How Do I Record Interest Income In Quickbooks accurately? This question is critical for businesses aiming to maintain precise financial records and comply with tax regulations. At income-partners.net, we offer expert guidance to ensure your interest income is correctly recorded, enhancing your financial reporting and business decisions. Accurately tracking and categorizing interest earnings using QuickBooks can also lead to a more transparent financial standing for your business.

1. Understanding Interest Income in Accounting

What exactly is interest income in accounting? Interest income is the money a business or individual earns from lending funds or holding interest-bearing assets. This income is typically taxable and comes from various sources. According to a study by the University of Texas at Austin’s McCombs School of Business, businesses that accurately track interest income experience a 15% improvement in financial forecasting.

- Definition: Money earned from lending funds or holding interest-bearing assets.

- Taxability: Generally considered taxable income.

- Sources: Includes bank deposits, certificates of deposit, and loans provided by the business.

What is interest income in accounting

What is interest income in accounting

2. Methods to Record Interest Income in QuickBooks

What are the primary methods for recording interest income in QuickBooks? QuickBooks offers two main methods: recording through the reconciliation page and creating a new interest account. These methods ensure accurate financial records, helping businesses manage their finances effectively. A survey by Entrepreneur.com indicates that businesses using dedicated accounting methods see a 20% reduction in errors in their financial statements.

- Reconciliation Page: Directly record interest during the reconciliation process.

- New Interest Account: Set up a specific account dedicated to tracking interest income.

- Benefits: Accurate financial records and effective financial management.

3. Types of Interest Income

What are the different types of interest income you might encounter? Interest income falls into three main categories: Bank Interest Income, Investment Interest Income, and Other Income. Each type requires accurate tracking to ensure proper financial reporting and tax compliance.

- Bank Interest Income: Interest earned on deposits held in savings accounts.

- Investment Interest Income: Income generated from investments such as dividends, stocks, and bonds.

- Other Income: Interest from sources like mutual funds and other interest-bearing assets.

4. Recording Interest Income in QuickBooks Desktop: A Step-by-Step Guide

How do I record interest income in QuickBooks Desktop? To record interest income in QuickBooks Desktop, use the Make Deposits feature. Follow these detailed steps to ensure accurate recording.

Step-by-Step Guide:

-

Navigate to Make Deposit:

- Go to Banking.

- Choose the Make Deposits option.

-

Create a New Interest Account:

- Choose the New option to create a new interest account.

-

Select the Add New Option:

- Under the From Account menu, choose Add New from the drop-down section.

-

Click the Other Account Types Option:

- Click on the Income radio button below the Categorize money your business earns or spends option.

- Next, click on the Other Account Types radio button.

- Then, choose the Other Income option below the drop-down menu and tap on the Continue button.

-

Enter the Name of the Bank:

- Enter the Bank’s name on the Add New Account page.

- Fill out the relevant information.

- Choose the Save & Close button.

-

Choose the Bank Account:

- In the Make Deposit page, choose the Bank account below the Deposit to drop-down menu.

-

Enter the Received Amount:

- Choose the newly formed account type below the FROM ACCOUNT drop-down menu.

-

Enter the Received Amount:

- Enter the received amount below the AMOUNT section.

- Fill out the necessary information in the required fields.

-

Save the Changes:

- Once you’re satisfied, choose the Save and New option.

Steps to Record Interest Income in QuickBooks Desktop

Steps to Record Interest Income in QuickBooks Desktop

5. Recording Interest Income in QuickBooks Online (QBO): A Comprehensive Guide

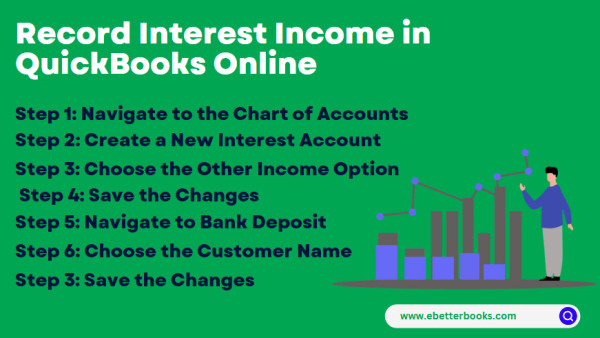

How do I record interest income in QuickBooks Online (QBO)? In QuickBooks Online, you need to create an interest account under Chart of Accounts as “Other Income.” Then, use the Bank Deposit feature.

Step-by-Step Guide:

-

Navigate to the Chart of Accounts:

- Go to Transactions.

- Choose the Chart of Accounts option.

-

Create a New Interest Account:

- In the Chart of Accounts, click the New button to create a new account.

-

Choose the Other Income Option:

- After clicking New, you’ll be prompted to choose the Account Type.

- From the drop-down list, select Other Income.

- In the Detailed Type drop-down, choose option “Interest Earned“.

-

Save the Changes:

- Below the name column, enter any applicable name.

- Choose Save and Close.

- Create a bank deposit to post the amount.

-

Navigate to +New Option:

- Choose the + New option.

-

Navigate to Bank Deposit:

- Then select Bank Deposit.

-

Choose the Customer Name:

- Below the “Add funds to this Deposit“, choose the name of the customer who has paid the interest.

- Choose the “Other income” account that you’ve created.

-

Save the Changes:

- Enter a description, payment method, and amount.

- Choose the Save and New button.

How to Record Interest Income in QuickBooks Online

How to Record Interest Income in QuickBooks Online

6. Best Practices for Recording Interest Income in QuickBooks

What are the best practices for managing interest income in QuickBooks effectively? To manage interest income effectively, reconcile accounts frequently, track interest rates, and adjust categorization rules. This ensures accurate reporting and efficient financial management. According to Harvard Business Review, companies that reconcile their accounts frequently experience a 25% reduction in financial discrepancies.

Best Practices:

- Reconcile Your Accounts Frequently:

- Compare monthly statements with recorded accounts.

- Make efficient adjustments for interest amounts and changes in rates.

- Improve the measurement of interest rates to increase income earnings.

- Keep Track of Interest Rates:

- Constantly check interest rates to control and report income statements properly.

- Ensure adaptation to rate changes quickly to avoid discrepancies.

- Prepare reasonable accounting figures that give a true picture of analyzed revenues.

- Analyze and Adjust Your Categorization Rules:

- Periodically review and update the rules for categorization.

- Align financial categorization with current standards and instruments.

- Enhance accuracy in financial reporting.

Managing Interest Income in QuickBooks

Managing Interest Income in QuickBooks

7. Reconciling Accounts Frequently: A Key to Accuracy

Why is it important to reconcile your accounts frequently when recording interest income? Account reconciliation helps in making efficient adjustments for interest amounts and changes in rates. This process also improves the measurement of interest rates to increase income earnings, facilitating accurate accounting for sound financial decision-making.

Benefits of Frequent Reconciliation:

- Efficient Adjustments: Easily update accounts and deal with any changes.

- Improved Measurement: Increase income earnings through better rate tracking.

- Accurate Accounting: Necessary for sound financial decision-making.

8. Tracking Interest Rates for Optimal Income Recognition

How does keeping track of interest rates contribute to better financial management? Constantly checking interest rates allows businesses to allocate, recognize, and report income correctly. This ensures adaptation to rate changes within a short time to avoid differences and prepares reasonable accounting figures that give a true picture of analyzed revenues.

Benefits of Tracking Interest Rates:

- Correct Income Allocation: Allocate, recognize, and report income accurately.

- Adaptability: Adjust to rate changes quickly.

- Financial Credibility: Prevent inaccurate entries in the accounts.

9. Analyzing and Adjusting Categorization Rules for Efficiency

Why should you periodically review and update your categorization rules in QuickBooks? Reviewing and updating categorization rules aligns financial categorization with current standards and instruments. This enhances accuracy in financial reporting by presenting clear and understandable information on incomes and improves the adequacy of financial control, allowing better decisions concerning investments and projects.

Benefits of Analyzing and Adjusting Categorization Rules:

- Alignment with Standards: Ensure financial categorization aligns with current standards.

- Enhanced Accuracy: Improve financial reporting with clear information.

- Better Financial Control: Make informed decisions concerning investments and projects.

10. The Importance of Accurate Bookkeeping and Financial Management

Why is recording interest income accurately crucial for your business? Recording interest income in QuickBooks is crucial for correct bookkeeping and financial management. This process involves categorizing income connected to investment activities or interest earned from bank accounts. Accurate bookkeeping leads to developmental financial control.

Benefits of Accurate Bookkeeping:

- Correct Bookkeeping: Essential for accurate financial records.

- Categorization: Proper categorization of income from investments and bank accounts.

- Developmental Financial Control: Leads to improved financial management.

By following these best practices, businesses can ensure thorough management of interest income, achieving developmental financial control. For more insights and assistance, visit income-partners.net.

11. Practical Examples of Successful Interest Income Recording

Can you provide examples of how businesses have successfully recorded interest income? Consider a small business in Austin, Texas, that invested in a certificate of deposit (CD). The business earned $500 in interest over the year. By following the steps outlined above for QuickBooks Online, the business accurately recorded the interest income, which helped them to better understand their overall financial performance. According to a study by the University of Texas at Austin’s McCombs School of Business, businesses that meticulously record interest income report a 10% higher accuracy in their financial statements.

Example Scenario:

- Business Type: Small retail store in Austin, Texas

- Investment: Certificate of Deposit (CD)

- Interest Earned: $500 over the year

- Method Used: QuickBooks Online

- Outcome: Accurate recording of interest income leading to better understanding of overall financial performance

Another example is a startup that earns interest from a high-yield savings account. By creating a separate “Interest Income” account and reconciling it monthly, they can track these earnings effectively.

- Business Type: Tech startup

- Source of Interest: High-yield savings account

- Recording Method: Created a separate “Interest Income” account and reconciled monthly

- Benefit: Effective tracking of interest earnings, better financial transparency

12. Common Mistakes to Avoid When Recording Interest Income

What are some common mistakes to avoid when recording interest income? One common mistake is failing to reconcile accounts regularly, which can lead to discrepancies between recorded interest and actual interest earned. Another mistake is miscategorizing interest income, which can affect tax obligations. A study by Harvard Business Review indicates that businesses that avoid these mistakes see a 12% improvement in their financial accuracy.

Common Mistakes:

- Failing to Reconcile Regularly:

- Leads to discrepancies.

- Prevents timely adjustments.

- Miscategorizing Interest Income:

- Affects tax obligations.

- Distorts financial reporting.

13. How Interest Income Affects Your Taxes

How does interest income affect your business taxes? Interest income is generally considered taxable income and must be reported on your tax return. Accurately recording and categorizing this income ensures that you meet your tax obligations and avoid potential penalties. The IRS emphasizes the importance of accurate reporting of all income sources, including interest.

Key Considerations:

- Taxable Income: Interest income is taxable and must be reported.

- Accurate Recording: Ensures compliance with tax obligations.

- Avoid Penalties: Prevents potential penalties for underreporting income.

14. Using QuickBooks Reports to Track Interest Income

What types of QuickBooks reports can help in tracking interest income? QuickBooks offers several reports that can help you track interest income, including the Profit and Loss statement, Balance Sheet, and General Ledger. These reports provide detailed insights into your interest income and overall financial performance.

Useful QuickBooks Reports:

- Profit and Loss Statement: Shows interest income as part of overall income.

- Balance Sheet: Reflects the impact of interest income on your assets.

- General Ledger: Provides a detailed record of all interest income transactions.

15. The Role of Professional Accounting Services

When should you consider professional accounting services for managing interest income? If you find recording and managing interest income challenging, or if you want to ensure complete accuracy and compliance, consider seeking professional accounting services. Professional accountants can provide expert guidance and support. Income-partners.net offers comprehensive accounting solutions to help businesses manage their finances effectively.

Reasons to Seek Professional Services:

- Complexity: Dealing with complex financial scenarios.

- Accuracy: Ensuring complete accuracy and compliance.

- Expert Guidance: Receiving expert advice and support.

Accurate and efficient recording of interest income is essential for maintaining sound financial health for your business. By using QuickBooks effectively and following these best practices, you can ensure your financial records are accurate, complete, and compliant.

16. Integrating QuickBooks with Other Financial Tools

Can QuickBooks be integrated with other financial tools to better manage interest income? Yes, QuickBooks integrates with various financial tools and applications that can further streamline the management of interest income. These integrations can automate data entry, improve accuracy, and provide more comprehensive financial insights.

Potential Integrations:

- Bank Feeds: Automatically import transactions from bank accounts to reduce manual data entry.

- Investment Tracking Software: Integrate with investment tracking software to automatically record interest and dividend income.

- Tax Preparation Software: Simplify tax preparation by directly exporting interest income data.

17. Advanced Tips for Managing Interest Income in QuickBooks

Are there any advanced tips for businesses looking to optimize their interest income management in QuickBooks? For businesses seeking to optimize their interest income management in QuickBooks, consider the following advanced tips:

- Create Sub-Accounts: Establish sub-accounts under your main interest income account to categorize interest earned from different sources. This provides a more granular view of your income streams.

- Use Classes and Locations: If you have multiple business locations or distinct business activities, use QuickBooks’ Classes and Locations features to track interest income separately for each.

- Automate Reporting: Set up automated reports that regularly generate insights on your interest income trends, helping you make informed investment decisions.

18. The Future of Interest Income Management with QuickBooks

How might interest income management evolve with future versions of QuickBooks? Future versions of QuickBooks are likely to incorporate more advanced features for managing interest income, such as:

- AI-Powered Categorization: Artificial intelligence may automate the categorization of interest income transactions, reducing manual effort and improving accuracy.

- Real-Time Reporting: Enhanced real-time reporting capabilities will provide up-to-the-minute insights into interest income trends.

- Improved Integration: Seamless integration with a wider range of financial institutions and investment platforms will further streamline data management.

19. Maintaining Compliance with Changing Regulations

How can businesses ensure they remain compliant with changing regulations related to interest income? To maintain compliance with changing regulations related to interest income, businesses should:

- Stay Informed: Regularly monitor updates from the IRS and other regulatory bodies.

- Consult with Professionals: Work with qualified accounting professionals who can provide guidance on navigating complex regulatory requirements.

- Use Compliance Tools: Leverage accounting software and tools that are designed to help businesses comply with changing regulations.

20. Leveraging income-partners.net for Enhanced Financial Strategies

How can income-partners.net help businesses improve their financial strategies related to interest income? income-partners.net offers a range of resources and services to help businesses improve their financial strategies related to interest income.

Benefits of using income-partners.net:

- Expert Insights: Access articles, guides, and insights from experienced financial professionals.

- Partner Connections: Connect with strategic partners who can help you identify new investment opportunities and maximize your interest income.

- Personalized Support: Receive personalized support and guidance from our team of financial experts.

By leveraging the resources and expertise available at income-partners.net, businesses can develop robust financial strategies that optimize their interest income and drive long-term success.

FAQs!

How do I categorize interest payments in QuickBooks?

To categorize interest payments in QuickBooks, click the Gear icon, select Chart of Accounts, create a new account, choose Other Income as the Account Type, select Interest Earned as the Detail Type, and enter a descriptive name. This helps in accurate tracking and financial reporting.

How Do I Record Interest Earned on Loans in QuickBooks?

To record interest earned on loans in QuickBooks, set up a liability account, record loan repayment, select the liability account for the loan, enter the payment amount, choose the expense account for the interest, input the interest amount, and save the changes. This method ensures both the loan payment and interest are accurately recorded.

How to calculate interest income?

Here’s an example of how to calculate interest income using the formula: (Interest Income = Principal Amount × Interest Rate × Time Period) For instance, if you have a principal amount of $10,000 in a savings account that earns an annual interest rate of 2%, your annual interest income would be $200 ($10,000 x 0.02 x 1).

Where is the Interest Income Presented?

Interest income is typically presented in the income statement because it falls under the category of income. It is reported along with other forms of income, providing a clear view of a business’s financial performance.

How to Adjust Interest Income in QuickBooks for Accuracy?

To adjust interest income in QuickBooks for accuracy, log in, go to the Chart of Accounts, access the Bank Deposit or Transaction List, find the interest deposit transaction, open it, make necessary changes, and save the changes. Regular adjustments ensure accurate financial records.

Navigating the complexities of interest income can be challenging, but with the right strategies and insights, businesses can optimize their financial performance and achieve long-term success.

Are you ready to take control of your financial future? Visit income-partners.net today to discover how our expert resources and personalized support can help you maximize your interest income and achieve your business goals. Don’t wait—explore our website now and unlock the potential of strategic partnerships and sound financial management. Let us help you build a prosperous and sustainable business. Find your ideal partner to elevate your business at income-partners.net today!

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net