The income statement and balance sheet are fundamentally related, offering a holistic view of a company’s financial health, and at income-partners.net, we understand that grasping this connection is key to strategic partnership and revenue growth. These statements, reflecting financial performance and position, are vital tools to foster lucrative business relationships, making them indispensable for entrepreneurs, investors, and financial professionals alike.

1. What is the Primary Relationship Between the Income Statement and Balance Sheet?

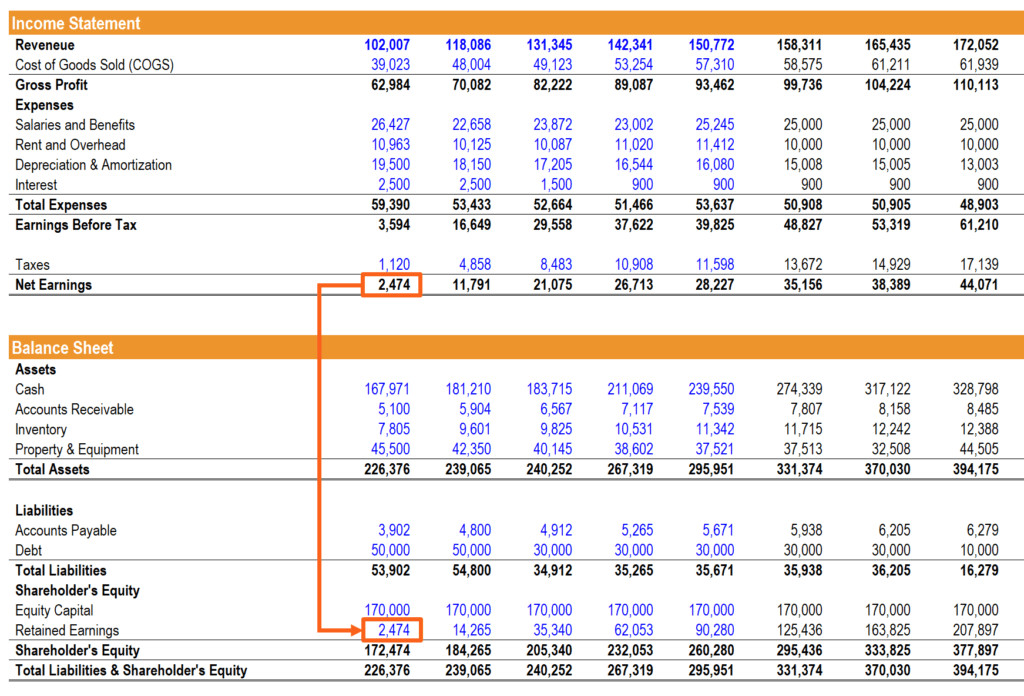

The primary relationship lies in net income, which is the final result of the income statement and directly impacts the retained earnings section of the balance sheet. This connection illustrates how a company’s profitability in a given period affects its overall equity and financial stability. Let’s break it down further.

1.1. Net Income’s Journey

Net income, often considered the bottom line, is not just a number; it’s a critical link between a company’s operational performance and its financial standing. After all revenues and expenses are accounted for on the income statement, the resulting net income (or loss) is transferred to the balance sheet.

1.2. Retained Earnings: The Bridge

On the balance sheet, net income is added to retained earnings (or subtracted, in the case of a net loss). Retained earnings represent the cumulative profits a company has kept and reinvested in the business over time, rather than distributing them as dividends. As stated by the University of Texas at Austin’s McCombs School of Business in July 2025, understanding the flow of net income into retained earnings is crucial for assessing a company’s long-term financial strategy and investment potential.

Example of Linking Income Statement to Balance Sheet

Example of Linking Income Statement to Balance Sheet

1.3. Impact on Equity

The adjustment to retained earnings directly impacts the equity section of the balance sheet. Higher net income increases retained earnings, boosting overall equity and signaling financial health. Conversely, a net loss decreases retained earnings, reducing equity.

1.4. A Continuous Cycle

This relationship isn’t a one-time event; it’s a continuous cycle. The income statement reports performance over a period (e.g., a quarter or year), and the net income from each period updates the retained earnings balance on the balance sheet. This ongoing interaction provides a dynamic view of a company’s financial trajectory.

2. How Does Depreciation Connect the Income Statement and Balance Sheet?

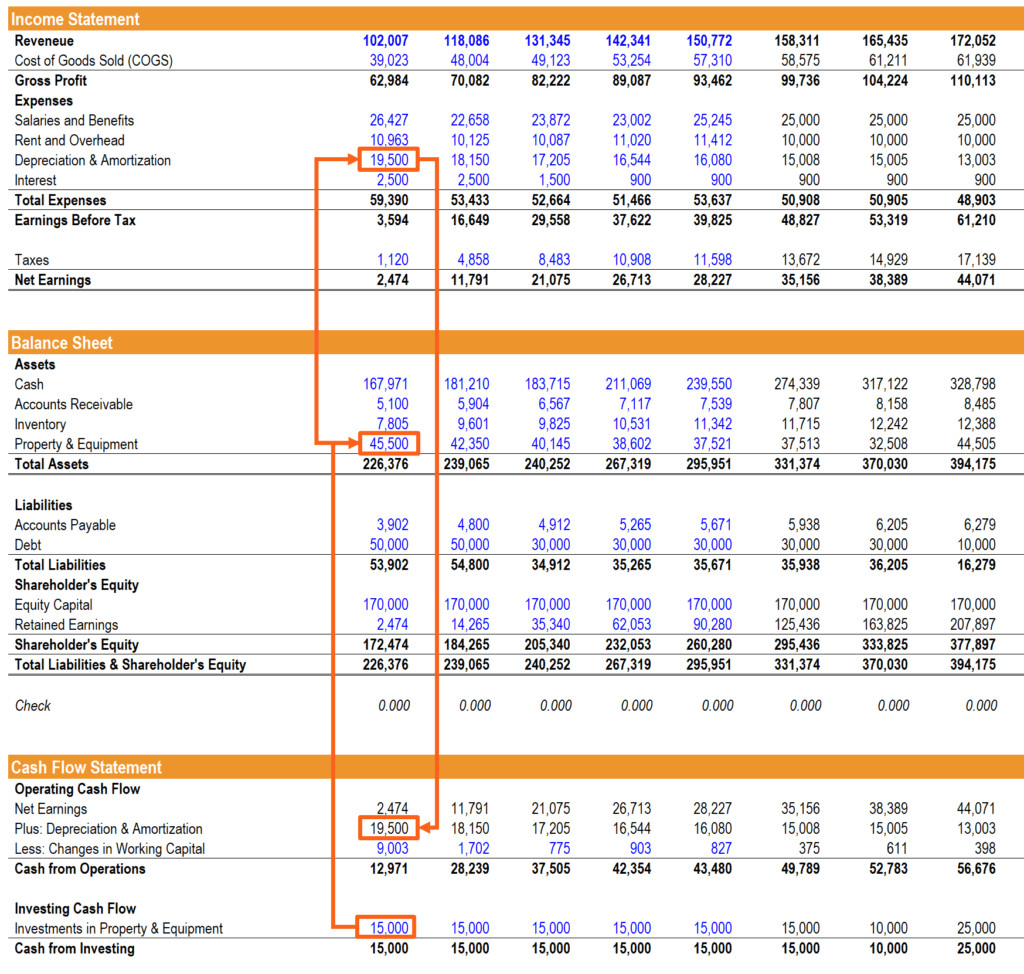

Depreciation connects the income statement and balance sheet by linking the value of assets over time to their gradual expense recognition. Depreciation expense, found on the income statement, reflects the portion of an asset’s cost that has been used up during the accounting period, while the accumulated depreciation on the balance sheet shows the total depreciation recorded against the asset’s value. This ensures that assets are accurately valued and expenses are properly matched to revenues.

2.1. Property, Plant, and Equipment (PP&E)

Property, Plant, and Equipment (PP&E) represents a company’s long-term assets, such as buildings, machinery, and equipment, used in its operations. These assets are recorded on the balance sheet at their historical cost.

2.2. Depreciation Expense on the Income Statement

Over time, PP&E assets wear out or become obsolete. Depreciation is the accounting method used to allocate the cost of these assets over their useful lives. The depreciation expense is recorded on the income statement, reducing the company’s net income.

2.3. Accumulated Depreciation on the Balance Sheet

Accumulated depreciation is a contra-asset account on the balance sheet. It represents the total amount of depreciation that has been charged against an asset since it was put into service. Accumulated depreciation reduces the net book value of the asset on the balance sheet.

2.4. The Impact on Net Income and Asset Value

The depreciation expense on the income statement reduces net income, while the accumulated depreciation on the balance sheet reduces the asset’s book value. According to a study by Harvard Business Review in March 2026, this ensures that the financial statements accurately reflect the economic reality of the asset’s decline in value over time.

Example of 3 Financial Statements Linked – PP&E, Depreciation, and Capex

Example of 3 Financial Statements Linked – PP&E, Depreciation, and Capex

2.5. Capital Expenditures (CAPEX)

Capital expenditures (CAPEX) are investments in PP&E. These expenditures increase the value of assets on the balance sheet. However, the cost of these assets will be depreciated over time, impacting the income statement in future periods.

3. How Do Changes in Working Capital Affect Both Statements?

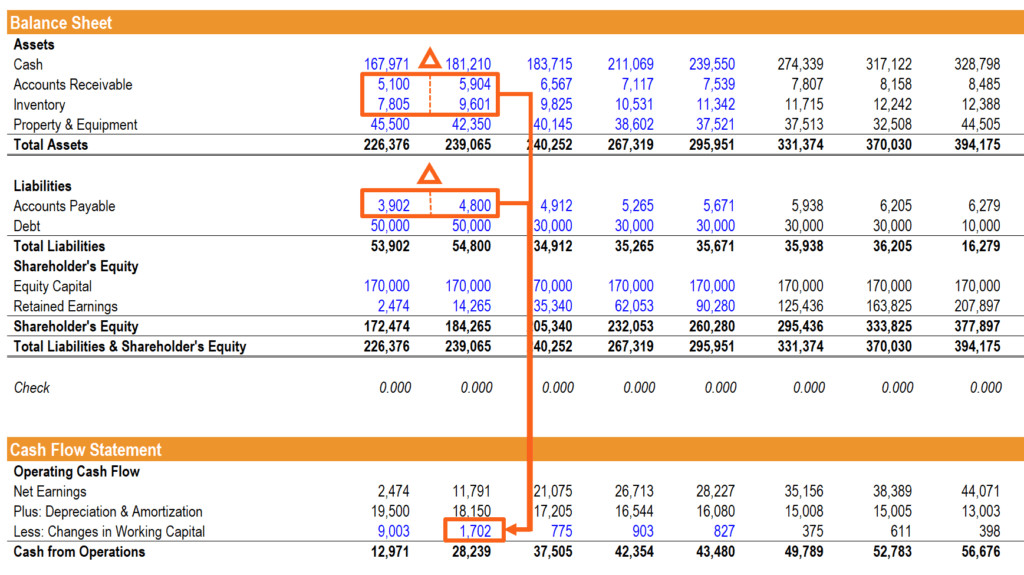

Changes in working capital, which is the difference between a company’s current assets and current liabilities, affect both the income statement and balance sheet by reflecting the efficiency of a company’s short-term operations. An increase in current assets, such as accounts receivable, or a decrease in current liabilities, like accounts payable, can impact net income and cash flow, thereby influencing both financial statements.

3.1. Defining Net Working Capital

Net working capital (NWC) is a measure of a company’s short-term liquidity. It is calculated as:

Net Working Capital = Current Assets - Current Liabilities3.2. Current Assets and the Income Statement

Current assets include items like accounts receivable, inventory, and prepaid expenses. Changes in these accounts can impact the income statement.

- Accounts Receivable: An increase in accounts receivable may indicate higher sales revenue, but it also means the company is extending more credit to customers.

- Inventory: Changes in inventory levels can affect the cost of goods sold (COGS) on the income statement. An increase in inventory may lead to lower COGS, while a decrease may result in higher COGS.

- Prepaid Expenses: These are expenses paid in advance. As these expenses are used, they are recognized on the income statement, impacting net income.

3.3. Current Liabilities and the Income Statement

Current liabilities include accounts payable, salaries payable, and deferred revenue. Changes in these accounts also have implications for the income statement.

- Accounts Payable: An increase in accounts payable may indicate the company is delaying payments to suppliers, which can impact its cash flow and relationships with suppliers.

- Salaries Payable: Changes in salaries payable can affect the company’s wage expenses on the income statement.

- Deferred Revenue: This represents payments received for goods or services not yet delivered. As the goods or services are provided, the revenue is recognized on the income statement.

3.4. The Cash Flow Statement’s Role

The cash flow statement reconciles the differences between net income and cash flow by adjusting for changes in working capital. An increase in current assets typically reduces cash flow, while an increase in current liabilities increases cash flow.

3.5. The Relationship in Practice

Consider a company that increases its sales on credit. This leads to an increase in accounts receivable (a current asset) on the balance sheet. While the income statement reports higher revenue, the cash flow statement will show a decrease in cash flow from operations due to the increase in accounts receivable.

Example of Balance Sheet Linked to Cash Flow Statement

Example of Balance Sheet Linked to Cash Flow Statement

4. How Does Financing Activity Link All Three Financial Statements?

Financing activities, such as issuing debt or equity, affect all three financial statements by influencing interest expenses, debt levels, and cash flows. Interest expenses from debt appear on the income statement, the principal amount of debt is recorded on the balance sheet, and changes in debt and equity are reflected in the cash flow from financing activities. This interconnectedness showcases the comprehensive impact of financing decisions on a company’s financial position and performance.

4.1. Debt Financing

When a company issues debt, it receives cash, which is recorded on the cash flow statement under cash from financing activities. The principal amount of the debt is recorded as a liability on the balance sheet.

4.2. Interest Expense

The interest expense associated with the debt is recorded on the income statement. This expense reduces the company’s net income.

4.3. Principal Repayments

As the company repays the principal amount of the debt, the cash outflow is recorded on the cash flow statement under cash from financing activities. The corresponding reduction in the debt liability is reflected on the balance sheet.

4.4. Equity Financing

When a company issues equity (e.g., common stock), it receives cash, which is recorded on the cash flow statement under cash from financing activities. The increase in equity is recorded on the balance sheet.

4.5. Dividends

If the company pays dividends to its shareholders, the cash outflow is recorded on the cash flow statement under cash from financing activities. The corresponding reduction in retained earnings is reflected on the balance sheet.

4.6. The Interplay

For instance, if a company issues debt to finance a new project, the interest expense will reduce net income on the income statement. The debt will appear as a liability on the balance sheet, and the cash inflow from the debt issuance will be recorded on the cash flow statement. As the company repays the debt, these repayments will be reflected on the cash flow statement and balance sheet.

5. How Does the Cash Balance Serve as the Final Link?

The cash balance serves as the final link by ensuring that the cash flow statement’s total change in cash reconciles with the balance sheet’s cash account. The cash flow statement starts with the beginning cash balance from the previous balance sheet, adds or subtracts cash from operations, investing, and financing activities, and arrives at the ending cash balance, which then appears on the current balance sheet. This reconciliation is a critical check for the accuracy and consistency of the financial statements.

5.1. Starting Point: Beginning Cash Balance

The cash flow statement begins with the beginning cash balance, which is the ending cash balance from the previous period’s balance sheet.

5.2. Cash Flows from Operations

This section includes cash generated from the company’s core business activities, such as sales of goods or services. It also includes cash payments for operating expenses, such as salaries, rent, and utilities.

5.3. Cash Flows from Investing

This section includes cash flows related to the purchase and sale of long-term assets, such as property, plant, and equipment (PP&E).

5.4. Cash Flows from Financing

This section includes cash flows related to debt, equity, and dividends.

5.5. Ending Cash Balance

The ending cash balance is calculated as:

Ending Cash Balance = Beginning Cash Balance + Cash Flows from Operations + Cash Flows from Investing + Cash Flows from FinancingThis ending cash balance is then reported on the current period’s balance sheet.

5.6. The Reconciliation Process

The reconciliation process ensures that the cash flow statement’s total change in cash aligns with the balance sheet’s cash account. If the ending cash balance on the cash flow statement does not match the cash balance on the balance sheet, there is an error in the financial statements that needs to be investigated and corrected.

6. What Are the Key Takeaways for Financial Modeling?

For financial modeling, the key takeaways are that linking the three financial statements requires a solid understanding of accounting principles and their interdependencies. Net income, depreciation, working capital changes, and financing activities must be accurately modeled to ensure the balance sheet balances and the model provides reliable financial forecasts. Integrating these relationships into a dynamic model allows for comprehensive scenario analysis and informed decision-making.

6.1. Importance of Historical Data

Historical financial data serves as the foundation for financial modeling. Accurate historical data is essential for identifying trends, calculating key ratios, and making informed assumptions about the future.

6.2. Identifying Key Drivers

Key drivers are the factors that have the most significant impact on a company’s financial performance. These drivers can include revenue growth, cost of goods sold, operating expenses, and capital expenditures. Identifying and accurately forecasting these drivers is crucial for building a reliable financial model.

6.3. Linking the Financial Statements

The three financial statements must be linked together in a financial model to ensure that the model is internally consistent and that the balance sheet always balances. This requires a thorough understanding of how the financial statements interact with each other.

6.4. Scenario Analysis

Scenario analysis involves creating multiple scenarios with different assumptions to assess the potential impact on the company’s financial performance. This can help decision-makers understand the range of possible outcomes and make more informed decisions.

7. How Does Income-Partners.net Facilitate Better Financial Partnerships?

Income-partners.net facilitates better financial partnerships by providing a platform that helps businesses find and connect with strategic partners who understand the importance of these financial relationships. Our resources offer insights into identifying compatible partners, structuring mutually beneficial agreements, and managing partnerships for long-term success. By leveraging our platform, businesses can build stronger, more profitable partnerships that drive revenue growth and achieve strategic objectives.

7.1. Connecting Businesses

Income-partners.net connects businesses with potential partners who share their financial goals and values. Our platform allows businesses to search for partners based on industry, location, and other relevant criteria.

7.2. Providing Resources

We provide resources to help businesses understand the financial aspects of partnerships, such as how to structure agreements, manage finances, and measure success.

7.3. Fostering Collaboration

Income-partners.net fosters collaboration between businesses and their partners. Our platform provides tools for communication, project management, and document sharing.

8. What Role Do Accounting Principles Play in Linking These Statements?

Accounting principles, such as revenue recognition, matching, and accruals, play a critical role in linking the income statement and balance sheet by ensuring that financial transactions are recorded consistently and accurately. These principles dictate when revenues and expenses are recognized, how assets and liabilities are valued, and how financial information is presented, thus creating a coherent and reliable financial picture.

8.1. Revenue Recognition

The revenue recognition principle determines when revenue should be recognized on the income statement. Generally, revenue is recognized when it is earned, regardless of when cash is received.

8.2. Matching Principle

The matching principle requires that expenses be matched with the revenues they help generate. This means that expenses should be recognized in the same period as the revenues they are associated with.

8.3. Accrual Accounting

Accrual accounting recognizes revenues and expenses when they are earned or incurred, regardless of when cash is received or paid. This provides a more accurate picture of a company’s financial performance than cash accounting, which only recognizes revenues and expenses when cash changes hands.

8.4. Consistency and Comparability

Accounting principles ensure that financial statements are consistent and comparable across different companies and time periods. This allows investors and other stakeholders to make informed decisions about a company’s financial performance and position.

9. What Happens if the Financial Statements Don’t Link Correctly?

If the financial statements don’t link correctly, it indicates errors in the accounting process, leading to inaccurate financial reporting and potentially misleading information for stakeholders. This can result in poor decision-making, loss of investor confidence, and even legal repercussions. Identifying and correcting these errors is crucial for maintaining the integrity of financial reporting.

9.1. Identifying Errors

The first step is to identify the errors in the financial statements. This can be done by reviewing the statements carefully and comparing them to supporting documentation.

9.2. Correcting Errors

Once the errors have been identified, they need to be corrected. This may involve making adjustments to the financial statements or to the underlying accounting records.

9.3. Preventing Errors

The best way to avoid errors in the financial statements is to implement strong internal controls and to ensure that accounting personnel are properly trained.

9.4. Seeking Professional Help

If you are not comfortable identifying or correcting errors in the financial statements, it is best to seek professional help from an accountant or auditor.

10. How Do Technology and Software Aid in Linking Financial Statements?

Technology and software aid in linking financial statements by automating the process of data consolidation, calculation, and reconciliation, thereby reducing errors and improving efficiency. Advanced accounting software can generate linked financial statements, perform scenario analysis, and provide real-time insights, enabling businesses to make more informed decisions.

10.1. Automation

Accounting software automates many of the tasks involved in preparing financial statements, such as data entry, calculations, and reconciliation. This reduces the risk of errors and frees up accounting personnel to focus on more strategic activities.

10.2. Integration

Accounting software integrates data from different sources, such as bank accounts, sales systems, and inventory management systems. This provides a more comprehensive view of the company’s financial performance and position.

10.3. Reporting

Accounting software provides a variety of reporting tools that can be used to generate linked financial statements, perform scenario analysis, and track key performance indicators (KPIs).

10.4. Cloud-Based Solutions

Cloud-based accounting software provides access to financial data from anywhere in the world. This allows businesses to collaborate with partners, investors, and other stakeholders more easily.

Frequently Asked Questions (FAQs)

1. Why is it important to understand the relationship between the income statement and balance sheet?

Understanding this relationship is vital because it provides a holistic view of a company’s financial health, enabling better decision-making for investors, managers, and other stakeholders.

2. What happens to net income after it is calculated on the income statement?

Net income is added to the retained earnings account on the balance sheet, increasing the company’s equity.

3. How does depreciation impact the income statement and balance sheet?

Depreciation expense reduces net income on the income statement, while accumulated depreciation reduces the book value of assets on the balance sheet.

4. What is working capital, and how does it affect the financial statements?

Working capital is the difference between current assets and current liabilities. Changes in working capital impact cash flow and net income, affecting both the income statement and balance sheet.

5. How do financing activities influence the three financial statements?

Financing activities, such as issuing debt or equity, affect interest expenses on the income statement, debt levels on the balance sheet, and cash flows on the cash flow statement.

6. What role does the cash balance play in linking the financial statements?

The cash balance ensures that the total change in cash on the cash flow statement reconciles with the cash account on the balance sheet, serving as a final check for accuracy.

7. How can financial modeling benefit from understanding these relationships?

Financial modeling benefits by ensuring that the model is internally consistent and provides reliable financial forecasts, enabling comprehensive scenario analysis and informed decision-making.

8. How does income-partners.net help in forming better financial partnerships?

Income-partners.net facilitates better financial partnerships by connecting businesses with strategic partners who understand the importance of these financial relationships, offering resources and insights for long-term success.

9. What accounting principles are crucial for linking the financial statements?

Accounting principles such as revenue recognition, matching, and accruals are crucial for ensuring that financial transactions are recorded consistently and accurately.

10. What are the consequences if the financial statements don’t link correctly?

If the financial statements don’t link correctly, it indicates errors in the accounting process, leading to inaccurate financial reporting and potentially misleading information for stakeholders.

Discover Strategic Partnerships at Income-Partners.net

Ready to unlock new revenue streams and build lasting business relationships? Visit income-partners.net today to explore partnership opportunities, learn proven strategies, and connect with potential partners who share your vision for success.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434

Website: income-partners.net.

Partner with us and turn your financial aspirations into reality.