The corporate income tax significantly impacts how businesses structure their finances and growth strategies, making it essential to understand. At income-partners.net, we provide the insights and tools necessary for businesses to navigate these complexities and discover partnership opportunities that can enhance profitability. By exploring effective tax strategies and collaboration opportunities, businesses can optimize their financial performance.

1. Understanding the Basics of Corporate Income Tax (CIT)

The corporate income tax (CIT) is a tax levied by both the federal and state governments on the profits of C corporations. Essentially, the CIT taxes the earnings that a corporation makes from its business activities during a specific tax year. This tax is a significant source of revenue for governments, funding public services and infrastructure.

1.1. Who Pays the Corporate Income Tax?

Only C corporations are subject to the corporate income tax. This is because other business structures, like S corporations, partnerships, and sole proprietorships, are considered pass-through entities.

1.2. What are Pass-Through Entities?

Pass-through entities don’t pay corporate income tax directly. Instead, the profits from these businesses are “passed through” to the owners, who then report the income on their individual income tax returns. This means that the business profits are taxed at the individual income tax rate rather than the corporate tax rate. According to research from the University of Texas at Austin’s McCombs School of Business, pass-through businesses account for over 95% of all businesses in the U.S, demonstrating their popularity and impact on the economy.

1.3. How is Corporate Income Tax Calculated?

Corporate income tax is calculated by applying the applicable tax rate to a corporation’s taxable income. Taxable income is calculated as the corporation’s total revenue minus allowable deductions. Deductions can include business expenses, cost of goods sold, and depreciation expenses.

2. Current Corporate Tax Rate in the U.S.

The corporate tax rate is a crucial factor for businesses when estimating their tax liabilities and making financial decisions. The federal corporate tax rate is currently set at 21%.

2.1. Historical Context of the Corporate Tax Rate

Before the Tax Cuts and Jobs Act (TCJA) of 2017, the federal corporate tax rate was 35%, among the highest in the world. The TCJA significantly reduced the rate to 21%, aiming to make U.S. businesses more competitive globally. This change has had a far-reaching impact on corporate profitability and investment decisions.

2.2. State Corporate Income Tax Rates

In addition to the federal corporate income tax, many states also impose a corporate income tax. The state corporate income tax rates vary significantly, ranging from 0% to over 10%. It is important for businesses to consider both federal and state tax rates when determining their overall tax burden. According to the Tax Foundation, states like Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming do not levy a corporate income tax, which can be a significant advantage for businesses operating within those states.

2.3. Combined Federal and State Corporate Income Tax Rate

The combined federal and state corporate income tax rate is the sum of the federal rate and the state rate. As of 2024, the combined rate averages around 25.8%. However, this can vary depending on the state in which the business operates.

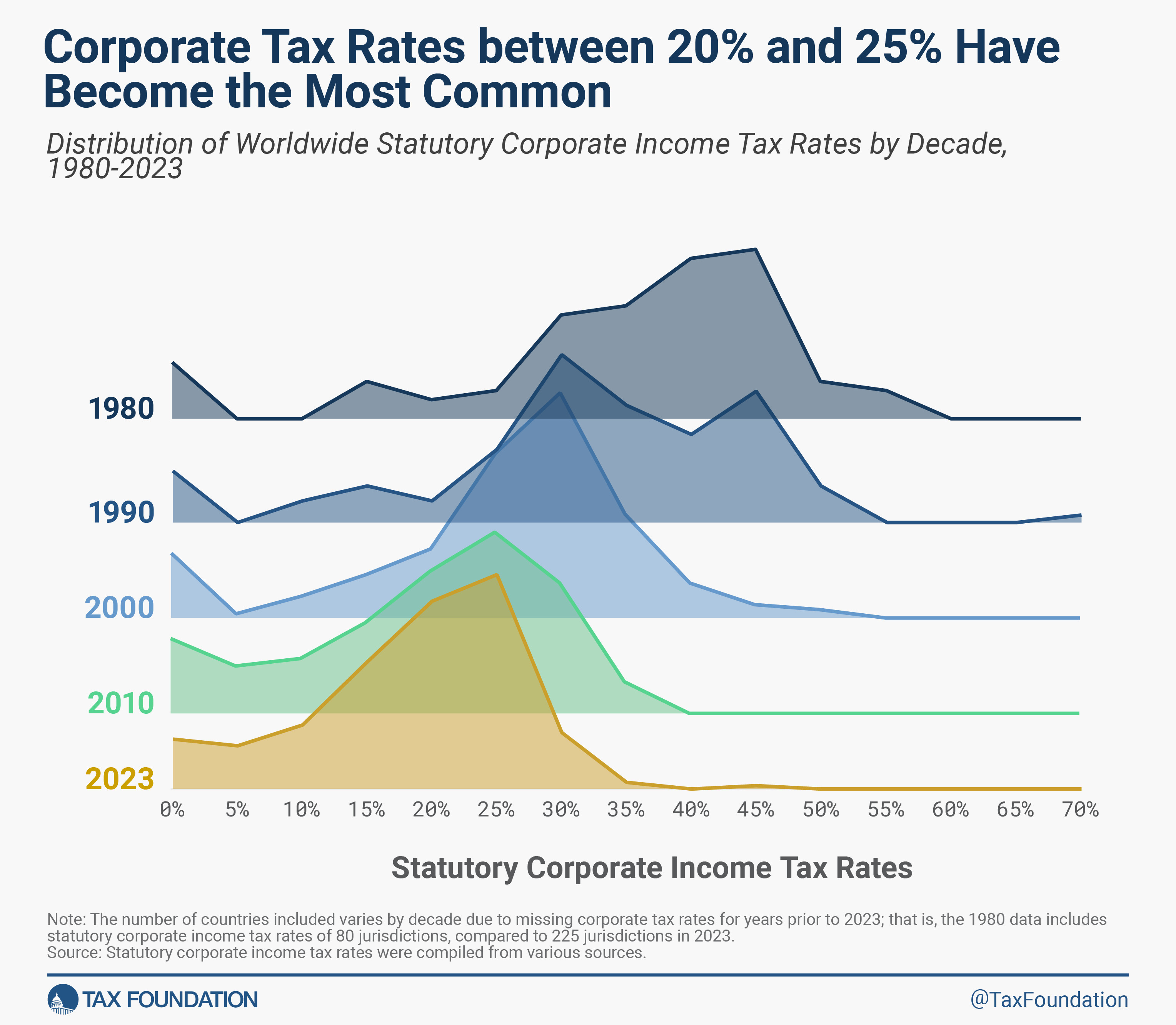

Combined State and Federal Corporate Income Tax Rates

Combined State and Federal Corporate Income Tax Rates

3. Understanding the Corporate Tax Base

The corporate tax base refers to the total amount of income that a corporation is subject to tax on. It is calculated by subtracting allowable deductions from a corporation’s gross income.

3.1. What is Included in Gross Income?

Gross income includes all revenues that a corporation receives from its business activities, such as sales, services, and investments. It also includes any other income that the corporation receives, such as interest, dividends, and royalties.

3.2. What are Allowable Deductions?

Allowable deductions are expenses that a corporation can subtract from its gross income to reduce its taxable income. These deductions can include:

- Business Expenses: Expenses incurred in the ordinary course of business, such as salaries, rent, utilities, and advertising costs.

- Cost of Goods Sold (COGS): The direct costs associated with producing goods or services, including raw materials, labor, and manufacturing overhead.

- Depreciation Expenses: The gradual reduction in the value of an asset over its useful life. This allows businesses to deduct a portion of the asset’s cost each year.

- Interest Expenses: The cost of borrowing money, which can be deducted from taxable income.

3.3. Impact of Capital Investments on Taxable Income

Capital investments, such as the purchase of equipment, machinery, and buildings, cannot be fully deducted in the year they are incurred. Instead, these costs must be deducted over an extended period of time through depreciation. This can inflate a business’s taxable income in the short term, increasing the cost of capital.

3.4. Net Operating Losses (NOLs)

A net operating loss (NOL) occurs when a corporation’s deductions exceed its gross income. Businesses can use NOLs to reduce their tax liability in other years through carryforwards and carrybacks. According to the IRS, a net operating loss (NOL) arises when a company’s allowable deductions surpass its gross income, presenting both challenges and opportunities in tax planning.

3.5. Carryforwards and Carrybacks

Carryforwards allow businesses to use NOLs to offset taxable income in future years. Carrybacks allow businesses to use NOLs to offset taxable income in prior years, potentially resulting in a refund of previously paid taxes.

3.6. Inventory Valuation Methods

The method used to value inventory can significantly impact a business’s taxable income. Common inventory valuation methods include:

- First-In, First-Out (FIFO): Assumes that the first units purchased are the first units sold.

- Last-In, First-Out (LIFO): Assumes that the last units purchased are the first units sold (not permitted under IFRS).

- Weighted-Average Cost: Calculates the average cost of all inventory items and uses this cost to determine the value of goods sold.

Tax basics reducing the corporate income tax rate is an efficient way to grow the economy

Tax basics reducing the corporate income tax rate is an efficient way to grow the economy

4. Who Ultimately Bears the Burden of Corporate Income Tax?

While C corporations are legally responsible for paying the corporate income tax, the economic burden of the tax is often shared among various stakeholders. According to research from Harvard Business Review, the ultimate burden of corporate income tax is distributed among shareholders, employees, and consumers.

4.1. Impact on Shareholders

Shareholders bear a portion of the corporate income tax burden through reduced profits and lower stock values. When a corporation pays taxes, it has less money available to distribute as dividends or reinvest in the business, which can negatively impact shareholder returns.

4.2. Impact on Employees

Employees may also bear a portion of the corporate income tax burden through lower wages and reduced benefits. Companies may reduce labor costs to offset the cost of paying taxes, which can affect employee compensation.

4.3. Impact on Consumers

Consumers may bear a portion of the corporate income tax burden through higher prices for goods and services. Companies may pass on the cost of paying taxes to consumers in the form of increased prices.

5. What are the Intentions to explore the “how does the corporate income tax work?”

There are several intentions when researching “How Does The Corporate Income Tax Work”.

- Understanding the Basics: Users want to know the fundamental principles of corporate income tax, including who pays it and how it is calculated.

- Tax Planning: Businesses and financial professionals seek to understand how the corporate income tax works to develop effective tax planning strategies.

- Compliance: Companies need to understand the rules and regulations of the corporate income tax to ensure they are in compliance with the law.

- Investment Decisions: Investors want to understand the impact of corporate income tax on company profitability and investment returns.

- Policy Analysis: Economists and policymakers analyze the effects of corporate income tax on the economy and develop policy recommendations.

6. Strategic Partnerships to Mitigate Corporate Income Tax

Strategic partnerships can play a pivotal role in mitigating the impact of corporate income tax, offering innovative avenues to optimize tax liabilities and enhance overall financial health. Income-partners.net provides insights into these strategies, helping businesses connect with partners who can offer expertise and resources to navigate tax complexities.

6.1. Joint Ventures for Research and Development (R&D)

Collaborating on R&D projects through joint ventures can lead to significant tax benefits. Many jurisdictions offer tax incentives for companies investing in R&D, such as tax credits or deductions for qualifying expenses. By partnering with other companies, businesses can pool resources and share the costs of R&D, maximizing their eligibility for these incentives.

- Tax Credits for R&D: Numerous countries offer tax credits to encourage companies to invest in research and development activities.

- Expense Deductions: Partnering on R&D can enable businesses to deduct a larger portion of their expenses.

- Resource Pooling: Joint ventures allow companies to pool financial and intellectual resources, making R&D projects more viable and cost-effective.

6.2. Utilizing Special Economic Zones (SEZs)

Operating within Special Economic Zones (SEZs) can offer substantial tax advantages. SEZs are designated areas within a country that have more liberal economic regulations than other regions. These zones often provide tax holidays, reduced tax rates, and exemptions from certain taxes. Forming partnerships with companies already operating in SEZs can provide access to these benefits.

- Tax Holidays: SEZs often offer tax holidays, where businesses are exempt from income tax for a specified period.

- Reduced Tax Rates: Corporate tax rates within SEZs are typically lower than the national average.

- Customs and VAT Exemptions: SEZs may offer exemptions from customs duties and value-added tax (VAT) on goods imported and exported from the zone.

6.3. International Tax Planning through Partnerships

International partnerships can facilitate effective tax planning by leveraging different tax jurisdictions and treaties. By forming strategic alliances with companies in countries with lower tax rates or favorable tax treaties, businesses can reduce their overall tax burden. It’s essential to consult with tax advisors to ensure compliance with international tax laws and regulations.

- Transfer Pricing Optimization: International partnerships can help optimize transfer pricing strategies, ensuring that profits are allocated to entities in lower-tax jurisdictions.

- Tax Treaty Benefits: Leveraging tax treaties between countries can reduce withholding taxes and other cross-border tax obligations.

- Offshore Investments: Partnering with companies in tax-efficient jurisdictions can facilitate offshore investments, which may offer tax advantages.

6.4. Mergers and Acquisitions (M&A) Tax Strategies

Mergers and acquisitions can be structured to optimize tax outcomes. Depending on the specific circumstances, M&A transactions can provide opportunities to reduce taxable income, utilize net operating losses, and access other tax benefits. Partnering with companies that have complementary tax attributes can enhance the value of M&A deals.

- Step-Up in Basis: M&A transactions can allow for a step-up in the tax basis of assets, increasing depreciation deductions and reducing future taxable gains.

- Net Operating Loss Utilization: Acquiring companies with net operating losses can provide an opportunity to offset future taxable income.

- Tax-Free Reorganizations: Structuring M&A transactions as tax-free reorganizations can defer or eliminate capital gains taxes.

6.5. Supply Chain Optimization through Partnerships

Collaborating with partners to optimize the supply chain can lead to tax efficiencies. By strategically locating manufacturing, distribution, and other supply chain activities in tax-advantaged locations, businesses can reduce their overall tax burden. Partnerships can also facilitate access to local expertise and resources.

- Location Incentives: Many jurisdictions offer tax incentives to attract businesses to locate their operations in specific areas.

- Logistics and Distribution Efficiencies: Optimizing the supply chain can reduce transportation costs and other expenses, leading to lower taxable income.

- Reduced Customs Duties: Partnering with companies in free trade zones can reduce or eliminate customs duties on imported goods.

6.6. Tax-Efficient Financing Structures

Partnerships can facilitate access to tax-efficient financing structures, such as hybrid instruments or cross-border lending arrangements. These structures can help reduce interest expenses and other financing costs, lowering taxable income. It’s important to ensure that these structures comply with applicable tax laws and regulations.

- Hybrid Instruments: Hybrid instruments, such as convertible bonds or preferred stock, can offer tax advantages by combining features of debt and equity.

- Cross-Border Lending: Structuring cross-border lending arrangements can reduce withholding taxes and other tax obligations.

- Interest Deductions: Partnering with companies in lower-tax jurisdictions can increase the deductibility of interest expenses.

6.7. Real Estate Investment Trusts (REITs) Collaborations

Partnering with Real Estate Investment Trusts (REITs) can offer tax benefits for real estate investments. REITs are companies that own or finance income-producing real estate. They are typically required to distribute a significant portion of their income to shareholders, which can provide tax advantages for investors.

- Pass-Through Taxation: REITs are generally subject to pass-through taxation, meaning that their income is taxed at the shareholder level rather than the corporate level.

- Dividend Deductions: REITs can deduct dividends paid to shareholders, reducing their taxable income.

- Real Estate Tax Benefits: Partnering with REITs can provide access to real estate tax benefits, such as depreciation deductions and property tax abatements.

6.8. Technology and Intellectual Property (IP) Sharing

Collaborating on technology and intellectual property (IP) can provide tax benefits, particularly in jurisdictions with favorable IP regimes. By forming partnerships to develop, commercialize, or license technology and IP, businesses can optimize their tax liabilities.

- IP Box Regimes: Many countries offer preferential tax treatment for income derived from patents and other intellectual property.

- R&D Tax Credits: Partnering on technology development can increase eligibility for R&D tax credits.

- Transfer Pricing for IP: Structuring transfer pricing arrangements for IP can optimize the allocation of profits to lower-tax jurisdictions.

6.9. Green Initiatives and Sustainability Projects

Engaging in green initiatives and sustainability projects can provide tax incentives, as many governments offer tax credits, deductions, and grants to encourage environmentally friendly activities. Partnering with companies that specialize in green technologies or sustainability practices can help businesses access these benefits.

- Renewable Energy Tax Credits: Numerous jurisdictions offer tax credits for investments in renewable energy projects, such as solar, wind, and hydro power.

- Energy Efficiency Deductions: Partnering on energy efficiency projects can provide deductions for the costs of upgrading buildings and equipment.

- Carbon Credits: Engaging in carbon offset projects can generate carbon credits, which can be sold or used to reduce a company’s carbon tax liabilities.

6.10. Community Development Partnerships

Collaborating on community development projects can provide tax benefits through incentives like the New Markets Tax Credit (NMTC) program in the United States. These partnerships can support economic development in low-income communities while also providing tax advantages for investors.

- New Markets Tax Credits: The NMTC program provides tax credits for investments in businesses and real estate projects located in low-income communities.

- Community Reinvestment Act (CRA): Banks and financial institutions can receive tax benefits for investments that support community development.

- Social Impact Bonds: Partnering on social impact bonds can provide tax incentives for investments that generate positive social and environmental outcomes.

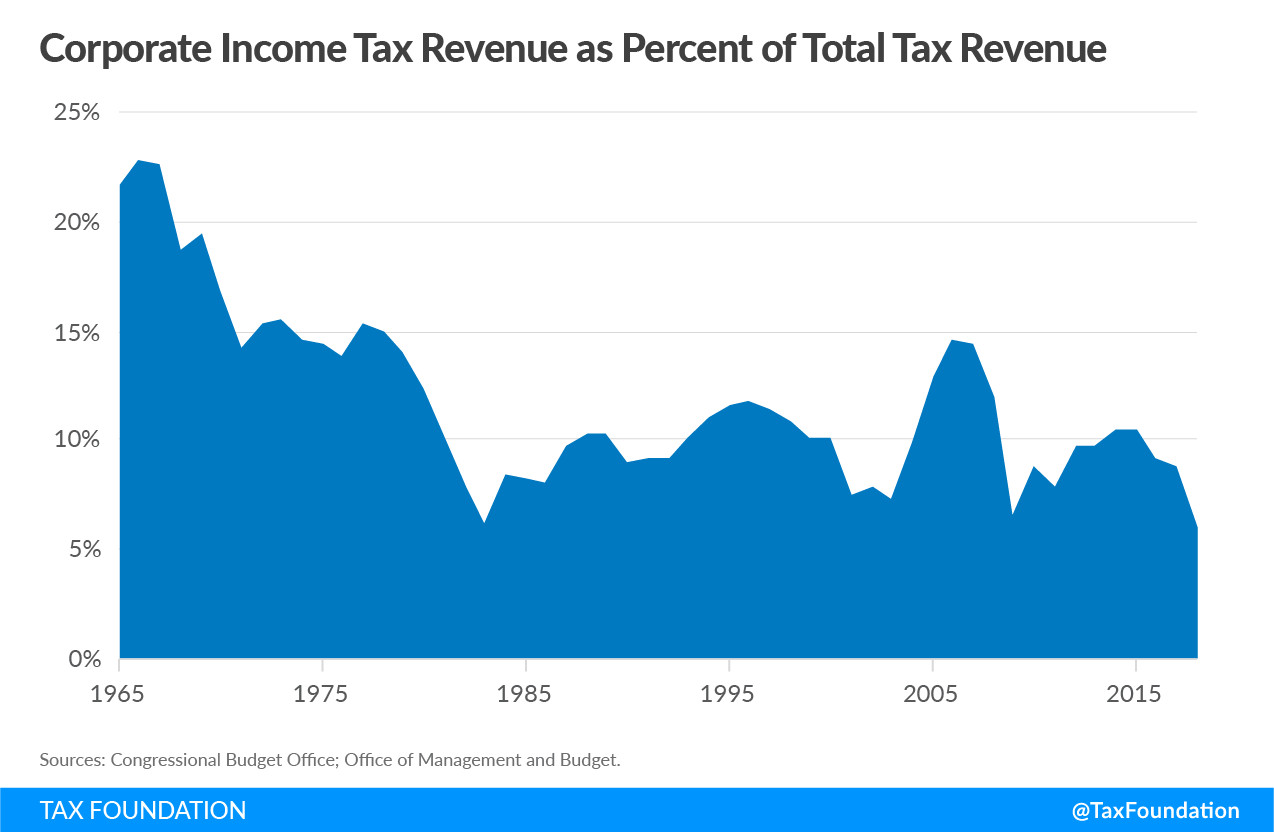

Corporate income tax revenue

Corporate income tax revenue

7. The Role of Income-Partners.Net in Facilitating Strategic Partnerships

Income-partners.net is a platform dedicated to helping businesses find strategic partners to enhance growth, profitability, and tax efficiency. By connecting businesses with complementary expertise and resources, income-partners.net facilitates collaborations that can lead to significant tax benefits.

7.1. Connecting Businesses with Complementary Expertise

Income-partners.net provides a comprehensive directory of businesses across various industries, allowing companies to identify potential partners with complementary expertise. Whether you are looking for a partner with specialized knowledge in R&D, international tax planning, or supply chain optimization, income-partners.net can help you find the right fit.

7.2. Providing Resources and Insights on Tax Planning Strategies

Income-partners.net offers a wealth of resources and insights on tax planning strategies, helping businesses stay informed about the latest tax laws, regulations, and incentives. Our platform provides access to expert articles, webinars, and case studies that can help you develop effective tax planning strategies.

7.3. Facilitating Collaboration and Communication

Income-partners.net provides tools and features that facilitate collaboration and communication between partners. Our platform allows you to easily share documents, exchange messages, and track progress on joint projects.

7.4. Showcasing Success Stories of Strategic Partnerships

Income-partners.net showcases success stories of strategic partnerships that have resulted in significant tax benefits. These case studies provide real-world examples of how businesses have leveraged partnerships to optimize their tax liabilities and enhance their overall financial performance.

7.5. Promoting a Culture of Collaboration and Innovation

Income-partners.net is committed to promoting a culture of collaboration and innovation. Our platform encourages businesses to share their knowledge, insights, and best practices, fostering a community of like-minded professionals who are dedicated to achieving success through strategic partnerships.

8. Latest Trends in Corporate Income Tax

Staying informed about the latest trends in corporate income tax is crucial for businesses to adapt and optimize their tax strategies. Recent developments include changes in tax rates, new regulations, and emerging incentives.

8.1. Global Minimum Tax

One of the most significant trends in corporate income tax is the implementation of a global minimum tax. The OECD (Organisation for Economic Co-operation and Development) has been working on a global tax deal that would set a minimum corporate tax rate of 15% for multinational corporations. This initiative aims to prevent companies from shifting profits to low-tax jurisdictions and ensure that they pay a fair share of taxes.

8.2. Digital Services Tax

Many countries are considering or have already implemented a digital services tax (DST) on the revenue of large digital companies. DSTs typically target companies that provide online advertising, social media platforms, and other digital services. These taxes are designed to capture revenue from digital companies that may not have a physical presence in the country but generate significant revenue from local users.

8.3. Green Tax Incentives

Governments are increasingly offering tax incentives for green initiatives and sustainability projects. These incentives aim to encourage businesses to invest in renewable energy, energy efficiency, and other environmentally friendly activities. Examples include tax credits for solar energy, deductions for energy-efficient equipment, and grants for green building projects.

8.4. Tax Reform in the United States

The United States has seen significant tax reform in recent years, including the Tax Cuts and Jobs Act (TCJA) of 2017. The TCJA reduced the federal corporate tax rate from 35% to 21% and made other changes to the tax code. However, there is ongoing debate about potential future tax reforms, including proposals to increase the corporate tax rate or modify other provisions of the TCJA.

8.5. Increased Tax Enforcement

Tax authorities around the world are increasing their efforts to enforce tax laws and combat tax evasion. This includes increased audits, enhanced data analytics, and greater collaboration between tax authorities. Businesses need to ensure that they are in compliance with all applicable tax laws and regulations to avoid penalties and reputational damage.

9. Navigating Corporate Income Tax: A Step-by-Step Guide

Navigating corporate income tax can be complex, but following a systematic approach can help businesses stay compliant and optimize their tax strategies.

9.1. Step 1: Determine Your Business Structure

The first step in navigating corporate income tax is to determine your business structure. Are you operating as a C corporation, S corporation, partnership, or sole proprietorship? The choice of business structure will impact how your business is taxed.

9.2. Step 2: Calculate Your Gross Income

Calculate your business’s gross income, which includes all revenues from sales, services, and investments. Make sure to keep accurate records of all income sources.

9.3. Step 3: Identify Allowable Deductions

Identify all allowable deductions, such as business expenses, cost of goods sold, depreciation expenses, and interest expenses. Keep detailed records of all expenses and ensure that they meet the requirements for deductibility.

9.4. Step 4: Calculate Your Taxable Income

Calculate your taxable income by subtracting allowable deductions from your gross income. This is the amount of income that will be subject to corporate income tax.

9.5. Step 5: Apply the Applicable Tax Rate

Apply the applicable federal and state corporate income tax rates to your taxable income. Remember that state tax rates vary, so it’s important to know the rate in your state.

9.6. Step 6: File Your Tax Return

File your corporate income tax return with the IRS and your state tax authority. Make sure to file on time to avoid penalties.

9.7. Step 7: Stay Informed and Adapt

Stay informed about the latest tax laws, regulations, and incentives. Adapt your tax strategies as needed to optimize your tax liabilities.

10. Frequently Asked Questions (FAQs) about Corporate Income Tax

10.1. What is the corporate income tax?

The corporate income tax (CIT) is a tax levied by federal and state governments on the profits of C corporations. It’s a tax on the earnings a corporation makes from its business activities during a tax year.

10.2. Who pays the corporate income tax?

Only C corporations pay the corporate income tax. Other business structures, like S corporations, partnerships, and sole proprietorships, are considered pass-through entities and don’t pay CIT directly.

10.3. How is the corporate income tax calculated?

Corporate income tax is calculated by applying the applicable tax rate to a corporation’s taxable income, which is total revenue minus allowable deductions.

10.4. What is the current federal corporate tax rate in the U.S.?

As of 2024, the federal corporate tax rate is 21%.

10.5. Can capital investments be fully deducted in the year they are incurred?

No, capital investments cannot be fully deducted in the year they are incurred. Instead, these costs must be deducted over an extended period of time through depreciation.

10.6. What are net operating losses (NOLs)?

A net operating loss (NOL) occurs when a corporation’s deductions exceed its gross income. Businesses can use NOLs to reduce their tax liability in other years through carryforwards and carrybacks.

10.7. What are carryforwards and carrybacks?

Carryforwards allow businesses to use NOLs to offset taxable income in future years. Carrybacks allow businesses to use NOLs to offset taxable income in prior years, potentially resulting in a refund of previously paid taxes.

10.8. How do strategic partnerships help in mitigating corporate income tax?

Strategic partnerships can provide various tax benefits, such as access to R&D tax credits, incentives for operating in special economic zones, and opportunities for international tax planning.

10.9. What is a global minimum tax?

A global minimum tax is an initiative to set a minimum corporate tax rate for multinational corporations, aiming to prevent companies from shifting profits to low-tax jurisdictions.

10.10. How can income-partners.net help businesses with corporate income tax?

Income-partners.net helps businesses find strategic partners to enhance growth, profitability, and tax efficiency. It provides a platform for connecting with experts, accessing resources on tax planning strategies, and facilitating collaboration.

Understanding how corporate income tax works is essential for businesses to optimize their financial strategies and ensure compliance. By leveraging strategic partnerships and staying informed about the latest trends, businesses can effectively manage their tax liabilities and enhance their overall performance. Explore the opportunities available at income-partners.net to connect with potential collaborators, access valuable insights, and drive your business forward. Visit income-partners.net today to discover how strategic partnerships can transform your approach to corporate income tax and boost your bottom line. For further information or assistance, contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.