Does Your Income Level Affect Your Saving Habits? Absolutely, your income level significantly influences your saving habits, impacting everything from the amount you save to your financial security. This is where strategic partnerships become invaluable for boosting income and optimizing savings, and income-partners.net can guide you in forging these beneficial alliances. Understanding the correlation between income and saving habits is key to enhancing your financial well-being, identifying opportunities for wealth accumulation, and implementing effective financial strategies.

1. The Intimate Relationship Between Income and Saving Habits

The relationship between income and saving habits is a cornerstone of personal finance, deeply influencing an individual’s financial well-being and future security. Higher income often correlates with increased savings, while lower income can present significant challenges in setting aside funds. This dynamic is crucial for understanding how different income levels affect financial behaviors and overall economic stability.

- Higher Income: Individuals with higher incomes typically have more discretionary funds available after covering essential expenses. This surplus allows them to save a larger percentage of their income, invest in various assets, and build a substantial financial cushion. Higher earners also tend to have greater access to financial planning resources, enabling them to make informed decisions about their savings and investments.

- Lower Income: Conversely, individuals with lower incomes often struggle to save due to the necessity of allocating most or all of their earnings to basic needs such as housing, food, and healthcare. This can create a cycle where saving becomes exceedingly difficult, hindering their ability to achieve financial security and long-term goals. Unexpected expenses can further derail savings efforts, leading to increased debt and financial instability.

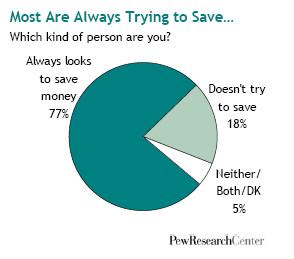

People describe themselves as the kind of person who “always looks for ways to save money”

People describe themselves as the kind of person who “always looks for ways to save money”

1.1. Examining Saving Trends Across Income Brackets

To further illustrate this relationship, let’s examine specific saving trends across different income brackets. According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, distinct patterns emerge as income levels vary.

| Income Bracket | Average Savings Rate | Common Saving Goals |

|---|---|---|

| Lower Income (Under $40k) | 0-5% | Emergency fund, basic necessities, debt reduction |

| Middle Income ($40k-$100k) | 5-15% | Retirement, education, home purchase |

| Upper Income (Over $100k) | 15%+ | Investments, wealth accumulation, estate planning |

These trends highlight how income directly impacts the ability to save and the types of financial goals individuals can pursue. Lower-income individuals often prioritize immediate needs and debt repayment, while higher-income individuals focus on long-term investments and wealth building.

1.2. Psychological Factors Influencing Saving Habits

Beyond the practical constraints of income, psychological factors also play a significant role in shaping saving habits. These factors can affect individuals across all income levels, influencing their attitudes toward money, risk tolerance, and financial planning.

- Financial Literacy: A lack of financial knowledge can hinder effective saving and investment strategies, regardless of income.

- Risk Aversion: Lower-income individuals may be more risk-averse due to financial insecurity, limiting their investment options.

- Present Bias: The tendency to prioritize immediate gratification over future rewards can lead to undersaving, particularly among those with limited resources.

- Financial Anxiety: Stress and worry about money can negatively impact financial decision-making and saving habits.

Addressing these psychological barriers through education, counseling, and access to financial resources can help individuals develop healthier saving habits and improve their financial well-being.

2. Key Statistics on Income and Savings in the US

Understanding the current state of savings in the United States requires examining key statistics and trends related to income and savings rates. These figures provide valuable insights into the financial health of Americans across different income levels and demographic groups.

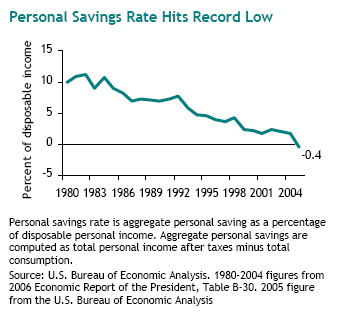

- Personal Savings Rate: The U.S. personal savings rate, which measures the percentage of disposable income that Americans save, has fluctuated significantly over the past few decades. According to the Bureau of Economic Analysis, the savings rate has ranged from a high of over 10% in the early 1980s to a low of below 2% in the mid-2000s. As of 2024, the savings rate is around 5%, indicating that Americans are saving a smaller portion of their income compared to previous generations.

The American public has been spending more money than it has earned after taxes

The American public has been spending more money than it has earned after taxes

-

Income Inequality: Income inequality in the U.S. has been steadily increasing, with a growing gap between the highest and lowest earners. Data from the U.S. Census Bureau shows that the top 20% of households hold a disproportionately large share of the nation’s wealth, while the bottom 20% struggle to make ends meet. This disparity in income distribution directly impacts saving habits, as lower-income households have limited capacity to save.

-

Retirement Savings: Many Americans face a retirement savings crisis, with insufficient funds to cover their expenses in retirement. A report by the National Retirement Risk Index found that over half of U.S. households are at risk of not being able to maintain their pre-retirement standard of living. This shortfall is particularly pronounced among lower-income individuals, who often lack access to employer-sponsored retirement plans and face challenges in saving independently.

-

Emergency Savings: A significant number of Americans lack adequate emergency savings to cover unexpected expenses. According to a survey by the Federal Reserve, nearly 40% of adults would struggle to cover a $400 emergency expense. This lack of financial resilience can lead to increased debt and financial instability, particularly for those with lower incomes.

2.1. Disparities in Savings Across Demographic Groups

In addition to income, demographic factors such as age, gender, race, and education level also influence saving habits. Understanding these disparities is crucial for developing targeted strategies to promote financial inclusion and improve savings outcomes for all Americans.

| Demographic Group | Average Savings Rate | Common Challenges |

|---|---|---|

| Younger Adults | Lower | Student loan debt, lower wages, competing financial priorities |

| Women | Lower | Gender pay gap, career interruptions, longer life expectancy |

| Minorities | Lower | Historical wealth disparities, systemic barriers to financial access |

| Less Educated | Lower | Lower wages, limited access to financial education |

Addressing these disparities requires comprehensive policy interventions, including initiatives to promote financial literacy, reduce income inequality, expand access to affordable financial services, and eliminate systemic barriers to wealth accumulation.

3. How to Improve Saving Habits Regardless of Income

While income undoubtedly plays a significant role in saving habits, it is possible to improve your financial situation and build wealth regardless of your current income level. By implementing effective strategies and adopting a proactive approach to financial planning, you can enhance your saving habits and achieve your financial goals.

3.1. Budgeting and Expense Tracking

Creating a budget and tracking your expenses is the first step toward improving your saving habits. By understanding where your money is going, you can identify areas where you can cut back and allocate more funds toward savings.

- Create a Detailed Budget: List all sources of income and categorize your expenses into fixed costs (e.g., rent, mortgage, utilities) and variable costs (e.g., food, entertainment, transportation).

- Track Your Spending: Use a budgeting app, spreadsheet, or notebook to record your daily expenses.

- Identify Areas for Reduction: Analyze your spending patterns and identify areas where you can reduce discretionary spending, such as dining out, entertainment, or shopping.

- Set Realistic Saving Goals: Establish specific, measurable, achievable, relevant, and time-bound (SMART) saving goals, such as saving a certain percentage of your income each month or building an emergency fund.

3.2. Automating Savings

Automating your savings is an effective way to ensure that you consistently save money without having to actively think about it. By setting up automatic transfers from your checking account to your savings or investment accounts, you can make saving a seamless part of your financial routine.

- Set Up Automatic Transfers: Schedule regular transfers from your checking account to your savings or investment accounts on a weekly, bi-weekly, or monthly basis.

- Take Advantage of Employer-Sponsored Retirement Plans: Enroll in your employer’s 401(k) or other retirement plan and contribute enough to take full advantage of any employer matching contributions.

- Use Round-Up Apps: Consider using apps that round up your purchases to the nearest dollar and automatically transfer the difference to your savings account.

3.3. Reducing Debt

High levels of debt can significantly impede your ability to save and build wealth. By reducing your debt burden, you can free up more funds to allocate toward savings and investments.

- Prioritize High-Interest Debt: Focus on paying down high-interest debt, such as credit card debt, first to minimize interest charges and accelerate your debt repayment.

- Consider Debt Consolidation: Explore options for consolidating your debt, such as balance transfer credit cards or personal loans, to potentially lower your interest rates and simplify your payments.

- Avoid Accumulating New Debt: Be mindful of your spending habits and avoid accumulating new debt, particularly on unnecessary purchases.

3.4. Increasing Income Streams

Increasing your income can significantly boost your ability to save and achieve your financial goals. By exploring opportunities to earn additional income, you can accelerate your savings rate and build wealth more quickly. income-partners.net is an excellent resource for finding strategic partnerships that can help you increase your income.

- Negotiate a Raise: Research industry standards and negotiate a raise with your current employer based on your performance and contributions.

- Start a Side Hustle: Explore opportunities to earn additional income through freelance work, consulting, online businesses, or other side hustles.

- Invest in Education and Skills Development: Enhance your skills and knowledge through education, training, or certifications to increase your earning potential.

3.5. Setting Financial Goals

Setting clear financial goals is essential for staying motivated and focused on your saving efforts. By defining your goals and tracking your progress, you can stay on track and achieve your financial aspirations.

- Define Your Goals: Identify your short-term, medium-term, and long-term financial goals, such as building an emergency fund, saving for a down payment on a home, or funding your retirement.

- Create a Timeline: Establish a timeline for achieving each of your financial goals, setting realistic deadlines and milestones along the way.

- Track Your Progress: Regularly monitor your progress toward your goals and make adjustments to your saving and investment strategies as needed.

3.6. Seeking Professional Advice

If you are struggling to improve your saving habits or manage your finances effectively, consider seeking professional advice from a financial advisor. A qualified financial advisor can provide personalized guidance and support to help you develop a sound financial plan and achieve your goals.

- Find a Qualified Advisor: Look for a financial advisor who is experienced, knowledgeable, and trustworthy.

- Discuss Your Goals and Concerns: Share your financial goals, concerns, and priorities with your advisor to ensure that they understand your unique circumstances.

- Develop a Comprehensive Plan: Work with your advisor to develop a comprehensive financial plan that addresses your saving, investing, debt management, and retirement planning needs.

4. Real-Life Examples of Successful Savers

To inspire and motivate your saving efforts, let’s explore some real-life examples of individuals who have successfully improved their saving habits and achieved their financial goals, regardless of their income levels.

- Sarah, the Teacher: Sarah, a teacher with a modest income, was struggling to save for retirement due to student loan debt and rising living expenses. By creating a detailed budget, automating her savings, and increasing her income through tutoring, she was able to pay off her student loans and significantly boost her retirement savings.

- John, the Freelancer: John, a freelancer with fluctuating income, found it challenging to save consistently. By tracking his expenses, setting up a separate savings account for emergencies, and investing in skills development to increase his earning potential, he was able to build a solid financial foundation.

- Maria, the Single Parent: Maria, a single parent working a minimum-wage job, faced numerous financial challenges. By prioritizing her expenses, seeking assistance from community resources, and setting small, achievable saving goals, she was able to build an emergency fund and improve her financial stability.

These examples demonstrate that with determination, discipline, and the right strategies, anyone can improve their saving habits and achieve their financial goals, regardless of their income level.

5. The Role of Financial Literacy in Saving Habits

Financial literacy plays a crucial role in shaping saving habits and promoting financial well-being. Individuals with a strong understanding of financial concepts and principles are better equipped to make informed decisions about saving, investing, and managing their money effectively.

- Understanding Financial Concepts: Financial literacy encompasses a wide range of topics, including budgeting, saving, investing, debt management, and retirement planning.

- Making Informed Decisions: Financially literate individuals are more likely to make informed decisions about their money, such as choosing the right savings accounts, investing in diversified portfolios, and avoiding high-interest debt.

- Achieving Financial Goals: Financial literacy empowers individuals to set realistic financial goals, develop effective strategies for achieving those goals, and stay on track over time.

5.1. Resources for Improving Financial Literacy

Fortunately, there are numerous resources available to help individuals improve their financial literacy and develop sound saving habits.

- Online Courses: Many websites and organizations offer free or low-cost online courses on personal finance topics.

- Financial Workshops: Community centers, libraries, and nonprofit organizations often host financial workshops and seminars.

- Books and Articles: There are countless books and articles available on personal finance topics, providing valuable insights and practical advice.

- Financial Advisors: Working with a financial advisor can provide personalized guidance and support to help you improve your financial literacy and develop a sound financial plan.

By investing in your financial education and seeking out reliable resources, you can empower yourself to make informed decisions about your money and achieve your financial goals.

6. Government Policies and Saving Incentives

Government policies and saving incentives can play a significant role in encouraging individuals to save and build wealth. By implementing policies that promote savings and provide tax benefits for retirement contributions, governments can help individuals achieve financial security and reduce reliance on social safety nets.

- Tax-Advantaged Retirement Accounts: Tax-advantaged retirement accounts, such as 401(k)s and IRAs, provide incentives for individuals to save for retirement by offering tax deductions, tax-deferred growth, or tax-free withdrawals.

- Saver’s Credit: The Saver’s Credit is a tax credit available to low- and moderate-income taxpayers who contribute to a retirement account.

- Financial Education Programs: Government-sponsored financial education programs can help individuals improve their financial literacy and develop sound saving habits.

6.1. Policy Recommendations for Promoting Savings

To further promote savings and financial security, policymakers can consider implementing the following policy recommendations:

- Expand Access to Retirement Savings Plans: Make it easier for small businesses and self-employed individuals to offer and participate in retirement savings plans.

- Increase the Saver’s Credit: Increase the amount of the Saver’s Credit and make it available to a broader range of taxpayers.

- Implement Automatic Enrollment in Retirement Plans: Require employers to automatically enroll employees in retirement plans, with the option for employees to opt out.

- Provide Financial Education in Schools: Integrate financial education into the curriculum of schools and colleges to equip students with the knowledge and skills they need to manage their money effectively.

By implementing these policies, governments can create a more supportive environment for savings and help individuals achieve financial security.

7. The Impact of Unexpected Expenses on Saving Habits

Unexpected expenses can significantly impact saving habits, particularly for individuals with limited financial resources. These expenses can derail saving plans, deplete emergency funds, and lead to increased debt and financial stress.

- Medical Bills: Unexpected medical bills can be a major financial burden, particularly for those without adequate health insurance.

- Car Repairs: Car repairs can be costly and often come at inconvenient times, forcing individuals to dip into their savings or take on debt.

- Home Repairs: Home repairs can be expensive and disruptive, requiring homeowners to allocate significant funds to address issues such as leaky roofs, plumbing problems, or appliance breakdowns.

- Job Loss: Losing a job can have a devastating impact on financial stability, making it difficult to meet basic needs and save for the future.

7.1. Strategies for Managing Unexpected Expenses

To mitigate the impact of unexpected expenses on saving habits, it is essential to develop strategies for managing these financial shocks.

- Build an Emergency Fund: Building an emergency fund is the most effective way to prepare for unexpected expenses. Aim to save at least three to six months’ worth of living expenses in a readily accessible savings account.

- Purchase Insurance: Purchase adequate insurance coverage, including health insurance, auto insurance, and homeowners insurance, to protect yourself from financial losses due to unexpected events.

- Create a Contingency Plan: Develop a contingency plan for managing unexpected expenses, including identifying potential sources of funds, such as savings, credit, or assistance programs.

- Seek Financial Assistance: If you are struggling to manage unexpected expenses, seek assistance from community resources, such as nonprofit organizations, government agencies, or financial counselors.

By implementing these strategies, you can minimize the impact of unexpected expenses on your saving habits and maintain your financial stability.

8. The Benefits of Partnering for Increased Income

Partnering with other businesses or individuals can be a powerful strategy for increasing income and accelerating your savings rate. By leveraging the resources, expertise, and networks of your partners, you can unlock new opportunities for growth and profitability.

- Access to New Markets: Partnering with businesses in different geographic regions or industries can provide access to new markets and customers.

- Increased Efficiency: Collaborating with partners can streamline operations, reduce costs, and improve efficiency.

- Shared Resources: Partnering allows you to share resources such as technology, equipment, and personnel, reducing the financial burden on any one party.

- Innovation: Working with partners can foster innovation and creativity, leading to the development of new products, services, and business models.

income-partners.net specializes in connecting individuals and businesses seeking strategic partnerships to boost their income and savings.

8.1. How income-partners.net Facilitates Partnerships

income-partners.net provides a platform for individuals and businesses to connect, collaborate, and create mutually beneficial partnerships. The website offers a range of resources and tools to help you find the right partners, negotiate agreements, and manage your partnerships effectively.

- Partner Matching: income-partners.net uses advanced algorithms to match you with potential partners based on your skills, interests, and goals.

- Networking Opportunities: The website hosts networking events and online forums where you can connect with other members and explore partnership opportunities.

- Educational Resources: income-partners.net provides a wealth of educational resources, including articles, videos, and webinars, on topics such as partnership strategies, negotiation tactics, and legal considerations.

- Support and Guidance: The income-partners.net team is available to provide support and guidance throughout the partnership process, helping you navigate challenges and achieve your goals.

By leveraging the resources and expertise of income-partners.net, you can unlock the power of partnerships and accelerate your path to financial success.

9. Creating a Savings Plan That Works for You

Creating a savings plan that works for you involves tailoring your strategies to your individual circumstances, goals, and preferences. There is no one-size-fits-all approach to saving, so it is essential to develop a plan that aligns with your unique needs and priorities.

- Assess Your Financial Situation: Start by assessing your current financial situation, including your income, expenses, debts, and assets.

- Set Clear Goals: Define your short-term, medium-term, and long-term financial goals, such as building an emergency fund, saving for a down payment on a home, or funding your retirement.

- Create a Budget: Develop a detailed budget that outlines your income and expenses, and identifies areas where you can cut back and allocate more funds toward savings.

- Automate Your Savings: Set up automatic transfers from your checking account to your savings or investment accounts to make saving a seamless part of your financial routine.

- Monitor Your Progress: Regularly monitor your progress toward your goals and make adjustments to your saving and investment strategies as needed.

- Seek Professional Advice: If you are struggling to create a savings plan that works for you, consider seeking professional advice from a financial advisor.

9.1. Tailoring Your Plan to Your Income Level

When creating your savings plan, it is essential to tailor your strategies to your income level.

- Lower Income: If you have a lower income, focus on building an emergency fund, paying down high-interest debt, and seeking opportunities to increase your income.

- Middle Income: If you have a middle income, prioritize saving for retirement, investing in diversified portfolios, and paying down debt.

- Upper Income: If you have an upper income, focus on maximizing your retirement savings, investing in a variety of assets, and exploring opportunities for wealth accumulation.

By tailoring your savings plan to your income level, you can maximize your savings potential and achieve your financial goals more effectively.

10. Future Trends in Income and Savings

As the economic landscape continues to evolve, it is essential to stay informed about future trends in income and savings. Understanding these trends can help you anticipate challenges and opportunities and adapt your financial strategies accordingly.

- Automation and Artificial Intelligence: Automation and artificial intelligence are likely to disrupt the labor market, potentially leading to job displacement and wage stagnation.

- Gig Economy: The gig economy is expected to continue to grow, offering new opportunities for flexible work and income generation, but also presenting challenges in terms of job security and benefits.

- Rising Healthcare Costs: Healthcare costs are projected to continue to rise, placing a significant financial burden on individuals and families.

- Longer Lifespans: People are living longer, requiring them to save more for retirement.

10.1. Preparing for the Future

To prepare for these future trends, it is essential to:

- Invest in Skills Development: Enhance your skills and knowledge to remain competitive in the changing job market.

- Diversify Your Income Streams: Explore opportunities to generate income from multiple sources to reduce your reliance on any one job or industry.

- Prioritize Healthcare Savings: Save for healthcare expenses and explore options for reducing your healthcare costs, such as preventive care and generic medications.

- Save More for Retirement: Increase your retirement savings to ensure that you have adequate funds to cover your expenses in retirement.

By staying informed and taking proactive steps to prepare for the future, you can protect your financial security and achieve your long-term goals.

FAQ: Your Top Questions Answered About Income and Savings

1. How does income level really affect saving habits?

Income level significantly impacts saving habits; higher incomes generally allow for more savings, while lower incomes often make saving difficult due to essential expenses.

2. What are some key saving statistics in the US that I should know?

Key statistics include the personal savings rate, income inequality, retirement savings shortfalls, and the number of Americans lacking emergency savings.

3. Can I improve my saving habits regardless of my income?

Yes, improving saving habits is possible at any income level through budgeting, automating savings, reducing debt, and increasing income streams.

4. What role does financial literacy play in improving my saving habits?

Financial literacy is crucial, as it enables informed decisions about saving, investing, and managing money effectively, leading to better financial outcomes.

5. What government policies support savings, and how can I take advantage of them?

Government policies like tax-advantaged retirement accounts and the Saver’s Credit encourage saving; take advantage by contributing to retirement accounts and claiming eligible tax credits.

6. How do unexpected expenses affect my saving habits, and what can I do about it?

Unexpected expenses can derail savings, but building an emergency fund, purchasing insurance, and creating a contingency plan can mitigate their impact.

7. What are the benefits of partnering to increase my income, and how can I find partners?

Partnering can provide access to new markets and increase efficiency; platforms like income-partners.net help you find strategic partners.

8. How can I create a savings plan that works specifically for me?

Tailor your savings plan to your individual circumstances, goals, and income level, regularly monitoring your progress and seeking professional advice when needed.

9. What future trends in income and savings should I be aware of?

Be aware of trends like automation, the gig economy, rising healthcare costs, and longer lifespans, and prepare by investing in skills development and diversifying income.

10. Where can I find more resources to help me improve my income and saving habits?

income-partners.net offers valuable resources, including partner matching, networking opportunities, and educational content, to help you boost your income and savings. For specific financial advice, Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.

By addressing these key questions and providing actionable strategies, this article equips readers with the knowledge and tools they need to improve their saving habits and achieve financial security, regardless of their income level.

Ready to take control of your financial future? Visit income-partners.net today to explore partnership opportunities, discover proven strategies for building wealth, and connect with a community of like-minded individuals. Start building your path to financial success now!