Paying off debt with a low income might seem daunting, but it’s absolutely achievable with the right strategies. At income-partners.net, we provide the insights and resources needed to manage debt and build financial stability through strategic partnerships. Our website offers tools and support to turn your financial challenges into opportunities for growth and long-term prosperity.

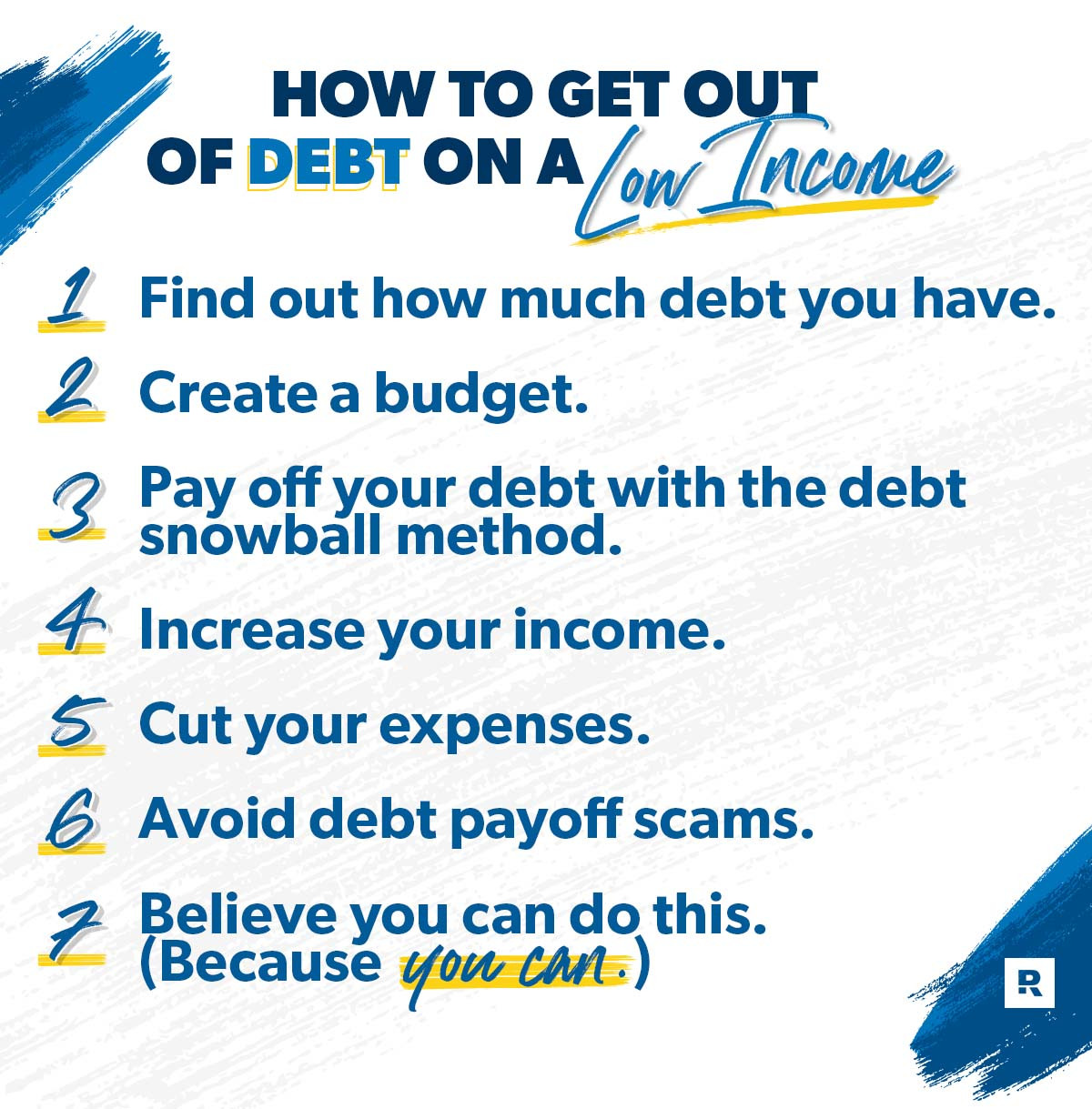

1. Determine Your Total Debt

The first step to conquering your debt is knowing exactly what you’re up against. List all your debts, including credit cards, loans, and any other outstanding balances. Include the creditor, the total amount owed, and the interest rate for each. According to financial experts, understanding the full scope of your debt is crucial for creating an effective repayment plan.

Why is it important to list out every debt?

Listing out every debt gives you a clear picture of your financial obligations. This clarity helps you prioritize which debts to tackle first and ensures you don’t overlook any liabilities. By itemizing each debt, you gain a comprehensive understanding of your financial landscape, enabling you to create a more informed and effective repayment strategy. This thorough approach can significantly reduce stress and improve your chances of successfully paying off your debt.

How do I find all my debts?

You can find all your debts by checking your credit report, which you are entitled to receive for free annually from each of the three major credit bureaus: Experian, Equifax, and TransUnion. Additionally, review your financial statements, loan documents, and online banking accounts to identify any outstanding balances. Contact each creditor to confirm the current balance and interest rate. Keeping an organized record of all your debts ensures you have a complete and accurate picture of your financial obligations.

What if I have debts I don’t know about?

If you suspect you have debts you don’t know about, the best course of action is to request your credit report from Experian, Equifax, and TransUnion. These reports will list all debts reported to the credit bureaus. Additionally, review old financial records and statements. If you still find discrepancies or suspect unknown debts, contact a credit counseling agency or a financial advisor to help you investigate further and ensure your financial records are accurate.

2. Create a Realistic Budget

Budgeting is the cornerstone of any debt repayment plan, especially when you’re working with a low income. Create a budget that outlines all your income and expenses. Prioritize essential expenses like housing, food, and transportation, and then identify areas where you can cut back. Using budgeting tools or apps can help you track your spending and stay on course.

What is the best budgeting method for low-income earners?

For low-income earners, the 50/30/20 rule is a practical budgeting method. It allocates 50% of your income to needs (housing, food, transportation), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. This method helps prioritize essential expenses while also allowing for some flexibility. By allocating a specific portion to debt repayment, you ensure consistent progress towards becoming debt-free.

How do I cut expenses when I’m already on a tight budget?

Cutting expenses on a tight budget requires creativity and diligence. Look for small, recurring costs that can be reduced or eliminated. Consider options like meal planning to reduce food costs, negotiating bills with service providers, and finding free or low-cost entertainment options. Even small savings can add up over time and free up more funds for debt repayment. Regularly review your budget to identify new opportunities for savings.

What if my income is too low to cover all my essential expenses?

If your income is too low to cover all essential expenses, explore options to increase your income. Consider taking on a side hustle, freelancing, or finding a higher-paying job. Simultaneously, seek assistance programs such as food banks, rental assistance, and energy assistance programs to help cover essential needs. Addressing both sides of the equation—increasing income and reducing expenses—can help you achieve financial stability and start paying off debt.

budgeting worksheet

budgeting worksheet

3. Use the Debt Snowball Method

The debt snowball method involves listing your debts from smallest to largest, regardless of interest rate. Focus on paying off the smallest debt first, while making minimum payments on the others. Once the smallest debt is paid off, apply that payment to the next smallest debt, and so on. This method provides quick wins and motivates you to continue paying off your debts.

Why does the debt snowball method work?

The debt snowball method works because it provides quick psychological wins. By paying off smaller debts first, you see immediate progress, which motivates you to continue. This momentum can be especially helpful when dealing with debt on a low income, where motivation is essential to staying committed to your repayment plan.

What are the drawbacks of the debt snowball method?

The main drawback of the debt snowball method is that it does not prioritize debts with the highest interest rates. This means you might pay more in interest over the long term compared to other methods like the debt avalanche. However, the psychological benefits and increased motivation often outweigh the higher interest costs for many people.

Is the debt snowball method better than the debt avalanche method?

Whether the debt snowball method is better than the debt avalanche method depends on your personal preferences and financial situation. The debt avalanche method prioritizes debts with the highest interest rates, saving you money in the long run. However, the debt snowball method provides quicker wins, which can be more motivating. Choose the method that best aligns with your financial goals and psychological needs.

4. Increase Your Income

Increasing your income can significantly accelerate your debt repayment efforts. Consider taking on a part-time job, freelancing, or selling items you no longer need. Even a small increase in income can make a big difference in how quickly you pay off your debts. Income-partners.net offers resources and opportunities for individuals looking to boost their earnings through strategic partnerships.

What are some realistic ways to increase my income quickly?

Realistic ways to increase your income quickly include driving for ride-sharing services, delivering food, freelancing online, selling items on platforms like eBay or Craigslist, and taking on temporary or seasonal jobs. These options offer flexibility and can provide immediate income to put towards debt repayment.

How can income-partners.net help me increase my income?

Income-partners.net helps you increase your income by connecting you with strategic partnerships and income-generating opportunities. Our platform provides access to resources and networks that can help you start a side hustle, find freelance work, or even launch a new business venture. By leveraging our partnerships, you can boost your earning potential and accelerate your debt repayment journey.

What skills are most valuable for earning extra income?

Skills most valuable for earning extra income include writing, graphic design, web development, social media management, virtual assistance, and tutoring. These skills are in high demand in the freelance market and can provide opportunities for remote work and flexible hours. Investing in developing these skills can significantly increase your earning potential.

increase income

increase income

5. Reduce Your Expenses

Look for ways to reduce your monthly expenses. This might involve cutting back on non-essential spending, negotiating lower rates on your bills, or finding cheaper alternatives for your regular purchases. Every dollar saved can be put towards debt repayment, accelerating your progress.

What are some common areas where I can cut expenses?

Common areas to cut expenses include dining out, entertainment, clothing, transportation, and subscriptions. Consider cooking at home more often, finding free or low-cost entertainment options, reducing shopping trips, using public transportation or carpooling, and canceling unused subscriptions. Small changes in these areas can lead to significant savings over time.

How can I negotiate lower rates on my bills?

To negotiate lower rates on your bills, start by researching the average rates for similar services in your area. Contact your service providers and ask if they can match these rates. Be polite but firm, and mention that you are considering switching providers if they cannot offer a better deal. Often, companies are willing to negotiate to retain your business.

What if I can’t find any more expenses to cut?

If you can’t find any more expenses to cut, consider more drastic measures like downsizing your home, selling your car and using public transportation, or moving to a more affordable area. While these changes may be challenging, they can significantly reduce your expenses and free up more money for debt repayment. Additionally, explore options for increasing your income to offset your essential expenses.

6. Avoid New Debt

While you’re working on paying off your existing debt, it’s crucial to avoid taking on any new debt. Put away your credit cards, and avoid taking out new loans unless absolutely necessary. Focus on living within your means and making progress towards becoming debt-free.

Why is it important to avoid new debt while paying off existing debt?

Avoiding new debt while paying off existing debt is essential because it prevents you from falling deeper into the debt cycle. New debt can undo your progress and make it more difficult to achieve your financial goals. By avoiding new debt, you can focus your resources on eliminating your current obligations and building a more secure financial future.

How can I resist the temptation to take on new debt?

To resist the temptation to take on new debt, create a budget that includes a buffer for unexpected expenses. Avoid impulse purchases, and think carefully before making any major financial decisions. Consider unsubscribing from marketing emails and avoiding situations that might trigger unnecessary spending. Focus on the progress you’re making in paying off your existing debt to stay motivated.

What should I do if I have an unexpected expense?

If you have an unexpected expense, first evaluate whether it is truly necessary. If it is, try to cover the expense with your emergency fund or by cutting back on non-essential spending. If you must use credit, choose a credit card with the lowest interest rate and pay it off as quickly as possible. Avoid taking out new loans, if possible, and explore options for temporary financial assistance.

7. Seek Professional Help

If you’re struggling to manage your debt on your own, consider seeking professional help. Credit counseling agencies can provide guidance and support, and may even be able to negotiate lower interest rates or payment plans with your creditors. Income-partners.net can connect you with reputable financial advisors who can help you develop a personalized debt repayment strategy.

When should I consider seeking professional help for debt?

You should consider seeking professional help for debt when you feel overwhelmed, are unable to make progress on your own, or are facing serious consequences like wage garnishment or foreclosure. A financial advisor or credit counselor can provide expert guidance and support to help you get back on track.

What are the benefits of working with a credit counseling agency?

The benefits of working with a credit counseling agency include receiving personalized advice, developing a budget, negotiating lower interest rates and payment plans, and gaining access to educational resources. Credit counseling agencies can help you create a sustainable debt repayment plan and improve your financial literacy.

How can income-partners.net help me find a reputable financial advisor?

Income-partners.net can help you find a reputable financial advisor by connecting you with qualified professionals who have a proven track record of helping individuals manage their debt. Our platform provides access to a network of trusted advisors who can offer personalized guidance and support to help you achieve your financial goals.

8. Stay Positive and Persistent

Paying off debt on a low income can be challenging, but it’s important to stay positive and persistent. Celebrate your small victories, and don’t get discouraged by setbacks. With dedication and hard work, you can achieve your goal of becoming debt-free.

How can I stay motivated while paying off debt?

To stay motivated while paying off debt, set realistic goals, track your progress, and celebrate your achievements. Find a support system of friends, family, or online communities who can offer encouragement and accountability. Visualize your debt-free future, and remind yourself of the reasons why you want to become debt-free.

What should I do if I experience a setback in my debt repayment plan?

If you experience a setback in your debt repayment plan, don’t get discouraged. Evaluate what went wrong, adjust your budget or repayment strategy, and recommit to your goals. Remember that setbacks are a normal part of the process, and it’s important to learn from them and keep moving forward.

How can I reward myself without derailing my debt repayment efforts?

You can reward yourself without derailing your debt repayment efforts by choosing low-cost or free rewards. Consider activities like going for a walk, reading a book, spending time with loved ones, or enjoying a relaxing bath. These rewards can provide a sense of accomplishment and motivation without breaking the bank.

FAQ: Paying off Debt With Low Income

Q1: Can I really pay off debt with a low income?

Yes, you can absolutely pay off debt with a low income by creating a budget, prioritizing debt repayment, increasing your income, and reducing your expenses.

Q2: How long will it take to pay off my debt?

The timeline for paying off your debt depends on the amount of debt you have, your income, and the repayment strategies you use. With dedication and persistence, you can make significant progress over time.

Q3: What if I can’t afford the minimum payments on my debts?

If you can’t afford the minimum payments on your debts, contact your creditors to discuss your options. They may be willing to offer a lower interest rate or payment plan. Additionally, seek help from a credit counseling agency.

Q4: Should I consolidate my debts?

Debt consolidation can be a good option if it allows you to lower your interest rate or simplify your payments. However, be sure to compare the terms and fees of different consolidation options before making a decision.

Q5: How can I improve my credit score while paying off debt?

You can improve your credit score while paying off debt by making timely payments, keeping your credit utilization low, and avoiding new debt.

Q6: Are there government programs to help with debt repayment?

There are some government programs that can help with debt repayment, such as income-driven repayment plans for federal student loans. Research your options to see if you qualify for any assistance.

Q7: What is the difference between debt settlement and debt management?

Debt settlement involves negotiating with your creditors to pay a lower amount than you owe, while debt management involves working with a credit counseling agency to create a repayment plan and lower your interest rates.

Q8: How do I avoid debt payoff scams?

Avoid debt payoff scams by being wary of companies that promise quick or easy debt relief, charge high fees, or ask for upfront payments. Always do your research and work with reputable organizations.

Q9: Can bankruptcy help me get rid of debt?

Bankruptcy can be a last resort for getting rid of debt, but it can also have negative consequences for your credit score and financial future. Consider all your options before filing for bankruptcy.

Q10: Where can I find more resources and support for paying off debt?

You can find more resources and support for paying off debt at income-partners.net, as well as through credit counseling agencies, financial advisors, and online communities.

Conclusion

Paying off debt with a low income requires discipline, planning, and persistence. By following these strategies and utilizing the resources available at income-partners.net, you can take control of your finances and achieve your goal of becoming debt-free. Start today, and take the first step towards a brighter financial future. Visit income-partners.net to explore partnership opportunities, learn more about debt management, and connect with professionals who can help you succeed.

Are you ready to transform your financial situation and start building a prosperous future? Visit income-partners.net today to discover how our strategic partnerships and expert resources can help you achieve financial freedom! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.