The balance sheet and income statement are connected because net income from the income statement flows into the retained earnings section of the balance sheet, reflecting a company’s profitability over a period and its cumulative earnings kept for reinvestment. Understanding this connection is vital for strategic partnership decisions, and at income-partners.net, we help you explore these financial relationships for optimal business alliances and revenue enhancement. This knowledge enables informed decision-making, fostering sustainable growth and successful collaborations through financial statement analysis, profitability assessment, and investment strategies.

1. What Is the Primary Link Between the Balance Sheet and Income Statement?

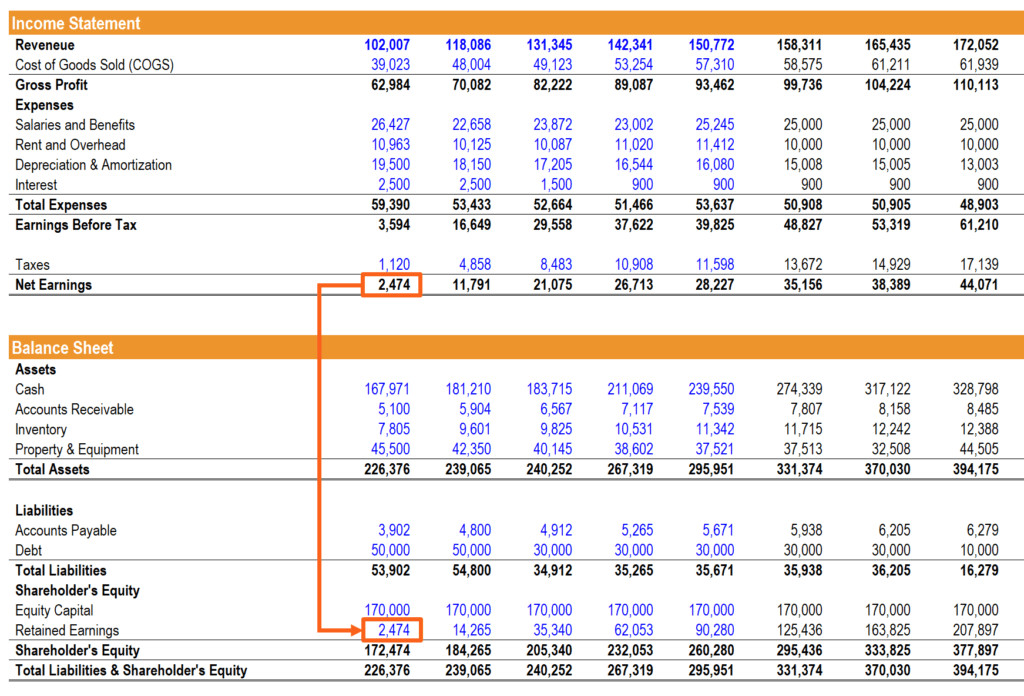

The primary link between the balance sheet and income statement is net income. The net income calculated on the income statement flows into the retained earnings account on the balance sheet, representing the cumulative profits of a company that have been retained for reinvestment in the business rather than distributed as dividends. This crucial connection demonstrates how a company’s profitability over a period directly impacts its financial position.

Net income essentially acts as the bridge, translating the operational performance detailed in the income statement into an adjustment of the equity section of the balance sheet. Retained earnings, a component of shareholders’ equity, increases when a company reports a net income and decreases when there’s a net loss or when dividends are paid out to shareholders. Understanding this flow is critical for investors and analysts as it reflects the company’s ability to generate profits and its decisions regarding reinvestment versus distribution of earnings. According to a study by the University of Texas at Austin’s McCombs School of Business, companies with consistent positive net income and strategic reinvestment policies often exhibit stronger long-term growth potential.

2. How Does Net Income from the Income Statement Affect the Balance Sheet?

Net income directly impacts the balance sheet by increasing or decreasing the retained earnings. A positive net income increases the retained earnings, while a net loss decreases it. Retained earnings is a component of shareholders’ equity, so net income effectively contributes to the overall equity position of the company.

This is a fundamental accounting relationship that reflects the accumulation of profits over time. When a company earns a profit (net income), that profit is added to the retained earnings account, boosting the equity portion of the balance sheet. Conversely, when a company incurs a loss (net loss), that loss is subtracted from the retained earnings, decreasing the equity. This mechanism ensures that the balance sheet reflects the cumulative financial performance of the company since its inception. For example, if a company has $1 million in retained earnings at the beginning of the year and generates a net income of $200,000 during the year, the retained earnings at the end of the year will be $1.2 million (assuming no dividends are paid). This increase in retained earnings strengthens the company’s financial position, making it more attractive to investors and lenders.

3. How Do Assets, Liabilities, and Equity on the Balance Sheet Relate to the Income Statement?

Assets, liabilities, and equity on the balance sheet relate to the income statement through various transactions that impact both. For example, depreciation of assets affects the income statement as an expense and reduces the asset’s book value on the balance sheet. Interest expense on liabilities appears on the income statement and is linked to the debt balance on the balance sheet. Revenue generation increases assets (e.g., cash or accounts receivable) and is reported on the income statement.

The interconnection is multifaceted and critical for understanding a company’s financial health. Here’s a breakdown:

- Revenue and Assets: Sales (revenue) reported on the income statement often result in an increase in assets, such as cash or accounts receivable, on the balance sheet.

- Expenses and Liabilities: Expenses on the income statement can create or increase liabilities on the balance sheet. For example, accrued expenses (expenses incurred but not yet paid) are reported as liabilities.

- Depreciation and PP&E: Depreciation expense on the income statement reflects the reduction in the value of fixed assets (Property, Plant, and Equipment) on the balance sheet.

- Cost of Goods Sold (COGS) and Inventory: COGS on the income statement is directly related to the inventory asset on the balance sheet. As inventory is sold, its cost is transferred to COGS.

- Debt and Interest Expense: The amount of debt a company has (a liability on the balance sheet) directly influences the interest expense reported on the income statement.

- Equity and Net Income: As previously discussed, net income (or loss) ultimately affects the retained earnings, a component of shareholders’ equity on the balance sheet.

These relationships highlight how the balance sheet provides a snapshot of what a company owns (assets) and owes (liabilities), as well as the owners’ stake (equity) at a specific point in time, while the income statement summarizes the company’s financial performance over a period.

4. Why Is Understanding the Link Between These Financial Statements Important for Businesses?

Understanding the link between the balance sheet and income statement is crucial for businesses because it provides a holistic view of financial performance and position. It allows for better decision-making, strategic planning, and accurate financial modeling. This understanding helps in assessing profitability, solvency, and overall financial health, which are essential for attracting investors, securing loans, and managing operations effectively.

A comprehensive grasp of these connections enables businesses to:

- Assess Profitability and Solvency: By understanding how net income flows into retained earnings, businesses can assess their ability to generate profits and maintain long-term solvency.

- Make Informed Decisions: Linking financial data helps in making informed decisions about investments, financing, and operational strategies.

- Attract Investors and Secure Loans: A clear understanding of these links can improve financial reporting, making the business more attractive to investors and lenders.

- Plan Strategically: Businesses can use this knowledge to develop strategic plans that align with their financial goals and ensure sustainable growth.

- Manage Operations Effectively: Understanding the relationship between expenses and liabilities, as well as revenue and assets, can help businesses manage their operations more efficiently.

According to a study by Harvard Business Review, companies that effectively integrate their financial statements into their strategic planning process are more likely to achieve their financial objectives and maintain a competitive edge. This is especially crucial for businesses seeking strategic partnerships to expand their operations and boost revenues, as a deep understanding of their own financial standing helps them identify the most beneficial alliances.

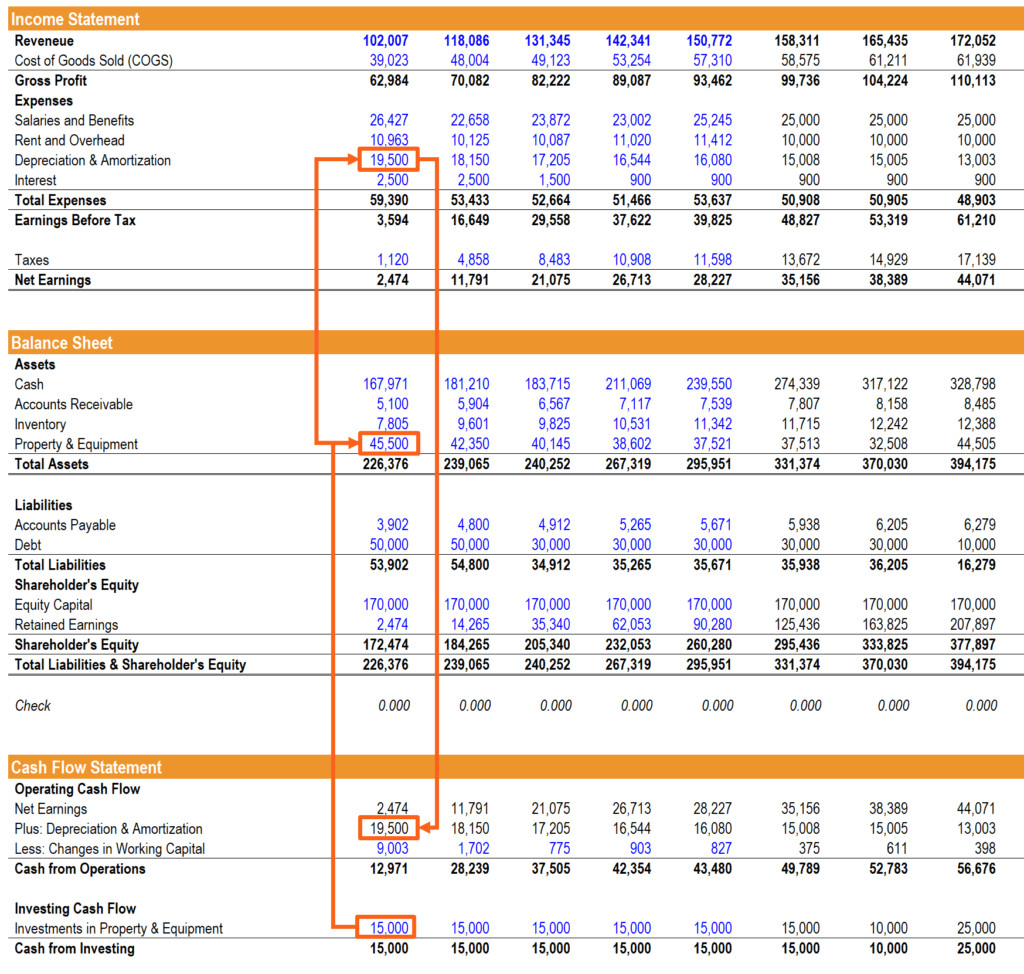

5. How Does Depreciation Connect the Balance Sheet and Income Statement?

Depreciation connects the balance sheet and income statement by allocating the cost of a fixed asset over its useful life. On the income statement, depreciation is recorded as an expense, reducing net income. On the balance sheet, the accumulated depreciation reduces the book value of the asset, reflecting the asset’s decline in value over time.

Here’s a more detailed explanation:

- Income Statement: Depreciation expense represents the portion of a fixed asset’s cost that is recognized as an expense during a specific accounting period. This expense reduces the company’s net income, reflecting the consumption of the asset’s economic benefits.

- Balance Sheet: Fixed assets (such as property, plant, and equipment) are initially recorded at their historical cost. As the asset is used, depreciation is accumulated over time. The accumulated depreciation is a contra-asset account that reduces the asset’s book value (original cost less accumulated depreciation).

For instance, if a company purchases a machine for $100,000 with an estimated useful life of 10 years and uses the straight-line depreciation method, the annual depreciation expense would be $10,000. Each year, $10,000 is recorded as depreciation expense on the income statement, and the accumulated depreciation on the balance sheet increases by $10,000. After five years, the machine’s book value on the balance sheet would be $50,000 ($100,000 original cost less $50,000 accumulated depreciation). This connection ensures that the cost of using the asset is recognized over its useful life, providing a more accurate picture of the company’s financial performance and position.

Depreciation Connects Balance Sheet and Income Statement

Depreciation Connects Balance Sheet and Income Statement

6. How Does Capital Expenditure (CAPEX) Affect Both Financial Statements?

Capital expenditure (CAPEX) affects both financial statements because it represents investments in fixed assets. CAPEX is not immediately expensed on the income statement; instead, it is capitalized on the balance sheet as an asset. Over time, this asset is depreciated, and the depreciation expense is recognized on the income statement. CAPEX also impacts the cash flow statement as an outflow in the investing activities section.

The journey of CAPEX through the financial statements can be detailed as follows:

- Balance Sheet: When a company incurs CAPEX, it increases its fixed assets (Property, Plant, and Equipment) on the balance sheet. The asset is recorded at its historical cost.

- Income Statement: CAPEX itself is not reported on the income statement. However, the depreciation expense related to these assets is recorded on the income statement over the asset’s useful life.

- Cash Flow Statement: The cash outflow for CAPEX is reported in the investing activities section of the cash flow statement. This reflects the actual cash spent on acquiring the fixed asset.

For example, suppose a company spends $500,000 on new equipment. This $500,000 is recorded as an increase in fixed assets on the balance sheet and as a cash outflow in the investing activities section of the cash flow statement. Over the asset’s useful life, a portion of its cost is recognized as depreciation expense on the income statement, reducing net income.

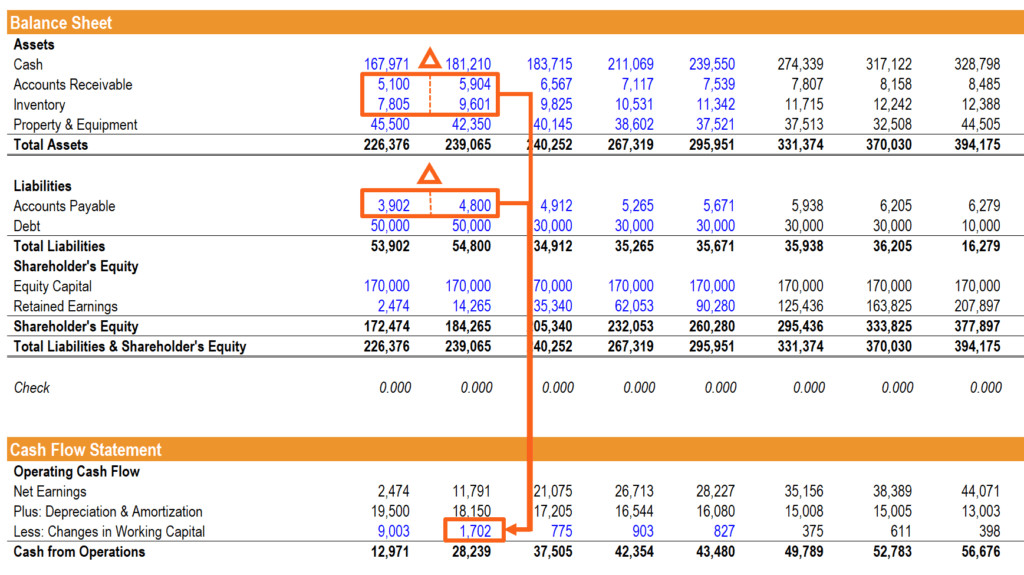

7. How Does Working Capital Link the Income Statement and Balance Sheet?

Working capital links the income statement and balance sheet through current assets and current liabilities. Changes in these accounts impact the cash flow from operations, which in turn affects the cash balance on the balance sheet. Additionally, revenue and expenses on the income statement are directly related to accounts like accounts receivable, accounts payable, and inventory, which are components of working capital.

Net working capital (NWC) is calculated as current assets minus current liabilities. Here’s how changes in these accounts affect the financial statements:

- Accounts Receivable: Revenue from the income statement that hasn’t been collected yet is recorded as accounts receivable on the balance sheet. An increase in accounts receivable means more revenue has been earned but not yet received in cash.

- Inventory: The cost of goods sold (COGS) on the income statement is directly related to the inventory account on the balance sheet. As inventory is sold, its cost is transferred to COGS.

- Accounts Payable: Expenses incurred but not yet paid are recorded as accounts payable on the balance sheet. An increase in accounts payable means the company has incurred more expenses but hasn’t yet paid them in cash.

For example, if a company increases its sales (revenue on the income statement) and extends credit to its customers, accounts receivable (a current asset on the balance sheet) will increase. This increase in accounts receivable will be reflected as an adjustment in the cash flow from operations on the cash flow statement, affecting the cash balance on the balance sheet. Efficient management of working capital is essential for maintaining liquidity and ensuring that the company can meet its short-term obligations.

Balance Sheet Linked to Cash Flow Statement

Balance Sheet Linked to Cash Flow Statement

8. How Do Financing Activities Affect Both the Income Statement and Balance Sheet?

Financing activities affect both the income statement and balance sheet primarily through debt and equity. When a company issues debt, it increases liabilities on the balance sheet, and the related interest expense is reported on the income statement. Equity financing, such as issuing stock, increases equity on the balance sheet, and any dividends paid to shareholders reduce retained earnings.

Here’s a breakdown of the effects:

-

Debt Financing:

- Balance Sheet: Issuing debt increases the company’s liabilities (e.g., loans payable or bonds payable).

- Income Statement: The interest expense associated with the debt is recorded on the income statement, reducing net income.

- Cash Flow Statement: The proceeds from issuing debt are recorded as an inflow in the financing activities section, while the repayment of debt principal is recorded as an outflow.

-

Equity Financing:

- Balance Sheet: Issuing stock increases the company’s equity (e.g., common stock or preferred stock).

- Income Statement: Issuing stock itself does not directly affect the income statement. However, dividends paid to shareholders reduce retained earnings, which indirectly impacts the income statement over time.

- Cash Flow Statement: The proceeds from issuing stock are recorded as an inflow in the financing activities section.

For example, if a company issues $1 million in bonds, the balance sheet will show a $1 million increase in liabilities. The annual interest payments on the bonds will be recorded as interest expense on the income statement, reducing net income. The initial receipt of $1 million is reflected as a cash inflow in the financing activities section of the cash flow statement.

9. How Does the Cash Balance Act as the Final Link Between the Three Statements?

The cash balance acts as the final link because it is affected by all activities reported on the other two statements. The cash flow statement summarizes the changes in cash resulting from operating, investing, and financing activities. The ending cash balance on the cash flow statement is then reported on the balance sheet, ensuring that the balance sheet reflects all cash inflows and outflows that occurred during the period.

Here’s a detailed explanation:

- Income Statement: Net income (or loss) from the income statement is a key input in calculating cash flow from operations on the cash flow statement. Adjustments are made for non-cash items like depreciation and changes in working capital accounts.

- Balance Sheet: The balance sheet provides the beginning and ending balances of assets, liabilities, and equity accounts, which are used to calculate changes in working capital and other cash flow items.

- Cash Flow Statement: The cash flow statement reconciles the changes in cash resulting from operating, investing, and financing activities. The ending cash balance on the cash flow statement must match the cash balance reported on the balance sheet.

The interconnectedness ensures that all financial activities are properly reflected across the financial statements. The sum of cash from operations, investing, and financing activities is added to the prior period’s closing cash balance to arrive at the current period’s closing cash balance on the balance sheet.

10. What Are Some Common Errors in Linking the Financial Statements and How Can They Be Avoided?

Common errors in linking the financial statements include incorrectly calculating depreciation, mismanaging working capital changes, and failing to properly account for debt and equity financing. To avoid these errors, ensure accurate data entry, maintain detailed schedules for depreciation and debt, and thoroughly understand the accounting principles underlying each transaction.

Here are some specific errors and how to avoid them:

- Incorrect Depreciation Calculation:

- Error: Using an incorrect depreciation method, useful life, or salvage value.

- Solution: Maintain a detailed depreciation schedule that accurately tracks the depreciation method, useful life, and salvage value for each asset. Double-check calculations and ensure consistency with accounting standards.

- Mismanagement of Working Capital Changes:

- Error: Incorrectly calculating changes in accounts receivable, inventory, and accounts payable.

- Solution: Carefully analyze changes in working capital accounts and understand their impact on cash flow. Use a consistent approach to calculate these changes and reconcile them with the income statement and balance sheet.

- Failure to Properly Account for Debt and Equity Financing:

- Error: Incorrectly recording the issuance or repayment of debt, interest expense, or equity transactions.

- Solution: Maintain detailed debt and equity schedules that track the principal amount, interest rate, repayment terms, and equity issuances. Ensure that interest expense is accurately recorded on the income statement and that debt and equity transactions are properly reflected on the balance sheet and cash flow statement.

- Mathematical Errors and Formula Mistakes:

- Error: Using incorrect formulas or making mathematical errors in calculations.

- Solution: Double-check all formulas and calculations. Use spreadsheet software with built-in error-checking features and regularly audit the financial statements to identify and correct any errors.

By paying close attention to these areas and implementing robust internal controls, businesses can ensure the accurate and reliable linking of their financial statements.

Example of Linking Income Statement to Balance Sheet

Example of Linking Income Statement to Balance Sheet

Partnering for Profit: How income-partners.net Can Help

At income-partners.net, we understand the intricate dance between the balance sheet and income statement. Our platform is designed to help you navigate these financial relationships and find strategic partners who align with your financial goals. Whether you’re looking to expand your market reach, innovate your product line, or simply boost your bottom line, we connect you with partners who can help you achieve sustainable growth.

Discover the Power of Strategic Partnerships

Unlock new revenue streams and growth opportunities by leveraging the expertise and resources of our network. income-partners.net offers:

- Diverse Partnership Opportunities: Explore various types of partnerships tailored to your specific business needs.

- Expert Guidance: Access resources and tools to evaluate potential partners and structure mutually beneficial agreements.

- Data-Driven Insights: Make informed decisions based on comprehensive financial data and performance metrics.

Ready to take your business to the next level? Visit income-partners.net today and start building partnerships that drive profitability and long-term success.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

FAQ: Understanding the Balance Sheet and Income Statement Connection

- What is the basic accounting equation and how does it relate to the balance sheet?

- The basic accounting equation is Assets = Liabilities + Equity. It represents the foundation of the balance sheet, showing that a company’s assets are financed by either liabilities (what it owes to others) or equity (the owners’ stake).

- How do changes in retained earnings affect a company’s financial stability?

- An increase in retained earnings generally indicates improved financial stability, as it shows the company is profitable and reinvesting in its operations. A decrease may signal financial difficulties or significant dividend payouts.

- What role does the cash flow statement play in understanding the link between the balance sheet and income statement?

- The cash flow statement reconciles net income with the actual cash inflows and outflows, providing insights into how a company manages its cash and highlighting discrepancies between reported profits and cash balances.

- How can businesses use the information from these financial statements to improve their creditworthiness?

- By demonstrating consistent profitability, effective asset management, and responsible debt management through these statements, businesses can improve their creditworthiness and attract favorable loan terms.

- What are some key financial ratios that rely on data from both the balance sheet and income statement?

- Key ratios include Return on Equity (ROE), Debt-to-Equity ratio, and Profit Margin. These ratios provide a comprehensive view of a company’s profitability, leverage, and efficiency.

- How can investors use these financial statements to assess a company’s investment potential?

- Investors can analyze these statements to assess a company’s profitability, solvency, and growth potential, making informed decisions about whether to invest in the company.

- Why is it important to reconcile the ending cash balance on the cash flow statement with the cash balance on the balance sheet?

- Reconciling these balances ensures the accuracy of the financial statements and verifies that all cash inflows and outflows have been properly accounted for, providing confidence in the financial reporting process.

- How do non-cash expenses, such as depreciation, affect the cash flow statement and the link between the balance sheet and income statement?

- Non-cash expenses are added back to net income on the cash flow statement to reflect the actual cash generated from operations, highlighting the differences between reported profits and cash flows.

- What are some red flags that analysts look for when examining the relationships between these financial statements?

- Red flags include inconsistent revenue recognition, unusual increases in debt, and declining profitability, which may indicate financial mismanagement or fraudulent activities.

- How can understanding these financial statement links help a business owner make better operational decisions?

- By understanding how operational decisions impact the financial statements, business owners can make informed choices about pricing, inventory management, and capital investments to optimize profitability and financial health.