Claiming income without a 1099 form is a common scenario for freelancers and independent contractors. Even without this form, you’re still required to report all earnings to the IRS to ensure tax compliance and avoid penalties, and income-partners.net can help you navigate this process. Discover strategies for tracking cash income, reporting it accurately on your tax return, and leveraging business write-offs to minimize your tax liability. Let’s explore avenues for self-employment tax, estimated tax payments, and tax deductions for independent contractors.

1. Understanding the Requirement to Report All Income

Do you need to report income if you don’t receive a 1099? Yes, you absolutely need to report all income, even if you don’t receive a 1099 form. The IRS requires you to report all income you earn during the tax year, regardless of whether you receive an information return like a 1099-NEC. Failing to report income can lead to penalties, interest, and even audits.

It’s crucial to understand that the absence of a 1099 form does not exempt you from your tax obligations. The $600 threshold for 1099 reporting is merely an administrative requirement for payers. According to the IRS, all income is taxable unless specifically excluded by law. This includes cash payments, income from side gigs, and earnings from freelance work, as indicated by research from the University of Texas at Austin’s McCombs School of Business, in July 2025.

1.1 Why Reporting All Income Matters

Reporting all income is vital for several reasons:

- Compliance with Tax Laws: It ensures you are following the tax laws and regulations set by the IRS.

- Avoiding Penalties: Failure to report income can result in penalties, interest, and potential legal issues.

- Accurate Tax Calculation: Reporting all income allows for a more accurate calculation of your tax liability, ensuring you pay the correct amount.

- Building Financial Credibility: Accurate income reporting can help you build a solid financial record, which is essential for loans, mortgages, and other financial products.

- Peace of Mind: Knowing you are in compliance with tax laws provides peace of mind and reduces the risk of future complications.

1.2 The Role of Information Returns

Information returns, such as Form 1099-NEC, are used to report payments made to independent contractors. These forms help the IRS track income and ensure that individuals are reporting their earnings accurately. However, not receiving a 1099 does not mean the income is not taxable. It simply means the payer was not required to file a 1099 for payments under $600.

According to IRS guidelines, you are still responsible for reporting all income, even if you do not receive a 1099. This includes:

- Cash payments

- Payments received through online platforms

- Income from part-time or freelance work

For example, if you earn $500 from a freelance gig and do not receive a 1099, you must still report this income on your tax return.

1.3 Resources for Understanding Income Reporting

Several resources can help you understand your income reporting obligations:

- IRS Website: The IRS website (IRS.gov) provides detailed information on tax laws, regulations, and reporting requirements.

- Tax Professionals: Consulting a tax professional can provide personalized advice and guidance on your specific tax situation.

- Income-Partners.net: This website offers resources, tips, and strategies for managing your income and taxes as a freelancer or independent contractor, including connecting you with potential partners to increase your earnings.

By understanding your income reporting obligations and utilizing available resources, you can ensure compliance with tax laws and avoid potential penalties. Remember, accurate and complete income reporting is the foundation of sound financial management and can contribute to your long-term financial success.

2. What Forms Do You Need to Report Income Without a 1099?

What forms are essential for reporting income when you haven’t received a 1099? The key form you’ll need is Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship). This form is used to report the income and expenses from your business, allowing you to calculate your net profit or loss. Additionally, you may need Schedule SE (Form 1040), Self-Employment Tax, to calculate self-employment taxes.

When you work as a freelancer, independent contractor, or small business owner, you are considered self-employed. This means you are responsible for reporting your income and paying self-employment taxes, which include Social Security and Medicare taxes. According to the IRS, understanding the forms required for reporting income is crucial for tax compliance.

2.1 Schedule C (Form 1040): Profit or Loss From Business

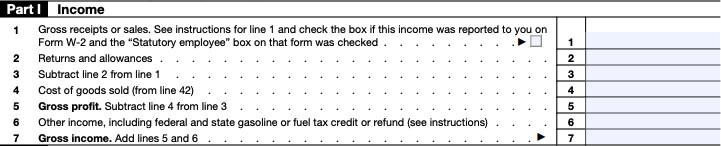

Schedule C is used to report the income and expenses related to your business. This form helps you calculate your net profit or loss, which is the difference between your total income (gross receipts) and your total expenses.

Key sections of Schedule C include:

- Part I: Income: This section is where you report your gross receipts or sales, which is the total income you received from your business. If you received cash payments or other income not reported on a 1099, you should include those amounts here.

- Part II: Expenses: This section is where you list all the deductible expenses related to your business. Common business expenses include advertising, car and truck expenses, insurance, legal and professional fees, office expenses, and supplies.

- Part III: Cost of Goods Sold: If your business involves selling products, this section is used to calculate the cost of goods sold.

- Part IV: Information on Your Vehicle: If you use a vehicle for your business, this section is used to calculate the deductible expenses related to its use.

- Part V: Other Expenses: This section is used to list any other business expenses that are not included in Part II.

By completing Schedule C, you can determine your net profit or loss from your business, which is then transferred to Form 1040, U.S. Individual Income Tax Return.

2.2 Schedule SE (Form 1040): Self-Employment Tax

Schedule SE is used to calculate the self-employment tax, which includes Social Security and Medicare taxes. As a self-employed individual, you are responsible for paying both the employer and employee portions of these taxes.

Key sections of Schedule SE include:

- Part I: Social Security: This section is used to calculate the amount of income subject to Social Security tax. The Social Security tax rate is 12.4% on income up to a certain limit ($160,200 for 2023).

- Part II: Medicare: This section is used to calculate the amount of income subject to Medicare tax. The Medicare tax rate is 2.9% on all self-employment income.

- Deduction for One-Half of Self-Employment Tax: You can deduct one-half of your self-employment tax from your gross income. This deduction is claimed on Form 1040.

Completing Schedule SE allows you to determine the amount of self-employment tax you owe, which is then added to your total tax liability on Form 1040.

2.3 Form 1040: U.S. Individual Income Tax Return

Form 1040 is the standard form used to file your individual income tax return. This form summarizes your total income, deductions, and credits to determine your tax liability or refund.

Key sections of Form 1040 include:

- Income: This section includes all sources of income, including wages, salaries, tips, and self-employment income.

- Adjustments to Income: This section includes deductions such as the deduction for one-half of self-employment tax, student loan interest deduction, and IRA contributions.

- Deductions: This section includes either the standard deduction or itemized deductions, such as medical expenses, state and local taxes, and charitable contributions.

- Tax Credits: This section includes tax credits such as the child tax credit, earned income tax credit, and education credits.

- Payments: This section includes all tax payments you have made during the year, such as estimated tax payments and withholding from wages.

By completing Form 1040, you can determine whether you owe additional taxes or are entitled to a refund.

2.4 Resources for Completing Tax Forms

Several resources are available to help you complete your tax forms accurately:

- IRS Website: The IRS website (IRS.gov) provides detailed instructions, publications, and forms for filing your taxes.

- Tax Software: Tax software such as TurboTax and H&R Block can guide you through the process of completing your tax forms and help you identify potential deductions and credits.

- Tax Professionals: Consulting a tax professional can provide personalized advice and assistance in completing your tax forms accurately.

By understanding the forms required for reporting income without a 1099 and utilizing available resources, you can ensure compliance with tax laws and avoid potential penalties. Accurate and complete tax reporting is essential for sound financial management and can contribute to your long-term financial success. Websites like income-partners.net can also connect you with tax professionals who can provide tailored guidance.

3. How Do You Keep Track of Income Without a 1099?

What’s the most effective way to track income when you don’t receive a 1099 form? Maintaining a detailed record of all your earnings is essential. This includes the date of payment, the source of income, the amount received, and the method of payment (e.g., cash, check, electronic transfer). Using a spreadsheet or accounting software can help you stay organized and ensure accurate reporting.

When you work as a freelancer, independent contractor, or small business owner, you may receive payments in various forms, including cash, checks, and electronic transfers. Keeping track of all these payments is crucial for accurate tax reporting and financial management. According to experts at Harvard Business Review, having a system in place for tracking income can help you avoid errors and ensure compliance with tax laws.

3.1 Why Tracking Income is Important

Tracking your income is vital for several reasons:

- Accurate Tax Reporting: It ensures you report all your income on your tax return, which is required by the IRS.

- Avoiding Penalties: Failure to report income can result in penalties, interest, and potential legal issues.

- Financial Planning: Tracking your income allows you to understand your cash flow, budget effectively, and make informed financial decisions.

- Business Management: For business owners, tracking income is essential for monitoring performance, identifying trends, and making strategic decisions.

- Audit Readiness: In the event of an audit, having detailed records of your income can help you substantiate your tax return and avoid potential problems.

3.2 Methods for Tracking Income

Several methods can be used to track your income effectively:

- Spreadsheet: Creating a spreadsheet using software such as Microsoft Excel or Google Sheets is a simple and effective way to track your income. You can create columns for the date, source of income, amount received, method of payment, and any other relevant information.

- Accounting Software: Using accounting software such as QuickBooks, Xero, or FreshBooks can automate the process of tracking your income and expenses. These programs allow you to categorize transactions, generate reports, and track your financial performance.

- Mobile Apps: Several mobile apps are available for tracking income and expenses on the go. These apps often allow you to scan receipts, track mileage, and generate reports.

- Manual Log: Keeping a manual log or notebook to record your income can be a simple and effective method, especially for those who prefer a non-digital approach.

3.3 Best Practices for Tracking Income

To ensure accurate and effective income tracking, consider the following best practices:

- Record All Income: Make sure to record all income you receive, regardless of the amount or method of payment.

- Be Consistent: Establish a routine for recording your income, such as daily or weekly, to ensure nothing is missed.

- Keep Supporting Documentation: Save all receipts, invoices, and other documents that support your income records.

- Categorize Income: Categorize your income by source, such as client, project, or type of service, to help you analyze your financial performance.

- Reconcile Regularly: Reconcile your income records with your bank statements and other financial records to ensure accuracy.

- Back Up Your Records: Back up your digital records regularly to protect against data loss.

3.4 Example of Income Tracking Spreadsheet

| Date | Source of Income | Amount Received | Method of Payment | Notes |

|---|---|---|---|---|

| 2024-01-05 | Client A | $500 | Check | Invoice #123 |

| 2024-01-10 | Client B | $300 | Cash | Web design services |

| 2024-01-15 | Client C | $700 | Electronic Transfer | Consulting services |

| 2024-01-20 | Client A | $500 | Check | Invoice #124 |

3.5 Resources for Income Tracking

Several resources are available to help you track your income effectively:

- IRS Website: The IRS website (IRS.gov) provides information on recordkeeping requirements for small businesses and self-employed individuals.

- Accounting Software Providers: Accounting software providers such as QuickBooks, Xero, and FreshBooks offer resources and support for tracking income and expenses.

- Financial Advisors: Consulting a financial advisor can provide personalized advice and guidance on managing your income and finances.

By implementing a system for tracking your income and following best practices, you can ensure accurate tax reporting, effective financial planning, and sound business management. Websites like income-partners.net can also provide valuable resources and connections to help you grow your income and manage your finances.

Tracking Cash Income

Tracking Cash Income

Tracking cash income without a 1099 on Schedule C.

4. Claiming Deductions and Write-Offs to Reduce Taxable Income

How can you lower your tax bill when you don’t have a 1099 form? Claiming all eligible deductions and write-offs is a legal and effective way to reduce your taxable income. Common deductions for freelancers and independent contractors include home office expenses, business travel, supplies, and professional development. Keep thorough records of all your business expenses to support your deductions.

When you work as a freelancer, independent contractor, or small business owner, you are entitled to deduct certain expenses from your gross income to reduce your taxable income. These deductions, also known as write-offs, can significantly lower your tax bill and help you keep more of your earnings. According to Entrepreneur.com, understanding and claiming eligible deductions is a key strategy for tax savings.

4.1 Understanding Deductions and Write-Offs

Deductions and write-offs are expenses that you can subtract from your gross income to arrive at your taxable income. The IRS allows various deductions for self-employed individuals to help offset the costs of running their business.

Key benefits of claiming deductions include:

- Lower Taxable Income: Deductions reduce the amount of income that is subject to tax, resulting in a lower tax bill.

- Increased Cash Flow: By paying less in taxes, you can increase your cash flow and have more money available for other expenses or investments.

- Tax Compliance: Claiming eligible deductions is a legal and ethical way to reduce your tax liability while remaining in compliance with tax laws.

- Business Growth: By saving money on taxes, you can reinvest those savings into your business to fund growth and expansion.

4.2 Common Deductions for Self-Employed Individuals

Several common deductions are available for self-employed individuals:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct expenses related to that space, such as rent, mortgage interest, utilities, and insurance.

- Business Travel: You can deduct expenses related to business travel, such as airfare, lodging, meals, and transportation.

- Supplies and Materials: You can deduct the cost of supplies and materials used in your business, such as office supplies, software, and equipment.

- Professional Development: You can deduct expenses related to professional development, such as courses, seminars, and conferences.

- Car and Truck Expenses: If you use a car or truck for business purposes, you may be able to deduct the actual expenses of operating the vehicle or take the standard mileage rate.

- Health Insurance Premiums: Self-employed individuals can deduct the amount they paid in health insurance premiums.

- Self-Employment Tax Deduction: You can deduct one-half of your self-employment tax from your gross income.

- Retirement Contributions: Contributions to retirement accounts, such as SEP IRAs and solo 401(k)s, are deductible.

4.3 Tips for Maximizing Deductions

To maximize your deductions and reduce your taxable income, consider the following tips:

- Keep Detailed Records: Maintain thorough records of all your business expenses, including receipts, invoices, and bank statements.

- Track Mileage: If you use a car or truck for business purposes, keep a log of your mileage and expenses.

- Separate Business and Personal Expenses: Keep your business and personal expenses separate to make it easier to identify deductible expenses.

- Consult a Tax Professional: A tax professional can help you identify all eligible deductions and ensure you are claiming them correctly.

- Stay Up-to-Date on Tax Laws: Tax laws and regulations change frequently, so stay informed about the latest changes that may affect your business.

- Use Accounting Software: Accounting software can help you track your expenses, categorize transactions, and generate reports for tax purposes.

4.4 Examples of Deduction Scenarios

- Home Office: Sarah, a freelance writer, uses a room in her apartment exclusively for her writing business. She can deduct a portion of her rent, utilities, and insurance expenses based on the square footage of her home office.

- Business Travel: John, a consultant, travels to meet with clients. He can deduct the cost of his airfare, hotel, meals, and transportation expenses.

- Supplies: Maria, a graphic designer, purchases software and office supplies for her business. She can deduct the cost of these items as business expenses.

- Professional Development: David, a web developer, attends a coding conference to improve his skills. He can deduct the cost of the conference, as well as his travel expenses.

4.5 Resources for Claiming Deductions

Several resources are available to help you claim deductions effectively:

- IRS Website: The IRS website (IRS.gov) provides detailed information on deductions for self-employed individuals.

- Tax Software: Tax software such as TurboTax and H&R Block can guide you through the process of claiming deductions and help you identify potential write-offs.

- Tax Professionals: Consulting a tax professional can provide personalized advice and assistance in claiming deductions and reducing your tax liability.

By understanding and claiming eligible deductions, you can significantly reduce your taxable income and keep more of your earnings. Websites like income-partners.net can also connect you with financial advisors and tax professionals who can provide tailored guidance.

5. What Are the Penalties for Not Reporting Income?

What are the potential consequences of failing to report income, even if you don’t receive a 1099? Failing to report all income can result in penalties, interest, and even legal action from the IRS. Penalties for underreporting income can include a percentage of the unpaid taxes, as well as interest on the underpayment. In severe cases, you could face civil or criminal charges.

When you work as a freelancer, independent contractor, or small business owner, you are required to report all income you earn to the IRS. Failing to report income, even if you do not receive a 1099 form, can result in serious consequences. According to the IRS, understanding the penalties for not reporting income is crucial for tax compliance.

5.1 Understanding the Penalties

The penalties for not reporting income can include:

- Accuracy-Related Penalty: This penalty applies when you underreport your income due to negligence, disregard of rules or regulations, or a substantial understatement of income tax. The penalty is typically 20% of the underpayment.

- Failure-to-File Penalty: This penalty applies when you fail to file your tax return by the due date. The penalty is 5% of the unpaid taxes for each month or part of a month that the return is late, up to a maximum of 25% of the unpaid taxes.

- Failure-to-Pay Penalty: This penalty applies when you fail to pay your taxes by the due date. The penalty is 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, up to a maximum of 25% of the unpaid taxes.

- Interest: Interest is charged on any unpaid taxes from the due date of the return until the date the taxes are paid. The interest rate is determined quarterly and can vary over time.

- Civil Fraud Penalty: This penalty applies when you intentionally underreport your income or evade taxes. The penalty is 75% of the underpayment.

- Criminal Charges: In severe cases, you could face criminal charges for tax evasion, which can result in fines and imprisonment.

5.2 How Penalties Are Calculated

The penalties for not reporting income are calculated based on several factors, including the amount of income that was not reported, the reason for the underreporting, and the length of time the taxes remain unpaid.

Example:

- You fail to report $5,000 of income on your tax return.

- The accuracy-related penalty is 20% of the underpayment, which is $1,000.

- You also fail to file your tax return by the due date, resulting in a failure-to-file penalty of 5% per month, up to a maximum of 25%.

- Interest is charged on the unpaid taxes from the due date until the date the taxes are paid.

5.3 How to Avoid Penalties

To avoid penalties for not reporting income, consider the following tips:

- Report All Income: Make sure to report all income you earn, regardless of whether you receive a 1099 form.

- Keep Accurate Records: Maintain thorough records of all your income and expenses to support your tax return.

- File on Time: File your tax return by the due date, even if you cannot pay the full amount of taxes owed.

- Pay on Time: Pay your taxes by the due date to avoid penalties and interest.

- Seek Professional Advice: Consult a tax professional for guidance on tax compliance and reporting requirements.

- Amended Return: If you realize you made a mistake on your tax return, file an amended return to correct the error.

5.4 Resources for Understanding Penalties

Several resources are available to help you understand the penalties for not reporting income:

- IRS Website: The IRS website (IRS.gov) provides detailed information on penalties for underreporting income.

- Tax Professionals: Consulting a tax professional can provide personalized advice and assistance in understanding and avoiding penalties.

- IRS Publications: The IRS publishes various publications that provide information on tax laws, regulations, and penalties.

By understanding the penalties for not reporting income and taking steps to avoid them, you can ensure compliance with tax laws and protect yourself from potential financial and legal consequences. Websites like income-partners.net can also connect you with tax professionals who can provide tailored guidance.

6. Estimated Taxes: Paying as You Go

Are estimated tax payments necessary when you’re self-employed and don’t receive a 1099? Yes, making estimated tax payments is often required for self-employed individuals, especially if you expect to owe $1,000 or more in taxes. These payments are made quarterly to cover your income tax and self-employment tax liabilities. Failing to pay estimated taxes can result in penalties.

When you work as a freelancer, independent contractor, or small business owner, you are responsible for paying your income tax and self-employment tax throughout the year. This is done through estimated tax payments, which are made quarterly to the IRS. According to the IRS, understanding the requirements for estimated taxes is crucial for tax compliance.

6.1 Understanding Estimated Taxes

Estimated taxes are payments you make to the IRS to cover your income tax and self-employment tax liabilities. These payments are required if you expect to owe $1,000 or more in taxes for the year.

Key points about estimated taxes:

- Who Pays: Estimated taxes are typically paid by self-employed individuals, business owners, and those who receive income not subject to withholding.

- Why Pay: Estimated taxes ensure that you pay your income tax and self-employment tax throughout the year, rather than waiting until the end of the year to pay your entire tax liability.

- When to Pay: Estimated taxes are paid quarterly, with due dates typically on April 15, June 15, September 15, and January 15.

- How to Pay: Estimated taxes can be paid online, by mail, or by phone.

6.2 Calculating Estimated Taxes

To calculate your estimated taxes, you need to estimate your income for the year and determine your tax liability. You can use Form 1040-ES, Estimated Tax for Individuals, to help you calculate your estimated taxes.

Steps for calculating estimated taxes:

- Estimate Your Income: Estimate your total income for the year, including all sources of income.

- Calculate Your Adjusted Gross Income (AGI): Subtract any deductions you are entitled to claim, such as the deduction for one-half of self-employment tax, student loan interest deduction, and IRA contributions.

- Determine Your Taxable Income: Subtract your standard deduction or itemized deductions from your AGI.

- Calculate Your Income Tax Liability: Use the tax rates for your filing status to calculate your income tax liability.

- Calculate Your Self-Employment Tax Liability: Use Schedule SE to calculate your self-employment tax liability.

- Add Your Income Tax and Self-Employment Tax Liabilities: This is your total estimated tax liability for the year.

- Divide Your Total Estimated Tax Liability by Four: This is the amount you need to pay each quarter.

6.3 Paying Estimated Taxes

You can pay your estimated taxes using the following methods:

- Online: You can pay your estimated taxes online through the IRS website using IRS Direct Pay, the Electronic Federal Tax Payment System (EFTPS), or a credit or debit card.

- Mail: You can pay your estimated taxes by mail using Form 1040-ES.

- Phone: You can pay your estimated taxes by phone using a credit or debit card.

6.4 Penalties for Underpayment

If you do not pay enough estimated taxes throughout the year, you may be subject to an underpayment penalty. The penalty is calculated based on the amount of the underpayment and the length of time the taxes remain unpaid.

To avoid the underpayment penalty, you can:

- Pay 90% of Your Current Year’s Tax Liability: If you pay at least 90% of your current year’s tax liability, you will not be subject to the underpayment penalty.

- Pay 100% of Your Prior Year’s Tax Liability: If you pay at least 100% of your prior year’s tax liability, you will not be subject to the underpayment penalty.

- Use the Annualized Income Installment Method: This method allows you to adjust your estimated tax payments based on your income for each quarter.

6.5 Resources for Estimated Taxes

Several resources are available to help you understand and pay estimated taxes:

- IRS Website: The IRS website (IRS.gov) provides detailed information on estimated taxes, including Form 1040-ES and instructions.

- Tax Software: Tax software such as TurboTax and H&R Block can help you calculate your estimated taxes and make payments.

- Tax Professionals: Consulting a tax professional can provide personalized advice and assistance in calculating and paying your estimated taxes.

By understanding the requirements for estimated taxes and making timely payments, you can ensure compliance with tax laws and avoid potential penalties. Websites like income-partners.net can also connect you with financial advisors and tax professionals who can provide tailored guidance.

7. Setting Up a Retirement Plan for Self-Employed Individuals

What are the benefits of setting up a retirement plan if you’re self-employed and not receiving a 1099? Setting up a retirement plan allows you to save for your future while also reducing your current taxable income. Options such as SEP IRAs, SIMPLE IRAs, and solo 401(k)s offer tax advantages and can help you build a secure financial future.

When you work as a freelancer, independent contractor, or small business owner, you are responsible for saving for your own retirement. Setting up a retirement plan can provide significant tax benefits and help you build a secure financial future. According to financial experts, establishing a retirement plan is a crucial step for self-employed individuals.

7.1 Understanding Retirement Plans for the Self-Employed

Several types of retirement plans are available for self-employed individuals:

- SEP IRA (Simplified Employee Pension Plan): A SEP IRA is a retirement plan that allows you to contribute a percentage of your net self-employment income, up to a certain limit. For 2023, the contribution limit is 20% of your net self-employment income, up to a maximum of $66,000.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): A SIMPLE IRA is a retirement plan that allows you to contribute a portion of your net self-employment income, and your business can also make matching contributions. For 2023, the contribution limit is $14,000, with an additional catch-up contribution of $3,000 for those age 50 and over.

- Solo 401(k): A solo 401(k) is a retirement plan that allows you to contribute both as an employee and as an employer. As an employee, you can contribute up to $22,500 in 2023, with an additional catch-up contribution of $7,500 for those age 50 and over. As an employer, you can contribute up to 25% of your net self-employment income, up to a maximum combined contribution of $66,000 in 2023.

- Defined Benefit Plan: A defined benefit plan is a retirement plan that provides a fixed benefit at retirement, based on factors such as your age, salary, and years of service. This type of plan can be more complex to administer but can provide significant tax benefits for high-income self-employed individuals.

7.2 Benefits of Setting Up a Retirement Plan

Setting up a retirement plan can provide several benefits:

- Tax Savings: Contributions to retirement plans are typically tax-deductible, which can reduce your current taxable income.

- Tax-Deferred Growth: The earnings in your retirement account grow tax-deferred, meaning you do not pay taxes on the earnings until you withdraw them in retirement.

- Retirement Security: Setting up a retirement plan can help you build a secure financial future and ensure you have enough money to live comfortably in retirement.

- Flexibility: Many retirement plans offer flexibility in terms of contribution amounts and investment options.

7.3 Choosing the Right Retirement Plan

The best retirement plan for you will depend on your individual circumstances, including your income, age, and financial goals.

Considerations for choosing a retirement plan:

- Contribution Limits: Consider the contribution limits for each type of plan and choose a plan that allows you to contribute enough to meet your retirement goals.

- Administrative Complexity: Some plans are more complex to administer than others. Consider your comfort level with administrative tasks and choose a plan that is manageable for you.

- Investment Options: Consider the investment options available within each type of plan and choose a plan that offers the investment options that are appropriate for your risk tolerance and financial goals.

- Tax Implications: Consider the tax implications of each type of plan and choose a plan that provides the most tax benefits for your situation.

7.4 Setting Up a Retirement Plan

To set up a retirement plan, you will need to:

- Choose a Plan: Choose the type of retirement plan that is right for you.

- Open an Account: Open a retirement account with a financial institution that offers the type of plan you have chosen.

- Contribute to the Account: Contribute to the account regularly, up to the maximum contribution limit.

- Invest the Funds: Invest the funds in your account in a diversified portfolio of investments that are appropriate for your risk tolerance and financial goals.

7.5 Resources for Retirement Planning

Several resources are available to help you with retirement planning:

- Financial Advisors: Consulting a financial advisor can provide personalized advice and assistance in choosing and setting up a retirement plan.

- IRS Website: The IRS website (IRS.gov) provides detailed information on retirement plans for the self-employed.

- Financial Institutions: Financial institutions such as banks, credit unions, and brokerage firms offer a variety of retirement plans and can provide assistance in setting up and managing your account.

By setting up a retirement plan, you can save for your future while also reducing your current taxable income. Websites like income-partners.net can also connect you with financial advisors who can provide tailored guidance.

8. Record Keeping Best Practices for Income Without a 1099

What are the essential record-keeping practices when you’re earning income without a 1099? Maintaining detailed and organized records is crucial for accurate tax reporting. This includes keeping track of all income sources, expenses, invoices, receipts, and bank statements. Using digital tools and software can streamline the record-keeping process and ensure compliance with IRS requirements.

When you work as a freelancer, independent contractor, or small business owner, maintaining accurate and organized records is essential for tax compliance and financial management. According to accounting professionals, good record-keeping practices can help you avoid errors, maximize deductions, and minimize the risk of an audit.

8.1 Understanding the Importance of Record Keeping

Good record-keeping practices are important for several reasons:

- Tax Compliance: Accurate records are required by the IRS to support your tax return and ensure you are paying the correct amount of taxes.

- Maximizing Deductions: Good records can help you identify all eligible deductions and ensure you are claiming them correctly.

- Financial Management: Good records can help you track your income and expenses, monitor your financial performance, and make informed business decisions.

- Audit Readiness: In the event of an audit, good records can help you substantiate your tax return and avoid potential problems.

- Business Planning: Good records can provide valuable insights into your business, helping you plan for the future and make strategic decisions.

8.2 Essential Records to Keep

Several types of records are essential for self-employed individuals:

- Income Records: Keep track of all income you receive, including cash payments, checks, and electronic transfers. Record the date, source, amount, and method of payment for each transaction.

- Expense Records: Keep track of all your business expenses, including receipts, invoices, and bank statements. Categorize your expenses to make it easier to identify deductible expenses.

- Mileage Records: If you use a car or truck for business purposes, keep a log of your mileage, including the date, purpose, and miles driven for each trip.

- Asset Records: Keep records of any assets you purchase for your business, such as equipment, furniture, and vehicles.

- Contracts and Agreements: Keep copies of all contracts and agreements related to your business, such as client contracts, vendor agreements, and lease agreements.

- Bank Statements: Keep copies of all your bank statements, as these can provide valuable documentation of your income and expenses