Determining taxable income involves calculating the amount of your income that is subject to tax after deductions and exemptions, impacting your tax liability and financial planning; income-partners.net provides resources to help navigate this process. This guide offers practical advice, strategic insights, and expert guidance to help you understand how to calculate your taxable income, optimize your financial strategies, and explore partnership opportunities. Explore our website for more information on effective tax strategies and partnership opportunities, and stay informed about the latest developments in tax regulations and financial planning.

1. What Is Taxable Income and Why Does It Matter?

Taxable income is the portion of your gross income that is subject to taxation after all eligible deductions and exemptions have been applied. This figure is essential because it directly affects the amount of tax you owe to federal, state, and local governments. Understanding how to calculate your taxable income allows you to make informed financial decisions, potentially reduce your tax liability, and plan for your financial future more effectively. Proper calculation ensures compliance with tax laws, helping you avoid penalties and audits.

1.1. Understanding Gross Income

Gross income is the starting point for calculating taxable income. It includes all income you receive in the form of money, property, and services that are not specifically exempt from tax.

What to Include in Gross Income:

- Wages and Salaries: This includes all compensation you receive from employment, including bonuses, commissions, and tips.

- Business Income: Revenue from self-employment, freelancing, and owning a business.

- Investment Income: Dividends, interest, capital gains, and rental income from investments.

- Retirement Income: Distributions from pensions, 401(k)s, and traditional IRAs (Roth IRA distributions are typically tax-free).

- Other Income: This category includes alimony, unemployment compensation, Social Security benefits (if applicable), and any other income not specifically excluded.

1.2. Above-the-Line Deductions: Reducing Your AGI

Above-the-line deductions are subtractions from your gross income that you can claim regardless of whether you itemize or take the standard deduction. These deductions reduce your adjusted gross income (AGI), which is a crucial figure in determining your eligibility for certain tax credits and deductions.

Common Above-the-Line Deductions:

- Traditional IRA Contributions: Contributions to a traditional IRA may be deductible, depending on your income and whether you are covered by a retirement plan at work.

- Student Loan Interest: You can deduct the interest you pay on qualified student loans, up to a certain limit.

- Health Savings Account (HSA) Contributions: Contributions to an HSA are deductible, offering a tax-advantaged way to save for healthcare expenses.

- Self-Employment Tax: You can deduct one-half of your self-employment tax, which is the equivalent of the employer’s portion of Social Security and Medicare taxes.

- Alimony Payments: For divorce agreements finalized before December 31, 2018, alimony payments are deductible by the payer.

1.3. Adjusted Gross Income (AGI): An Intermediate Step

Adjusted Gross Income (AGI) is calculated by subtracting above-the-line deductions from your gross income. AGI is a significant figure because many tax benefits, such as certain credits and deductions, are based on your AGI. A lower AGI can increase the amount of these benefits you are eligible to receive.

Importance of AGI:

- Eligibility for Tax Credits: Many tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit, have AGI limits.

- Deductibility of Medical Expenses: The amount of medical expenses you can deduct is limited to the amount exceeding 7.5% of your AGI.

- IRA Contributions: The ability to deduct traditional IRA contributions may be limited based on your AGI if you are covered by a retirement plan at work.

2. Standard Deduction vs. Itemized Deductions: Choosing the Right Approach

After calculating your AGI, you must decide whether to take the standard deduction or itemize your deductions. This decision can significantly impact your taxable income and, consequently, your tax liability.

2.1. Understanding the Standard Deduction

The standard deduction is a fixed dollar amount that reduces your taxable income, and it varies based on your filing status (single, married filing jointly, head of household, etc.). The standard deduction is adjusted annually for inflation.

2023 Standard Deduction Amounts:

| Filing Status | Standard Deduction |

|---|---|

| Single | $13,850 |

| Married Filing Separately | $13,850 |

| Married Filing Jointly | $27,700 |

| Head of Household | $20,800 |

Benefits of Taking the Standard Deduction:

- Simplicity: It simplifies tax preparation as you don’t need to track and document specific expenses.

- Time-Saving: It reduces the time spent on tax preparation.

- No Record-Keeping: You don’t need to keep detailed records of various deductible expenses.

2.2. Understanding Itemized Deductions

Itemized deductions are specific expenses that you can deduct from your AGI. These deductions can include medical expenses, state and local taxes (SALT), home mortgage interest, and charitable contributions.

Common Itemized Deductions:

- Medical Expenses: You can deduct medical expenses that exceed 7.5% of your AGI. This includes costs for doctors, hospitals, insurance premiums, and long-term care.

- State and Local Taxes (SALT): You can deduct state and local property taxes, income taxes (or sales taxes), up to a combined limit of $10,000 per household.

- Home Mortgage Interest: You can deduct the interest you pay on a mortgage for your primary or secondary residence, subject to certain limitations based on the mortgage amount and when it was taken out.

- Charitable Contributions: You can deduct contributions to qualified charitable organizations, typically up to 60% of your AGI for cash contributions and 50% for other property.

2.3. Choosing Between Standard and Itemized Deductions

You should choose the option that results in the lower taxable income. Compare the total of your itemized deductions to the standard deduction for your filing status. If your itemized deductions exceed the standard deduction, you should itemize. Otherwise, take the standard deduction.

Factors to Consider:

- High Medical Expenses: If you have significant medical expenses, itemizing may be beneficial.

- High State and Local Taxes: If you live in a state with high property and income taxes, your SALT deduction could exceed the standard deduction.

- Homeownership: Homeowners often have mortgage interest and property taxes that can make itemizing worthwhile.

- Charitable Giving: If you make substantial charitable contributions, itemizing may be advantageous.

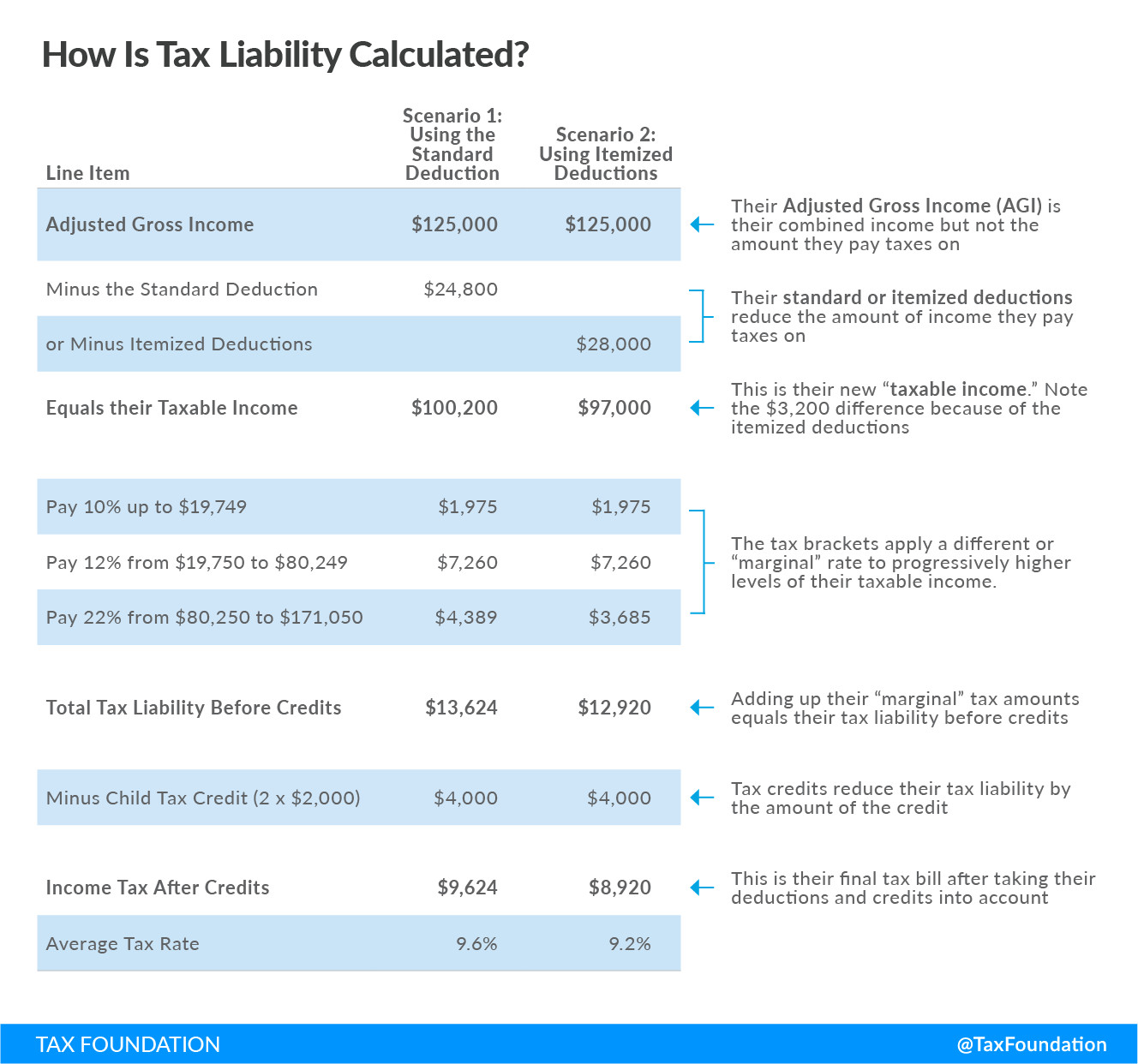

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

3. Specific Deductions and Exemptions That Lower Taxable Income

Certain deductions and exemptions can significantly lower your taxable income. Understanding these can help you optimize your tax strategy.

3.1. Business Expenses for the Self-Employed

If you are self-employed, you can deduct many business-related expenses from your gross income.

Common Business Deductions:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct expenses related to that space.

- Business Vehicle Expenses: You can deduct the actual expenses of operating your vehicle for business purposes or take the standard mileage rate.

- Supplies and Equipment: Expenses for supplies and equipment used in your business are deductible.

- Advertising and Marketing: Costs associated with advertising and marketing your business are deductible.

- Professional Fees: Fees paid to attorneys, accountants, and other professionals for business services are deductible.

3.2. Rental Property Expenses

If you own rental property, you can deduct various expenses related to the property.

Deductible Rental Property Expenses:

- Mortgage Interest: You can deduct the interest you pay on a mortgage for the rental property.

- Property Taxes: Property taxes you pay are deductible.

- Insurance: Insurance premiums for the rental property are deductible.

- Repairs and Maintenance: Costs for repairs and maintenance are deductible, while improvements are capitalized and depreciated over time.

- Depreciation: You can deduct a portion of the property’s cost each year as depreciation.

3.3. Retirement Contributions

Contributions to retirement accounts, such as 401(k)s and IRAs, can provide significant tax benefits.

Tax Advantages of Retirement Contributions:

- Traditional 401(k) and IRA: Contributions are often tax-deductible, reducing your current taxable income.

- Roth 401(k) and IRA: While contributions are not deductible, qualified distributions in retirement are tax-free.

- Employer Matching: Employer contributions to your 401(k) are not taxable to you until you withdraw them in retirement.

3.4. Health Savings Accounts (HSAs)

HSAs are tax-advantaged savings accounts for healthcare expenses.

Benefits of HSAs:

- Tax-Deductible Contributions: Contributions to an HSA are deductible.

- Tax-Free Growth: Investment earnings in an HSA grow tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are tax-free.

3.5. Education-Related Deductions and Credits

Several education-related tax benefits can help reduce your taxable income or tax liability.

Education Tax Benefits:

- Student Loan Interest Deduction: You can deduct the interest you pay on qualified student loans, up to a certain limit.

- American Opportunity Tax Credit (AOTC): This credit is for expenses paid for the first four years of higher education.

- Lifetime Learning Credit (LLC): This credit is for expenses paid for any course to acquire job skills.

- Tuition and Fees Deduction: Although this deduction has been expired it allows you to deduct qualified tuition and fees paid for higher education.

4. How Taxable Income Differs for Individuals and Corporations

The calculation of taxable income varies significantly between individuals and corporations due to differences in income sources, deductions, and tax regulations.

4.1. Taxable Income for Individuals

For individuals, taxable income is determined by subtracting deductions and exemptions from gross income to arrive at AGI, then further reducing AGI by either the standard deduction or itemized deductions.

Key Components for Individuals:

- Gross Income: Includes wages, salaries, tips, investment income, and other earnings.

- Above-the-Line Deductions: Subtractions from gross income for items like IRA contributions and student loan interest.

- Adjusted Gross Income (AGI): Gross income minus above-the-line deductions.

- Standard Deduction or Itemized Deductions: Choice between a fixed amount (standard deduction) or specific expenses (itemized deductions).

- Taxable Income: AGI minus the standard deduction or itemized deductions.

4.2. Taxable Income for Corporations

For corporations, taxable income is calculated by subtracting business expenses and other deductions from gross revenue.

Key Components for Corporations:

- Gross Revenue: Total income from sales, services, and other sources.

- Cost of Goods Sold (COGS): Direct costs associated with producing goods or services.

- Operating Expenses: Expenses for running the business, such as salaries, rent, and utilities.

- Interest Expense: Interest paid on business loans.

- Depreciation: Deduction for the wear and tear of assets over time.

- Taxable Income: Gross revenue minus COGS, operating expenses, interest expense, and depreciation.

4.3. Key Differences Summarized

| Feature | Individuals | Corporations |

|---|---|---|

| Income Sources | Wages, salaries, investments, self-employment | Sales, services, investments |

| Deductions | Standard or itemized (medical expenses, SALT, mortgage interest, etc.), above-the-line deductions (IRA contributions) | Business expenses (salaries, rent, utilities), COGS, depreciation, interest expense |

| Tax Forms | Form 1040 | Form 1120 (C corporations), Form 1120S (S corporations) |

| Tax Rates | Progressive tax rates based on income brackets | Corporate tax rate (currently a flat 21% federal rate) |

| Pass-Through Entities | Income passes through to individual owners and is taxed at individual rates (e.g., S corporations, partnerships) | Income is taxed at the corporate level (C corporations) |

5. Understanding Nontaxable Income

Not all income is subject to taxation. Understanding what qualifies as nontaxable income is crucial for accurate financial planning and tax compliance.

5.1. Common Types of Nontaxable Income

Several types of income are generally considered nontaxable by the IRS.

Examples of Nontaxable Income:

- Life Insurance Payouts: Proceeds from a life insurance policy paid to beneficiaries are generally not taxable.

- Gifts and Inheritances: Gifts you receive are generally not taxable, although large gifts may be subject to gift tax for the giver. Inheritances are also typically not taxable at the federal level, though estate taxes may apply to the estate.

- Qualified Roth IRA Distributions: Distributions from a Roth IRA are tax-free if certain conditions are met, such as being at least 59 1/2 years old and having held the account for at least five years.

- Health Savings Account (HSA) Withdrawals: Withdrawals from an HSA for qualified medical expenses are tax-free.

- Certain Scholarship and Grant Amounts: Scholarship and grant amounts used for tuition, fees, and required books are generally not taxable.

5.2. Income That Can Be Taxed Differently

Some forms of income are technically not considered taxable income but may be subject to other taxes.

Examples of Income with Special Tax Treatment:

- Financial Gifts Over the Annual Exclusion: Gifts over $17,000 per recipient in 2023 may be subject to gift tax. The giver pays this tax, not the recipient.

- Inheritances: While inheritances are not taxed as income to the recipient, the estate may be subject to estate taxes if it exceeds a certain threshold (over $12.92 million in 2023).

5.3. The Importance of Knowing What Is Nontaxable

Understanding what types of income are nontaxable helps you avoid overpaying taxes and accurately report your income. It also aids in financial planning, as you can make informed decisions about savings, investments, and gifts.

6. Tax Planning Strategies to Minimize Taxable Income

Effective tax planning involves implementing strategies to legally minimize your taxable income and reduce your tax liability. Here are some key strategies to consider.

6.1. Maximize Retirement Contributions

Contributing the maximum amount to retirement accounts can significantly reduce your taxable income.

Strategies:

- 401(k) Contributions: Contribute up to the maximum allowed by law. In 2023, the maximum employee contribution is $22,500 (with an additional $7,500 catch-up contribution for those age 50 and over).

- IRA Contributions: Contribute to a traditional IRA, which may be tax-deductible. The maximum IRA contribution for 2023 is $6,500 (with an additional $1,000 catch-up contribution for those age 50 and over).

- SEP IRA for Self-Employed: If you’re self-employed, consider a Simplified Employee Pension (SEP) IRA, which allows for substantial contributions.

6.2. Take Advantage of All Available Deductions

Ensure you’re taking all eligible deductions to reduce your taxable income.

Strategies:

- Itemize Deductions When Possible: If your itemized deductions exceed the standard deduction, itemize to reduce your taxable income.

- Home Office Deduction: If you work from home, claim the home office deduction if you meet the requirements.

- Business Expenses: If you own a business, deduct all eligible business expenses.

6.3. Utilize Tax-Advantaged Accounts

Use tax-advantaged accounts like HSAs and 529 plans to save on taxes.

Strategies:

- Health Savings Account (HSA): Contribute to an HSA if you have a high-deductible health plan. Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- 529 Plans: Save for education expenses using a 529 plan. Contributions may be tax-deductible at the state level, and earnings grow tax-free.

6.4. Strategic Charitable Giving

Plan your charitable giving to maximize tax benefits.

Strategies:

- Donate Appreciated Assets: Donate appreciated stocks or mutual funds to avoid paying capital gains taxes and deduct the fair market value of the donation.

- Bunching Donations: If you don’t itemize every year, consider bunching your charitable donations into a single year to exceed the standard deduction.

- Qualified Charitable Distributions (QCDs): If you’re age 70 1/2 or older, you can make QCDs from your IRA directly to a charity, which can satisfy your required minimum distributions (RMDs) and reduce your taxable income.

6.5. Investment Strategies

Implement tax-efficient investment strategies to minimize taxes on your investment income.

Strategies:

- Tax-Loss Harvesting: Sell investments that have lost value to offset capital gains.

- Hold Investments Longer Than One Year: Capital gains on assets held for more than one year are taxed at lower rates than short-term gains.

- Invest in Tax-Advantaged Accounts: Use accounts like 401(k)s, IRAs, and HSAs to shield your investments from taxes.

7. Common Mistakes to Avoid When Calculating Taxable Income

Calculating taxable income can be complex, and it’s easy to make mistakes. Avoiding these common errors can save you time and money.

7.1. Overlooking Deductions

One of the most common mistakes is overlooking eligible deductions.

How to Avoid:

- Keep Detailed Records: Maintain detailed records of all potential deductions, including medical expenses, charitable contributions, and business expenses.

- Use Tax Software: Utilize tax software or work with a tax professional to ensure you’re not missing any deductions.

- Review Tax Laws Regularly: Stay updated on changes to tax laws that may affect your eligibility for deductions.

7.2. Incorrect Filing Status

Choosing the wrong filing status can result in overpaying taxes.

How to Avoid:

- Understand Filing Status Options: Familiarize yourself with the different filing statuses (single, married filing jointly, married filing separately, head of household, qualifying widow(er)) and choose the one that best fits your situation.

- Consider Head of Household: If you’re unmarried and pay more than half the costs of keeping up a home for a qualifying child, you may be eligible for head of household status, which offers a larger standard deduction and more favorable tax rates than single status.

7.3. Miscalculating Income

Inaccurately calculating your income can lead to significant tax errors.

How to Avoid:

- Report All Income: Ensure you report all income, including wages, self-employment income, investment income, and other earnings.

- Use Accurate Forms: Use the correct tax forms (W-2, 1099, etc.) to report your income accurately.

- Double-Check Your Math: Double-check all calculations to ensure accuracy.

7.4. Not Adjusting for Inflation

Failing to adjust for inflation can lead to incorrect calculations of deductions and credits.

How to Avoid:

- Use Current-Year Data: Use the current-year standard deduction amounts, tax brackets, and other relevant figures when calculating your taxable income.

- Stay Informed: Keep up with annual inflation adjustments to tax laws.

7.5. Not Seeking Professional Advice

Attempting to navigate complex tax situations without professional help can lead to costly mistakes.

How to Avoid:

- Consult a Tax Professional: Work with a qualified tax advisor or accountant to ensure you’re accurately calculating your taxable income and taking advantage of all eligible tax benefits.

- Use Reliable Resources: Consult reliable tax resources, such as the IRS website and publications, for guidance.

8. The Impact of Tax Reforms on Taxable Income Calculation

Tax reforms can significantly impact how taxable income is calculated. Staying informed about these changes is essential for accurate tax planning and compliance.

8.1. Recent Tax Law Changes

Recent tax law changes, such as the Tax Cuts and Jobs Act (TCJA) of 2017, have made significant alterations to the calculation of taxable income.

Key Changes from the TCJA:

- Increased Standard Deduction: The TCJA nearly doubled the standard deduction, making it less beneficial for many taxpayers to itemize.

- SALT Deduction Limit: The TCJA limited the deduction for state and local taxes (SALT) to $10,000 per household.

- Elimination of Personal Exemptions: The TCJA eliminated personal exemptions, but it increased the child tax credit.

- Changes to Business Deductions: The TCJA created a new deduction for qualified business income (QBI) for pass-through entities.

8.2. Staying Updated on Tax Law Changes

Tax laws are subject to change, so it’s important to stay informed about the latest developments.

How to Stay Informed:

- Follow the IRS: Regularly check the IRS website for updates, publications, and guidance.

- Consult Tax Professionals: Work with a tax advisor who stays current on tax law changes.

- Read Tax News: Subscribe to tax news publications and follow reputable tax experts on social media.

8.3. Adjusting Tax Strategies

When tax laws change, you may need to adjust your tax strategies to maximize your tax benefits.

How to Adjust Your Strategies:

- Review Your Deductions: Re-evaluate your itemized deductions and compare them to the standard deduction to determine whether itemizing is still beneficial.

- Adjust Withholding: Adjust your W-4 form with your employer to ensure you’re not underpaying or overpaying your taxes.

- Update Your Tax Plan: Work with a tax advisor to update your tax plan to reflect the new tax laws.

9. Resources for Calculating and Minimizing Taxable Income

Several resources are available to help you accurately calculate and minimize your taxable income.

9.1. IRS Resources

The IRS provides numerous resources to help taxpayers understand and comply with tax laws.

Key IRS Resources:

- IRS Website: The IRS website (www.irs.gov) offers a wealth of information, including publications, forms, and FAQs.

- IRS Publications: IRS publications cover a wide range of tax topics and provide detailed guidance on specific issues.

- IRS Taxpayer Assistance Centers: The IRS operates Taxpayer Assistance Centers where you can get in-person help with your taxes.

- IRS Free File: The IRS Free File program offers free tax software and online filing options for eligible taxpayers.

9.2. Tax Software

Tax software can simplify the process of calculating your taxable income and filing your taxes.

Popular Tax Software Options:

- TurboTax: A popular tax software program that offers step-by-step guidance and a user-friendly interface.

- H&R Block: Another popular tax software option that provides a range of features and support options.

- TaxAct: A more affordable tax software option that still offers comprehensive features and support.

9.3. Tax Professionals

Working with a tax professional can provide personalized guidance and ensure you’re accurately calculating your taxable income and taking advantage of all eligible tax benefits.

Types of Tax Professionals:

- Certified Public Accountants (CPAs): CPAs are licensed professionals who have passed a rigorous exam and met certain education and experience requirements.

- Enrolled Agents (EAs): EAs are federally licensed tax practitioners who have demonstrated competence in tax law.

- Tax Attorneys: Tax attorneys are lawyers who specialize in tax law and can provide legal advice on tax matters.

9.4. Online Resources

Numerous online resources can help you calculate and minimize your taxable income.

Useful Online Resources:

- Tax Foundation: A non-profit organization that provides analysis and information on tax policy.

- AICPA: The American Institute of Certified Public Accountants offers resources and guidance for taxpayers.

- Income-partners.net: Explore our website for more information on effective tax strategies and partnership opportunities.

10. How Partnership Opportunities Can Impact Your Taxable Income

Partnerships can offer unique opportunities to manage and potentially reduce your taxable income through strategic business and investment decisions.

10.1. Understanding Partnership Structures

Different partnership structures can affect how income and deductions are allocated and taxed.

Types of Partnerships:

- General Partnership (GP): All partners share in the business’s operational management and liabilities. Income and losses are typically divided equally, unless otherwise stated in the partnership agreement.

- Limited Partnership (LP): Includes general partners (who manage the business and have unlimited liability) and limited partners (who have limited liability and are not involved in day-to-day operations).

- Limited Liability Partnership (LLP): Protects partners from the negligence or malpractice of other partners. This is common among professionals like attorneys and accountants.

- Limited Liability Company (LLC): While technically not a partnership, it offers similar pass-through taxation and liability protection.

10.2. Tax Implications of Partnership Income

Partnership income is typically “passed through” to the partners, who report their share of the income on their individual tax returns.

Key Tax Implications:

- Pass-Through Taxation: The partnership itself does not pay income tax. Instead, each partner reports their share of the partnership’s income, gains, losses, and deductions on their individual tax return.

- Self-Employment Tax: General partners are subject to self-employment tax on their share of the partnership’s income. Limited partners are typically not subject to self-employment tax unless they actively participate in the business.

- Qualified Business Income (QBI) Deduction: Partners may be eligible for the QBI deduction, which allows them to deduct up to 20% of their qualified business income.

10.3. Strategic Tax Planning in Partnerships

Effective tax planning within a partnership can help minimize overall tax liability.

Strategies for Tax Planning:

- Partnership Agreement: A well-drafted partnership agreement can allocate income, losses, and deductions in a way that minimizes taxes for the partners.

- Asset Allocation: Strategically allocating assets among partners can optimize tax benefits.

- Timing of Income and Expenses: Carefully timing income and expenses can help manage tax liability.

- Retirement Planning: Utilizing retirement plans like SEP IRAs or SIMPLE IRAs can provide tax advantages for partners.

10.4. How Income-Partners.Net Can Help

Income-partners.net offers resources and opportunities to explore strategic partnerships that can optimize your financial situation and reduce your taxable income. By connecting with the right partners, you can leverage collective expertise and resources to achieve greater financial success.

Are you ready to explore new partnership opportunities and take control of your financial future? Visit income-partners.net today to discover how strategic collaborations can help you minimize your taxable income and maximize your earning potential.

FAQ: Determining Taxable Income

1. How is taxable income different from gross income?

Taxable income is the amount of income subject to tax after deductions and exemptions, while gross income is the total income earned before any deductions or exemptions are applied.

2. What are above-the-line deductions?

Above-the-line deductions are subtractions from your gross income that reduce your adjusted gross income (AGI), such as contributions to traditional IRAs, student loan interest, and health savings account (HSA) contributions.

3. What is adjusted gross income (AGI)?

Adjusted Gross Income (AGI) is your gross income minus above-the-line deductions, and it is a crucial figure in determining eligibility for certain tax credits and deductions.

4. What is the standard deduction?

The standard deduction is a fixed dollar amount that reduces your taxable income, and it varies based on your filing status, providing simplicity and time-saving benefits.

5. What are itemized deductions?

Itemized deductions are specific expenses that you can deduct from your AGI, including medical expenses, state and local taxes (SALT), home mortgage interest, and charitable contributions.

6. How do I choose between the standard deduction and itemized deductions?

Choose the option that results in the lower taxable income by comparing the total of your itemized deductions to the standard deduction for your filing status.

7. What are some common business deductions for the self-employed?

Common business deductions include the home office deduction, business vehicle expenses, supplies and equipment, advertising and marketing costs, and professional fees.

8. What types of income are considered nontaxable?

Nontaxable income includes life insurance payouts, gifts and inheritances, qualified Roth IRA distributions, health savings account (HSA) withdrawals, and certain scholarship and grant amounts.

9. How can I minimize my taxable income through tax planning strategies?

You can minimize your taxable income by maximizing retirement contributions, taking advantage of all available deductions, utilizing tax-advantaged accounts, and implementing strategic charitable giving and investment strategies.

10. How can income-partners.net help me with tax planning and partnership opportunities?

income-partners.net provides resources and opportunities to explore strategic partnerships that can optimize your financial situation, reduce your taxable income, and connect you with valuable business collaborations.