Knowing how to determine your taxable income is crucial for accurate tax filing and financial planning, and at income-partners.net, we help you understand this key aspect of your financial life. Understanding how to calculate your taxable income involves knowing what’s included in your gross income, what deductions you can take, and what income sources are tax-exempt. We help business owners, entrepreneurs, investors and marketers discover and evaluate income potential, business deductions, tax planning so they can get access to partnership opportunities for wealth creation.

1. What Is Taxable Income And Why Does It Matter?

Taxable income is the foundation upon which your tax liability is calculated. It’s the part of your gross income that remains after all applicable deductions and exemptions have been subtracted. Knowing your taxable income is the initial step towards understanding how much you owe in taxes and is essential for effective financial planning.

- Accurate Tax Filing: Understanding your taxable income ensures you file your taxes accurately, avoiding penalties and interest.

- Financial Planning: Knowing your taxable income helps in budgeting, saving, and investment decisions.

- Taking Advantage of Tax Benefits: Correctly identifying your taxable income allows you to leverage all available deductions and credits, maximizing your tax savings.

2. What Is Included In Gross Income?

Gross income includes all income you receive in the form of money, property, and services that are not tax-exempt. It’s essential to have a thorough understanding of what constitutes gross income to accurately calculate your taxable income.

- Wages and Salaries: All compensation received from employment, including wages, salaries, bonuses, and commissions.

- Business Income: Revenue generated from your business, minus the cost of goods sold and other business expenses.

- Investment Income: Includes dividends, interest, capital gains from the sale of stocks or other assets, and rental income.

- Retirement Income: Distributions from retirement accounts such as 401(k)s, traditional IRAs, and pensions.

- Other Income: Miscellaneous income such as alimony, royalties, prizes, and gambling winnings.

3. What Are Above-The-Line Deductions And How Do They Reduce AGI?

Above-the-line deductions, also known as adjustments to gross income, are deductions you can take before calculating your Adjusted Gross Income (AGI). These deductions reduce your gross income and can significantly lower your taxable income.

- IRA Contributions: Contributions to traditional Individual Retirement Accounts (IRAs) can be deducted, potentially lowering your taxable income.

- Student Loan Interest: You can deduct the interest paid on qualified student loans, subject to certain limitations.

- Health Savings Account (HSA) Contributions: Contributions to an HSA are deductible, offering a tax-advantaged way to save for medical expenses.

- Self-Employment Tax: One-half of your self-employment tax is deductible, acknowledging the employer’s portion of Social Security and Medicare taxes.

- Alimony Payments: Alimony payments made under divorce or separation agreements executed before 2019 are deductible.

- Moving Expenses for Armed Forces: Members of the Armed Forces on active duty who move due to a permanent change of station can deduct certain moving expenses.

4. What Is Adjusted Gross Income (AGI) And Why Is It Important?

Adjusted Gross Income (AGI) is your gross income minus above-the-line deductions. AGI is a crucial figure because it is the starting point for calculating many deductions and credits.

- Calculation: AGI is calculated by subtracting above-the-line deductions from your gross income.

- Eligibility for Deductions and Credits: Many tax deductions and credits have AGI limitations. Higher AGI can reduce or eliminate your eligibility for certain tax benefits.

- State Income Tax: Many states use AGI as the starting point for calculating state income tax liability.

- Financial Aid: AGI is often used to determine eligibility for financial aid for college.

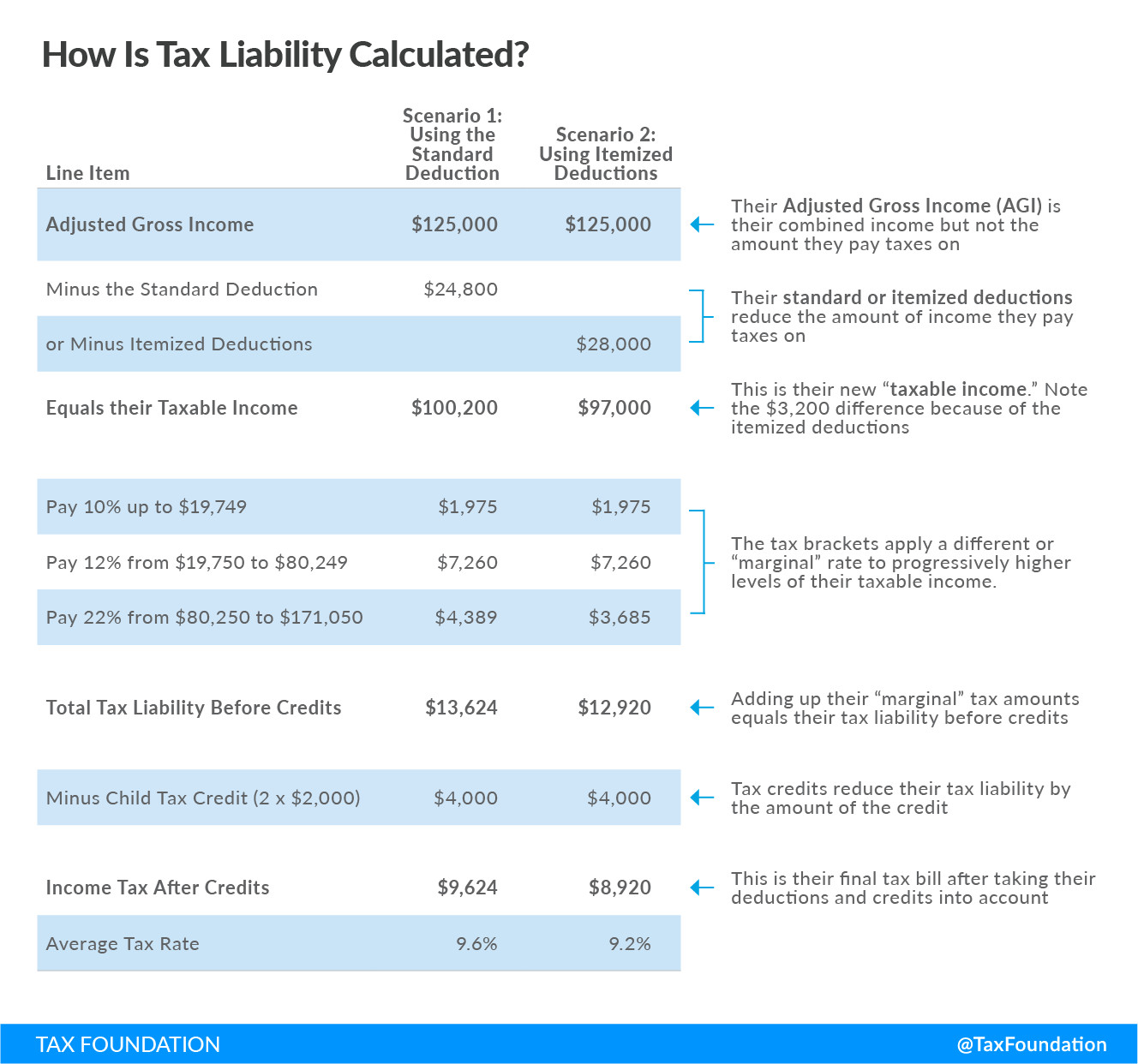

5. Standard Deduction Vs. Itemized Deductions: Which Should I Choose?

After calculating your AGI, you must decide whether to take the standard deduction or itemize your deductions. This decision depends on whether your itemized deductions exceed the standard deduction for your filing status.

- Standard Deduction: A fixed amount that depends on your filing status (single, married filing jointly, etc.). It reduces the income subject to tax.

- Itemized Deductions: Specific expenses that can be deducted from your AGI. Common itemized deductions include medical expenses, state and local taxes (SALT), home mortgage interest, and charitable contributions.

- Decision-Making: Compare your total itemized deductions to the standard deduction for your filing status. Choose whichever is higher to minimize your taxable income.

5.1. What Are the Current Standard Deduction Amounts?

The standard deduction amounts vary each year. For the 2023 tax year, they are as follows:

| Filing Status | Standard Deduction |

|---|---|

| Single | $13,850 |

| Married Filing Separately | $13,850 |

| Married Filing Jointly | $27,700 |

| Head of Household | $20,800 |

| Qualifying Widow(er) | $27,700 |

Note: These amounts are subject to change annually.

5.2. What Are Common Itemized Deductions?

- Medical Expenses: You can deduct medical expenses exceeding 7.5% of your AGI. This includes payments for doctors, dentists, hospitals, insurance premiums, and long-term care.

- State and Local Taxes (SALT): You can deduct state and local income, sales, and property taxes, up to a combined limit of $10,000 per household.

- Home Mortgage Interest: You can deduct interest paid on a mortgage for your primary or secondary residence. For mortgages taken out after December 15, 2017, the deduction is limited to interest on the first $750,000 of debt.

- Charitable Contributions: You can deduct contributions to qualified charitable organizations, up to certain limits based on your AGI.

- Casualty and Theft Losses: You can deduct losses from casualty or theft of property, but only if the loss is due to a federally declared disaster.

6. How Do Business Expenses Affect Taxable Income for the Self-Employed?

For self-employed individuals, business expenses play a crucial role in reducing taxable income. These expenses are deducted from your business revenue to determine your net profit, which is subject to self-employment tax and income tax.

- Deductible Business Expenses: Common business expenses include office supplies, business travel, advertising, insurance, and professional fees.

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct expenses related to that space.

- Vehicle Expenses: You can deduct the actual expenses of operating a vehicle for business purposes or take the standard mileage rate.

- Depreciation: You can deduct the cost of depreciable assets, such as equipment and vehicles, over their useful lives.

- Qualified Business Income (QBI) Deduction: Self-employed individuals may be eligible for the QBI deduction, which allows them to deduct up to 20% of their qualified business income.

7. What Are Capital Gains And How Are They Taxed?

Capital gains are profits from the sale of capital assets, such as stocks, bonds, and real estate. The tax rate on capital gains depends on how long you held the asset (short-term vs. long-term) and your income level.

- Short-Term Capital Gains: Profits from assets held for one year or less are taxed at your ordinary income tax rate.

- Long-Term Capital Gains: Profits from assets held for more than one year are taxed at preferential rates, which are generally lower than ordinary income tax rates.

- Capital Losses: If your capital losses exceed your capital gains, you can deduct up to $3,000 of the net loss per year. Any excess loss can be carried forward to future years.

8. What Income Sources Are Considered Nontaxable?

While most income is taxable, some sources of income are generally considered nontaxable by the IRS. Understanding these exclusions can help you avoid overpaying your taxes.

- Gifts and Inheritances: Generally, gifts and inheritances are not considered taxable income to the recipient. However, large gifts may be subject to gift tax paid by the donor.

- Life Insurance Proceeds: Life insurance payouts are usually tax-free to the beneficiary.

- Certain Scholarship and Grant Monies: Scholarship and grant money used for qualified education expenses, such as tuition and fees, is typically tax-free.

- Child Support Payments: Child support payments received are not considered taxable income.

- Workers’ Compensation Benefits: Benefits received as compensation for work-related injuries or illnesses are generally tax-free.

- Qualified Roth IRA Distributions: Distributions from a Roth IRA are tax-free in retirement, provided certain conditions are met.

9. How Do Retirement Account Distributions Affect Taxable Income?

Retirement account distributions can have a significant impact on your taxable income. The tax treatment of distributions depends on the type of retirement account.

- Traditional IRA and 401(k) Distributions: Distributions from traditional IRAs and 401(k)s are taxed as ordinary income in the year they are received.

- Roth IRA and 401(k) Distributions: Qualified distributions from Roth IRAs and 401(k)s are tax-free in retirement, provided certain conditions are met.

- Early Withdrawals: Withdrawals from retirement accounts before age 59 ½ are generally subject to a 10% penalty, in addition to being taxed as ordinary income.

- Required Minimum Distributions (RMDs): Once you reach a certain age (currently 73), you are required to take minimum distributions from traditional IRAs and 401(k)s, which are taxable.

10. How Does Filing Status Impact Taxable Income?

Your filing status significantly affects your standard deduction, tax brackets, and eligibility for certain tax benefits. Choosing the correct filing status can minimize your tax liability.

- Single: For unmarried individuals who do not qualify for another filing status.

- Married Filing Jointly: For married couples who agree to file a joint return.

- Married Filing Separately: For married individuals who choose to file separate returns. This status may result in a higher tax liability compared to filing jointly.

- Head of Household: For unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child.

- Qualifying Widow(er) with Dependent Child: For a surviving spouse who maintains a home for a dependent child for the entire year.

11. What Role Do Tax Credits Play In Reducing My Tax Liability?

Tax credits directly reduce your tax liability, dollar for dollar, making them more valuable than tax deductions. They can be either refundable or nonrefundable.

- Child Tax Credit: A credit for each qualifying child under age 17. The credit can be partially refundable, meaning you may receive a portion of it back as a refund, even if you don’t owe any taxes.

- Earned Income Tax Credit (EITC): A credit for low-to-moderate income workers and families. The EITC is refundable, providing a significant tax benefit to eligible taxpayers.

- Child and Dependent Care Credit: A credit for expenses paid for the care of a qualifying child or other dependent, allowing you to work or look for work.

- Education Credits: The American Opportunity Tax Credit (AOTC) and Lifetime Learning Credit help offset the costs of higher education.

- Energy Credits: Credits for investments in energy-efficient improvements to your home, such as solar panels and energy-efficient windows.

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income12. How Do State And Local Taxes Interact With Federal Taxable Income?

The interaction between state and local taxes (SALT) and federal taxable income is an important consideration for many taxpayers, particularly those living in states with high income or property taxes.

- SALT Deduction: Taxpayers can itemize and deduct state and local taxes, including income, sales, and property taxes, up to a combined limit of $10,000 per household.

- Impact on Federal Taxable Income: The SALT deduction reduces your federal taxable income, potentially lowering your federal tax liability.

- State Income Tax Calculation: Many states use either AGI or federal taxable income as a starting point for calculating state income tax liability.

- Considerations: The limited SALT deduction may impact taxpayers in high-tax states, as it reduces the tax benefits of itemizing state and local taxes.

13. What Are Some Common Mistakes To Avoid When Calculating Taxable Income?

Calculating taxable income can be complex, and it’s easy to make mistakes. Avoiding these common errors can help ensure your tax return is accurate and that you’re not paying more than you owe.

- Incorrectly Reporting Income: Failing to report all sources of income, such as side hustle earnings, investment income, and gig economy income.

- Missing Deductions: Overlooking eligible deductions, such as IRA contributions, student loan interest, and health savings account (HSA) contributions.

- Choosing the Wrong Filing Status: Selecting an incorrect filing status, such as single instead of head of household, which can affect your standard deduction and tax bracket.

- Miscalculating Basis: Calculating your capital gains or losses from the sale of assets.

- Failing to Keep Adequate Records: Not keeping sufficient records to support your income, deductions, and credits. This can make it difficult to substantiate your tax return if you’re audited.

14. How Can I Plan Throughout The Year To Minimize My Taxable Income?

Effective tax planning involves strategies to minimize your taxable income throughout the year. Here are some tips to help you reduce your tax liability:

- Maximize Retirement Contributions: Contribute as much as possible to tax-advantaged retirement accounts, such as 401(k)s and traditional IRAs. These contributions reduce your taxable income and allow your investments to grow tax-deferred.

- Take Advantage of Health Savings Accounts (HSAs): If you have a high-deductible health insurance plan, contribute to an HSA. These contributions are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

- Consider Tax-Loss Harvesting: Offset capital gains by selling investments at a loss.

- Bunch Itemized Deductions: If your itemized deductions are close to the standard deduction amount, consider bunching deductions in alternating years to exceed the standard deduction threshold.

15. How Does The Tax Reform (Tax Cuts And Jobs Act) Affect Taxable Income?

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, made significant changes to the tax code that affected how taxable income is calculated. Here are some key provisions of the TCJA and their impact:

- Standard Deduction: The TCJA nearly doubled the standard deduction amounts, making it more beneficial for many taxpayers to take the standard deduction rather than itemize.

- Itemized Deductions: The TCJA limited or eliminated certain itemized deductions, such as the deduction for state and local taxes (SALT), which is now capped at $10,000 per household.

- Personal Exemptions: The TCJA eliminated personal exemptions, which previously allowed taxpayers to deduct a set amount for themselves, their spouse, and their dependents.

- Tax Rates and Brackets: The TCJA reduced income tax rates and adjusted the income brackets, which affected the amount of tax owed at different income levels.

- Qualified Business Income (QBI) Deduction: The TCJA introduced the QBI deduction, which allows self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

16. What Resources Are Available To Help Me Calculate My Taxable Income?

Several resources are available to help you calculate your taxable income accurately.

- IRS Publications and Forms: The IRS provides a wealth of information on its website, including publications, forms, and instructions.

- Tax Software: Tax software programs like TurboTax and H&R Block guide you through the tax preparation process and calculate your taxable income automatically.

- Tax Professionals: Hiring a certified public accountant (CPA) or other tax professional can provide personalized advice and assistance in calculating your taxable income and minimizing your tax liability.

- Income-Partners.net: This website provides resources, tools, and partnership opportunities to help you increase your income and minimize your tax liability.

- University of Texas at Austin’s McCombs School of Business: This institution offers research and resources related to tax planning and financial management.

17. How Do I Know If I Am Being Audited And What Should I Do?

An audit is an examination of your tax return by the IRS to verify that you’ve reported your income, deductions, and credits accurately. If you are selected for an audit, it’s essential to know what to expect and how to respond.

- Notification: The IRS typically notifies you of an audit by mail.

- Types of Audits: Audits can be conducted by mail, in person at an IRS office, or in person at your home or business.

- Preparation: Gather all relevant documents to support your tax return, including income statements, receipts, bank statements, and other records.

- Representation: You have the right to represent yourself during an audit or hire a tax professional to represent you.

- Appeal: If you disagree with the results of the audit, you have the right to appeal the decision.

18. What Are The Key Tax Planning Strategies For High-Income Earners?

High-income earners often face more complex tax situations and may benefit from advanced tax planning strategies to minimize their tax liability.

- Maximize Retirement Contributions: High-income earners should maximize contributions to tax-advantaged retirement accounts, such as 401(k)s, IRAs, and other retirement plans.

- Consider Tax-Advantaged Investments: Invest in tax-exempt municipal bonds, which offer interest income that is exempt from federal income tax.

- Use Estate Planning Strategies: Work with an estate planning attorney to develop strategies for minimizing estate taxes.

- Charitable Giving: Donate appreciated assets to qualified charitable organizations, which can provide a tax deduction for the fair market value of the asset.

- Tax-Efficient Investment Strategies: Use tax-efficient investment strategies, such as tax-loss harvesting and asset location, to minimize your investment taxes.

19. How Can I Use Partnerships To Improve My Tax Situation?

Strategic partnerships can offer various tax benefits, especially for business owners and investors.

- Business Expansion: Partners can pool resources, share expenses, and expand their business operations, potentially leading to increased revenue and tax benefits.

- Investment Opportunities: Partners can pool capital to invest in real estate, stocks, or other assets, and share the tax benefits and liabilities associated with those investments.

- Risk Mitigation: Partners can share the financial risks associated with business ventures, reducing the tax liabilities for each individual partner.

- Tax Planning: Partners can engage in coordinated tax planning strategies to optimize their tax positions and minimize their overall tax liability.

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, strategic partnerships provide access to new markets and technologies, and can lead to increased profitability and tax savings.

20. What Are The Latest Updates In Tax Laws And How Do They Affect Me?

Tax laws are subject to change, and staying informed about the latest updates is crucial for accurate tax planning. Some recent updates include:

- Tax Cuts and Jobs Act (TCJA): Many provisions of the TCJA are set to expire at the end of 2025, which could lead to significant changes in tax rates, deductions, and credits.

- Inflation Adjustments: The IRS adjusts many tax provisions annually for inflation, including standard deduction amounts, tax brackets, and contribution limits for retirement accounts.

- New Tax Credits and Incentives: New tax credits and incentives are introduced periodically to encourage certain behaviors, such as investments in renewable energy or energy-efficient home improvements.

- Changes to IRS Regulations: The IRS updates its regulations and guidance frequently, which can affect how certain tax rules are interpreted and applied.

Conclusion

Understanding how to determine your taxable income is crucial for accurate tax filing and financial planning. By following these guidelines, you can confidently navigate the complexities of tax law and minimize your tax liability.

Ready to take control of your financial future and explore strategic partnership opportunities? Visit income-partners.net today to discover a wealth of resources, connect with potential partners, and unlock new avenues for wealth creation. Don’t miss out on the chance to optimize your tax situation and build a successful financial future with income-partners.net.

FAQ Section

Q1: What is the basic formula for calculating taxable income?

Taxable Income = Gross Income – Above-the-Line Deductions – (Standard Deduction or Itemized Deductions)

Q2: How does self-employment tax impact my taxable income?

You can deduct one-half of your self-employment tax from your gross income as an above-the-line deduction, reducing your adjusted gross income (AGI) and ultimately your taxable income.

Q3: Are distributions from a Roth IRA taxable?

Qualified distributions from a Roth IRA are generally tax-free in retirement, provided certain conditions are met, such as being at least 59 ½ years old and having the account open for at least five years.

Q4: What happens if my itemized deductions are less than the standard deduction?

If your total itemized deductions are less than the standard deduction for your filing status, you should take the standard deduction, as it will result in a lower taxable income.

Q5: Can I deduct medical expenses from my taxable income?

Yes, you can deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI) as an itemized deduction.

Q6: How does my filing status affect my taxable income?

Your filing status affects your standard deduction amount, tax brackets, and eligibility for certain tax benefits, all of which impact your taxable income and tax liability.

Q7: What is the Qualified Business Income (QBI) deduction?

The QBI deduction allows self-employed individuals and small business owners to deduct up to 20% of their qualified business income, reducing their taxable income.

Q8: Are gifts and inheritances considered taxable income?

Generally, gifts and inheritances are not considered taxable income to the recipient. However, large gifts may be subject to gift tax paid by the donor.

Q9: How can I minimize my taxable income through retirement contributions?

Contribute as much as possible to tax-advantaged retirement accounts, such as 401(k)s and traditional IRAs, as these contributions reduce your taxable income and allow your investments to grow tax-deferred.

Q10: What resources are available to help me calculate my taxable income accurately?

Resources include IRS publications and forms, tax software, tax professionals, income-partners.net, and educational resources from institutions like the University of Texas at Austin’s McCombs School of Business.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.