Does The City Of Chicago Have An Income Tax? Understanding Chicago’s tax landscape is vital for businesses and individuals alike. At income-partners.net, we help you navigate these complexities to foster strategic partnerships and revenue growth. This guide clarifies the current tax situation in Chicago, explores potential impacts, and offers insights into how to leverage opportunities despite the tax environment. Boost your financial partnerships by understanding the nuances of municipal finance, local taxation, and fiscal policy.

1. What Is the Current Income Tax Situation in Chicago?

Currently, the City of Chicago does not have a local income tax. The Illinois Constitution requires that the state’s General Assembly grant specific authority to home rule units like Chicago before they can impose such a tax. As of now, this authority has not been granted.

Expanding on this, it’s important to understand the implications. Without a city income tax, Chicago relies on other revenue streams such as property taxes, sales taxes, and various fees. This affects how the city funds its services and infrastructure, and consequently, the business environment. For those looking to form strategic partnerships, understanding these financial underpinnings is crucial.

2. Could Chicago Implement a City Income Tax in the Future?

While Chicago doesn’t currently have an income tax, the possibility of implementing one in the future remains a topic of discussion. Given the city’s financial challenges, various mayoral and aldermanic candidates have, in the past, considered this option as a potential revenue source.

The implementation of a city income tax would necessitate legislative action at the state level, either through the passage of a bill by the Illinois General Assembly or a constitutional amendment. If such measures were to succeed, numerous considerations would come into play, including the tax base, rates, and administration. Keep an eye on local fiscal policy and municipal finance discussions for updates on this evolving situation.

3. What Would a Chicago Income Tax Base Include?

If Chicago were to implement an income tax, defining the tax base would be a critical step. Generally, a local income tax base can encompass:

- Earned income: Wages, salaries, tips, and other forms of taxable employee pay.

- Proprietary income: Income from privately owned businesses.

- Corporate income.

- Personal income: Compensation from salaries, wages, and bonuses; dividends and distributions from investments; rental income; and business profit sharing.

The breadth of the tax base can vary. For instance, Pennsylvania has a narrow base that includes only earned and proprietary income, while New York City has a broader base that encompasses personal, proprietary, and corporate income. The choice of tax base significantly impacts the revenue generated and the burden on different segments of the population.

4. Who Would Pay a Chicago Municipal Income Tax?

If a municipal income tax were to be enacted, determining who would be liable to pay it would be a key consideration. The tax could be applied to:

- Residents only: Those who live within the city limits.

- Non-residents who work or do business in the city: This would capture income earned within Chicago, regardless of where the individual resides.

The decision to include non-residents can mitigate the potential disincentive for residents to live and work in the city, as it distributes the tax burden more broadly. Additionally, the tax rates for residents and non-residents could be the same or different, depending on policy objectives.

5. How Would a Chicago Income Tax Be Administered?

The administration and collection of a Chicago municipal income tax would be a logistical undertaking. The responsibility could fall to:

- The State of Illinois: Leveraging the existing state income tax infrastructure.

- Local authorities: Creating a new municipal tax collection system.

Choosing between these options would involve weighing the costs and benefits of each approach. Utilizing the state’s system could streamline the process and reduce administrative expenses, while local control could allow for greater flexibility and responsiveness to the city’s needs.

6. What Are the Potential Pros of a Local Income Tax in Chicago?

There are several arguments in favor of a local option income tax, including:

| Argument | Description |

|---|---|

| Reduces Reliance on Regressive Taxes | It can replace or reduce the need for increasing other more regressive taxes such as property or sales taxes. |

| Elastic Revenue Source | Income taxes are an elastic revenue source that yield greater amounts of revenue as the economy grows. |

| Contributes to Revenue Diversification | The use of income taxes could contribute to revenue diversification, thereby lessening reliance on other revenue sources such as property taxes. |

| Generates Significant Revenue | Income taxes can generate significant amounts of revenue, helping to fund essential city services and infrastructure. |

| Captures Non-Resident Contributions | If imposed on nonresidents who work in a jurisdiction, local income tax revenue can be used to help pay for municipal services and infrastructure used by them. |

These advantages could help stabilize Chicago’s finances and provide a more sustainable funding model for the future. Partnering with experts in municipal finance and local taxation can provide further insights into these potential benefits.

7. What Are the Potential Cons of a Local Income Tax in Chicago?

Conversely, there are several arguments against local income taxes, including:

- Disincentive to Live, Work, or Do Business: A local income tax may be a disincentive to live, work, or do business in a city imposing the tax. Mitigating this impact might involve extending the tax to nonresidents or imposing a county or regional income tax rather than a municipal tax.

- Tax Avoidance: It may be possible to avoid a local income tax that is only imposed on residents by moving out of the jurisdiction.

- High Composite Tax Rate: A local income tax base will be shared with federal and state income taxes, which may lead to a high composite tax rate.

- Limits on Local Tax Deduction: The 2017 federal tax reform act limits the deduction of local taxes, increasing the relative burden on taxpayers.

- Revenue Volatility: Because income taxes are elastic, there may be significant fluctuations in revenue. In economic downturns income tax revenues may fall precipitously, forcing governments to find alternative funding sources.

- Tax Burden Export: A local income tax can export the tax burden to nonresidents who do not fully utilize city services.

- Negative Impact on Economic Development: A local income tax applied to corporate income may negatively impact economic development if it is perceived to create an unfavorable business climate.

These potential drawbacks need careful consideration to ensure that the tax is implemented in a way that minimizes negative impacts on the city’s economy and residents.

8. How Would Exemptions Work with a Chicago Income Tax?

If Chicago were to institute a local income tax, policymakers would need to determine what exemptions would be permitted. Exemptions can be designed to:

- Protect low-income taxpayers: Ensuring that the tax burden does not disproportionately affect those least able to pay.

- Attract specific industries or workers: Offering tax breaks to incentivize certain types of economic activity.

- Provide relief for specific circumstances: Such as exemptions for military personnel or those with disabilities.

The design of exemptions can significantly impact the fairness and effectiveness of the tax.

9. How Would a Chicago Income Tax Affect Businesses?

A Chicago income tax could have significant implications for businesses, depending on how it is structured. Key considerations include:

- Tax base: Whether corporate income is included in the tax base.

- Nexus: How nexus (the connection between a business and the city) is established for taxable business activity.

- Rates: The tax rates applied to corporate and personal income.

A municipal income tax applied to corporate income may negatively impact economic development if it is perceived to create an unfavorable business climate. Therefore, policymakers need to carefully weigh the potential impacts on businesses when designing the tax.

10. What Are Some Alternatives to a Chicago Income Tax?

Given the potential drawbacks of a local income tax, it’s important to consider alternative revenue sources for the City of Chicago. These could include:

- Increased property taxes: Although this can be unpopular and disproportionately affect homeowners.

- Higher sales taxes: Which can impact consumer spending and make the city less competitive with neighboring jurisdictions.

- New or increased fees: Such as fees for specific services or activities.

- Revenue sharing with the state: Negotiating a larger share of state tax revenues.

- Economic development initiatives: Attracting new businesses and jobs to the city.

Exploring these alternatives can help Chicago find a sustainable and equitable funding model for the future.

jurisdictions_levying_income_tax.png

jurisdictions_levying_income_tax.png

11. What Was the Inspector General’s Estimate of Revenue from a Chicago Income Tax?

In 2011, the City of Chicago Inspector General’s Office estimated that a 1% municipal income tax could raise approximately $500 million. This figure was calculated by assuming that a 1% city income tax would be imposed on Chicago’s share of the adjusted gross income used by the state to calculate state income taxes in 2009.

This estimate provides a sense of the potential revenue that could be generated from a city income tax. However, it’s important to note that this is just an estimate, and the actual revenue could be higher or lower depending on the specific design of the tax and the state of the economy.

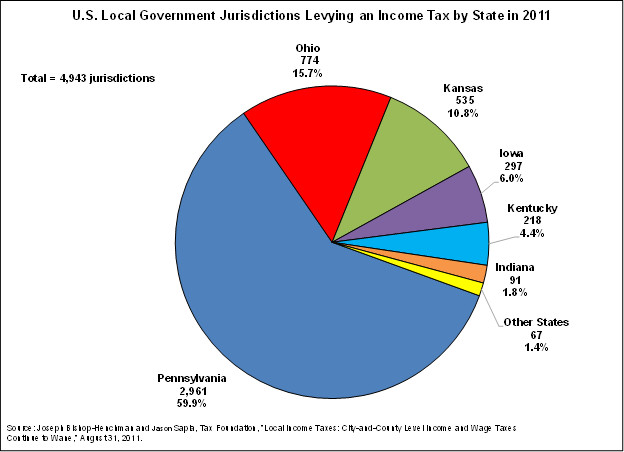

12. How Many Jurisdictions in the U.S. Have Local Income Taxes?

According to the Tax Foundation, in 2011 approximately 4,943 local government jurisdictions in 17 states imposed local option income taxes. These jurisdictions were primarily municipalities and counties.

The states permitting local option income taxes and the number of jurisdictions in each authorized to levy income taxes are: Alabama (4), California (1), Colorado (3), Delaware (1), Indiana (91), Iowa (297), Kansas (535), Kentucky (218), Maryland (24), Michigan (22), Missouri (2), New Jersey (1), New York (4), Ohio (774), Oregon (2), Pennsylvania (2,961) and West Virginia (3).

Nearly 60% of these jurisdictions are in Pennsylvania. This data provides context for understanding the prevalence of local income taxes in the United States.

13. What Are the Key Considerations for Creating a Chicago Municipal Income Tax?

Implementing a Chicago municipal income tax would require careful consideration of several key issues, including:

| Issue | Description |

|---|---|

| Municipal Income Tax Base | What would constitute the municipal income tax base? |

| Tax Applicability | Would the tax be applied only to residents or to nonresidents who work or do business in the City as well? |

| Resident and Nonresident Tax Rates | If so, would the resident and nonresident tax rates be the same or different? |

| Tax Administration | Would the municipal income tax be administered and collected by the State of Illinois or by local authorities? |

| Permitted Exemptions | What exemptions would be permitted? |

| Nexus for Corporate Income | If the municipal income tax base includes corporate income, how would nexus be established for taxable business activity? |

Addressing these issues would be essential to designing a fair, effective, and sustainable municipal income tax.

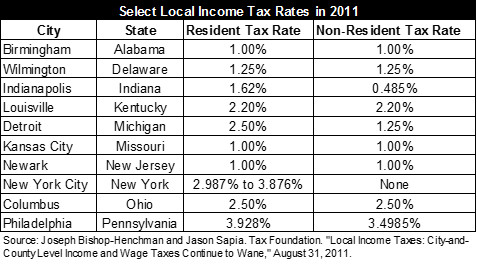

14. How Do Local Income Tax Rates Vary?

Local income tax rates vary widely across jurisdictions. In most jurisdictions, the local income tax is levied on residents as well as nonresidents who work in the taxing jurisdiction. The nonresident tax rate is typically lower than imposed on residents.

Most jurisdictions impose a flat rate income tax. New York City, however, has implemented a graduated rate. This variation in rates reflects the different fiscal needs and policy objectives of local governments.

15. How Can Businesses Prepare for Potential Tax Changes in Chicago?

To prepare for potential tax changes in Chicago, businesses should:

- Stay informed: Monitor local government discussions and legislative proposals related to taxation.

- Analyze potential impacts: Assess how different tax scenarios could affect their bottom line.

- Engage with policymakers: Advocate for policies that support a favorable business climate.

- Plan for contingencies: Develop strategies to mitigate the potential negative impacts of tax increases.

By taking these steps, businesses can proactively manage their tax exposure and ensure their long-term success in Chicago.

local_income_tax_rates_2011.png

local_income_tax_rates_2011.png

16. What Role Does the Illinois Constitution Play in Chicago’s Ability to Impose an Income Tax?

The Illinois Constitution plays a crucial role in determining Chicago’s ability to impose an income tax. The constitution provides that home rule units of governments such as the City of Chicago may only impose a local income tax if that authority is granted by the General Assembly.

This provision effectively prevents Chicago from enacting a local income tax without the express permission of the state legislature. Any attempt to implement a city income tax would require either a change in state law or a constitutional amendment.

17. How Could a Chicago Income Tax Affect Real Estate Values?

A Chicago income tax could potentially affect real estate values, depending on how it is structured and perceived by the market. Key considerations include:

- Impact on disposable income: If the tax reduces residents’ disposable income, it could dampen demand for housing and put downward pressure on prices.

- Disincentive to live in the city: If the tax is seen as too burdensome, it could discourage people from living in Chicago, leading to lower demand for housing.

- Offsetting factors: Other factors, such as job growth and amenities, could offset the negative impacts of the tax on real estate values.

The ultimate impact on real estate values would depend on a complex interplay of factors.

18. What Are the Implications for Low-Income Residents?

A Chicago income tax could have significant implications for low-income residents. If the tax is not carefully designed, it could disproportionately burden those least able to pay.

To mitigate this risk, policymakers could consider:

- Exemptions for low-income taxpayers: Providing tax breaks to reduce the burden on those with limited incomes.

- Progressive tax rates: Implementing a system where higher earners pay a larger percentage of their income in taxes.

- Targeted assistance programs: Providing direct assistance to help low-income residents offset the cost of the tax.

By taking these steps, the city can ensure that the tax is implemented in a way that is fair and equitable for all residents.

19. How Would a Chicago Income Tax Compare to Other Major Cities?

To understand the potential impact of a Chicago income tax, it’s helpful to compare it to other major cities that have such taxes. Key considerations include:

- Tax rates: How do Chicago’s potential rates compare to those in other cities?

- Tax base: What types of income are subject to the tax in different cities?

- Revenue generated: How much revenue do other cities generate from their income taxes?

- Economic impacts: What have been the economic impacts of income taxes in other cities?

By examining these factors, Chicago can learn from the experiences of other cities and make informed decisions about its own tax policy.

20. Where Can I Find More Information About Chicago’s Tax Landscape and Partnering Opportunities?

For more in-depth information on Chicago’s tax landscape and to explore strategic partnering opportunities, visit income-partners.net. We provide valuable insights, resources, and connections to help you navigate the complexities of the Chicago business environment and foster revenue growth. Our platform offers a comprehensive overview of municipal finance, local taxation, and fiscal policy, empowering you to make informed decisions and build successful partnerships.

FAQ: Chicago Income Tax

Here are some frequently asked questions about the possibility of a Chicago income tax:

- Does Chicago currently have an income tax?

No, Chicago does not currently have a local income tax. - What would need to happen for Chicago to implement an income tax?

The Illinois General Assembly would need to grant the city the authority to impose such a tax. - Who would pay a Chicago income tax?

It could apply to residents, non-residents who work in the city, or both. - What are the potential benefits of a Chicago income tax?

It could reduce reliance on regressive taxes and diversify revenue streams. - What are the potential drawbacks of a Chicago income tax?

It could disincentivize living or doing business in the city and increase the overall tax burden. - How much revenue could a Chicago income tax generate?

The Inspector General estimated a 1% tax could raise $500 million in 2011. - How do other cities with income taxes structure them?

Rates and tax bases vary widely, with some cities taxing non-residents and others using graduated rates. - What alternatives are there to a Chicago income tax?

Options include increased property or sales taxes, new fees, and revenue sharing with the state. - How can businesses prepare for potential tax changes in Chicago?

Stay informed, analyze impacts, engage with policymakers, and plan for contingencies. - Where can I find more information about Chicago’s tax landscape and partnering opportunities?

Visit income-partners.net for comprehensive resources and connections.

Ready to explore strategic partnerships in Chicago? At income-partners.net, we connect you with opportunities to thrive in any tax environment. Discover innovative strategies, build valuable relationships, and unlock your business potential today. Visit our website to learn more and get started!

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

By understanding the nuances of Chicago’s tax landscape and leveraging the resources available at income-partners.net, businesses and individuals can navigate the complexities of the city’s financial environment and achieve their goals.