Does Va Have Local Income Tax? Yes, Virginia does not have local income taxes. Income-partners.net provides resources that help you navigate state and federal taxes, including understanding which areas collect local income taxes and how to plan your financial strategy accordingly, especially if you’re looking to increase revenue. By understanding these tax implications, you can make informed decisions and maximize your income potential. Explore resources on municipal taxes, state income, and tax regulations to better plan your financial strategies.

1. Understanding Income Tax in Virginia

1.1 What is Income Tax?

Income tax is a levy imposed by a government on the income of individuals or businesses. It is a primary source of revenue for governments, funding public services such as education, healthcare, and infrastructure. The structure of income tax can vary, including progressive (higher income taxed at a higher rate), regressive (lower income taxed at a higher rate), or flat (all income taxed at the same rate). According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, income tax systems significantly impact economic equity and social welfare.

1.2 Does Virginia Have a State Income Tax?

Yes, Virginia has a state income tax. Virginia’s individual income tax system features several tax brackets, with rates increasing as income rises. These rates are subject to change, and the Virginia Department of Taxation provides detailed information on current rates and brackets. Understanding Virginia’s state income tax is crucial for individuals and businesses operating within the state. The tax is a significant source of revenue for Virginia, supporting various state-level programs and services. For more insights on how state income tax affects your financial planning, visit income-partners.net.

1.3 Does Virginia Have Local Income Tax?

No, Virginia does not have local income taxes. Local governments in Virginia, such as counties and cities, are not authorized to impose their own income taxes. Instead, they rely on other forms of revenue, such as property taxes, sales taxes, and fees. Because Virginia does not have local income tax, it makes the tax system easier to understand for residents.

2. The Tax System in Virginia

2.1 Overview of Virginia’s Tax Structure

Virginia’s tax system relies on income tax, sales and use tax, and property tax. The Commonwealth’s revenue is largely generated from these sources, which fund public services and infrastructure. The Institute on Taxation and Economic Policy have found that the overall tax incidence in Virginia can be regressive, meaning lower-income households pay a higher percentage of their income in taxes than higher-income households.

2.2 State Income Tax in Detail

Virginia’s state income tax is a significant revenue source for the state. The individual income tax accounts for approximately 70% of the state’s General Fund revenues. Virginia’s tax brackets are structured such that the top tax rate applies to incomes above a relatively low threshold, making the income tax system resemble a flat tax for many residents.

2.3 Local Taxes in Virginia

Since Virginia does not have local income taxes, cities and counties depend on other revenue sources. The main sources of local revenue in Virginia include:

- Property Taxes: These are a primary source of revenue for local governments, levied on real estate and personal property.

- Sales Taxes: Localities collect a portion of the state sales tax, which is applied to retail sales.

- Fees and Charges: Local governments impose various fees for services like utilities, permits, and licenses.

- Other Taxes: These can include taxes on hotels, meals, and other specific items or services.

Image alt: Overview of Virginia’s upside-down tax system, showing its impact on residents.

3. Understanding Local Tax Systems in the U.S.

3.1 States With Local Income Taxes

Several states in the U.S. allow local governments to impose income taxes. The structures, rates, and applications of these taxes vary widely, affecting both residents and businesses operating in those areas. Here are a few examples of states with local income taxes:

- Pennsylvania: Allows municipalities and school districts to levy a local earned income tax (EIT). Rates vary and are usually a small percentage of earned income.

- Ohio: Cities and villages can impose municipal income taxes, which are typically a percentage of wages earned within the municipality, as well as income earned by residents regardless of where they work.

- New York: New York City imposes a local income tax on its residents, in addition to the state income tax.

- Maryland: All counties and Baltimore City levy local income taxes, referred to as “local income tax” or “piggyback tax,” which are a percentage of the state income tax.

- Alabama: Some cities and counties impose local occupational taxes, which are similar to income taxes but often apply to specific professions or occupations.

3.2 How Local Income Taxes Work

Local income taxes are typically administered alongside state income taxes, with employers withholding the appropriate amounts from employees’ paychecks. The revenue generated from local income taxes is used to fund local government services, such as schools, public safety, and infrastructure. In states like Pennsylvania and Ohio, local income taxes can be a significant source of revenue for municipalities, allowing them to provide services without relying solely on property taxes or state funding.

3.3 Impact of Local Income Taxes

Local income taxes can impact residents and businesses, affecting decisions on where to live or operate. For individuals, local income taxes reduce the amount of disposable income, potentially affecting spending and savings. For businesses, these taxes add to the overall cost of doing business, which can influence investment and location decisions. Research from Harvard Business Review indicates that local tax policies significantly affect business growth and employment rates.

4. The Impact of Tax Policies on Virginia Residents

4.1 How Virginia’s Tax System Affects Different Income Groups

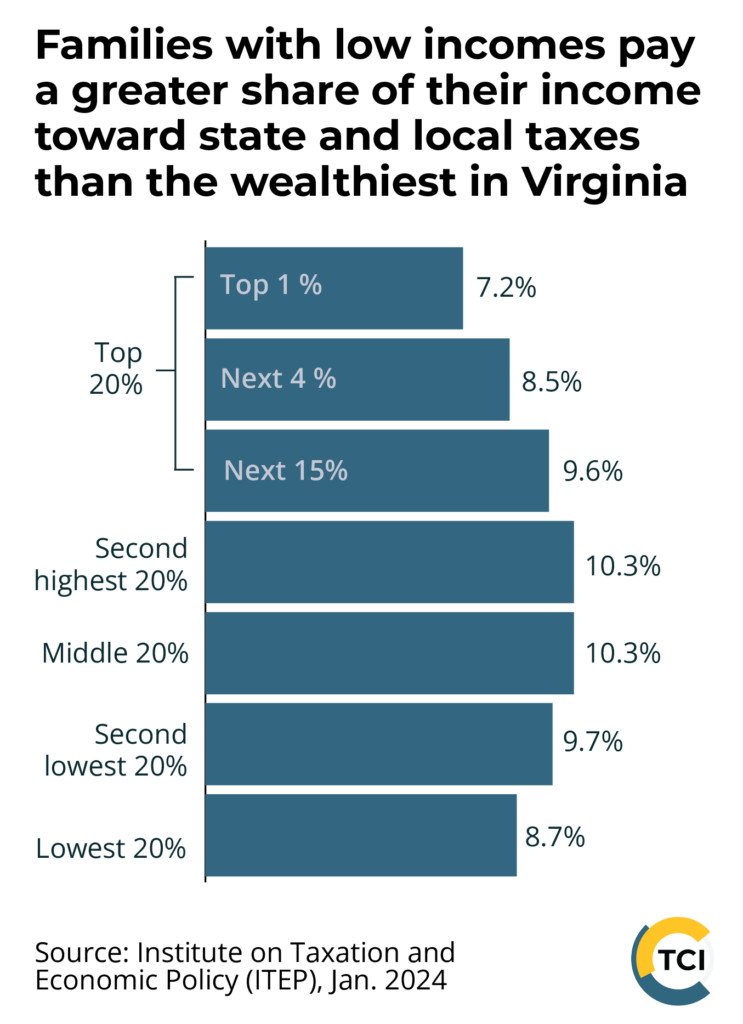

Virginia’s tax system has been criticized for being regressive. The Institute on Taxation and Economic Policy found that lower-income households in Virginia pay a higher percentage of their income in taxes compared to higher-income households. This is due to the reliance on sales taxes and the structure of the state income tax brackets, which apply the top rate to relatively low-income levels.

Table: Tax Burden by Income Group in Virginia

| Income Group | Share of Income Paid in Taxes |

|---|---|

| Lowest 20% | 9.9% |

| Middle 20% | 8.5% |

| Top 1% | 7.1% |

Source: Institute on Taxation and Economic Policy, Jan 2021

4.2 Racial Equity and Tax Policy in Virginia

Tax policies can disproportionately affect different racial and ethnic groups. In Virginia, the regressive nature of the tax system exacerbates existing racial income inequality. Black and Latino households often bear a higher tax burden relative to their income compared to white households. This is due to disparities in income and wealth, as well as the types of taxes that disproportionately affect lower-income individuals and families. Income-partners.net is committed to providing resources that promote financial literacy and equitable economic opportunities for all communities.

4.3 Potential Reforms to Virginia’s Tax System

Several reforms could make Virginia’s tax system more equitable and efficient:

- Progressive Income Tax Brackets: Adjusting the income tax brackets to ensure higher-income earners pay a higher percentage of their income in taxes.

- Expanding Refundable Tax Credits: Enhancing the state’s Earned Income Tax Credit (EITC) and creating a Child Tax Credit (CTC) to support low- and moderate-income families.

- Modernizing Sales Tax: Applying the sales tax to a broader range of goods and services, including digital products and services, to reflect changes in consumer spending patterns.

- Closing Corporate Tax Loopholes: Preventing large corporations from using accounting maneuvers to avoid paying state income taxes.

5. Strategies for Managing Taxes in Virginia

5.1 Tax Planning for Individuals

Effective tax planning can help individuals minimize their tax liability and maximize their financial well-being. Here are some strategies for managing taxes in Virginia:

- Take Advantage of Deductions and Credits: Familiarize yourself with eligible deductions and credits, such as those for education expenses, medical expenses, and charitable contributions.

- Maximize Retirement Contributions: Contribute to tax-advantaged retirement accounts, such as 401(k)s and IRAs, to reduce your taxable income.

- Plan for Capital Gains: Understand the tax implications of selling assets, such as stocks or real estate, and plan accordingly.

- Consult a Tax Professional: Seek advice from a qualified tax professional to ensure you are taking advantage of all available tax benefits.

5.2 Tax Planning for Businesses

Businesses in Virginia can also benefit from strategic tax planning to minimize their tax obligations and improve their bottom line. Some tax planning strategies for businesses include:

- Choosing the Right Business Structure: Selecting the most tax-efficient business structure, such as an LLC or S corporation, based on your specific circumstances.

- Taking Advantage of Business Deductions: Claiming all eligible business deductions, such as those for expenses, depreciation, and amortization.

- Utilizing Tax Credits and Incentives: Taking advantage of state and federal tax credits and incentives for businesses, such as those for research and development, job creation, and energy efficiency.

- Managing Inventory and Assets: Implementing strategies to efficiently manage inventory and assets to minimize tax liabilities.

5.3 Resources for Taxpayers in Virginia

Several resources are available to help taxpayers in Virginia navigate the tax system and access tax assistance:

- Virginia Department of Taxation: Provides information on state tax laws, regulations, and forms.

- Internal Revenue Service (IRS): Offers resources on federal tax laws, regulations, and programs.

- Tax Counseling for the Elderly (TCE): Provides free tax assistance to seniors and low-income individuals.

- Volunteer Income Tax Assistance (VITA): Offers free tax preparation services to individuals and families with low to moderate incomes.

Image alt: Visual representation of families with low incomes in Virginia paying a greater share of their income towards state and local taxes.

6. Understanding Tax Implications for Business Partnerships

6.1 Types of Business Partnerships

Business partnerships come in various forms, each with unique tax implications:

- General Partnership: All partners share in the business’s operational management and liability.

- Limited Partnership (LP): Has both general and limited partners. General partners manage the business and assume liability, while limited partners have limited involvement and liability.

- Limited Liability Partnership (LLP): Offers liability protection to partners, shielding them from the business’s debts and obligations.

- Joint Venture: Temporary partnership established for a specific project or purpose.

6.2 Tax Implications for Partnerships

Partnerships are typically treated as pass-through entities for tax purposes. This means that the partnership itself does not pay income taxes. Instead, profits and losses are passed through to the partners, who report them on their individual income tax returns. Each partner receives a Schedule K-1, which details their share of the partnership’s income, deductions, and credits.

6.3 Managing Tax Obligations in Partnerships

To effectively manage tax obligations in a partnership:

- Maintain Accurate Records: Keep detailed records of all income, expenses, and transactions.

- Understand K-1 Forms: Carefully review Schedule K-1 forms to ensure accurate reporting of income and deductions.

- Plan for Self-Employment Taxes: Partners are usually considered self-employed and must pay self-employment taxes on their share of the partnership’s profits.

- Consult with a Tax Advisor: Seek advice from a tax professional to optimize tax planning and ensure compliance with tax laws.

7. Exploring Business Opportunities in Austin, TX

7.1 Austin’s Thriving Business Environment

Austin, TX, is a hub for innovation and entrepreneurship, offering numerous opportunities for businesses and investors. The city’s vibrant economy is driven by the tech industry, a supportive business community, and a high quality of life. Austin attracts talent from around the world, making it an ideal location for startups and established companies alike.

7.2 Key Industries in Austin

Some of the key industries in Austin include:

- Technology: Austin is known as “Silicon Hills,” with major tech companies and startups driving innovation.

- Healthcare: A growing healthcare sector provides opportunities for medical businesses and healthcare professionals.

- Renewable Energy: Austin is a leader in renewable energy, with numerous companies focused on solar, wind, and other sustainable energy sources.

- Creative Industries: The city’s vibrant arts and culture scene supports creative businesses in music, film, and design.

7.3 Networking and Partnership Opportunities in Austin

Austin offers numerous networking and partnership opportunities for businesses looking to expand or collaborate. These include:

- Startup Incubators and Accelerators: Programs that provide resources and mentorship to early-stage companies.

- Industry Associations: Organizations that bring together businesses in specific sectors for networking and advocacy.

- Business Events and Conferences: Numerous events throughout the year that offer opportunities to connect with potential partners and investors.

- Co-working Spaces: Shared office spaces that foster collaboration and networking among entrepreneurs and freelancers.

8. Partnering for Success: Strategies and Opportunities

8.1 Identifying the Right Business Partners

Finding the right business partners is crucial for success. Look for partners who share your vision, complement your skills, and bring unique resources to the table. Key considerations include:

- Shared Values: Align on core values and business ethics.

- Complementary Skills: Find partners who fill gaps in your skillset.

- Financial Stability: Ensure partners have the financial resources to contribute to the venture.

- Clear Communication: Establish open and honest communication channels.

8.2 Building Successful Partnerships

To build a successful business partnership:

- Define Roles and Responsibilities: Clearly outline each partner’s roles and responsibilities.

- Establish a Partnership Agreement: Create a formal agreement that outlines the terms of the partnership, including ownership, decision-making, and dispute resolution.

- Communicate Regularly: Maintain open and frequent communication to address issues and align on goals.

- Build Trust and Respect: Foster a culture of trust and respect among partners.

8.3 Legal Considerations for Partnerships

Before entering into a partnership, it is important to consider the legal implications:

- Partnership Agreement: Consult with an attorney to draft a comprehensive partnership agreement that protects your interests.

- Liability: Understand the liability implications of different partnership structures and ensure adequate insurance coverage.

- Compliance: Comply with all relevant laws and regulations, including tax laws and business licensing requirements.

9. Maximizing Income Through Strategic Partnerships

9.1 Types of Strategic Partnerships

Strategic partnerships can take many forms, each offering unique benefits:

- Joint Ventures: Collaborations on specific projects or ventures, sharing resources and expertise.

- Distribution Agreements: Partnerships to expand market reach through distribution networks.

- Marketing Alliances: Collaborations on marketing campaigns to reach new customers.

- Technology Partnerships: Collaborations to develop and integrate new technologies.

9.2 Benefits of Strategic Partnerships

Strategic partnerships can provide numerous benefits:

- Increased Revenue: Access to new markets and customers, leading to higher sales.

- Reduced Costs: Shared resources and expenses, lowering operating costs.

- Enhanced Innovation: Access to new ideas and technologies, fostering innovation.

- Competitive Advantage: Stronger market position through collaboration and shared expertise.

9.3 Case Studies of Successful Partnerships

Examples of successful strategic partnerships include:

- Starbucks and Barnes & Noble: A partnership that offers customers a coffee shop experience within bookstores, enhancing the overall customer experience.

- Apple and Nike: A collaboration that integrates technology and fitness, creating products like the Apple Watch Nike+ edition.

- BMW and Toyota: A partnership to develop new technologies for electric vehicles and fuel cell systems, sharing research and development costs.

10. Frequently Asked Questions (FAQ)

10.1 Does Virginia have local income taxes?

No, Virginia does not have local income taxes. Local governments rely on property taxes, sales taxes, and fees for revenue.

10.2 What is the state income tax rate in Virginia?

Virginia has a progressive income tax system with several tax brackets. The top rate of 5.75% starts at a relatively low-income level.

10.3 How can I minimize my tax liability in Virginia?

Individuals can minimize their tax liability by taking advantage of deductions and credits, maximizing retirement contributions, and consulting a tax professional.

10.4 What are the tax implications for business partnerships?

Partnerships are pass-through entities, meaning profits and losses are passed through to the partners, who report them on their individual income tax returns.

10.5 What types of business partnerships exist?

Types of business partnerships include general partnerships, limited partnerships, limited liability partnerships, and joint ventures.

10.6 What are the benefits of strategic partnerships?

Strategic partnerships can lead to increased revenue, reduced costs, enhanced innovation, and a stronger competitive advantage.

10.7 How can I find the right business partners?

Look for partners who share your vision, complement your skills, and bring unique resources to the table.

10.8 What are the key industries in Austin, TX?

Key industries in Austin include technology, healthcare, renewable energy, and creative industries.

10.9 How can I manage tax obligations in a partnership?

Maintain accurate records, understand K-1 forms, plan for self-employment taxes, and consult with a tax advisor.

10.10 What resources are available for taxpayers in Virginia?

Resources include the Virginia Department of Taxation, the IRS, Tax Counseling for the Elderly (TCE), and Volunteer Income Tax Assistance (VITA).

Are you looking for strategic partners to grow your business and increase revenue? Visit income-partners.net to explore partnership opportunities, learn strategies for building successful relationships, and connect with potential partners in the U.S. Discover how effective collaboration can drive financial success and create long-term value for your business.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.