Does race affect income? Yes, race significantly impacts income due to historical and ongoing systemic inequities, but income-partners.net offers insights and strategies for overcoming these barriers through strategic partnerships and diverse collaborations. By exploring various partnership models and success stories, income equality can be increased, along with financial empowerment and wealth creation for all.

1. What Systemic Inequities Contribute To Racial Income Disparities?

Systemic inequities like historical discrimination, unequal access to education, and biased hiring practices significantly contribute to racial income disparities. These barriers hinder people of color from achieving economic security, but at income-partners.net you can find resources to help build a path to increased earnings.

Racial income disparities are deeply rooted in historical and ongoing systemic inequities. These inequities manifest in various forms, creating significant barriers for people of color in achieving economic security. Understanding these factors is crucial for addressing and mitigating the disparities.

-

Historical Discrimination: Historical discrimination, including slavery, Jim Crow laws, and redlining, has had a lasting impact on wealth accumulation and economic opportunities for people of color. These practices systematically excluded racial and ethnic minorities from accessing education, employment, and housing, thereby limiting their ability to build wealth and pass it on to future generations.

-

Educational Inequalities: Unequal access to quality education is a significant contributor to income disparities. Schools in predominantly minority communities often lack the resources and funding necessary to provide a competitive education. This disparity can lead to lower academic achievement and limited opportunities for higher education, ultimately affecting career prospects and earning potential.

-

Employment Discrimination: Biased hiring practices and workplace discrimination continue to affect the career advancement and earnings of people of color. Studies have shown that applicants with names that sound “Black” or “Latino” are less likely to receive callbacks for job interviews, even when their qualifications are identical to those of white applicants. Furthermore, once employed, people of color may face barriers to promotion and equal pay for equal work.

-

Housing Segregation: Housing segregation limits access to quality education, employment opportunities, and healthcare services. Redlining, a discriminatory practice that denied loans and services to residents of predominantly minority neighborhoods, has contributed to the concentration of poverty and limited access to resources in these communities. This segregation perpetuates income disparities by restricting access to wealth-building opportunities and essential services.

-

Access to Capital: Limited access to capital and financial services is another significant barrier to economic advancement for people of color. Minority-owned businesses often face challenges in obtaining loans and investments, hindering their ability to grow and create jobs. Additionally, predatory lending practices and lack of financial literacy resources can further exacerbate financial instability and wealth inequality.

-

Criminal Justice System: The disproportionate impact of the criminal justice system on communities of color also contributes to income disparities. High rates of incarceration and involvement in the criminal justice system can lead to job loss, difficulty finding employment, and limited access to education and housing. These factors create a cycle of poverty and disadvantage that perpetuates income inequality.

Systemic inequities in education contribute to racial income disparities, limiting opportunities for people of color.

Systemic inequities in education contribute to racial income disparities, limiting opportunities for people of color.

2. How Does Homeownership Affect Racial Wealth And Income Gaps?

Homeownership, a key wealth-building tool, sees racial disparities due to systemic racism in housing. Black families’ homeownership lags behind white families, widening the wealth gap, but income-partners.net can help bridge this gap.

Homeownership is one of the most effective ways for Americans to build wealth, which can be passed down from generation to generation. It provides families with financial security, stability, and the opportunity to accumulate assets. However, systemic racism within housing institutions has long kept communities of color from accessing fair housing opportunities, contributing significantly to racial wealth and income gaps.

-

Historical Context: Historically, discriminatory housing policies such as redlining, restrictive covenants, and discriminatory lending practices have prevented people of color, particularly Black Americans, from purchasing homes in desirable neighborhoods. These policies limited their access to quality education, employment opportunities, and other resources, thereby hindering their ability to build wealth.

-

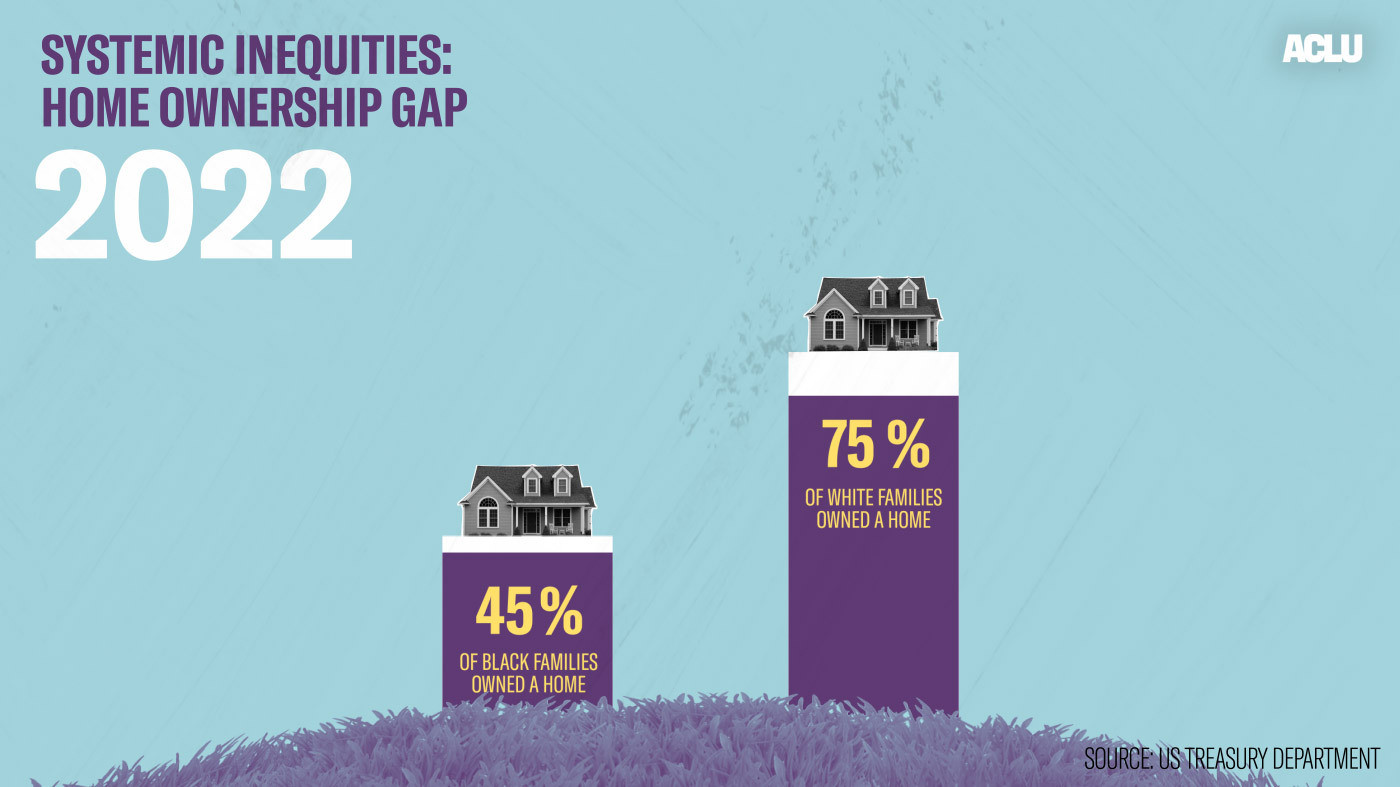

Homeownership Rates: The gap between Black and white families’ homeownership rates has persisted over the years. For example, in 1976, the gap between Black and white families’ homeownership was 25 percent (44 percent of Black families owned a home, compared to 69 percent of white families). In 2022, the gap grew even more to 30 percent (45 percent of Black families owned a home, compared to 75 percent of white families).

-

Impact on Wealth: Homeownership is a primary driver of wealth accumulation. Homeowners build equity over time as they pay down their mortgages and their property values appreciate. This equity can be used to finance education, start a business, or provide a financial safety net. However, due to lower homeownership rates, people of color have been less able to benefit from this wealth-building opportunity.

-

Property Values: Homes in predominantly minority neighborhoods often appreciate at a slower rate than those in predominantly white neighborhoods. This disparity can be attributed to factors such as underinvestment in infrastructure, limited access to quality schools and services, and discriminatory appraisal practices. As a result, homeowners of color may not see the same returns on their investment as their white counterparts.

-

Access to Mortgage Loans: Black and Latino applicants are more likely to be denied mortgage loans than white applicants. According to an analysis of 2019 data, Black applicants were 1.8 times more likely to be denied for a mortgage than white applicants, while Latino applicants were 1.4 times more likely to be denied than white applicants. This disparity limits the ability of people of color to purchase homes and build wealth.

-

Mortgage Interest Rates: Racial bias in mortgage interest rates also contributes to the wealth gap. Black homeowners with high incomes often receive higher interest rates than low-income white homeowners. For example, among those who earn between $30,000 to $44,999 in annual income, the median interest rate for Black homeowners is significantly higher than that of white homeowners.

-

Impact on Future Generations: Homeownership allows families to pass down wealth to future generations, providing them with a financial head start. However, due to lower homeownership rates and discriminatory housing practices, people of color have been less able to transfer wealth to their children and grandchildren, perpetuating the cycle of poverty and inequality.

Racial bias in mortgage interest rates exacerbates the wealth gap in homeownership.

Racial bias in mortgage interest rates exacerbates the wealth gap in homeownership.

3. How Do Mortgage Loan Denials Affect Different Racial Groups?

Mortgage loan denials disproportionately affect Black and Latino applicants, hindering their ability to build wealth through homeownership. At income-partners.net you can explore how diverse partnership strategies can level the playing field in accessing capital and financial services.

Mortgage loan denials significantly impact different racial groups, particularly Black and Latino applicants, hindering their ability to build wealth through homeownership. The disparities in mortgage loan approvals reflect systemic biases and inequalities within the financial system.

-

Denial Rates: Black applicants are significantly more likely to be denied mortgage loans compared to white applicants. For example, an analysis of 2019 data revealed that Black applicants were 1.8 times more likely to be denied a mortgage than white applicants. Latino applicants were also disproportionately affected, with a denial rate 1.4 times higher than that of white applicants.

-

Reasons for Denial: Several factors contribute to the higher denial rates among Black and Latino applicants. These include:

- Credit Scores: Lower credit scores are a common reason for mortgage loan denials. People of color are more likely to have lower credit scores due to historical and ongoing financial disadvantages, such as limited access to credit, higher debt burdens, and predatory lending practices.

- Debt-to-Income Ratio: A high debt-to-income ratio can also lead to mortgage loan denials. People of color often have higher debt-to-income ratios due to lower incomes, higher student loan debt, and other financial obligations.

- Down Payment: Insufficient down payment is another barrier to homeownership. People of color may struggle to save for a down payment due to lower incomes and limited access to wealth-building opportunities.

- Appraisal Bias: Homes in predominantly minority neighborhoods are often undervalued by appraisers, leading to lower loan amounts and higher denial rates. This appraisal bias reflects systemic racism within the housing market.

-

Impact on Wealth Building: Mortgage loan denials prevent people of color from accessing homeownership, a primary driver of wealth accumulation. Without the opportunity to build equity and pass down wealth to future generations, the racial wealth gap continues to widen.

-

Financial Instability: Mortgage loan denials can lead to financial instability and housing insecurity. Renters often face higher housing costs and lack the stability and security of homeownership. This instability can make it difficult to save for the future and build wealth.

-

Economic Consequences: The disparities in mortgage loan approvals have broader economic consequences. They contribute to the concentration of poverty in minority communities, limit economic growth, and perpetuate racial inequality.

-

Addressing the Disparities: Addressing the disparities in mortgage loan approvals requires a multi-faceted approach, including:

- Fair Lending Practices: Enforcing fair lending laws and regulations to prevent discrimination in mortgage lending.

- Credit Counseling: Providing credit counseling and financial education to help people of color improve their credit scores and manage their finances.

- Down Payment Assistance: Offering down payment assistance programs to help people of color overcome the barrier of insufficient down payment.

- Appraisal Reform: Implementing reforms to address appraisal bias and ensure that homes in minority neighborhoods are fairly valued.

Higher denial rates among Black mortgage applicants reflect financial system biases.

Higher denial rates among Black mortgage applicants reflect financial system biases.

4. What Is The Impact Of The Black-White Income Gap On Economic Stability?

The persistent Black-white income gap, widening since 1970, undermines economic stability for Black families and perpetuates inequality. Discover strategies at income-partners.net to foster economic empowerment and close this gap through impactful partnerships.

The Black-white income gap has persisted and grown since 1970, creating significant economic instability for Black families and perpetuating racial inequality. Understanding the extent and impact of this gap is crucial for developing effective strategies to promote economic stability and close the racial wealth divide.

-

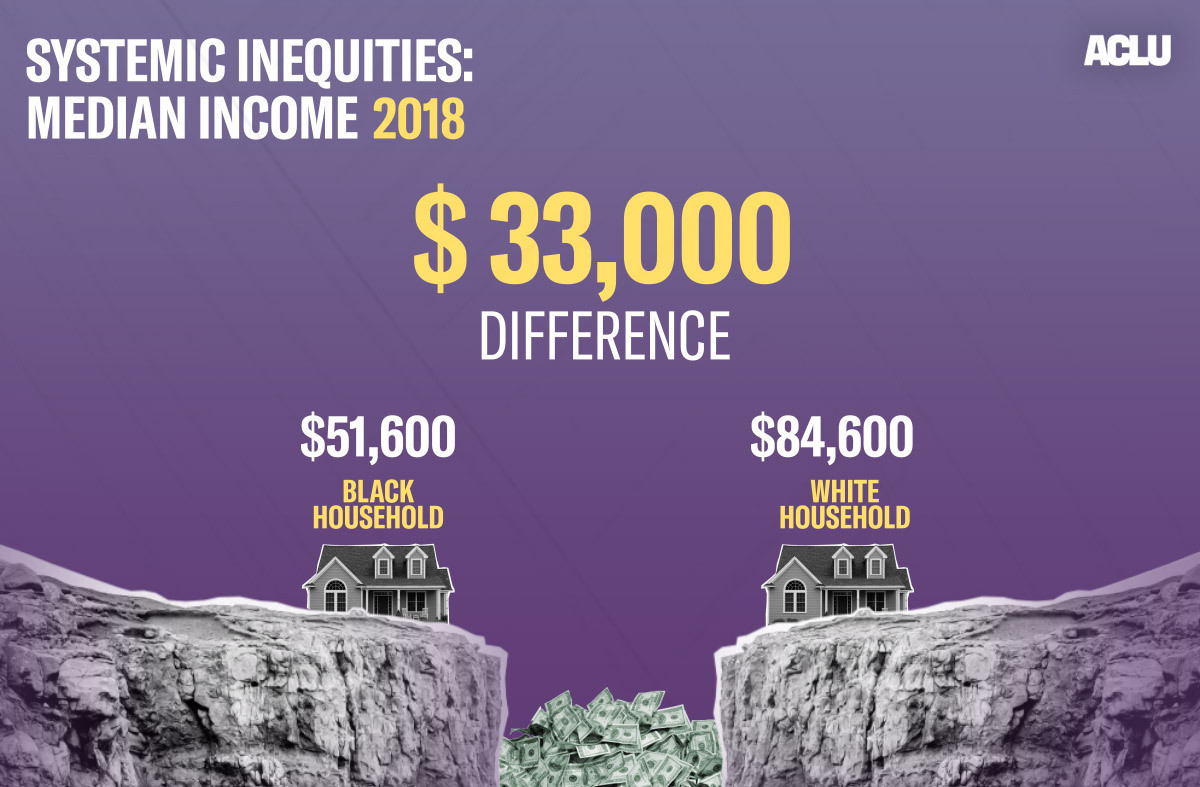

Historical Trends: The Black-white income gap has widened over the past several decades. In 1970, the gap was $23,700, with the median income for a Black household at $30,400 compared to $54,100 for a white household. By 2018, the gap had grown to $33,000, with the median income for a Black family of three at $51,600 compared to $84,600 for a white family of the same size.

-

Factors Contributing to the Gap: Several factors contribute to the Black-white income gap, including:

- Education: Differences in educational attainment and quality of education contribute to income disparities. Black individuals are less likely to have access to quality education and may face barriers to higher education, limiting their career prospects and earning potential.

- Employment: Discrimination in hiring practices, promotion opportunities, and pay equity contributes to the income gap. Black workers may face bias in the workplace, leading to lower wages and limited opportunities for advancement.

- Occupation: Black workers are often concentrated in lower-paying occupations and industries. Occupational segregation limits their earning potential and contributes to the income gap.

- Wealth: The racial wealth gap exacerbates income disparities. Black families have significantly less wealth than white families, limiting their ability to invest in education, start businesses, and build financial security.

- Location: Housing segregation and residential inequality limit access to quality schools, employment opportunities, and other resources. Black individuals living in segregated neighborhoods may face limited economic opportunities and lower earning potential.

-

Impact on Economic Stability: The Black-white income gap has a significant impact on the economic stability of Black families. Lower incomes make it difficult to:

- Meet Basic Needs: Black families are more likely to struggle to meet basic needs such as housing, food, and healthcare.

- Save for the Future: Lower incomes limit the ability to save for retirement, education, and other long-term goals.

- Build Wealth: The income gap perpetuates the racial wealth gap, limiting the ability to build assets and pass down wealth to future generations.

- Weather Economic Shocks: Black families are more vulnerable to economic shocks such as job loss, illness, and unexpected expenses.

-

Economic Consequences: The Black-white income gap has broader economic consequences, including:

- Reduced Consumer Spending: Lower incomes limit consumer spending, which can slow economic growth.

- Increased Poverty Rates: The income gap contributes to higher poverty rates among Black families.

- Reduced Social Mobility: The income gap limits social mobility and perpetuates cycles of poverty and inequality.

- Economic Instability: The income gap can contribute to economic instability and social unrest.

-

Addressing the Gap: Addressing the Black-white income gap requires a multi-faceted approach, including:

- Education Reform: Investing in quality education and ensuring equal access to higher education.

- Employment Equity: Promoting fair hiring practices, pay equity, and equal opportunities for advancement in the workplace.

- Wealth Building: Implementing policies to promote wealth building and asset accumulation among Black families.

- Housing Integration: Promoting housing integration and eliminating residential segregation.

- Economic Development: Investing in economic development in underserved communities.

5. How Can Strategic Partnerships Help Reduce Racial Income Inequality?

Strategic partnerships can bridge resource gaps, promote diverse hiring, and create economic opportunities for marginalized communities. At income-partners.net, you can discover how collaborative ventures can foster inclusive growth and narrow racial income disparities.

Strategic partnerships can play a crucial role in reducing racial income inequality by bridging resource gaps, promoting diverse hiring practices, and creating economic opportunities for marginalized communities. Collaborative ventures can foster inclusive growth and narrow racial income disparities.

-

Resource Sharing: Strategic partnerships can facilitate the sharing of resources, such as funding, expertise, and technology, to support initiatives that address racial income inequality. For example, partnerships between corporations and community organizations can provide funding for job training programs, small business development, and financial literacy initiatives.

-

Diverse Hiring Practices: Partnerships between businesses and educational institutions can promote diverse hiring practices by creating pathways for students of color to enter high-paying professions. Internships, mentorship programs, and scholarships can help students gain the skills and experience needed to succeed in the workforce.

-

Economic Development: Strategic partnerships can drive economic development in marginalized communities by investing in local businesses, creating jobs, and promoting entrepreneurship. Partnerships between government agencies, private companies, and community organizations can revitalize underserved neighborhoods and create economic opportunities for residents.

-

Policy Advocacy: Strategic partnerships can advocate for policies that promote racial equity and reduce income inequality. Coalitions of organizations can lobby for legislation that addresses systemic barriers to economic opportunity, such as discriminatory lending practices, unequal access to education, and biased hiring practices.

-

Community Empowerment: Strategic partnerships can empower communities of color by providing them with the resources and support they need to advocate for their own interests and drive change. Community-led initiatives can address local needs and priorities, while partnerships with external organizations can provide technical assistance and funding.

-

Examples of Successful Partnerships:

- Year Up: A national nonprofit organization that partners with companies to provide young adults from underserved communities with job training, internships, and career opportunities.

- National Urban League: A civil rights organization that partners with corporations and community organizations to promote economic empowerment and social justice.

- Minority Business Development Agency (MBDA): A government agency that partners with businesses and organizations to promote the growth of minority-owned businesses.

-

Addressing Systemic Barriers: Strategic partnerships can address systemic barriers to economic opportunity by promoting policy changes, challenging discriminatory practices, and investing in underserved communities. By working together, organizations can create a more equitable and inclusive economy for all.

6. What Role Does Education Play In Overcoming Racial Income Gaps?

Education is a critical factor in overcoming racial income gaps, providing individuals with skills and knowledge to compete effectively. Visit income-partners.net to learn how partnerships with educational institutions can drive career advancement and economic empowerment for all.

Education plays a pivotal role in overcoming racial income gaps by equipping individuals with the skills, knowledge, and credentials needed to compete effectively in the labor market. Access to quality education is a powerful tool for promoting economic mobility and reducing racial inequality.

-

Skills Development: Education provides individuals with the skills and knowledge needed to succeed in high-paying professions. A strong foundation in math, science, and technology can open doors to careers in fields such as engineering, computer science, and healthcare, where demand is high and salaries are competitive.

-

Credential Attainment: Educational credentials, such as college degrees and professional certifications, signal to employers that individuals have the skills and knowledge needed to perform specific jobs. Individuals with higher levels of education tend to earn more than those with less education.

-

Critical Thinking: Education fosters critical thinking skills, which are essential for problem-solving, decision-making, and innovation. Individuals with strong critical thinking skills are better able to adapt to changing job requirements and advance in their careers.

-

Networking Opportunities: Educational institutions provide networking opportunities that can lead to job opportunities and career advancement. Alumni networks, career fairs, and internships can help students connect with employers and gain valuable experience.

-

Breaking Down Barriers: Education can help break down barriers to economic opportunity by providing individuals with the skills and knowledge needed to overcome systemic discrimination and bias. A strong education can empower individuals to advocate for their rights and challenge inequality in the workplace.

-

Addressing Educational Disparities: Addressing educational disparities is essential for closing the racial income gap. Schools in predominantly minority communities often lack the resources and funding needed to provide a competitive education. Investing in these schools and providing additional support to students of color can help them succeed academically and prepare for college and careers.

-

Promoting Access to Higher Education: Promoting access to higher education is another key strategy for closing the racial income gap. Scholarships, grants, and loan forgiveness programs can help make college more affordable for students of color. Additionally, outreach and support programs can help students navigate the college application process and succeed in higher education.

-

Career and Technical Education: Career and technical education programs can provide students with the skills and training needed to enter high-demand occupations. These programs can be particularly effective for students who are not interested in pursuing a four-year college degree.

7. How Do Biased Hiring Practices Perpetuate Income Inequality?

Biased hiring practices, including both conscious and unconscious biases, limit opportunities for qualified candidates of color, perpetuating income inequality. At income-partners.net, discover how to create fair hiring processes and build diverse, high-performing teams through strategic partnerships.

Biased hiring practices perpetuate income inequality by limiting opportunities for qualified candidates of color. These practices can take various forms, including both conscious and unconscious biases, and can occur at any stage of the hiring process, from initial screening to final selection.

-

Conscious Bias: Conscious bias refers to intentional discrimination based on race, ethnicity, gender, or other protected characteristics. While overt forms of discrimination are less common today, they still exist in some workplaces.

-

Unconscious Bias: Unconscious bias, also known as implicit bias, refers to attitudes or stereotypes that affect our understanding, actions, and decisions in an unconscious manner. These biases can influence hiring decisions without the decision-maker being aware of them.

-

Examples of Biased Hiring Practices:

- Name-Based Discrimination: Studies have shown that applicants with names that sound “Black” or “Latino” are less likely to receive callbacks for job interviews, even when their qualifications are identical to those of white applicants.

- Lack of Diversity in Recruitment: If recruitment efforts are focused on predominantly white networks or institutions, qualified candidates of color may be overlooked.

- Subjective Evaluation Criteria: Subjective evaluation criteria, such as “cultural fit,” can be influenced by unconscious biases and lead to discriminatory hiring decisions.

- Lack of Structured Interviews: Unstructured interviews allow interviewers to ask inconsistent questions and rely on their gut feelings, which can be influenced by unconscious biases.

- Reliance on Referrals: Relying on employee referrals can perpetuate existing diversity gaps, as employees tend to refer candidates who are similar to themselves.

-

Impact on Income Inequality: Biased hiring practices limit opportunities for qualified candidates of color, leading to lower wages, limited career advancement, and higher rates of unemployment. This perpetuates the racial income gap and contributes to broader economic inequality.

-

Creating Fair Hiring Processes: Creating fair hiring processes requires a multi-faceted approach, including:

- Blind Resume Screening: Removing names and other identifying information from resumes to reduce name-based discrimination.

- Diverse Recruitment Strategies: Actively recruiting candidates from diverse networks and institutions.

- Structured Interviews: Using structured interviews with standardized questions and evaluation criteria to reduce subjectivity and bias.

- Bias Training: Providing bias training to hiring managers and interviewers to raise awareness of unconscious biases and how they can affect hiring decisions.

- Monitoring and Accountability: Monitoring hiring outcomes to identify and address any disparities.

-

Building Diverse Teams: Building diverse teams can improve organizational performance, enhance innovation, and create a more inclusive workplace culture. Companies with diverse workforces are better able to attract and retain top talent and serve diverse customer bases.

8. How Can Access To Capital Help Minority-Owned Businesses Grow?

Access to capital is essential for minority-owned businesses to grow, create jobs, and build wealth in their communities. At income-partners.net, you’ll gain access to partnership opportunities that foster economic empowerment and reduce racial wealth disparities.

Access to capital is essential for minority-owned businesses to grow, create jobs, and build wealth in their communities. Limited access to capital is a significant barrier to the success of minority-owned businesses, hindering their ability to compete in the marketplace and contribute to economic growth.

-

Challenges in Accessing Capital: Minority-owned businesses often face challenges in accessing capital from traditional sources, such as banks and venture capital firms. These challenges include:

- Creditworthiness: Minority-owned businesses may have difficulty obtaining loans due to lower credit scores or limited credit history.

- Collateral: Minority-owned businesses may lack the collateral needed to secure loans.

- Loan Size: Minority-owned businesses often require smaller loans, which may be less attractive to traditional lenders.

- Discrimination: Bias in lending practices can limit access to capital for minority-owned businesses.

-

Importance of Capital: Access to capital is essential for minority-owned businesses to:

- Start a Business: Capital is needed to cover startup costs, such as rent, equipment, and inventory.

- Expand Operations: Capital is needed to expand operations, hire employees, and invest in marketing and sales.

- Acquire Assets: Capital is needed to acquire assets, such as real estate, equipment, and technology.

- Manage Cash Flow: Capital is needed to manage cash flow and cover short-term expenses.

-

Alternative Sources of Capital:

- Community Development Financial Institutions (CDFIs): CDFIs are mission-driven lenders that provide financing to underserved communities.

- Microloan Programs: Microloan programs provide small loans to entrepreneurs and small business owners.

- Venture Capital: Venture capital firms invest in high-growth startups and emerging companies.

- Angel Investors: Angel investors are individuals who invest in early-stage companies.

- Crowdfunding: Crowdfunding platforms allow entrepreneurs to raise capital from a large number of individuals.

-

Government Programs:

- Small Business Administration (SBA) Loans: The SBA provides loan guarantees to lenders, making it easier for small businesses to obtain financing.

- Minority Business Development Agency (MBDA) Programs: The MBDA provides assistance to minority-owned businesses in accessing capital and other resources.

-

Impact on Economic Growth: When minority-owned businesses have access to capital, they can create jobs, generate wealth, and contribute to economic growth in their communities. Investing in minority-owned businesses is a powerful strategy for promoting economic equity and reducing racial inequality.

9. What Policies Can Promote Racial Equity And Reduce Income Inequality?

Policies such as affirmative action, fair housing, and equitable education funding can promote racial equity and reduce income inequality. Learn at income-partners.net how strategic partnerships can support and advocate for these policies.

Policies such as affirmative action, fair housing, and equitable education funding can play a critical role in promoting racial equity and reducing income inequality. These policies aim to address systemic barriers to economic opportunity and create a more level playing field for all individuals, regardless of race or ethnicity.

-

Affirmative Action: Affirmative action policies seek to address past and present discrimination by taking proactive steps to ensure equal opportunity in education and employment. These policies may include targeted recruitment efforts, set-asides for minority-owned businesses, and preferential treatment for qualified candidates of color.

-

Fair Housing: Fair housing policies aim to prevent discrimination in housing and ensure that all individuals have equal access to safe, affordable housing. These policies may include laws that prohibit discrimination based on race, ethnicity, religion, or other protected characteristics, as well as programs that promote housing integration and affordability.

-

Equitable Education Funding: Equitable education funding policies seek to address disparities in school funding and ensure that all students have access to quality education, regardless of their race or socioeconomic status. These policies may include reforms to school finance formulas, investments in under-resourced schools, and programs that provide additional support to students of color.

-

Minimum Wage Laws: Minimum wage laws set a minimum wage that employers must pay to their employees. Raising the minimum wage can help reduce income inequality by boosting the earnings of low-wage workers, many of whom are people of color.

-

Earned Income Tax Credit (EITC): The EITC is a tax credit for low- to moderate-income working individuals and families. Expanding the EITC can help reduce poverty and income inequality by providing a financial boost to those who need it most.

-

Child Care Subsidies: Child care subsidies help low-income families afford quality child care. Access to affordable child care can enable parents to work or attend school, boosting their earnings and reducing poverty.

-

Paid Family Leave: Paid family leave policies provide workers with paid time off to care for a new child or a sick family member. Access to paid family leave can help reduce income inequality by enabling workers to balance work and family responsibilities without sacrificing their income.

-

Universal Basic Income (UBI): UBI is a policy proposal that would provide all citizens with a regular, unconditional income. Proponents argue that UBI could help reduce poverty and income inequality by providing a safety net for those who are struggling to make ends meet.

10. How Can Financial Literacy Programs Empower Communities Of Color?

Financial literacy programs empower communities of color by providing knowledge and skills for financial planning, investing, and wealth building. Discover how income-partners.net supports these initiatives through collaborative efforts and partnership opportunities.

Financial literacy programs can empower communities of color by providing individuals with the knowledge and skills they need to make informed financial decisions, manage their money effectively, and build wealth. These programs can address financial disparities and promote economic empowerment in underserved communities.

-

Key Components of Financial Literacy Programs:

- Budgeting: Teaching individuals how to create a budget, track their expenses, and save money.

- Credit Management: Teaching individuals how to build and maintain good credit, avoid debt, and manage their credit cards responsibly.

- Investing: Teaching individuals how to invest in stocks, bonds, and other assets to build wealth over time.

- Retirement Planning: Teaching individuals how to save for retirement and plan for their financial future.

- Homeownership: Providing information about the home buying process, mortgage options, and the responsibilities of homeownership.

- Insurance: Teaching individuals about different types of insurance and how to protect themselves and their families from financial risks.

-

Benefits of Financial Literacy Programs:

- Improved Financial Decision-Making: Financial literacy programs can help individuals make more informed financial decisions, such as choosing the right mortgage, selecting the right insurance policy, and investing wisely.

- Reduced Debt: Financial literacy programs can help individuals avoid debt and manage their existing debt more effectively.

- Increased Savings: Financial literacy programs can help individuals save more money for retirement, education, and other long-term goals.

- Increased Homeownership: Financial literacy programs can help individuals prepare for homeownership and navigate the home buying process.

- Improved Financial Security: Financial literacy programs can help individuals improve their financial security and reduce their vulnerability to financial shocks.

-

Targeted Programs: Financial literacy programs can be tailored to the specific needs of different communities. For example, programs for young adults may focus on student loan debt and career planning, while programs for seniors may focus on retirement planning and elder financial abuse.

-

Partnerships: Financial literacy programs are often delivered through partnerships between community organizations, schools, and financial institutions. These partnerships can leverage the expertise and resources of different organizations to reach a wider audience and provide more comprehensive financial education.

-

Community Outreach: Financial literacy programs should be accessible to all members of the community, regardless of their income, education, or language proficiency. Community outreach efforts can help ensure that these programs reach those who need them most.

FAQ: How Race Affects Income

1. What is the racial wealth gap?

The racial wealth gap refers to the disparity in wealth accumulation between white households and households of color, stemming from historical and ongoing systemic inequities. This disparity affects income and economic opportunities.

2. How does systemic racism affect income?

Systemic racism affects income by limiting access to quality education, fair housing, and employment opportunities for people of color, perpetuating income disparities.

3. What is redlining, and how does it affect wealth?

Redlining is a discriminatory practice that denies loans and services to residents of predominantly minority neighborhoods, limiting their ability to build wealth through homeownership and business development.

4. How do mortgage interest rates affect racial inequality?

Higher mortgage interest rates for Black and Latino homeowners increase the cost of homeownership, reducing wealth accumulation and exacerbating racial inequality.

5. What is the impact of educational disparities on income?

Educational disparities, such as unequal access to quality education, limit career prospects and earning potential for people of color, contributing to the racial income gap.

6. How do biased hiring practices affect income inequality?

Biased hiring practices, including both conscious and unconscious biases, limit opportunities for qualified candidates of color, perpetuating income inequality.

7. What role do strategic partnerships play in addressing racial income inequality?

Strategic partnerships can bridge resource gaps, promote diverse hiring practices, and create economic opportunities for marginalized communities, fostering inclusive growth and reducing racial income disparities.

8. How can access to capital help minority-owned businesses grow?

Access to capital is essential for minority-owned businesses to grow, create jobs, and build wealth in their communities, promoting economic empowerment and reducing racial wealth disparities.

9. What policies can promote racial equity and reduce income inequality?

Policies such as affirmative action, fair housing, and equitable education funding can address systemic barriers to economic opportunity and create a more level playing field for all individuals, regardless of race or ethnicity.

10. How can financial literacy programs empower communities of color?

Financial literacy programs provide individuals with the knowledge and skills they need to make informed financial decisions, manage their money effectively, and build wealth, promoting economic empowerment in underserved communities.

Are you ready to take the next step towards building strategic partnerships and maximizing your income potential? Visit income-partners.net today to explore our resources, connect with potential partners, and unlock new opportunities for growth. Don’t let systemic inequities hold you back – join our community and start building a brighter future. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.