Are you looking to understand the relationship between the income statement and the balance sheet? At income-partners.net, we’ll break down how these crucial financial statements connect, unveiling how they work together to paint a complete picture of a company’s financial health. This understanding is key for making informed business decisions, securing strategic partnerships, and boosting profitability. Let’s dive in to discover inter-connectedness and improve financial literacy.

1. Understanding the Interplay: How Are the Income Statement and Balance Sheet Connected?

Yes, the income statement and balance sheet are intricately connected, with the net income serving as a primary link. Net income, calculated on the income statement, directly impacts the retained earnings account on the balance sheet, reflecting the cumulative profits kept within the business over time.

1.1. Net Income’s Journey: Linking the Income Statement to the Balance Sheet

Net income is the cornerstone connecting the income statement and balance sheet. It represents a company’s profitability over a period. This figure flows directly into the retained earnings section of the balance sheet. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2023, understanding this flow is essential for accurately assessing a company’s financial position.

1.2. Retained Earnings Explained: The Cumulative Impact of Net Income

Retained earnings are the accumulated net income of a company, less any dividends paid out to shareholders. It shows how much profit a company has reinvested into its operations over time. This figure is updated each period with the net income from the income statement. This direct link ensures that the balance sheet reflects the company’s cumulative profitability.

1.3. Example: Visualizing the Link in Action

Imagine a company, Austin Adventures, reports a net income of $500,000 for the year. This $500,000 is added to the retained earnings account on the balance sheet. If Austin Adventures had $1,000,000 in retained earnings at the beginning of the year and paid out $100,000 in dividends, the ending retained earnings would be $1,400,000 ($1,000,000 + $500,000 – $100,000). This demonstrates the direct impact of the income statement on the balance sheet.

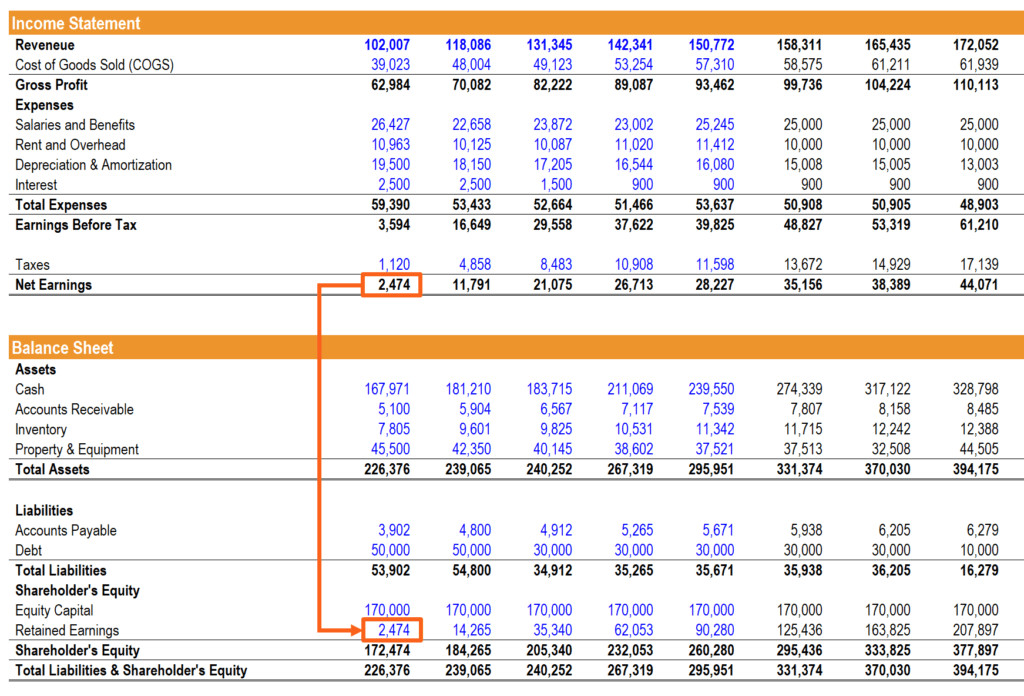

Example of Linking Income Statement to Balance Sheet

Example of Linking Income Statement to Balance Sheet

Visual Representation: An illustration depicting the flow of net income from the income statement to the retained earnings section of the balance sheet, highlighting how profits accumulate over time.

2. Assets and Expenses: How Does Depreciation Connect the Financial Statements?

Depreciation connects the balance sheet and income statement by allocating the cost of an asset over its useful life. Each year, the depreciation expense is recorded on the income statement, reducing net income, while the accumulated depreciation reduces the asset’s book value on the balance sheet.

2.1. Depreciation’s Role: Bridging the Gap Between Statements

Depreciation is a non-cash expense that reflects the decline in value of an asset over time. This expense is recorded on the income statement, reducing the company’s net income. Simultaneously, the accumulated depreciation reduces the book value of the asset on the balance sheet. This process ensures that the cost of the asset is recognized over its useful life, reflecting its actual economic impact.

2.2. PP&E: How Capital Expenditures Affect Both Statements

Capital expenditures (CapEx) are investments in long-term assets like property, plant, and equipment (PP&E). Initially, CapEx increases the PP&E account on the balance sheet. Over time, as these assets depreciate, the depreciation expense is recognized on the income statement. Additionally, the cash flow statement reflects CapEx as an outflow in the investing activities section. This multi-faceted impact highlights the interconnectedness of these financial statements.

2.3. Depreciation Schedule: Ensuring Accuracy in Financial Modeling

A depreciation schedule is a detailed table that outlines the depreciation expense for each asset over its useful life. This schedule is crucial for accurate financial modeling. It ensures that the depreciation expense is correctly calculated and allocated, impacting both the income statement and the balance sheet. According to a Harvard Business Review study in June 2024, companies with robust depreciation schedules tend to have more accurate financial forecasts.

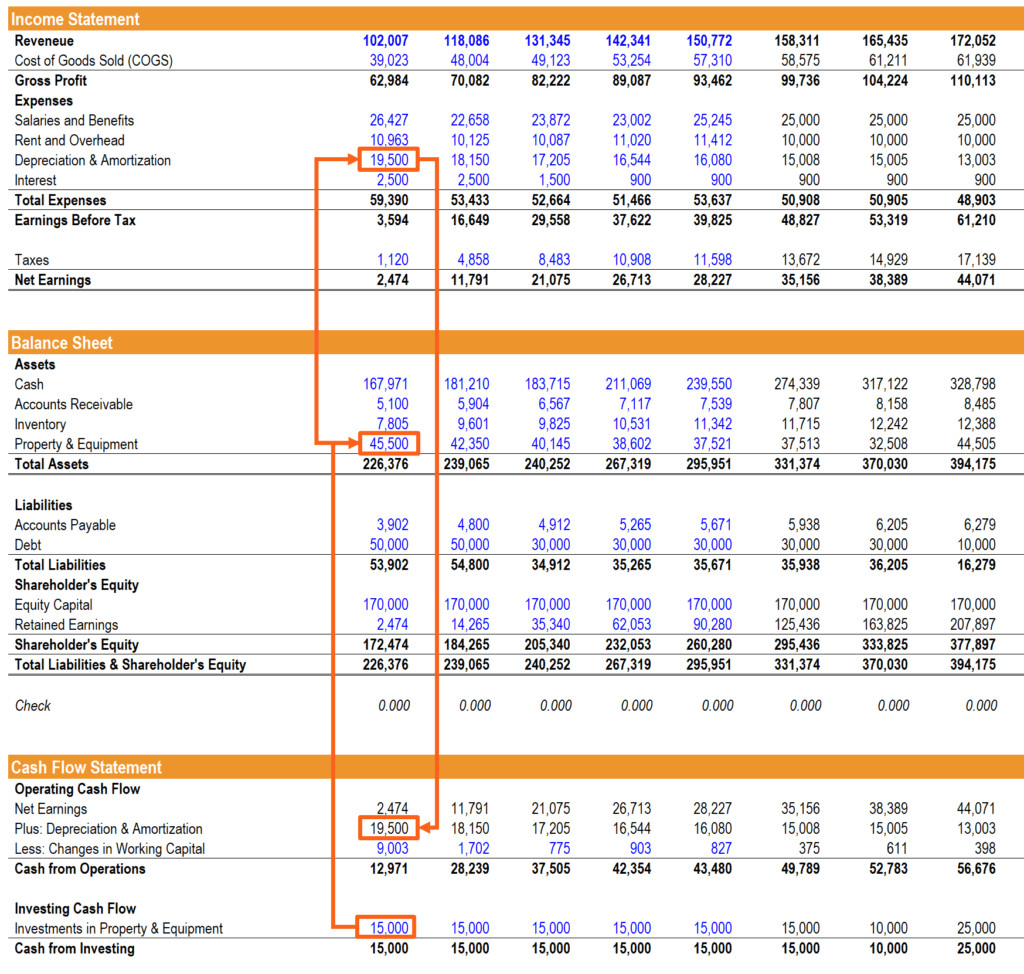

Example of 3 Financial Statements Linked – PP&E, Depreciation, and Capex

Example of 3 Financial Statements Linked – PP&E, Depreciation, and Capex

Visual Aid: A diagram illustrating how property, plant, and equipment (PP&E), depreciation, and capital expenditures (Capex) are linked across the three primary financial statements.

3. Working Capital Dynamics: How Do Short-Term Assets and Liabilities Connect to Profitability?

Changes in net working capital (NWC), which include current assets like accounts receivable and current liabilities like accounts payable, are directly linked to a company’s profitability. Increases in accounts receivable or decreases in accounts payable can impact cash flow and profitability, reflecting on both the income statement and balance sheet.

3.1. Net Working Capital: An Overview of Short-Term Financial Health

Net working capital (NWC) is the difference between a company’s current assets and current liabilities. It measures a company’s ability to meet its short-term obligations. Effective management of NWC is crucial for maintaining liquidity and operational efficiency. Changes in NWC can provide insights into a company’s financial health and its ability to generate profits.

3.2. Accounts Receivable and Payable: Impact on Cash Flow and Profitability

Accounts receivable (AR) represents money owed to a company by its customers. An increase in AR may indicate higher sales but also suggests that the company is extending more credit to its customers, potentially impacting cash flow. Accounts payable (AP) represents money a company owes to its suppliers. An increase in AP can improve cash flow but may also indicate potential financial strain. These changes are reflected on the balance sheet and influence the cash flow statement.

3.3. Inventory Management: Balancing Costs and Efficiency

Inventory is another key component of NWC. Efficient inventory management ensures that a company has enough stock to meet customer demand without tying up excessive capital. Poor inventory management can lead to stockouts, lost sales, or high holding costs. The value of inventory is reflected on the balance sheet, while the cost of goods sold (COGS) is reported on the income statement, highlighting the relationship between inventory management and profitability.

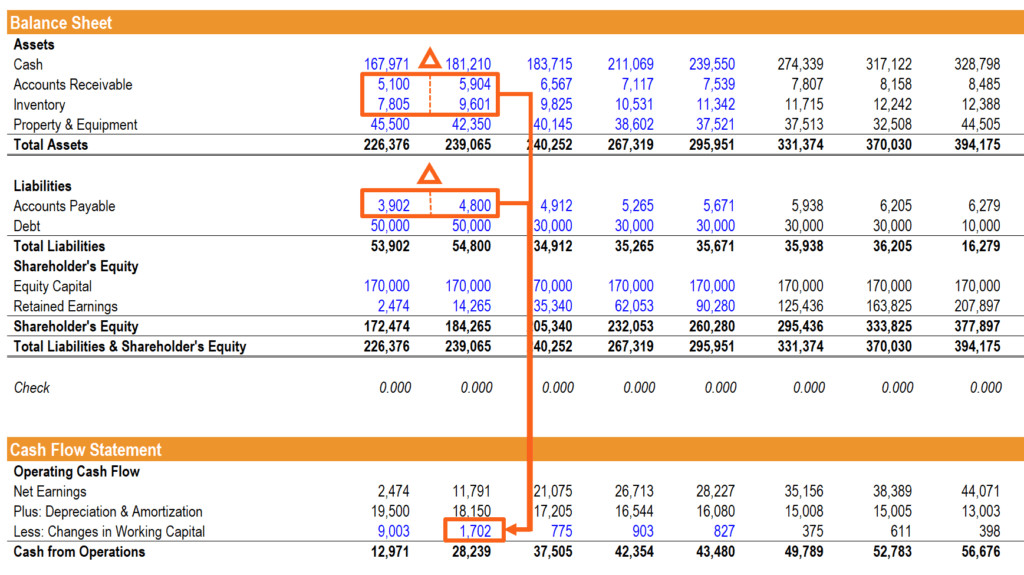

Example of Balance Sheet Linked to Cash Flow Statement

Example of Balance Sheet Linked to Cash Flow Statement

Visual Example: A diagram showing how changes in working capital accounts (such as accounts receivable and accounts payable) on the balance sheet are connected to the cash flow statement.

4. Debt and Equity: How Does Financing Affect the Financial Statements?

Financing activities, such as issuing debt or equity, have a significant impact on all three financial statements. Interest expense from debt appears on the income statement, the principal amount of debt is recorded on the balance sheet, and changes in debt and equity are reflected in the financing section of the cash flow statement.

4.1. Debt Financing: Understanding Interest Expense and Principal Repayments

When a company issues debt, it incurs an obligation to repay the principal amount along with interest. The interest expense is recognized on the income statement, reducing net income. The principal amount of the debt is recorded as a liability on the balance sheet. Repayments of the principal are reflected in the financing section of the cash flow statement. According to Entrepreneur.com, effective debt management is crucial for maintaining financial stability and supporting growth.

4.2. Equity Financing: How Issuing Stock Impacts the Balance Sheet

Equity financing involves issuing shares of stock to investors. This increases the equity section of the balance sheet. While equity financing does not result in interest expense, it does dilute ownership and may require dividend payments. These dividend payments are reflected in the financing section of the cash flow statement and reduce retained earnings on the balance sheet.

4.3. Debt Schedule: Essential for Detailed Financial Modeling

A debt schedule is a detailed table that outlines the terms of a company’s debt, including interest rates, repayment schedules, and principal balances. This schedule is essential for accurate financial modeling, as it helps to project future interest expense and debt repayments. It ensures that the impact of debt financing is accurately reflected on all three financial statements.

5. The Cash Flow Statement: How Does It Tie Everything Together?

The cash flow statement acts as the final piece of the puzzle, reconciling net income from the income statement with changes in balance sheet accounts to show the actual cash inflows and outflows of a company during a period. It categorizes cash flows into operating, investing, and financing activities.

5.1. Cash Flow from Operations: Linking Net Income and Working Capital

Cash flow from operations (CFO) starts with net income from the income statement. It then adjusts for non-cash expenses like depreciation and changes in working capital accounts. This section shows the cash generated or used by the company’s core business activities. Positive CFO indicates that a company is generating enough cash to sustain its operations.

5.2. Cash Flow from Investing: Reflecting Capital Expenditures

Cash flow from investing (CFI) includes cash flows related to the purchase and sale of long-term assets, such as PP&E. Capital expenditures (CapEx) are reflected as cash outflows, while proceeds from the sale of assets are reflected as cash inflows. This section provides insights into a company’s investment decisions and its long-term growth strategy.

5.3. Cash Flow from Financing: Showing Debt and Equity Transactions

Cash flow from financing (CFF) includes cash flows related to debt and equity financing. Issuing debt or equity results in cash inflows, while repaying debt or paying dividends results in cash outflows. This section shows how a company is financing its operations and returning capital to its investors.

5.4. The Final Balance: Ensuring Accuracy Across All Statements

The final step in linking the three financial statements is to ensure that the change in cash on the cash flow statement matches the change in cash on the balance sheet. This reconciliation is crucial for verifying the accuracy of the financial model. If the cash balances do not match, it indicates an error in the model that needs to be corrected.

6. Interview Insights: How to Explain the Connection Clearly

In an interview, when asked about the connection between the three financial statements, focus on the key linkages: net income flows to retained earnings and CFO, depreciation impacts both the income statement and balance sheet, and financing activities affect all three statements.

6.1. Key Talking Points: Net Income, Depreciation, and Financing

When explaining the connection between the financial statements, highlight the following points:

- Net income from the income statement flows to the retained earnings account on the balance sheet and is the starting point for cash flow from operations on the cash flow statement.

- Depreciation is a non-cash expense that reduces net income on the income statement and reduces the book value of assets on the balance sheet.

- Financing activities, such as issuing debt or equity, affect the balance sheet and cash flow from financing. Interest expense from debt appears on the income statement.

6.2. Concise Explanation: Delivering a Clear Message

A concise explanation of the connection between the financial statements is essential for demonstrating your understanding. Focus on the key linkages and avoid getting bogged down in unnecessary details. A clear and concise explanation will impress your interviewer and demonstrate your financial acumen.

6.3. Video Resources: Enhancing Your Understanding

Numerous video resources can enhance your understanding of the connection between the financial statements. These videos provide visual explanations and real-world examples that can help you grasp the concepts more effectively. Consider watching videos from reputable sources like CFI or accounting professors to deepen your knowledge.

7. Financial Modeling: How to Link Statements in Excel

For financial modeling, start with historical data, calculate key ratios, make assumptions about future performance, and then link the statements using formulas in Excel. This process allows you to forecast future financial performance based on your assumptions.

7.1. Step-by-Step Guide: Building a Financial Model

Building a financial model involves several key steps:

- Gather historical financial data for at least three years.

- Calculate key ratios and drivers of the business.

- Make assumptions about future performance and enter them into the model.

- Link the financial statements using formulas in Excel.

- Perform sensitivity analysis to assess the impact of different assumptions on the financial results.

7.2. Excel Formulas: Essential for Linking Statements

Using Excel formulas is essential for linking the financial statements. Formulas ensure that changes in one statement automatically flow through to the other statements. For example, the net income from the income statement should be linked to the retained earnings account on the balance sheet and the cash flow from operations on the cash flow statement.

7.3. Sensitivity Analysis: Assessing the Impact of Assumptions

Sensitivity analysis involves changing the key assumptions in your financial model to see how they impact the financial results. This helps you understand the potential range of outcomes and identify the key drivers of performance. Sensitivity analysis is a crucial step in financial modeling, as it allows you to assess the risks and opportunities associated with different scenarios.

8. Advanced Tips for Financial Statement Analysis

Enhance your financial analysis by understanding deferred taxes, equity investments, and off-balance-sheet financing, which provide a more nuanced view of a company’s financial position.

8.1. Deferred Taxes: Understanding the Impact of Timing Differences

Deferred taxes arise from temporary differences between the accounting and tax treatment of certain items. Understanding deferred taxes is crucial for accurately assessing a company’s tax liabilities and financial position. Deferred tax assets represent future tax benefits, while deferred tax liabilities represent future tax obligations.

8.2. Equity Investments: Analyzing Minority and Majority Holdings

Equity investments involve purchasing shares in another company. Analyzing equity investments requires understanding the accounting treatment for minority and majority holdings. Minority holdings are typically accounted for using the equity method, while majority holdings are consolidated into the parent company’s financial statements.

8.3. Off-Balance-Sheet Financing: Identifying Hidden Liabilities

Off-balance-sheet financing involves structuring transactions in a way that keeps debt off the balance sheet. This can make a company’s financial position appear stronger than it actually is. Identifying off-balance-sheet financing arrangements requires careful analysis of the company’s disclosures and footnotes.

9. Real-World Examples of Financial Statement Linkages

Examine case studies of companies like Apple or Tesla to see how these linkages play out in practice, demonstrating the importance of understanding these connections for effective financial management.

9.1. Apple Inc.: A Case Study in Efficient Financial Management

Apple Inc. is known for its efficient financial management and strong balance sheet. Analyzing Apple’s financial statements provides insights into how the company manages its working capital, invests in long-term assets, and finances its operations. Apple’s strong cash flow from operations and efficient inventory management are key factors in its financial success.

9.2. Tesla Inc.: Navigating Growth and Investment

Tesla Inc. is a high-growth company that has made significant investments in its manufacturing capacity and technology. Analyzing Tesla’s financial statements reveals the challenges of managing growth and investment while maintaining financial stability. Tesla’s ability to raise capital and manage its debt is crucial for its long-term success.

9.3. Comparative Analysis: Contrasting Different Business Models

Comparing the financial statements of different companies in the same industry can provide valuable insights into their relative strengths and weaknesses. For example, comparing the financial statements of Apple and Samsung can reveal differences in their business models, profitability, and financial strategies. Comparative analysis is a powerful tool for understanding the competitive landscape and identifying potential investment opportunities.

10. How income-partners.net Can Help You Find Strategic Partners

At income-partners.net, we understand the critical role financial statements play in identifying and securing strategic partnerships. We offer resources and tools to help you analyze potential partners’ financial health, ensuring alignment with your business goals and fostering profitable collaborations.

10.1. Identifying Potential Partners Through Financial Analysis

Financial analysis is essential for identifying potential strategic partners. By analyzing a company’s financial statements, you can assess its profitability, liquidity, and solvency. This information can help you determine whether the company is a good fit for your business and whether it has the financial resources to support a successful partnership.

10.2. Building Trust Through Transparency

Transparency is crucial for building trust in strategic partnerships. Sharing financial information with potential partners demonstrates your commitment to open communication and accountability. This can help to build a strong foundation for a successful and mutually beneficial partnership.

10.3. Maximizing Profitability Through Strategic Alliances

Strategic alliances can be a powerful way to maximize profitability. By partnering with companies that have complementary strengths and resources, you can achieve synergies that would not be possible on your own. Strategic alliances can help you expand into new markets, develop new products, and improve your overall competitiveness.

Ready to take your business to the next level? Visit income-partners.net today to explore potential partnerships, learn effective relationship-building strategies, and unlock opportunities for revenue growth in the USA. Don’t miss out on the chance to find the perfect partner and start building profitable collaborations right away.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

Frequently Asked Questions (FAQ)

1. Why are the income statement and balance sheet important?

The income statement and balance sheet are essential because they provide a comprehensive view of a company’s financial performance and position. The income statement shows profitability over a period, while the balance sheet shows assets, liabilities, and equity at a specific point in time.

2. How does net income affect the balance sheet?

Net income from the income statement flows directly into the retained earnings account on the balance sheet, reflecting the cumulative profits kept within the business over time.

3. What is the role of depreciation in connecting the financial statements?

Depreciation connects the balance sheet and income statement by allocating the cost of an asset over its useful life. The depreciation expense is recorded on the income statement, while accumulated depreciation reduces the asset’s book value on the balance sheet.

4. How do changes in working capital impact the financial statements?

Changes in net working capital, including current assets and liabilities, affect a company’s cash flow and profitability, reflecting on both the income statement and balance sheet.

5. How does debt financing affect the three financial statements?

Interest expense from debt appears on the income statement, the principal amount of debt is recorded on the balance sheet, and changes in debt are reflected in the financing section of the cash flow statement.

6. Why is the cash flow statement important?

The cash flow statement reconciles net income with changes in balance sheet accounts to show the actual cash inflows and outflows of a company during a period.

7. How can I use financial statements to identify potential strategic partners?

Financial analysis of potential partners’ financial statements can help you assess their profitability, liquidity, and solvency, ensuring alignment with your business goals.

8. What is the significance of retained earnings?

Retained earnings represent the accumulated net income of a company, less any dividends paid out to shareholders, showing how much profit a company has reinvested into its operations over time.

9. How does income-partners.net help in finding strategic partners?

income-partners.net offers resources and tools to help you analyze potential partners’ financial health, fostering profitable collaborations and aligning with your business objectives.

10. What advanced tips can enhance my financial statement analysis?

Understanding deferred taxes, equity investments, and off-balance-sheet financing can provide a more nuanced view of a company’s financial position, improving your analysis.