Finding your taxable income can feel like navigating a maze, but it’s a crucial step in understanding your tax obligations. This comprehensive guide from income-partners.net simplifies the process, providing clear explanations and strategies to help you accurately calculate your taxable income and potentially uncover opportunities for partnership and increased income. Understanding how to determine your taxable income is the first step to effective tax planning, and it can open doors to strategic partnerships that boost your bottom line.

1. What Exactly is Taxable Income?

Taxable income is the portion of your total income that’s subject to income tax. It’s not simply your gross income; instead, it’s what remains after you’ve subtracted certain deductions and exemptions. This applies to both individuals and corporations. The difference between gross income and taxable income can be significant, so understanding how to calculate it correctly is essential.

Taxable income is a cornerstone of the tax system, influencing how much you ultimately owe in taxes. It’s important to remember that what constitutes taxable income can vary based on federal, state, and local tax laws.

According to research from the University of Texas at Austin’s McCombs School of Business, understanding taxable income is vital for financial planning, allowing businesses and individuals to make informed decisions about investments and expenditures.

2. How Do Individuals Calculate Taxable Income?

The process for individuals involves several steps, starting with gross income and working down to adjusted gross income (AGI) and then taxable income.

2.1. Starting with Gross Income

Gross income is the total amount of money you’ve earned during the year before any deductions. This includes:

- Salaries and wages

- Bonuses and commissions

- Tips

- Freelance income

- Rental property income

- Retirement plan payouts

- Unemployment benefits

- Court awards

- Gambling winnings

- Interest

- Digital assets and cryptocurrency income

- Royalties

Your filing status (single, married, head of household) also plays a role in determining your taxable income.

2.2. Calculating Adjusted Gross Income (AGI)

To get to your AGI, you subtract “above-the-line” deductions from your gross income. These deductions can include:

- Contributions to certain retirement plans (like traditional IRAs)

- Student loan interest payments

- Alimony payments (for agreements established before 2019)

- Health Savings Account (HSA) contributions

The AGI is an important benchmark because it’s used to determine eligibility for many other deductions and credits.

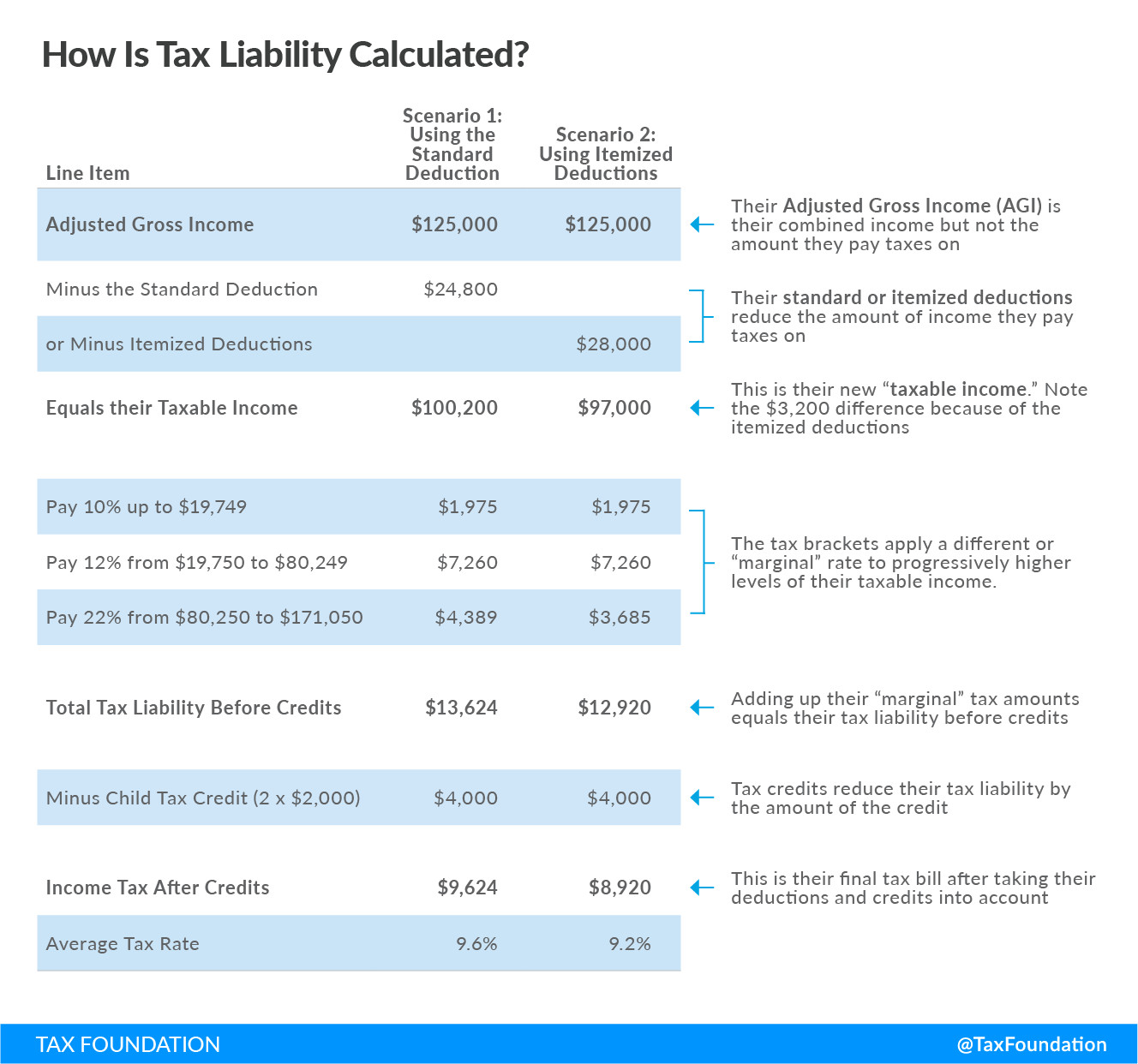

2.3. Determining Taxable Income: Standard vs. Itemized Deductions

After you’ve calculated your AGI, you can choose to take the standard deduction or itemize your deductions.

- Standard Deduction: This is a fixed amount that reduces your taxable income. The amount varies depending on your filing status and is adjusted annually for inflation.

- Itemized Deductions: This involves listing out individual deductions, such as:

- Medical expenses exceeding 7.5% of your AGI

- State and local taxes (SALT), capped at $10,000

- Home mortgage interest

- Charitable contributions

You should choose the option that results in a larger deduction, as this will lower your taxable income and potentially your tax liability.

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

2.4. Qualified Business Income (QBI) Deduction

If you’re a small business owner, freelancer, or independent contractor, you may also be eligible for the Qualified Business Income (QBI) deduction. This deduction allows eligible taxpayers to deduct up to 20% of their qualified business income. It’s a significant benefit that can substantially reduce your taxable income.

3. How Do Corporations Calculate Taxable Income?

For corporations, calculating taxable income involves subtracting various deductions from gross income. These deductions include:

- Compensation paid to employees

- Cost of goods sold (COGS)

- Depreciation expenses

- Interest expenses

- Other ordinary and necessary business expenses

The specific deductions available to a corporation can be complex and depend on the nature of the business.

4. Why is Taxable Income Important?

Understanding your taxable income is crucial for several reasons:

- Accurate Tax Filing: It ensures that you’re paying the correct amount of taxes.

- Financial Planning: Knowing your taxable income allows you to make informed financial decisions, such as planning for retirement or investing in your business.

- Tax Optimization: By understanding the deductions and credits available to you, you can strategically minimize your tax liability.

- Avoiding Penalties: Filing your taxes accurately helps you avoid penalties from the IRS.

5. What is Nontaxable Income?

While most income is taxable, some forms of revenue are generally considered nontaxable. These can include:

- Life insurance payouts

- Payouts from qualified Roth retirement accounts (under certain conditions)

- Health Savings Account (HSA) payments for qualified medical expenses

- The value of employer-provided health insurance

- Certain disability insurance payments

It’s important to note the distinction between income that’s excluded from the tax base altogether (like employer-sponsored health insurance) and income that receives special tax treatment through deductions or Roth accounts.

6. What are Common Mistakes to Avoid When Calculating Taxable Income?

Calculating taxable income can be tricky, and it’s easy to make mistakes. Here are some common errors to avoid:

- Incorrectly Reporting Income: Make sure you’re reporting all sources of income, including freelance work, investment income, and any other earnings.

- Missing Deductions: Don’t overlook eligible deductions, such as those for retirement contributions, student loan interest, or business expenses.

- Choosing the Wrong Deduction Method: Carefully consider whether to take the standard deduction or itemize, and choose the option that benefits you the most.

- Not Keeping Accurate Records: Maintain thorough records of your income and expenses to support your tax filings.

- Misunderstanding Tax Laws: Tax laws can be complex and change frequently, so stay informed about the latest regulations or consult with a tax professional.

7. How Can Strategic Partnerships Impact Your Taxable Income?

Strategic partnerships can significantly impact your taxable income, both directly and indirectly. Here’s how:

- Increased Revenue: Partnerships can lead to increased sales and revenue, which directly affects your gross income.

- Shared Expenses: By sharing resources and expenses with partners, you can reduce your business costs and increase your profitability.

- Tax Credits and Incentives: Some partnerships may qualify for specific tax credits or incentives, depending on the industry and location.

- New Business Opportunities: Partnerships can open doors to new markets and business opportunities, further boosting your income potential.

- Asset Protection: Forming strategic partnerships may lead to asset protection strategies that can affect taxable income.

According to a Harvard Business Review study, successful partnerships are often built on shared values, complementary skills, and a clear understanding of each partner’s goals.

8. What Types of Partnerships Can Help Reduce Taxable Income?

Several types of partnerships can be particularly beneficial for reducing taxable income:

- Strategic Alliances: These partnerships involve collaborating with other businesses to achieve common goals, such as developing new products or entering new markets.

- Joint Ventures: Joint ventures involve two or more businesses pooling their resources to undertake a specific project.

- Distribution Partnerships: These partnerships involve working with distributors to expand your market reach and increase sales.

- Affiliate Partnerships: Affiliate partnerships involve promoting other businesses’ products or services in exchange for a commission.

Each type of partnership has its own tax implications, so it’s important to consult with a tax professional to understand the specific benefits and requirements.

9. What are the Tax Implications of Different Business Structures in Partnerships?

The tax implications of partnerships vary depending on the business structure. Here are some common structures and their tax implications:

- Sole Proprietorship: In a sole proprietorship, the business income is reported on the owner’s personal tax return. The owner is also personally liable for the business’s debts and obligations.

- Partnership: In a partnership, the business income is passed through to the partners, who report it on their personal tax returns. The partnership itself doesn’t pay income tax.

- Limited Liability Company (LLC): An LLC can be taxed as a sole proprietorship, partnership, or corporation, depending on the owner’s preference. This flexibility can provide significant tax advantages.

- S Corporation: An S corporation is a pass-through entity, meaning that the business income is passed through to the shareholders, who report it on their personal tax returns. However, S corporations can also provide tax benefits related to self-employment tax.

- C Corporation: A C corporation is a separate legal entity from its owners and is subject to corporate income tax. Shareholders also pay taxes on dividends received from the corporation.

The choice of business structure can have a significant impact on your taxable income and overall tax liability.

10. How Can Income-Partners.Net Help You Find Strategic Partnerships to Optimize Your Taxable Income?

Income-partners.net is a valuable resource for individuals and businesses looking to find strategic partnerships that can help optimize their taxable income. Here’s how we can help:

- Extensive Network: We have a vast network of potential partners across various industries and locations.

- Targeted Matching: Our platform uses advanced algorithms to match you with partners who align with your business goals and tax objectives.

- Due Diligence Support: We provide resources and support to help you conduct thorough due diligence on potential partners.

- Negotiation Assistance: Our team can assist you in negotiating partnership agreements that are favorable to your tax situation.

- Ongoing Support: We offer ongoing support to help you manage and optimize your partnerships over time.

By leveraging the resources and expertise available at income-partners.net, you can find strategic partnerships that not only boost your revenue but also help you minimize your taxable income.

11. What Strategies Can You Use to Reduce Your Taxable Income Through Partnerships?

Here are some specific strategies you can use to reduce your taxable income through partnerships:

- Cost Sharing: Partner with other businesses to share expenses, such as marketing costs, rent, or equipment purchases.

- Joint Marketing Campaigns: Collaborate with partners on marketing campaigns to increase sales and reduce your individual marketing expenses.

- Research and Development (R&D) Partnerships: Partner with other companies to conduct R&D activities and take advantage of R&D tax credits.

- International Partnerships: Expand your business into international markets through partnerships and take advantage of international tax treaties.

- Opportunity Zone Investments: Partner with businesses in designated Opportunity Zones to invest in real estate or businesses and defer or eliminate capital gains taxes.

These strategies can help you reduce your taxable income while simultaneously growing your business and expanding your network.

12. What are the Benefits of Working with a Tax Professional to Optimize Partnership Tax Strategies?

Working with a tax professional can provide significant benefits when it comes to optimizing partnership tax strategies:

- Expert Knowledge: Tax professionals have in-depth knowledge of tax laws and regulations, which can help you identify tax-saving opportunities.

- Customized Strategies: They can develop customized tax strategies tailored to your specific business and partnership arrangements.

- Compliance Assurance: Tax professionals can help you ensure that you’re complying with all applicable tax laws and regulations.

- Audit Support: In the event of an audit, a tax professional can represent you and provide support throughout the audit process.

- Peace of Mind: Knowing that you have a qualified tax professional on your side can give you peace of mind and allow you to focus on growing your business.

According to a study by the National Federation of Independent Business (NFIB), small businesses that work with tax professionals are more likely to report accurate tax filings and avoid penalties.

13. How to Ensure Your Partnership Agreements are Tax-Efficient?

To ensure that your partnership agreements are tax-efficient, consider the following:

- Clearly Define Roles and Responsibilities: Clearly define each partner’s roles, responsibilities, and contributions to the partnership.

- Establish a Profit and Loss Allocation Method: Establish a clear method for allocating profits and losses among the partners.

- Consider Tax Implications of Distributions: Consider the tax implications of distributions of cash or property to the partners.

- Include Provisions for Tax Elections: Include provisions for making tax elections, such as the election to adjust the basis of partnership property.

- Consult with a Tax Professional: Consult with a tax professional to review your partnership agreement and ensure that it’s tax-efficient.

A well-drafted partnership agreement can help you minimize your taxable income and avoid potential tax disputes.

14. How Can You Stay Updated on Changes to Tax Laws that Affect Partnerships?

Tax laws are constantly changing, so it’s important to stay updated on the latest developments. Here are some ways to do so:

- Subscribe to Tax Newsletters: Subscribe to newsletters from reputable tax organizations, such as the Tax Foundation or the AICPA.

- Attend Tax Seminars and Webinars: Attend tax seminars and webinars to learn about the latest tax law changes.

- Follow Tax Experts on Social Media: Follow tax experts on social media to stay informed about tax news and insights.

- Consult with a Tax Professional: Consult with a tax professional on a regular basis to discuss any tax law changes that may affect your business.

- Check the IRS Website: Regularly check the IRS website for updates and guidance on tax law changes.

Staying informed about tax law changes can help you make informed decisions about your business and partnership strategies.

15. What are Some Real-Life Examples of Partnerships That Have Successfully Reduced Taxable Income?

Here are a few real-life examples of partnerships that have successfully reduced taxable income:

- A software company partnered with a marketing firm to launch a new product. By sharing marketing expenses, they were able to reduce their individual taxable income and increase their overall profitability.

- A real estate developer partnered with an investor to develop a property in an Opportunity Zone. By taking advantage of Opportunity Zone tax incentives, they were able to defer or eliminate capital gains taxes.

- A manufacturing company partnered with a research institution to conduct R&D activities. By taking advantage of R&D tax credits, they were able to reduce their taxable income and invest in innovation.

- A small business owner partnered with another entrepreneur to share office space and administrative expenses. By sharing expenses, they were able to reduce their individual taxable income and improve their cash flow.

These examples illustrate the power of strategic partnerships to reduce taxable income and drive business growth.

16. How do State and Local Taxes Impact Taxable Income?

State and local taxes can significantly impact your overall tax liability. Many states use either AGI or federal taxable income as a starting point for their own income tax calculations. Some states allow deductions for state and local taxes paid, while others do not. It’s crucial to understand the specific state and local tax laws that apply to your business and partnership arrangements.

Some states offer specific tax incentives for businesses that partner with other companies or invest in certain industries. These incentives can further reduce your state and local tax liability.

17. How Does the Qualified Business Income (QBI) Deduction Affect Partnerships?

The Qualified Business Income (QBI) deduction can be a significant tax benefit for partners in certain businesses. This deduction allows eligible taxpayers to deduct up to 20% of their qualified business income. However, there are certain limitations and requirements that must be met in order to qualify for the QBI deduction.

According to IRS guidance, the QBI deduction is generally available to partners in partnerships, S corporations, and sole proprietorships. The deduction is calculated at the individual partner level, based on their share of the partnership’s qualified business income.

18. What Are the Key Tax Forms Related to Partnerships?

Several tax forms are specifically related to partnerships and must be filed annually with the IRS. These forms include:

- Form 1065: U.S. Return of Partnership Income. This form is used to report the partnership’s income, deductions, and credits to the IRS.

- Schedule K-1 (Form 1065): Partner’s Share of Income, Deductions, Credits, etc. This form is used to report each partner’s share of the partnership’s income, deductions, and credits to the IRS and to the partners themselves.

- Form 8825: Rental Real Estate Income and Expenses of a Partnership or an S Corporation. This form is used to report rental real estate income and expenses.

Filing these forms accurately and on time is essential to avoid penalties and ensure compliance with tax laws.

19. What are the Potential Risks and Challenges of Partnerships from a Tax Perspective?

While partnerships can offer significant tax benefits, they also come with potential risks and challenges:

- Liability: Partners may be held liable for the debts and obligations of the partnership, including tax liabilities.

- Disagreements: Disagreements among partners can lead to disputes over tax matters, such as the allocation of income and expenses.

- Complexity: Partnership tax laws can be complex and difficult to navigate, especially for businesses with multiple partners or intricate financial arrangements.

- Changes in Tax Laws: Changes in tax laws can affect the tax treatment of partnerships, requiring businesses to adapt their strategies accordingly.

- Audit Risk: Partnerships may be subject to a higher risk of audit than other types of businesses.

It’s important to carefully consider these risks and challenges before entering into a partnership and to seek professional advice to mitigate them.

20. How Can You Use Tax Planning to Maximize the Benefits of Strategic Partnerships?

Tax planning is essential for maximizing the benefits of strategic partnerships. Here are some tax planning strategies you can use:

- Choose the Right Business Structure: Carefully consider the tax implications of different business structures and choose the one that best suits your needs.

- Allocate Income and Expenses Strategically: Work with a tax professional to allocate income and expenses among the partners in a way that minimizes your overall tax liability.

- Take Advantage of Tax Credits and Incentives: Research and take advantage of any tax credits and incentives that may be available to your partnership.

- Plan for Distributions: Plan for distributions of cash or property to the partners in a tax-efficient manner.

- Review Your Partnership Agreement Regularly: Review your partnership agreement regularly to ensure that it’s still aligned with your tax objectives and that it complies with current tax laws.

By engaging in proactive tax planning, you can maximize the benefits of your strategic partnerships and minimize your tax burden.

21. How Does Depreciation Affect Taxable Income in Partnerships?

Depreciation is a crucial factor in calculating taxable income for partnerships, especially those with significant investments in assets like equipment, buildings, or vehicles. Depreciation allows businesses to deduct a portion of the cost of these assets over their useful life, effectively reducing taxable income in the process. The IRS provides guidelines on how to calculate depreciation using methods like straight-line depreciation or accelerated methods. Understanding which assets qualify for depreciation and the appropriate method to use can significantly impact a partnership’s tax liability.

Furthermore, certain partnerships may qualify for bonus depreciation or Section 179 expensing, which allows for immediate deduction of a larger portion of the asset’s cost in the year of purchase. These provisions can provide substantial tax savings in the short term, but it’s important to consult with a tax professional to ensure compliance and optimize the depreciation strategy for your partnership.

22. How Do Inventory Valuation Methods Impact Taxable Income for Partnerships?

For partnerships that involve the sale of goods, the method used to value inventory can have a direct impact on taxable income. Common inventory valuation methods include First-In, First-Out (FIFO), Last-In, First-Out (LIFO), and weighted-average cost. The choice of method can affect the cost of goods sold (COGS), which is a key component in calculating gross profit and ultimately, taxable income.

During periods of inflation, using FIFO can result in a higher taxable income because older, less expensive inventory is assumed to be sold first, leading to a lower COGS. Conversely, LIFO can result in a lower taxable income because the most recently purchased, more expensive inventory is assumed to be sold first, leading to a higher COGS. However, LIFO is not permitted under IFRS (International Financial Reporting Standards). The weighted-average cost method provides a middle ground, averaging the cost of all inventory items to determine COGS. The most suitable inventory valuation method depends on the specific circumstances of the partnership and should be chosen in consultation with a tax advisor.

23. What Are the Tax Implications of Partnership Mergers and Acquisitions?

Partnership mergers and acquisitions (M&A) can have complex tax implications that require careful planning and execution. When one partnership acquires another, the transaction can be structured in various ways, each with its own tax consequences. For example, the acquisition can be treated as a purchase of assets, a purchase of partnership interests, or a merger. The tax treatment will depend on the specific structure of the deal and the applicable tax laws.

In some cases, a partnership merger may result in a taxable event for the partners, triggering capital gains or losses. It’s important to conduct thorough due diligence and consult with tax professionals to understand the potential tax consequences of a partnership merger or acquisition before proceeding with the transaction. Properly structuring the deal can help minimize tax liabilities and maximize the benefits of the merger or acquisition.

24. How Can Partnerships Utilize Tax Credits for Hiring Specific Groups?

Partnerships can potentially reduce their taxable income by taking advantage of tax credits for hiring individuals from specific groups. The Work Opportunity Tax Credit (WOTC) is a federal tax credit available to employers who hire individuals from certain targeted groups, such as veterans, individuals receiving government assistance, and ex-felons. The WOTC can provide a significant tax benefit for partnerships that actively recruit and hire individuals from these groups.

In addition to the WOTC, some states offer their own tax credits or incentives for hiring specific groups, such as individuals with disabilities or those living in economically disadvantaged areas. Partnerships should research the available tax credits in their state and develop a hiring strategy that aligns with these incentives. By strategically hiring individuals from targeted groups, partnerships can reduce their taxable income while also contributing to social and economic development.

25. How Do Foreign Partnerships Impact U.S. Taxable Income?

Foreign partnerships that conduct business in the United States or have U.S. partners are subject to U.S. tax laws. The tax treatment of foreign partnerships can be complex and depends on factors such as whether the partnership is engaged in a U.S. trade or business, whether it has U.S. source income, and whether it has U.S. partners. Foreign partnerships engaged in a U.S. trade or business are generally subject to U.S. income tax on their income effectively connected with that trade or business.

U.S. partners in foreign partnerships are generally required to report their share of the partnership’s income, deductions, and credits on their U.S. tax returns. They may also be subject to certain information reporting requirements, such as filing Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships. It’s crucial for foreign partnerships and their U.S. partners to understand and comply with U.S. tax laws to avoid penalties and ensure accurate reporting of taxable income.

26. What Role Does Estate Planning Play in Partnership Taxation?

Estate planning plays a critical role in partnership taxation, particularly in the event of a partner’s death or incapacity. A well-designed estate plan can help ensure a smooth transition of partnership interests and minimize potential tax liabilities. Without proper planning, the death of a partner can trigger complex tax consequences, such as estate taxes, income taxes, and potential disruptions to the partnership’s operations.

Estate planning strategies for partnerships may include buy-sell agreements, which provide a mechanism for the remaining partners to purchase the deceased partner’s interest in the partnership. These agreements can help ensure continuity of the business and provide liquidity to the deceased partner’s estate. Additionally, trusts and other estate planning tools can be used to minimize estate taxes and facilitate the transfer of partnership interests to the next generation. Consulting with an estate planning attorney and a tax advisor is essential to develop a comprehensive estate plan that addresses the specific needs and circumstances of the partnership and its partners.

27. How Can Partnerships Use Cost Segregation Studies to Reduce Taxable Income?

Cost segregation studies are a powerful tool that partnerships can use to accelerate depreciation deductions and reduce taxable income. A cost segregation study involves analyzing the various components of a building or other real property and classifying them into different asset classes with shorter depreciable lives. For example, certain electrical or plumbing components may be classified as personal property with a 5-year or 7-year depreciable life, rather than being depreciated over the 27.5-year or 39-year life of the building itself.

By reclassifying assets into shorter-lived categories, partnerships can claim larger depreciation deductions in the early years of ownership, resulting in a significant reduction in taxable income. Cost segregation studies are particularly beneficial for partnerships that have recently constructed, purchased, or renovated commercial properties. It’s important to engage a qualified cost segregation specialist to conduct the study and ensure compliance with IRS guidelines.

28. What are Common Tax Audit Triggers for Partnerships?

Partnerships, like any business entity, can be subject to tax audits by the IRS. Certain factors can increase the likelihood of a partnership being selected for an audit. Common tax audit triggers for partnerships include:

- Large Losses: Partnerships that report significant losses may be subject to increased scrutiny by the IRS.

- Unusual Deductions: Claiming deductions that are unusually large or inconsistent with industry norms can raise red flags.

- Related-Party Transactions: Transactions between the partnership and related parties, such as partners or their family members, may be closely examined.

- Lack of Documentation: Failing to maintain adequate documentation to support income, deductions, and credits can increase the risk of an audit.

- Industry-Specific Issues: Partnerships in certain industries that are known for tax compliance issues may be targeted for audits.

Being aware of these common audit triggers can help partnerships take steps to minimize their risk of being selected for an audit and ensure that they are prepared to respond to any inquiries from the IRS.

29. How Can Partnerships Document Business Expenses for Tax Purposes?

Proper documentation of business expenses is essential for partnerships to support their deductions and avoid potential tax issues. The IRS requires taxpayers to maintain adequate records to substantiate their income, deductions, and credits. For partnerships, this means keeping detailed records of all business expenses, including receipts, invoices, bank statements, and other supporting documentation.

When documenting business expenses, it’s important to record the date, amount, vendor, and business purpose of each expense. For expenses of $75 or more, a receipt is generally required. For travel and entertainment expenses, it’s important to document the dates, locations, and business purpose of the trip or event, as well as the names and relationships of the individuals involved. Maintaining organized and complete records of business expenses can help partnerships support their deductions and avoid penalties in the event of an audit.

30. What Tax Software and Resources are Available for Partnerships?

Several tax software programs and resources are available to help partnerships manage their tax obligations and comply with tax laws. Popular tax software options for partnerships include TurboTax Business, H&R Block Business, and TaxAct Business. These software programs can help partnerships prepare and file their federal and state tax returns, as well as track income, expenses, and deductions.

In addition to tax software, partnerships can also utilize online resources such as the IRS website, which provides access to tax forms, publications, and guidance. Professional tax organizations like the AICPA and the Tax Foundation also offer valuable resources and insights on tax law changes and planning strategies. Partnerships should explore these available tools and resources to ensure that they are well-equipped to manage their tax obligations and optimize their tax strategies.

By understanding these key concepts and strategies, partnerships can effectively navigate the complex world of taxation and maximize their financial success. Remember, income-partners.net is here to help you connect with the right partners and resources to achieve your business and tax objectives.

Ready to explore how strategic partnerships can transform your income and tax situation? Visit income-partners.net today to discover a world of opportunities! Our platform offers resources on partner selection, agreement negotiation, and proven strategies for success. Let income-partners.net be your guide to building profitable, tax-optimized partnerships.

FAQ: Finding Your Taxable Income

- What is the difference between gross income and taxable income? Gross income is your total income before any deductions, while taxable income is the portion of your income that’s subject to tax after deductions and exemptions.

- How do I calculate my adjusted gross income (AGI)? Subtract “above-the-line” deductions (like retirement contributions and student loan interest) from your gross income.

- What’s the difference between the standard deduction and itemizing? The standard deduction is a fixed amount, while itemizing involves listing individual deductions like medical expenses and mortgage interest. Choose the option that gives you a larger deduction.

- What is the Qualified Business Income (QBI) deduction? It’s a deduction for eligible small business owners, freelancers, and independent contractors, allowing them to deduct up to 20% of their qualified business income.

- What is considered nontaxable income? Examples include life insurance payouts, certain Roth retirement account distributions, and employer-provided health insurance.

- How can strategic partnerships impact my taxable income? They can increase revenue, share expenses, qualify for tax credits, and open new business opportunities.

- What types of partnerships can help reduce taxable income? Strategic alliances, joint ventures, distribution partnerships, and affiliate partnerships.

- How do I ensure my partnership agreements are tax-efficient? Clearly define roles, establish a profit/loss allocation method, consider distribution implications, and consult a tax professional.

- How can I stay updated on changes to tax laws that affect partnerships? Subscribe to tax newsletters, attend seminars, follow experts on social media, and consult with a tax professional.

- Where can I find strategic partners to optimize my taxable income? income-partners.net offers an extensive network, targeted matching, and expert support to help you find the right partnerships.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.