COVID-19 has significantly impacted low-income families, exacerbating existing financial vulnerabilities; however, income-partners.net provides resources and strategies to navigate these challenges and explore partnership opportunities for income enhancement. This article delves into the financial struggles faced by these families, focusing on job losses, reduced income, and increased economic insecurity, while highlighting potential avenues for income growth and collaborative success. Partnering for prosperity and seeking financial stability are vital for low-income families facing economic hardships.

1. What Were the Initial Financial Impacts of COVID-19 on Low-Income Families?

The initial financial impacts were significant. Low-income families experienced job losses, reduced work hours, and increased economic insecurity as businesses closed and industries faced disruptions. According to a Pew Research Center analysis, lower-income households saw a 3.0% decrease in median income from 2019 to 2020, highlighting the immediate economic strain. This created difficulties in covering basic needs such as housing, food, and healthcare. Income volatility increased as many low-income workers found themselves in unstable employment situations. Many families had to rely on emergency savings or government assistance programs to make ends meet.

2. How Did Job Losses Affect Low-Income Households During the Pandemic?

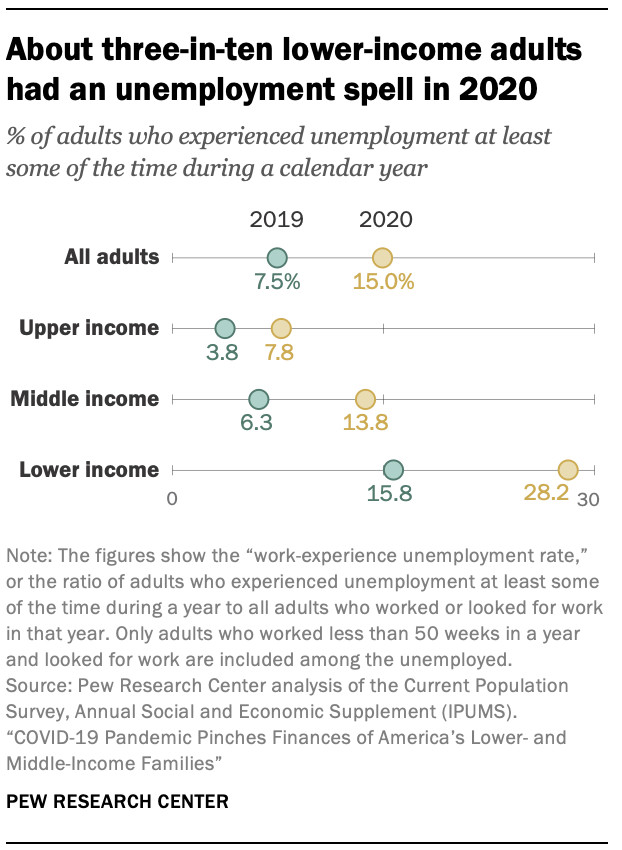

Job losses disproportionately affected low-income households. Many individuals in these families worked in sectors such as hospitality, retail, and service industries, which were severely impacted by lockdowns and social distancing measures. In 2020, about 28.2% of lower-income adults experienced unemployment at some point during the year, compared to 13.8% of middle-income adults and 7.8% of upper-income adults. The loss of employment led to a cascade of financial problems, including the inability to pay rent or mortgage, food insecurity, and lack of access to healthcare. The instability of the job market made it difficult for low-income families to plan for the future.

3. What Government Assistance Programs Were Available, and How Effective Were They?

Several government assistance programs, such as unemployment insurance and economic impact payments, provided crucial support to low-income families. The CARES Act, for example, established two rounds of economic impact payments that helped reduce poverty rates in 2020. In the 2021 CPS ASEC, approximately 97% of lower-income households reported receiving economic impact payments in 2020. However, despite these programs, many families still struggled to cover their basic needs due to the magnitude of the economic challenges. Eligibility requirements and delays in receiving assistance also posed barriers.

4. Did the Pandemic Widen the Income Gap Between Low-Income and High-Income Families?

Yes, the pandemic widened the income gap. While low-income households experienced income declines, upper-income households remained relatively stable. The share of aggregate U.S. household income held by upper-income families reached 50% in 2020, up from 46% in 2010, while the share held by lower-income families decreased from 9% to 8%. This disparity underscores the uneven impact of the pandemic, exacerbating existing inequalities. The long-term consequences of this widening gap could include reduced social mobility and increased economic stratification.

5. How Did COVID-19 Impact Access to Healthcare for Low-Income Families?

Access to healthcare became more challenging for low-income families. Many individuals lost their health insurance coverage when they lost their jobs, making it difficult to afford medical care. The pandemic also strained healthcare systems, leading to delays in appointments and limited availability of services. The fear of contracting the virus further deterred some families from seeking medical attention. The lack of healthcare access worsened existing health disparities and could have long-term health consequences.

6. What Strategies Can Low-Income Families Use to Improve Their Financial Situation Post-Pandemic?

Low-income families can employ various strategies to improve their financial situation. These include seeking job training and education to enhance employment prospects, creating a budget to manage expenses, and exploring opportunities for additional income through side hustles or part-time work. Resources available at income-partners.net can provide valuable insights into these strategies. Additionally, connecting with local community organizations and support services can offer assistance with housing, food, and other essential needs.

7. How Can Partnerships Help Low-Income Families Achieve Financial Stability?

Partnerships can play a crucial role in helping low-income families achieve financial stability. Collaborations with businesses, non-profit organizations, and community groups can provide access to resources, job opportunities, and financial education. For example, businesses can offer internships or apprenticeships to provide on-the-job training, while non-profits can provide financial counseling and assistance programs. Income-partners.net serves as a platform for connecting individuals and organizations interested in forming partnerships for economic empowerment.

8. What Types of Partnerships are Most Beneficial for Low-Income Communities?

Several types of partnerships can be particularly beneficial. These include:

- Job Creation Partnerships: Collaborations between businesses and workforce development programs to create job opportunities for low-income individuals.

- Financial Literacy Partnerships: Programs that provide financial education and counseling services to help families manage their finances and build assets.

- Community Development Partnerships: Initiatives that focus on revitalizing low-income neighborhoods through affordable housing, infrastructure improvements, and community services.

- Educational Partnerships: Programs that provide access to quality education and job training to improve long-term employment prospects.

9. How Can Income-Partners.net Facilitate Meaningful Connections for Income Growth?

Income-partners.net facilitates meaningful connections by providing a platform where individuals and organizations can connect, share resources, and collaborate on projects. The website offers resources on various types of partnerships, strategies for building effective relationships, and opportunities for collaboration. By leveraging the platform, low-income families can access the support and resources they need to improve their financial situations and achieve long-term stability. The platform also promotes the sharing of success stories and best practices to inspire and inform its users.

10. What Long-Term Solutions Can Address the Financial Vulnerabilities of Low-Income Families?

Addressing the financial vulnerabilities of low-income families requires a multi-faceted approach. This includes:

- Investing in Education: Providing access to quality education and job training to improve long-term employment prospects.

- Increasing Affordable Housing: Expanding the availability of affordable housing options to reduce housing costs and improve financial stability.

- Expanding Access to Healthcare: Ensuring that all families have access to affordable healthcare services.

- Strengthening Social Safety Nets: Enhancing government assistance programs to provide a safety net for those in need.

- Promoting Economic Opportunity: Creating policies and programs that promote economic growth and opportunity for all.

By implementing these long-term solutions, societies can create a more equitable and prosperous future for all families.

1. Understanding the Economic Shockwaves: How Did COVID-19 Impact Low-Income Families?

The COVID-19 pandemic delivered a significant blow to the financial stability of low-income families. These households often operate with minimal financial cushions, making them exceedingly vulnerable to economic downturns. The pandemic triggered widespread job losses, particularly in sectors heavily reliant on in-person interactions, such as hospitality, retail, and food service. A Pew Research Center study indicated that lower-income households experienced a median income decrease of 3.0% between 2019 and 2020, a stark contrast to the experiences of higher-income brackets.

This economic contraction led to a chain reaction of financial hardships. Families struggled to afford essential needs such as housing, food, and healthcare. Eviction moratoriums provided temporary relief, but the accumulation of unpaid rent left many families facing an uncertain future. Food banks saw unprecedented demand, highlighting the growing food insecurity among low-income communities. Moreover, the shift to remote learning placed additional strain on families, who often lacked the necessary technology and resources to support their children’s education.

Chart showing about three-in-ten lower-income adults had an unemployment spell in 2020

Chart showing about three-in-ten lower-income adults had an unemployment spell in 2020

The pandemic also exacerbated existing inequalities. Low-income families, disproportionately composed of minority groups, faced compounded challenges due to systemic racism and discrimination. The digital divide further widened the gap, as access to online resources and remote work opportunities remained limited for many low-income households. The long-term consequences of these economic shockwaves may include increased poverty rates, reduced social mobility, and lasting health disparities.

1.1. Job Losses and Reduced Work Hours

One of the primary ways COVID-19 affected low-income families was through widespread job losses and reduced work hours. Many low-income individuals work in industries that were heavily impacted by the pandemic, such as hospitality, retail, and food service. These sectors experienced closures and reduced demand due to lockdowns and social distancing measures.

According to the Bureau of Labor Statistics, the unemployment rate for workers in the leisure and hospitality sector reached a staggering 39.3% in April 2020. This job loss disproportionately affected low-income families, who often rely on these jobs for their livelihoods. Even for those who retained their employment, many experienced reduced work hours, leading to decreased earnings and financial instability.

1.2. Increased Food Insecurity

The pandemic exacerbated food insecurity among low-income families. With job losses and reduced incomes, many families struggled to afford enough food to meet their basic needs. Food banks and other charitable organizations saw a significant increase in demand for their services.

Feeding America, a national network of food banks, reported a 60% increase in food bank visits in 2020 compared to the previous year. Many families who had never relied on food assistance before found themselves turning to these resources for the first time. The increased demand put a strain on food banks, which struggled to keep up with the growing need.

1.3. Housing Instability

Housing instability was another significant challenge faced by low-income families during the pandemic. With job losses and reduced incomes, many families struggled to pay their rent or mortgage. Eviction moratoriums provided temporary relief, but the accumulation of unpaid rent left many families facing an uncertain future.

The National Equity Atlas reported that as of January 2021, over 11 million renters were behind on their rent, owing a total of $57.3 billion. The expiration of eviction moratoriums threatened to displace millions of families, leading to increased homelessness and instability.

2. Government Response: Evaluating the Effectiveness of Aid Programs

In response to the economic crisis, the U.S. government implemented several aid programs aimed at supporting individuals and families. Key initiatives included expanded unemployment benefits, stimulus checks, and rental assistance programs. While these programs provided much-needed relief, their effectiveness in addressing the specific challenges faced by low-income families has been a subject of debate.

Unemployment benefits were expanded to include gig workers and self-employed individuals, providing a crucial safety net for those who lost income due to the pandemic. Stimulus checks offered direct financial assistance to households, helping them to cover immediate expenses. Rental assistance programs aimed to prevent evictions and provide landlords with compensation for unpaid rent.

However, the implementation of these programs faced several challenges. Delays in processing unemployment claims left many families waiting weeks or months for assistance. Stimulus checks were often insufficient to cover the ongoing expenses of low-income households. Rental assistance programs were plagued by bureaucratic hurdles, making it difficult for both tenants and landlords to access the funds.

Moreover, some argue that these aid programs were too broad and did not adequately target the specific needs of low-income families. For example, stimulus checks were distributed to households regardless of income level, meaning that some high-income individuals received assistance that could have been better directed to those in greater need.

2.1. Unemployment Benefits

Unemployment benefits were expanded during the pandemic to include gig workers and self-employed individuals, providing a crucial safety net for those who lost income. The CARES Act, passed in March 2020, created the Pandemic Unemployment Assistance (PUA) program, which extended unemployment benefits to those who were not traditionally eligible.

However, the implementation of the PUA program faced several challenges. Many individuals experienced delays in processing their claims, leaving them without income for weeks or months. The complexity of the application process also posed a barrier for some, particularly those with limited English proficiency or technical skills.

2.2. Stimulus Checks

Stimulus checks offered direct financial assistance to households, helping them to cover immediate expenses. The CARES Act authorized the first round of stimulus checks, providing up to $1,200 per adult and $500 per child. Subsequent stimulus packages provided additional rounds of payments.

While stimulus checks provided much-needed relief, some argue that they were insufficient to address the ongoing financial challenges faced by low-income families. The payments were often used to cover essential expenses such as rent, food, and utilities, leaving little room for savings or investment.

2.3. Rental Assistance Programs

Rental assistance programs aimed to prevent evictions and provide landlords with compensation for unpaid rent. The Emergency Rental Assistance (ERA) program, established by the Consolidated Appropriations Act of 2021, provided billions of dollars in funding to state and local governments to distribute to eligible households.

However, the implementation of the ERA program faced significant challenges. Many programs were plagued by bureaucratic hurdles, making it difficult for both tenants and landlords to access the funds. Delays in processing applications left many families facing eviction despite being eligible for assistance.

3. Adapting and Overcoming: Strategies for Financial Resilience

Despite the challenges posed by the pandemic, low-income families have demonstrated remarkable resilience and resourcefulness. Many have adapted by seeking new employment opportunities, leveraging community resources, and developing creative strategies for managing their finances.

One common strategy has been to seek employment in essential sectors that experienced increased demand during the pandemic, such as grocery stores, delivery services, and healthcare. Others have pursued online work opportunities, leveraging their skills and talents to earn income remotely.

Community resources, such as food banks, free clinics, and social service agencies, have played a vital role in supporting low-income families. These organizations provide essential services such as food assistance, healthcare, and financial counseling.

Creative strategies for managing finances have also been essential. Many families have reduced their expenses by cutting back on non-essential items, negotiating with creditors, and seeking assistance with utility bills. Others have leveraged their networks to share resources and support each other.

3.1. Seeking New Employment Opportunities

Many low-income individuals have adapted by seeking new employment opportunities in sectors that experienced increased demand during the pandemic. Grocery stores, delivery services, and healthcare providers all saw a surge in demand for workers.

Some individuals have also pursued online work opportunities, leveraging their skills and talents to earn income remotely. Freelance platforms such as Upwork and Fiverr offer a variety of online jobs, ranging from writing and editing to graphic design and web development.

3.2. Leveraging Community Resources

Community resources have played a vital role in supporting low-income families during the pandemic. Food banks, free clinics, and social service agencies provide essential services such as food assistance, healthcare, and financial counseling.

Organizations such as the United Way and the Salvation Army offer a variety of programs and services to help low-income families meet their basic needs. These programs can provide assistance with housing, food, utilities, and other essential expenses.

3.3. Creative Financial Management

Creative strategies for managing finances have been essential for low-income families during the pandemic. Many families have reduced their expenses by cutting back on non-essential items, negotiating with creditors, and seeking assistance with utility bills.

Others have leveraged their networks to share resources and support each other. Sharing childcare responsibilities, carpooling, and pooling resources for groceries are all examples of how families can work together to reduce their expenses.

4. The Rise of Income Partnerships: A Collaborative Approach to Economic Empowerment

In the wake of the pandemic, a growing number of individuals and organizations are recognizing the potential of income partnerships as a means of promoting economic empowerment. Income partnerships involve collaborative relationships between individuals, businesses, and non-profit organizations, with the goal of creating economic opportunities and increasing financial stability for low-income families.

One example of an income partnership is a collaboration between a local business and a workforce development program. The business provides on-the-job training and employment opportunities for low-income individuals, while the workforce development program provides support services such as job coaching and financial counseling.

Another example is a partnership between a non-profit organization and a financial institution. The non-profit organization provides financial education and counseling services to low-income families, while the financial institution offers affordable financial products and services.

Income-partners.net serves as a platform for connecting individuals and organizations interested in forming income partnerships. The website provides resources on various types of partnerships, strategies for building effective relationships, and opportunities for collaboration.

4.1. Benefits of Income Partnerships

Income partnerships offer a variety of benefits for low-income families. These partnerships can provide access to job opportunities, financial education, and affordable financial products and services.

By working together, individuals, businesses, and non-profit organizations can create a more supportive and equitable economic environment for low-income families. Income partnerships can also help to build stronger communities and promote economic growth.

4.2. Types of Income Partnerships

There are many different types of income partnerships, each with its own unique focus and goals. Some common types of income partnerships include:

- Job Creation Partnerships: Collaborations between businesses and workforce development programs to create job opportunities for low-income individuals.

- Financial Literacy Partnerships: Programs that provide financial education and counseling services to help families manage their finances and build assets.

- Community Development Partnerships: Initiatives that focus on revitalizing low-income neighborhoods through affordable housing, infrastructure improvements, and community services.

- Educational Partnerships: Programs that provide access to quality education and job training to improve long-term employment prospects.

4.3. Building Successful Income Partnerships

Building successful income partnerships requires a commitment to collaboration, communication, and shared goals. It is essential to establish clear roles and responsibilities, develop a strong communication plan, and regularly evaluate the partnership’s progress.

It is also important to build trust and respect among partners. This can be achieved by fostering open communication, valuing diverse perspectives, and celebrating successes.

5. Income-Partners.net: Your Gateway to Collaborative Success

Income-partners.net is your go-to resource for exploring and establishing income partnerships that can uplift low-income families. Our platform offers a wealth of information, tools, and connections to help you navigate the world of collaborative economic empowerment.

Whether you’re an individual seeking new opportunities, a business looking to make a social impact, or a non-profit organization seeking to expand your reach, Income-partners.net can help you find the right partners and resources to achieve your goals.

Our website features a comprehensive directory of income partnership opportunities, as well as resources on building effective partnerships, developing successful programs, and measuring your impact. We also offer a community forum where you can connect with other individuals and organizations, share ideas, and ask questions.

5.1. Exploring Partnership Opportunities

Income-partners.net offers a comprehensive directory of income partnership opportunities. You can search for opportunities by location, industry, and type of partnership.

Our directory includes a variety of opportunities, ranging from job creation programs to financial literacy initiatives to community development projects. We also feature partnerships that focus on specific populations, such as veterans, people with disabilities, and formerly incarcerated individuals.

5.2. Building Effective Partnerships

Income-partners.net provides resources on building effective partnerships. Our website offers guidance on establishing clear roles and responsibilities, developing a strong communication plan, and regularly evaluating the partnership’s progress.

We also offer tips on building trust and respect among partners. This can be achieved by fostering open communication, valuing diverse perspectives, and celebrating successes.

5.3. Measuring Your Impact

Income-partners.net provides resources on measuring your impact. Our website offers guidance on developing metrics to track the progress of your partnership and evaluating its effectiveness.

We also offer tools to help you collect and analyze data, as well as resources on reporting your results to stakeholders. By measuring your impact, you can demonstrate the value of your partnership and attract additional funding and support.

6. Case Studies: Success Stories of Income Partnerships

Numerous successful income partnerships have demonstrated the transformative potential of collaboration in addressing the financial challenges faced by low-income families. These case studies offer valuable insights and inspiration for those seeking to create similar partnerships in their own communities.

One example is the partnership between Goodwill Industries and a local hospital. Goodwill provides job training and employment opportunities for low-income individuals, while the hospital offers entry-level positions in areas such as food service, housekeeping, and patient transport. This partnership has not only provided individuals with stable employment but has also helped the hospital to fill critical staffing needs.

Another example is the partnership between a community development financial institution (CDFI) and a local non-profit organization. The CDFI provides access to affordable loans and financial services for low-income entrepreneurs, while the non-profit organization offers business training and technical assistance. This partnership has helped to create new businesses and jobs in low-income communities.

These case studies demonstrate the power of collaboration in creating economic opportunities and improving the financial stability of low-income families. By learning from these success stories, individuals and organizations can develop innovative partnerships that address the specific needs of their communities.

6.1. Goodwill Industries and Local Hospital Partnership

Goodwill Industries partnered with a local hospital to provide job training and employment opportunities for low-income individuals. Goodwill provides training in areas such as customer service, computer skills, and healthcare basics.

The hospital offers entry-level positions in areas such as food service, housekeeping, and patient transport. This partnership has provided individuals with stable employment and helped the hospital to fill critical staffing needs.

6.2. CDFI and Non-Profit Organization Partnership

A community development financial institution (CDFI) partnered with a local non-profit organization to provide access to affordable loans and financial services for low-income entrepreneurs. The CDFI offers microloans and small business loans at below-market interest rates.

The non-profit organization provides business training and technical assistance, helping entrepreneurs to develop business plans, secure funding, and manage their finances. This partnership has helped to create new businesses and jobs in low-income communities.

6.3. Local Business and Workforce Development Program Partnership

A local business partnered with a workforce development program to provide on-the-job training and employment opportunities for low-income individuals. The business offers apprenticeships and internships in areas such as manufacturing, construction, and technology.

The workforce development program provides support services such as job coaching, resume writing, and interview skills training. This partnership has helped individuals gain valuable skills and experience, leading to long-term employment.

7. Navigating the Future: Long-Term Strategies for Economic Equity

Addressing the financial vulnerabilities of low-income families requires a long-term commitment to economic equity. This includes investing in education, expanding access to affordable housing, strengthening social safety nets, and promoting policies that create economic opportunities for all.

Investing in education is crucial for improving the long-term employment prospects of low-income individuals. This includes providing access to quality early childhood education, K-12 education, and higher education.

Expanding access to affordable housing is essential for reducing housing costs and improving financial stability. This includes increasing the supply of affordable housing units, providing rental assistance, and promoting policies that prevent discrimination in housing.

Strengthening social safety nets is necessary for providing a safety net for those in need. This includes expanding access to unemployment benefits, food assistance, and healthcare.

Promoting policies that create economic opportunities for all is crucial for creating a more equitable economic environment. This includes raising the minimum wage, promoting fair labor practices, and investing in infrastructure and job creation.

7.1. Investing in Education

Investing in education is crucial for improving the long-term employment prospects of low-income individuals. This includes providing access to quality early childhood education, K-12 education, and higher education.

Early childhood education programs such as Head Start can help to prepare low-income children for success in school. K-12 education reforms such as smaller class sizes, more funding for schools in low-income communities, and higher teacher salaries can improve the quality of education for all students.

Access to higher education is also essential for improving long-term employment prospects. Pell Grants and other financial aid programs can help to make college more affordable for low-income students.

7.2. Expanding Access to Affordable Housing

Expanding access to affordable housing is essential for reducing housing costs and improving financial stability. This includes increasing the supply of affordable housing units, providing rental assistance, and promoting policies that prevent discrimination in housing.

Increasing the supply of affordable housing units can be achieved through policies such as inclusionary zoning, density bonuses, and tax credits for developers who build affordable housing. Rental assistance programs such as Section 8 can help low-income families afford decent housing.

Policies that prevent discrimination in housing can help to ensure that all families have equal access to housing opportunities. These policies can prohibit discrimination based on race, ethnicity, religion, national origin, disability, and family status.

7.3. Strengthening Social Safety Nets

Strengthening social safety nets is necessary for providing a safety net for those in need. This includes expanding access to unemployment benefits, food assistance, and healthcare.

Unemployment benefits can provide income support for workers who lose their jobs. Food assistance programs such as SNAP can help low-income families afford enough food to meet their basic needs.

Healthcare programs such as Medicaid can provide access to affordable healthcare services for low-income individuals and families.

8. FAQs: Addressing Common Concerns About COVID-19 and Low-Income Families

Q1: How can I help low-income families in my community who are struggling due to COVID-19?

A1: You can help by donating to local food banks, volunteering at community organizations, and supporting businesses that employ low-income workers.

Q2: What resources are available for low-income families who are facing eviction?

A2: Contact your local housing authority, legal aid society, or non-profit organization for assistance with rental assistance programs and legal representation.

Q3: How can I improve my financial literacy and manage my finances more effectively?

A3: Take advantage of free financial education resources offered by non-profit organizations, community colleges, and online platforms.

Q4: What are some strategies for finding affordable healthcare options?

A4: Explore Medicaid, CHIP, and community health centers for low-cost or free healthcare services.

Q5: How can I connect with potential income partners in my community?

A5: Use Income-partners.net to connect with individuals and organizations interested in forming collaborative partnerships.

Q6: What types of job training programs are available for low-income individuals?

A6: Contact your local workforce development board or community college for information on job training programs in your area.

Q7: How can I start a business in a low-income community?

A7: Seek assistance from community development financial institutions (CDFIs) and small business development centers (SBDCs) for access to capital and business training.

Q8: What are some policies that can help to reduce income inequality?

A8: Support policies such as raising the minimum wage, expanding access to affordable housing, and investing in education and job training.

Q9: How can I advocate for policies that support low-income families?

A9: Contact your elected officials, participate in community advocacy groups, and support organizations that advocate for economic justice.

Q10: What is the long-term impact of COVID-19 on low-income families?

A10: The long-term impact may include increased poverty rates, reduced social mobility, and lasting health disparities. It is crucial to implement long-term strategies to address these challenges and promote economic equity.

9. Conclusion: Partnering for a Brighter Future

The COVID-19 pandemic has underscored the vulnerability of low-income families and the urgent need for collaborative solutions. Income partnerships offer a promising approach to economic empowerment, providing access to resources, opportunities, and support that can transform lives. By connecting individuals, businesses, and non-profit organizations, we can create a more equitable and prosperous future for all.

Income-partners.net is committed to facilitating these connections and providing the resources you need to succeed. Explore our website today to discover partnership opportunities, build effective relationships, and make a lasting impact on the lives of low-income families. Together, we can build a brighter future for all members of our communities. Don’t wait, visit income-partners.net today and start your journey towards collaborative success in the heart of the USA, including bustling hubs like Austin, Texas. Your next partnership opportunity awaits. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.

[