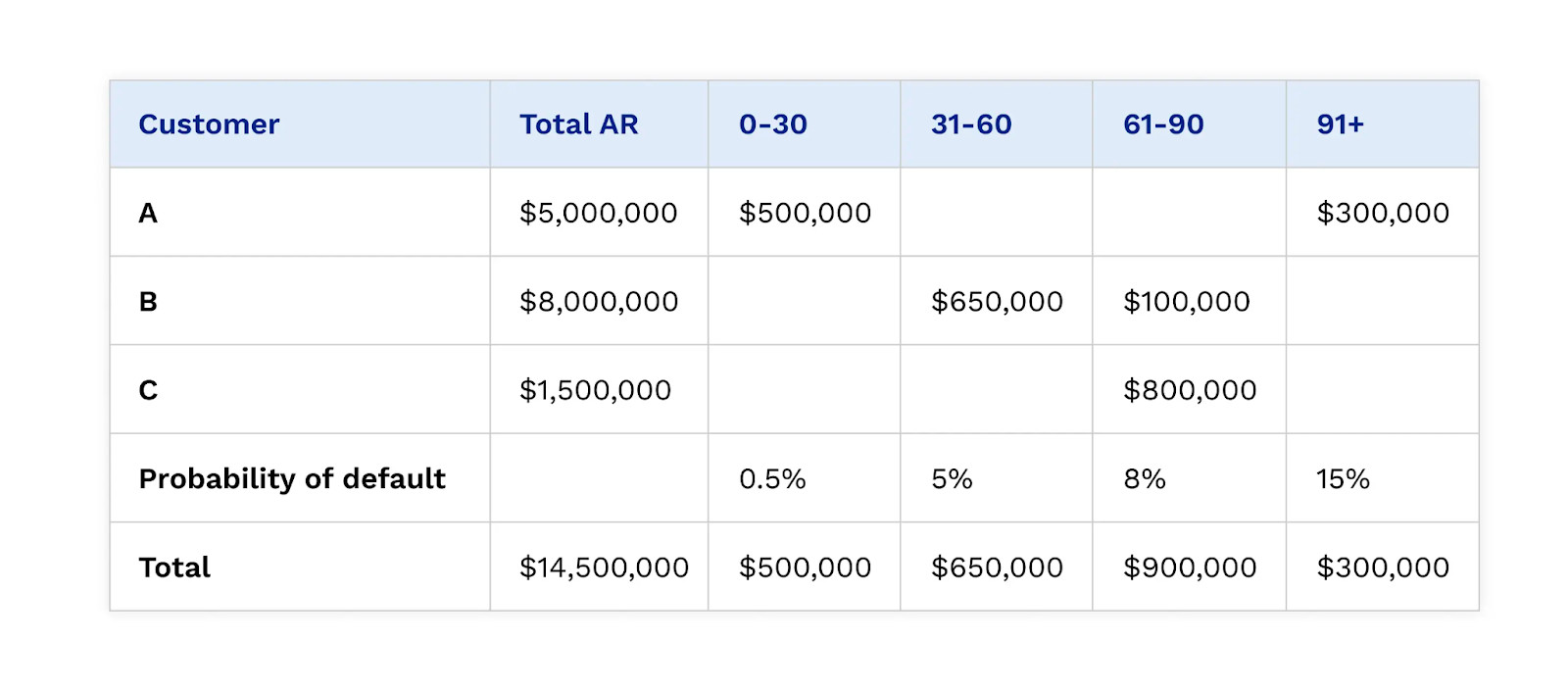

3.3. Aging of Accounts Receivable Method

The aging of accounts receivable method categorizes accounts receivable by age and assigns a different percentage of uncollectability to each category. This method provides a more detailed and accurate estimate of bad debt expense.

3.3.1. How it Works

- Create Aging Schedule: Prepare a schedule that categorizes accounts receivable by age (e.g., current, 1-30 days past due, 31-60 days past due, over 60 days past due).

- Assign Uncollectability Percentages: Assign a percentage of uncollectability to each aging category based on historical experience and industry data.

- Calculate Bad Debt Allowance: Multiply the balance in each aging category by its corresponding uncollectability percentage. Sum the results to determine the required AFDA balance.

- Calculate Adjustment: Determine the necessary adjustment to the AFDA balance by comparing the required balance to the existing balance.

3.3.2. Example

Consider the following aging schedule:

| Aging Category | Balance | Uncollectability Percentage | Estimated Uncollectible |

|---|---|---|---|

| Current | $200,000 | 1% | $2,000 |

| 1-30 days past due | $50,000 | 5% | $2,500 |

| 31-60 days past due | $30,000 | 10% | $3,000 |

| Over 60 days past due | $20,000 | 20% | $4,000 |

| Total | $300,000 | $11,500 |

The required AFDA balance is $11,500. If the existing AFDA balance is $5,000, the adjustment to bad debt expense would be $6,500 ($11,500 – $5,000).

3.3.3. Pros and Cons

- Pros: Most accurate method, considers the age of receivables, provides a detailed analysis of collectability.

- Cons: More complex and time-consuming, requires careful analysis of historical data.

Accounts Receivable Aging Report Example

Accounts Receivable Aging Report Example

4. Presentation on the Income Statement

The presentation of bad debt expense on the income statement is relatively straightforward. It is typically included as an operating expense, usually within the selling, general, and administrative (SG&A) expenses section.

4.1. Where to Report

Bad debt expense is reported as an operating expense on the income statement. It reduces the company’s operating income and, consequently, its net income.

4.2. Format

The typical format for reporting bad debt expense is as follows:

Income Statement (Partial)

- Revenue

- Cost of Goods Sold

- Gross Profit

- Operating Expenses:

- Salaries and Wages

- Rent Expense

- Bad Debt Expense

- Depreciation Expense

- Other Operating Expenses

- Operating Income

4.3. Impact on Financial Ratios

Bad debt expense affects several key financial ratios, including:

- Profit Margin: Higher bad debt expense reduces net income, decreasing the profit margin.

- Return on Assets (ROA): Lower net income reduces ROA, indicating lower efficiency in using assets to generate profit.

- Receivables Turnover: While not directly impacted, a high bad debt expense may indicate issues with credit policies, which can affect receivables turnover.

5. Factors Influencing Bad Debt Expense

Several internal and external factors can influence a company’s bad debt expense. Understanding these factors can help management proactively manage credit risk and minimize losses.

5.1. Internal Factors

- Credit Policies: Lax credit policies, such as extending credit to high-risk customers, can increase bad debt expense.

- Collection Practices: Inefficient collection practices can result in delayed payments and higher uncollectible accounts.

- Sales Practices: Aggressive sales tactics that prioritize volume over creditworthiness can lead to increased bad debt.

5.2. External Factors

- Economic Conditions: Economic downturns can increase the likelihood of customers defaulting on their payments.

- Industry Trends: Certain industries may have inherently higher credit risks due to the nature of their business or customer base.

- Competition: Intense competition may lead to looser credit terms to attract customers, increasing the risk of bad debt.

6. Strategies to Minimize Bad Debt Expense

Minimizing bad debt expense requires a proactive and strategic approach to credit management. Companies can implement several strategies to reduce their exposure to uncollectible accounts.

6.1. Implement Strict Credit Policies

Establish clear and consistent credit policies to evaluate the creditworthiness of potential customers. This includes:

- Credit Checks: Conducting thorough credit checks on new customers.

- Credit Limits: Setting appropriate credit limits based on creditworthiness.

- Payment Terms: Clearly defining payment terms and enforcing them consistently.

6.2. Improve Collection Practices

Implement efficient collection practices to ensure timely payments. This includes:

- Prompt Invoicing: Sending invoices promptly after the sale.

- Regular Follow-Up: Following up on overdue accounts regularly.

- Payment Reminders: Sending payment reminders before the due date.

6.3. Offer Incentives for Early Payment

Encourage customers to pay early by offering discounts or other incentives. This can improve cash flow and reduce the risk of bad debt.

6.4. Use Technology and Automation

Leverage technology and automation to streamline credit management and collection processes. Collaborative accounts receivable solutions such as Versapay can automate invoicing, collections, and payment processing workflows.

6.5. Monitor Accounts Receivable Aging

Regularly monitor the aging of accounts receivable to identify potential problem accounts early. This allows for timely intervention and collection efforts.

6.6. Insurance and Factoring

Consider using credit insurance or factoring services to mitigate the risk of bad debt. Credit insurance protects against losses from uncollectible accounts, while factoring involves selling receivables to a third party at a discount.

7. Bad Debt Expense in Different Industries

The level of bad debt expense can vary significantly across different industries due to factors such as the nature of the business, customer base, and economic conditions.

7.1. Retail Industry

Retail businesses often face higher bad debt expense due to the large volume of credit sales and the diverse customer base. Strategies to manage bad debt in retail include:

- Offering store credit cards with strict credit limits.

- Implementing loyalty programs to encourage timely payments.

- Using data analytics to identify high-risk customers.

7.2. Construction Industry

Construction companies may experience higher bad debt expense due to the long project cycles and the potential for disputes over payment terms. Strategies to manage bad debt in construction include:

- Requiring upfront deposits or progress payments.

- Using contracts with clear payment terms and dispute resolution mechanisms.

- Conducting thorough credit checks on subcontractors and suppliers.

7.3. Healthcare Industry

Healthcare providers often struggle with bad debt expense due to the complexities of insurance billing and patient payment responsibilities. Strategies to manage bad debt in healthcare include:

- Verifying insurance coverage before providing services.

- Offering payment plans and financial assistance programs.

- Outsourcing billing and collection services to specialized agencies.

8. Case Studies

Examining real-world case studies can provide valuable insights into how companies manage bad debt expense and the impact of effective credit management practices.

8.1. Case Study 1: XYZ Retail

XYZ Retail, a national chain of department stores, implemented a new credit scoring system to better assess the creditworthiness of new customers. As a result, they reduced their bad debt expense by 15% in the first year.

8.2. Case Study 2: ABC Construction

ABC Construction, a regional construction company, revised their contract terms to require progress payments at key milestones. This improved their cash flow and reduced their bad debt expense by 20%.

8.3. Case Study 3: 123 Healthcare

123 Healthcare, a multi-specialty clinic, implemented a patient financial counseling program to educate patients about their payment responsibilities and offer financial assistance options. This reduced their bad debt expense by 10%.

9. Legal and Regulatory Considerations

Companies must comply with various legal and regulatory requirements related to credit management and debt collection. These requirements can vary by jurisdiction and industry.

9.1. Fair Credit Reporting Act (FCRA)

The FCRA regulates the collection, use, and disclosure of consumer credit information. Companies must comply with the FCRA when conducting credit checks and reporting delinquent accounts to credit bureaus.

9.2. Fair Debt Collection Practices Act (FDCPA)

The FDCPA regulates the practices of debt collectors. Companies must comply with the FDCPA when collecting debts from consumers, including providing accurate information and avoiding abusive or deceptive practices.

9.3. State Laws

In addition to federal laws, companies must comply with state laws related to credit management and debt collection. These laws can vary significantly by state and may include requirements related to interest rates, late fees, and collection practices.

10. The Role of Collaborative Accounts Receivable

Collaborative accounts receivable solutions can play a significant role in minimizing bad debt expense by improving communication, streamlining processes, and enhancing customer relationships.

10.1. Improved Communication

Collaborative AR solutions facilitate better communication between AR staff, customers, and sales teams. This helps resolve disputes quickly and ensures that everyone is on the same page regarding payment terms and expectations.

10.2. Streamlined Processes

These solutions automate invoicing, collections, and payment processing workflows, reducing the risk of errors and delays. This allows AR staff to focus on more strategic tasks, such as identifying and resolving potential problem accounts.

10.3. Enhanced Customer Relationships

By providing customers with a seamless and transparent billing and payment experience, collaborative AR solutions can enhance customer relationships and increase the likelihood of timely payments.

10.4. Versapay Example

According to Versapay, collaborative AR minimizes bad debt expense through more transparent lines of communication, better alignment between sales and AR teams, and a greater focus on value-added work.

By implementing a collaborative AR solution, companies can significantly reduce their bad debt expense and improve their overall financial performance.

11. Future Trends in Bad Debt Management

The field of bad debt management is constantly evolving, with new technologies and strategies emerging to help companies mitigate credit risk.

11.1. Artificial Intelligence (AI)

AI-powered credit scoring systems can provide more accurate and predictive assessments of creditworthiness. AI can also be used to automate collection efforts and identify potential problem accounts early.

11.2. Blockchain Technology

Blockchain technology can enhance transparency and security in credit transactions, reducing the risk of fraud and disputes. Smart contracts can automate payment terms and enforce compliance.

11.3. Predictive Analytics

Predictive analytics can be used to forecast bad debt expense and identify factors that contribute to uncollectible accounts. This allows companies to proactively address potential issues and implement targeted strategies.

11.4. Machine Learning (ML)

Machine learning algorithms can analyze vast amounts of data to identify patterns and trends related to credit risk. This can help companies refine their credit policies and collection practices.

12. Conclusion: Optimizing Financial Health and Partnership Potential

Understanding how bad debt expense is reported on the income statement is crucial for maintaining financial transparency and making informed business decisions. By implementing effective credit management strategies and leveraging collaborative AR solutions like income-partners.net, companies can minimize bad debt expense, improve cash flow, and enhance customer relationships.

Accurate financial reporting and a proactive approach to credit risk management are essential for attracting potential partners and fostering long-term business success. Income-partners.net can help you navigate these challenges and optimize your financial health for partnership potential.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

Bad Debt Expense Journal Entry

Bad Debt Expense Journal Entry

FAQ on Bad Debt Expense Reporting

1. What Is Bad Debt Expense?

Bad debt expense is the portion of a company’s accounts receivable that is considered uncollectible, reflecting the risk of extending credit.

2. How Is Bad Debt Expense Reported on the Income Statement?

Bad debt expense is reported as an operating expense, typically within the selling, general, and administrative (SG&A) expenses section.

3. Why Is It Important to Accurately Report Bad Debt Expense?

Accurate reporting of bad debt expense provides a realistic view of a company’s financial health, aids decision-making, and enhances investor confidence.

4. What Are the Two Main Methods for Recording Bad Debt Expense?

The two main methods are the direct write-off method and the allowance method.

5. What Is the Direct Write-Off Method?

The direct write-off method recognizes bad debt expense only when an account is deemed uncollectible, debiting bad debt expense and crediting accounts receivable.

6. What Is the Allowance Method?

The allowance method estimates bad debt expense and creates an allowance for doubtful accounts, aligning with the matching principle.

7. What Are the Main Methods for Estimating Bad Debt Expense Under the Allowance Method?

The main methods are the percentage of sales method, the percentage of accounts receivable method, and the aging of accounts receivable method.

8. How Does the Percentage of Sales Method Work?

The percentage of sales method estimates bad debt expense as a percentage of credit sales.

9. How Does the Percentage of Accounts Receivable Method Work?

The percentage of accounts receivable method estimates bad debt expense as a percentage of the outstanding accounts receivable balance.

10. How Does the Aging of Accounts Receivable Method Work?

The aging of accounts receivable method categorizes accounts receivable by age and assigns a different percentage of uncollectability to each category.

Call to Action

Ready to optimize your financial health and unlock new partnership opportunities? Visit income-partners.net today to discover expert strategies, build valuable relationships, and minimize bad debt expense. Your path to financial success starts here!