How Do You Calculate Operating Income? Operating income, a crucial metric for assessing a company’s core profitability, is calculated by subtracting operating expenses from gross profit; income-partners.net can help you understand this metric and find partners to improve your financial strategies. Understanding operating income is key to identifying profit margins, assessing earnings quality, and improving capital allocation.

1. What is Operating Income and Why Is It Important?

Operating income, often referred to as Earnings Before Interest and Taxes (EBIT), represents the profit a company generates from its core operations. It’s calculated by deducting operating expenses, such as wages, depreciation, and the cost of goods sold (COGS), from gross profit.

1.1 Why Operating Income Matters

- Core Performance: It provides a clear picture of how well a company’s core business is performing, without the noise of financial leverage or tax implications.

- Efficiency Assessment: A rising operating income indicates improved efficiency and profitability in a company’s operations.

- Benchmarking: It allows for easier comparison of operational efficiency across different companies within the same industry.

- Investment Decisions: Investors use operating income to evaluate a company’s ability to generate profits from its operations, making it a key factor in investment decisions.

- Partner Evaluations: For those seeking partners, understanding a potential partner’s operating income can provide valuable insights into their financial health and operational efficiency, as facilitated by resources like income-partners.net.

1.2 Operating Income vs. Net Income

While both operating income and net income are important, they offer different perspectives:

- Operating Income: Focuses solely on the profitability of core business operations.

- Net Income: Represents the total profit after all expenses, including interest, taxes, and other non-operating items, are deducted.

Understanding the difference between these two metrics can provide a more nuanced view of a company’s financial performance. Net income can sometimes be misleading due to one-time gains or losses, whereas operating income gives a steadier view of the company’s ability to consistently profit from its core operations.

2. What is the Standard Operating Income Formula?

The standard formula to calculate operating income is straightforward:

Operating Income = Gross Profit – Operating Expenses

Each component plays a vital role in determining the final figure.

2.1 Breaking Down the Components

- Gross Profit: This is calculated as Revenue (Net Sales) less Cost of Goods Sold (COGS). It represents the profit a company makes after deducting the direct costs associated with producing and selling its products or services.

- Operating Expenses: These include all the costs incurred in running the business, such as salaries, rent, marketing expenses, research and development (R&D), and depreciation.

2.2 Step-by-Step Calculation

- Calculate Gross Profit:

- Gross Profit = Revenue – COGS

- Determine Operating Expenses:

- Add up all expenses related to the company’s operations.

- Calculate Operating Income:

- Operating Income = Gross Profit – Operating Expenses

2.3 Example Calculation

Let’s consider a hypothetical company, Tech Solutions Inc., with the following financials:

- Revenue: $1,000,000

- COGS: $400,000

- Operating Expenses: $300,000

- Gross Profit Calculation:

- Gross Profit = $1,000,000 (Revenue) – $400,000 (COGS) = $600,000

- Operating Income Calculation:

- Operating Income = $600,000 (Gross Profit) – $300,000 (Operating Expenses) = $300,000

Therefore, Tech Solutions Inc.’s operating income is $300,000. This indicates the company’s profitability from its core operations before considering interest and taxes.

Operating Income Formula

Operating Income Formula

2.4 How to Find Reliable Financial Data

To accurately calculate operating income, reliable financial data is essential. Here are some key sources:

- Company Financial Statements: These include the income statement, balance sheet, and cash flow statement, which are typically available on the company’s investor relations website.

- SEC Filings: Public companies in the U.S. are required to file reports with the Securities and Exchange Commission (SEC), such as the 10-K (annual report) and 10-Q (quarterly report). These filings provide detailed financial information.

- Financial News and Data Providers: Services like Bloomberg, Reuters, and Yahoo Finance provide financial data, news, and analysis on companies.

- Audited Reports: Always prioritize data from audited financial statements, as these have been reviewed by independent auditors and are more likely to be accurate.

By using reliable data sources, you can ensure that your calculations of operating income are accurate and meaningful.

3. What is Included and Excluded in Operating Income?

Understanding what is included and excluded in operating income is essential for accurate analysis. Operating income focuses on the core operational profitability of a company.

3.1 Items Included in Operating Income

- Revenue: The income generated from the company’s primary business activities, such as sales of goods or services.

- Cost of Goods Sold (COGS): The direct costs associated with producing goods or services, including raw materials, direct labor, and manufacturing overhead.

- Operating Expenses: Costs incurred to support the company’s operations, including:

- Salaries and Wages: Compensation paid to employees.

- Rent: Payments for office or facility space.

- Utilities: Expenses for electricity, water, and other utilities.

- Marketing and Advertising: Costs associated with promoting the company’s products or services.

- Research and Development (R&D): Expenses for developing new products or improving existing ones.

- Depreciation and Amortization: Allocation of the cost of assets over their useful lives.

- Administrative Expenses: Costs related to managing the company, such as office supplies and administrative salaries.

3.2 Items Excluded from Operating Income

- Interest Income and Expense: Income earned on investments and expenses incurred on debt are excluded because they are related to financing activities, not core operations.

- Gains and Losses on Investments: Profits or losses from the sale of investments are not part of the company’s regular business activities.

- Income Tax Expense: Taxes are excluded to provide a clear picture of profitability before taxes, allowing for easier comparison between companies in different tax jurisdictions.

- One-Time or Non-Recurring Items: These include gains or losses from the sale of assets, restructuring costs, and other unusual items that are not part of the company’s normal operations.

3.3 Examples of Items and Their Treatment

| Item | Included in Operating Income? | Reason |

|---|---|---|

| Revenue | Yes | Represents income from core business activities. |

| Cost of Goods Sold (COGS) | Yes | Direct costs associated with producing goods or services. |

| Salaries and Wages | Yes | Compensation for employees directly involved in operations. |

| Rent | Yes | Cost of facility space used for operations. |

| Interest Expense | No | Related to financing activities, not core operations. |

| Gains on Investment Sales | No | Not part of the company’s regular business activities. |

| Income Tax Expense | No | Excluded to show profitability before taxes. |

| Restructuring Costs | No | Non-recurring item not part of normal operations. |

| Depreciation | Yes | Allocation of asset costs over time, representing wear and tear on operational assets. |

| Marketing Expenses | Yes | Costs incurred to promote and sell products or services, directly supporting revenue generation. |

| Research & Development | Yes | Expenses related to creating new products or improving existing ones, essential for long-term operational success. |

| Administrative Expenses | Yes | Costs for managing the company’s operations, such as office supplies and administrative salaries, necessary for supporting core activities. |

| Utilities | Yes | Essential expenses for running the business, directly supporting operational activities. |

| Losses on Asset Sales | No | Unusual items not part of normal operations. |

| Legal Settlements | No | Typically non-recurring and unrelated to core business activities. |

| Foreign Exchange Gains/Losses | No | These relate to currency fluctuations, not the core business operations. |

3.4 Impact of Misclassifying Items

Misclassifying items can significantly distort operating income, leading to inaccurate financial analysis. For example:

- Including Interest Expense: Overstates operating expenses, understating operating income.

- Excluding Depreciation: Overstates operating income, masking the true costs of using assets.

Investors and analysts must carefully review financial statements to ensure items are correctly classified for an accurate assessment of operational profitability.

4. How to Calculate Operating Income Margin?

The operating income margin is a profitability ratio that measures how much profit a company makes from its operations, relative to its total revenue. It’s a key indicator of operational efficiency and profitability.

4.1 Formula for Operating Income Margin

The formula is:

Operating Income Margin = (Operating Income / Revenue) x 100%

This ratio is expressed as a percentage, making it easy to compare companies of different sizes.

4.2 Steps to Calculate Operating Income Margin

- Determine Operating Income: Calculate operating income using the formula: Gross Profit – Operating Expenses.

- Identify Revenue: Find the total revenue from the company’s income statement.

- Apply the Formula: Divide operating income by revenue and multiply by 100 to get the margin as a percentage.

4.3 Example Calculation

Using the previous example of Tech Solutions Inc.:

- Operating Income: $300,000

- Revenue: $1,000,000

- Operating Income Margin Calculation:

- Operating Income Margin = ($300,000 / $1,000,000) x 100% = 30%

This means Tech Solutions Inc. earns 30 cents of operating income for every dollar of revenue.

4.4 Interpreting the Operating Income Margin

- High Margin: Indicates the company is efficient at controlling costs and generating profit from operations.

- Low Margin: Suggests the company may have high operating expenses or low pricing power.

- Trend Analysis: Tracking the margin over time can reveal whether the company’s operational efficiency is improving or declining.

- Industry Comparison: Compare the margin to industry peers to assess the company’s relative performance.

4.5 Benchmarking and Industry Standards

Operating income margins vary widely by industry:

- Software Companies: Often have high margins due to low COGS and scalable business models.

- Retail Companies: Typically have lower margins due to high COGS and competitive pricing.

- Manufacturing Companies: Margins can vary depending on production efficiency and raw material costs.

According to research from New York University’s Stern School of Business, the average operating margin across all industries varies significantly, but a margin above 10% is generally considered healthy.

4.6 Using Operating Margin for Partnership Evaluations

For those considering business partnerships, the operating income margin is a critical metric. A partner with a consistently high operating margin is likely more financially stable and efficient. Resources like income-partners.net can help you assess potential partners’ financial health and make informed decisions.

5. What Factors Affect Operating Income?

Several factors can influence a company’s operating income, both internal and external.

5.1 Internal Factors

- Cost Management: Efficient cost control can significantly improve operating income.

- Pricing Strategy: Setting optimal prices can maximize revenue and profitability.

- Operational Efficiency: Streamlining operations and reducing waste can lower expenses.

- Product Mix: Selling higher-margin products can boost operating income.

- Research and Development (R&D): Successful R&D can lead to innovative products and increased revenue, but high R&D spending can also temporarily lower operating income.

- Sales and Marketing Effectiveness: Effective sales and marketing efforts can increase revenue and market share.

- Supply Chain Management: A well-managed supply chain can reduce costs and ensure timely delivery of products.

5.2 External Factors

- Economic Conditions: Economic growth or recession can impact consumer demand and sales.

- Competition: Intense competition can pressure prices and margins.

- Industry Trends: Changes in technology, consumer preferences, and regulations can affect a company’s operations.

- Raw Material Prices: Fluctuations in raw material prices can impact COGS and profitability.

- Regulatory Environment: Changes in regulations can increase compliance costs and affect operations.

- Exchange Rates: Currency fluctuations can impact revenue and expenses for companies operating internationally.

5.3 Impact of Strategic Decisions

Strategic decisions made by management can have a significant impact on operating income:

- Investments in Technology: Can improve efficiency and lower costs but may require significant upfront investment.

- Expansion into New Markets: Can increase revenue but also increase operating expenses.

- Mergers and Acquisitions (M&A): Can create synergies and increase market share but also involve integration costs.

- Restructuring: Can streamline operations and reduce costs but may involve severance payments and other restructuring charges.

5.4 How External Events Can Shift Operating Income

External events can dramatically shift operating income.

- Pandemics: The COVID-19 pandemic significantly impacted many businesses, with some industries experiencing increased demand (e.g., e-commerce) and others facing severe declines (e.g., hospitality).

- Geopolitical Events: Trade wars, political instability, and other geopolitical events can disrupt supply chains, increase costs, and affect revenue.

- Natural Disasters: Hurricanes, earthquakes, and other natural disasters can disrupt operations and damage assets.

5.5 Strategies for Managing These Factors

- Diversification: Diversifying product lines, markets, and supply chains can reduce risk.

- Hedging: Using financial instruments to mitigate the impact of currency fluctuations and commodity price volatility.

- Contingency Planning: Developing plans to address potential disruptions from external events.

- Continuous Improvement: Regularly reviewing and improving processes to enhance efficiency and reduce costs.

- Staying Informed: Monitoring economic conditions, industry trends, and regulatory changes to anticipate and adapt to changes.

6. Common Mistakes in Calculating Operating Income and How to Avoid Them

Calculating operating income accurately is crucial for effective financial analysis. However, several common mistakes can lead to inaccurate results.

6.1 Misclassifying Expenses

- Mistake: Incorrectly classifying expenses as either operating or non-operating.

- Impact: Distorts the true profitability of core business operations.

- How to Avoid: Understand the definitions of operating and non-operating expenses. Refer to accounting standards and guidelines. Consult with accounting professionals if needed.

6.2 Ignoring Non-Recurring Items

- Mistake: Failing to exclude non-recurring items, such as gains or losses from asset sales, from operating income.

- Impact: Makes it difficult to compare operating income across different periods and assess the company’s underlying performance.

- How to Avoid: Carefully review the income statement and footnotes to identify and exclude non-recurring items. Focus on recurring, core business activities.

6.3 Errors in Calculating COGS

- Mistake: Inaccurate calculation of the Cost of Goods Sold (COGS), such as including indirect costs or using incorrect inventory valuation methods.

- Impact: Directly affects gross profit and, consequently, operating income.

- How to Avoid: Ensure accurate tracking of direct costs, such as raw materials and direct labor. Use consistent inventory valuation methods (e.g., FIFO, LIFO, weighted average).

6.4 Overlooking Depreciation and Amortization

- Mistake: Failing to include depreciation and amortization expenses, which represent the allocation of the cost of assets over their useful lives.

- Impact: Overstates operating income, as it doesn’t account for the wearing out of assets used in operations.

- How to Avoid: Accurately calculate and record depreciation and amortization expenses. Use appropriate depreciation methods (e.g., straight-line, accelerated).

6.5 Not Standardizing for Comparison

- Mistake: Not comparing operating income or margin to industry benchmarks or historical data.

- Impact: Fails to provide context for assessing the company’s performance relative to peers or its own track record.

- How to Avoid: Calculate and compare operating income margin to industry averages. Analyze trends in operating income and margin over time.

6.6 Relying on Unverified Data

- Mistake: Using unaudited or unverified financial data.

- Impact: Increases the risk of errors and inaccuracies in the calculation of operating income.

- How to Avoid: Use data from audited financial statements or reliable sources. Verify data from multiple sources if possible.

6.7 Ignoring the Impact of Inflation

- Mistake: Not considering the impact of inflation on revenue and expenses, which can distort operating income.

- Impact: Makes it difficult to compare operating income across different periods, especially during times of high inflation.

- How to Avoid: Adjust financial data for inflation using appropriate price indices. Focus on real (inflation-adjusted) growth rates.

6.8 Common Mistakes and How to Correct Them

| Mistake | Impact | How to Avoid |

|---|---|---|

| Misclassifying Expenses | Distorted profitability of core operations | Understand definitions, refer to standards, consult professionals |

| Ignoring Non-Recurring Items | Difficult comparison across periods | Review income statement, exclude non-recurring items |

| Errors in Calculating COGS | Directly affects gross profit and operating income | Track direct costs, use consistent inventory valuation methods |

| Overlooking Depreciation | Overstated operating income | Accurately calculate and record depreciation |

| Not Standardizing for Comparison | Fails to provide context for performance assessment | Calculate and compare operating margin to industry averages |

| Relying on Unverified Data | Increased risk of errors and inaccuracies | Use data from audited statements, verify data from multiple sources |

| Ignoring Inflation | Difficult comparison across periods, especially during high inflation | Adjust financial data for inflation, focus on real growth rates |

| Not Understanding Lease Accounting | Operating leases can affect how operating expenses are reported | Understand the difference between operating and finance leases, ensure proper accounting treatment under current standards (e.g., IFRS 16 or ASC 842) |

| Using Old Financial Data | Can lead to decisions based on outdated information | Always use the most recent financial statements available, typically quarterly or annually |

7. How to Improve Operating Income?

Improving operating income is a key goal for businesses, as it reflects better operational efficiency and profitability.

7.1 Strategies for Increasing Revenue

- Pricing Optimization: Adjust prices to maximize revenue and profit margins. Conduct market research to understand price sensitivity and competitive pricing.

- Sales and Marketing Initiatives: Invest in effective marketing campaigns, improve sales processes, and enhance customer relationships. Use data analytics to identify target markets and optimize marketing spend.

- Product Innovation: Develop new products and services that meet customer needs and differentiate the company from competitors. Invest in research and development (R&D) to drive innovation.

- Market Expansion: Expand into new geographic markets or customer segments. Conduct market research to assess potential opportunities and risks.

- Strategic Partnerships: Collaborate with other businesses to expand market reach, access new technologies, or share resources.

7.2 Strategies for Reducing Costs

- Cost Control: Implement cost-cutting measures across all areas of the business. Review expenses regularly and identify opportunities to reduce waste and improve efficiency.

- Supply Chain Optimization: Streamline the supply chain to reduce costs and improve delivery times. Negotiate better terms with suppliers and consider alternative sourcing options.

- Operational Efficiency: Improve operational processes to reduce waste, increase productivity, and lower costs. Implement lean manufacturing principles and automation technologies.

- Technology Adoption: Invest in technology solutions that automate tasks, improve efficiency, and reduce labor costs.

- Outsourcing: Outsource non-core activities to specialized providers to reduce costs and improve focus on core competencies.

- Energy Efficiency: Reduce energy consumption to lower utility costs. Implement energy-efficient technologies and practices.

7.3 Using Technology to Enhance Efficiency

- Automation: Automate repetitive tasks and processes to reduce labor costs and improve accuracy.

- Data Analytics: Use data analytics to identify trends, optimize processes, and make better decisions.

- Cloud Computing: Use cloud-based solutions to reduce IT costs and improve scalability.

- Customer Relationship Management (CRM): Implement a CRM system to improve customer relationships, increase sales, and enhance marketing effectiveness.

- Enterprise Resource Planning (ERP): Implement an ERP system to integrate and streamline business processes, improve efficiency, and reduce costs.

7.4 Case Studies of Companies That Improved Operating Income

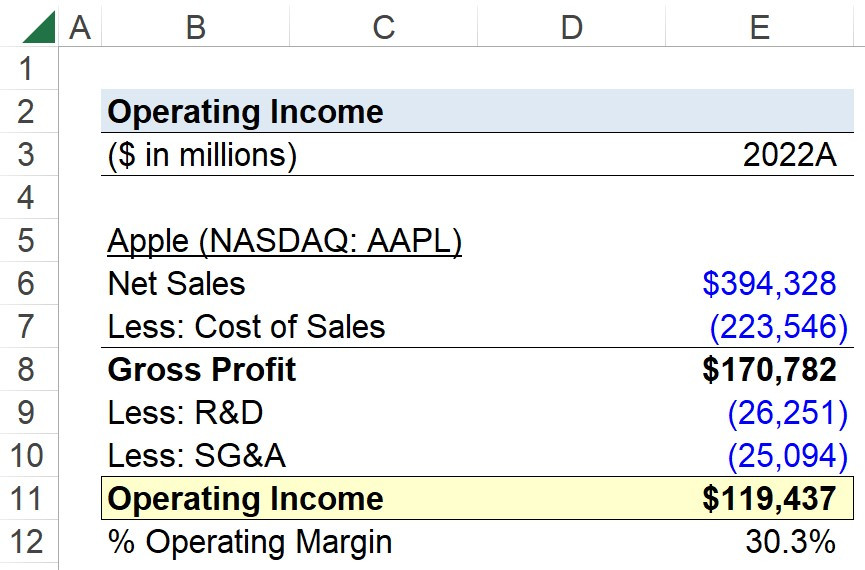

- Apple Inc.: Apple has consistently improved its operating income through product innovation, pricing optimization, and supply chain management.

- Amazon.com Inc.: Amazon has improved its operating income through cost control, operational efficiency, and technology adoption.

- Procter & Gamble Co.: Procter & Gamble has improved its operating income through product innovation, marketing initiatives, and cost-cutting measures.

7.5 How Partnerships Can Enhance Operating Income

Strategic partnerships can significantly enhance operating income by:

- Expanding Market Reach: Partnering with complementary businesses to reach new markets and customer segments.

- Sharing Resources: Sharing resources, such as technology, infrastructure, and expertise, to reduce costs and improve efficiency.

- Accessing New Technologies: Partnering with technology companies to access innovative solutions that improve operations and enhance revenue.

- Improving Supply Chain: Collaborating with suppliers to improve supply chain efficiency and reduce costs.

- Joint Marketing Initiatives: Conducting joint marketing campaigns to increase brand awareness and drive sales.

For companies looking to explore partnership opportunities, platforms like income-partners.net can be invaluable in identifying and connecting with potential partners.

Operating Income Calculator

Operating Income Calculator

8. How Does Operating Income Relate to Business Valuation?

Operating income is a critical component in business valuation because it reflects the profitability of a company’s core operations, independent of financing and accounting decisions.

8.1 Role of Operating Income in Valuation

- Free Cash Flow (FCF) Calculation: Operating income is often used as a starting point for calculating free cash flow, which is a key metric in discounted cash flow (DCF) analysis.

- Earnings Multiple Valuation: Operating income can be used in earnings multiple valuation methods, such as the price-to-operating income ratio.

- Comparison to Peers: Operating income allows for easier comparison of profitability between companies in the same industry, regardless of their capital structure or tax rates.

8.2 Valuation Methods Using Operating Income

- Discounted Cash Flow (DCF) Analysis: In DCF analysis, operating income is used to project future free cash flows, which are then discounted back to their present value to arrive at an estimate of the company’s intrinsic value.

- Earnings Multiple Valuation: Earnings multiple valuation involves comparing a company’s operating income to its market capitalization or enterprise value. Common multiples include price-to-operating income (P/OI) and enterprise value-to-operating income (EV/OI).

- Relative Valuation: Operating income can be used to compare a company’s valuation to that of its peers in the same industry.

8.3 Advantages and Disadvantages

| Valuation Method | Advantages | Disadvantages |

|---|---|---|

| Discounted Cash Flow (DCF) | Comprehensive, forward-looking, considers time value of money | Requires numerous assumptions, sensitive to changes in assumptions, can be complex |

| Earnings Multiple Valuation | Simple, easy to understand, based on market data | May not reflect future growth potential, can be distorted by accounting practices, sensitive to choice of comparable companies |

| Relative Valuation | Provides context for valuation, based on market data | Can be distorted by market conditions, sensitive to choice of comparable companies, may not reflect unique aspects of the company being valued |

8.4 How to Use Operating Income in DCF Analysis

- Project Future Operating Income: Forecast future operating income based on historical data, industry trends, and company-specific factors.

- Calculate Free Cash Flow (FCF): Calculate FCF by adjusting operating income for non-cash expenses (e.g., depreciation), capital expenditures, and changes in working capital.

- Discount FCF to Present Value: Discount the projected FCFs back to their present value using an appropriate discount rate (e.g., weighted average cost of capital).

- Sum Present Values: Sum the present values of the projected FCFs to arrive at an estimate of the company’s intrinsic value.

8.5 How Operating Income Helps Investors

- Assessing Profitability: Operating income provides a clear picture of a company’s core profitability, allowing investors to assess its ability to generate profits from its operations.

- Comparing Companies: Operating income enables investors to compare the profitability of different companies in the same industry, regardless of their capital structure or tax rates.

- Making Investment Decisions: Operating income is a key input in valuation models, helping investors make informed investment decisions.

9. What Are the Limitations of Using Operating Income?

While operating income is a valuable metric, it has limitations that users should be aware of.

9.1 What Operating Income Doesn’t Tell You

- Financing Costs: Operating income excludes interest expense, which can be a significant cost for companies with high levels of debt.

- Tax Implications: Operating income does not consider income taxes, which can vary depending on the company’s location and tax strategy.

- Non-Operating Items: Operating income excludes non-operating items, such as gains or losses from asset sales, which can impact the company’s overall profitability.

- Capital Investments: Operating income does not directly reflect capital investments, which are essential for long-term growth.

9.2 Potential for Manipulation

- Accounting Practices: Companies can use accounting practices to manipulate operating income, such as delaying expenses or accelerating revenue recognition.

- Non-Recurring Items: Companies can selectively exclude non-recurring items to present a more favorable picture of their operating performance.

- Lease Accounting: Companies can use lease accounting to classify leases as operating leases rather than capital leases, which can reduce reported operating expenses.

9.3 Alternative Metrics

- Net Income: Net income provides a more comprehensive measure of profitability, as it includes all expenses and revenues, including financing costs and income taxes.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): EBITDA is a non-GAAP metric that is often used to assess a company’s operating performance.

- Free Cash Flow (FCF): Free cash flow measures the cash a company generates from its operations after accounting for capital expenditures.

9.4 Supplementing with Other Financial Metrics

To gain a more complete understanding of a company’s financial performance, it’s important to supplement operating income with other financial metrics.

- Revenue Growth: Analyze revenue growth to assess the company’s ability to increase sales.

- Gross Margin: Analyze gross margin to assess the company’s pricing power and cost control.

- Net Profit Margin: Analyze net profit margin to assess the company’s overall profitability.

- Return on Equity (ROE): Analyze ROE to assess the company’s ability to generate profits from its equity.

- Debt-to-Equity Ratio: Analyze the debt-to-equity ratio to assess the company’s financial leverage.

9.5 How to See the Full Picture

- Analyze Financial Statements: Carefully review the company’s financial statements, including the income statement, balance sheet, and cash flow statement.

- Read Footnotes: Read the footnotes to the financial statements to understand the company’s accounting policies and any significant non-recurring items.

- Compare to Peers: Compare the company’s financial performance to that of its peers in the same industry.

- Consider Industry Trends: Consider industry trends and economic conditions when analyzing the company’s financial performance.

- Seek Expert Advice: Seek advice from financial professionals if needed.

10. FAQ About Calculating Operating Income

Here are some frequently asked questions about calculating operating income:

10.1 What is the difference between operating income and gross profit?

- Operating Income: Profit after deducting operating expenses from gross profit.

- Gross Profit: Revenue less the cost of goods sold (COGS).

10.2 How do you calculate operating income from net income?

- Start with net income. Add back interest expense, taxes, and any non-operating expenses or losses. Subtract any non-operating income or gains.

10.3 Is depreciation included in operating income?

- Yes, depreciation is an operating expense and is deducted when calculating operating income.

10.4 How does operating income affect a company’s stock price?

- Generally, higher operating income can positively affect a company’s stock price as it indicates better operational efficiency and profitability.

10.5 What is a good operating income margin?

- It varies by industry, but a margin above 10% is generally considered healthy. Compare with industry peers.

10.6 How often should operating income be calculated?

- Operating income is typically calculated quarterly and annually as part of a company’s financial reporting.

10.7 Can operating income be negative?

- Yes, if a company’s operating expenses exceed its gross profit, operating income can be negative.

10.8 Why is operating income important for investors?

- It provides a clear picture of a company’s core profitability and allows for comparison with peers.

10.9 How do one-time gains or losses affect operating income?

- One-time gains or losses are typically excluded from operating income to provide a clearer picture of core operational performance.

10.10 Where can I find a company’s operating income?

- On the company’s income statement, which is usually available on their investor relations website or in SEC filings (10-K and 10-Q).

By understanding these FAQs, you can gain a clearer understanding of operating income and its importance in financial analysis. If you’re looking to partner with businesses that demonstrate strong operating income, income-partners.net offers resources to help you find and evaluate potential partners.

Ultimately, a deep understanding of how to calculate and interpret operating income can significantly enhance your ability to assess financial health, identify growth opportunities, and build successful business partnerships, making resources like income-partners.net essential for informed decision-making. Visit income-partners.net to explore partnership opportunities, discover strategies for building strong business relationships, and find reliable information to support your financial growth.