Does Net Investment Income Tax Apply To Ira Distributions? Yes, while IRA distributions themselves aren’t directly subject to the Net Investment Income Tax (NIIT), they can indirectly trigger it. This can occur by pushing your adjusted gross income (AGI) above the threshold where the NIIT applies, potentially increasing your overall tax liability. Income-partners.net is here to guide you through the complexities of investment income and tax planning, helping you make informed decisions to optimize your financial strategy.

1. What is Net Investment Income Tax (NIIT)?

The Net Investment Income Tax (NIIT) is a 3.8% tax on certain investment income for individuals, estates, and trusts with income above certain thresholds. Understanding the NIIT is crucial for effective financial planning, especially when managing IRA distributions and other investment income.

Understanding the Basics of NIIT

The NIIT was introduced as part of the Affordable Care Act (ACA) to help fund Medicare. It applies to individuals, estates, and trusts with income above specific thresholds:

- Single filers: Adjusted Gross Income (AGI) above $200,000

- Married filing jointly: AGI above $250,000

- Married filing separately: AGI above $125,000

- Estates and trusts: AGI above $12,950 (for 2023)

What is Included in Net Investment Income?

Net investment income includes various forms of income, such as:

- Interest: Income earned from savings accounts, bonds, and other interest-bearing investments.

- Dividends: Payments from stocks, mutual funds, and other dividend-paying investments.

- Capital Gains: Profits from the sale of stocks, bonds, real estate, and other capital assets.

- Rental and Royalty Income: Income from rental properties and royalties from intellectual property.

- Passive Activity Income: Income from businesses where the individual does not materially participate.

What is Excluded from Net Investment Income?

Certain types of income are excluded from the NIIT, including:

- Wages and Salaries: Income earned from employment.

- Social Security Benefits: Payments received from the Social Security Administration.

- Tax-Exempt Interest: Interest from municipal bonds and other tax-exempt investments.

- Distributions from Qualified Retirement Plans: While generally excluded, the impact on overall AGI is critical.

How the NIIT is Calculated

The NIIT is calculated as 3.8% of the lesser of:

- Net investment income, or

- The amount by which the taxpayer’s modified adjusted gross income (MAGI) exceeds the threshold for their filing status.

Example:

Let’s say John is a single filer with an AGI of $220,000 and net investment income of $30,000.

- AGI Exceeds Threshold: $220,000 – $200,000 (threshold) = $20,000

- NIIT Calculation: 3.8% of the lesser of $30,000 (net investment income) or $20,000 (AGI exceeding threshold) = 3.8% of $20,000 = $760

John would owe $760 in NIIT.

Why Understanding NIIT is Important

Understanding the NIIT is crucial for several reasons:

- Tax Planning: Knowing how the NIIT applies can help you make informed decisions about your investments and income strategies.

- Retirement Planning: Planning for IRA distributions and Roth conversions requires an understanding of how these actions can affect your NIIT liability.

- Investment Strategies: You may choose to adjust your investment portfolio to minimize NIIT exposure, such as favoring tax-exempt investments.

2. IRA Distributions and the Net Investment Income Tax

While distributions from traditional IRAs and Roth IRAs are generally not considered “net investment income” for the purpose of the NIIT, they can significantly impact your overall Adjusted Gross Income (AGI). This, in turn, can trigger or increase your NIIT liability on other investment income.

How IRA Distributions Affect AGI

Traditional IRA distributions are typically taxed as ordinary income in the year they are received. This income is added to your AGI, which can push you over the NIIT threshold. Roth IRA distributions, if they are qualified (i.e., meet certain age and holding period requirements), are tax-free and generally do not affect your AGI. However, non-qualified Roth IRA distributions can be taxable and therefore affect AGI.

Example:

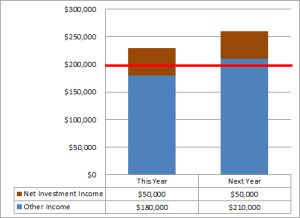

Consider Sarah, a single filer with the following income:

- Salary: $180,000

- Dividends: $15,000

- Capital Gains: $5,000

Without any IRA distributions, Sarah’s AGI would be $200,000, which is the NIIT threshold for single filers. If Sarah takes a $20,000 distribution from her traditional IRA, her AGI would increase to $220,000. This would trigger the NIIT on her investment income.

Scenarios Where IRA Distributions Trigger NIIT

- Crossing the Threshold: Even if your investment income is below the NIIT threshold, an IRA distribution can push your AGI over the limit, subjecting your investment income to the tax.

- Increasing NIIT Liability: If you are already subject to NIIT, an IRA distribution can increase the amount of your income that is subject to the tax.

Strategies to Manage IRA Distributions and NIIT

Several strategies can help you manage IRA distributions to minimize your NIIT liability:

- Tax Planning: Coordinate your IRA distributions with other income sources to keep your AGI below the NIIT threshold.

- Roth Conversions: Converting traditional IRA assets to a Roth IRA can reduce future taxable distributions, but be mindful of the immediate tax implications.

- Phased Withdrawals: Instead of taking a large distribution in one year, consider spreading withdrawals over several years to manage your AGI.

By carefully planning your IRA distributions, you can minimize the impact of the NIIT on your overall tax liability.

IRA Distributions and AGI

IRA Distributions and AGI

3. The Medicare Tax Crossover Zone

The Medicare Tax Crossover Zone refers to the income range where taking distributions from retirement accounts, such as IRAs, can indirectly trigger or increase the 3.8% Net Investment Income Tax (NIIT) on other investment income. This happens because these distributions, although not directly subject to NIIT, can push your Adjusted Gross Income (AGI) above the threshold where NIIT applies. Understanding this zone is crucial for effective tax planning.

Defining the Crossover Zone

The crossover zone occurs when some, but not all, of your investment income is above the NIIT threshold. In this scenario, taking additional income, like an IRA distribution, can push more of your investment income over the line, resulting in a higher NIIT liability.

Example:

Consider a single taxpayer, Alex, with $170,000 of employment income and $35,000 of capital gains. Their AGI would be $205,000, which means $5,000 of their capital gains would be subject to the 3.8% NIIT.

If Alex decides to take a $10,000 distribution from their traditional IRA, their AGI increases to $215,000. Now, $15,000 of their capital gains is subject to the NIIT. Even though the IRA distribution itself is not investment income, it caused more of the capital gains to be taxed under NIIT.

How Retirement Distributions Trigger the NIIT

Retirement distributions from traditional IRAs are typically taxed as ordinary income, adding to your AGI. Although these distributions are not considered “net investment income,” they can indirectly trigger or increase NIIT on other investment income.

Factors Influencing the Crossover Zone

- AGI Thresholds: The NIIT thresholds vary based on filing status. Being close to these thresholds increases the likelihood of entering the crossover zone.

- Single: $200,000

- Married Filing Jointly: $250,000

- Married Filing Separately: $125,000

- Head of Household: $200,000

- Amount of Investment Income: The more net investment income you have (e.g., dividends, capital gains, rental income), the greater the impact of the crossover zone.

- Size of Retirement Distributions: Larger distributions from traditional IRAs are more likely to push you into the crossover zone.

Planning Strategies to Navigate the Crossover Zone

- Income Smoothing: Distribute retirement income strategically over multiple years to stay below the NIIT threshold. This can help minimize the tax impact in any single year.

- Roth Conversions: Convert traditional IRA assets to a Roth IRA to reduce future taxable distributions. This strategy may increase your current tax liability but can be beneficial in the long run by avoiding future NIIT implications.

- Tax-Advantaged Investments: Prioritize investments that offer tax advantages, such as municipal bonds, which are exempt from federal income tax and NIIT.

- Careful Planning: Evaluate the impact of any retirement distributions on your AGI and potential NIIT liability. Use tax planning software or consult with a financial advisor to model different scenarios.

Real-World Examples

-

Scenario 1: Minimizing NIIT with Roth Conversions

- Lisa, a single filer, anticipates having significant capital gains in the current year. To mitigate the impact of NIIT, she decides to convert a portion of her traditional IRA to a Roth IRA. While this increases her taxable income for the current year, it reduces her future taxable retirement income, helping her manage her long-term tax liability.

-

Scenario 2: Strategic Income Distribution

- John and Mary, filing jointly, plan to retire soon. They strategize to take smaller, phased distributions from their traditional IRAs over several years to keep their AGI below the NIIT threshold. This allows them to avoid triggering NIIT while still accessing the funds they need for retirement.

Conclusion

Navigating the Medicare Tax Crossover Zone requires careful planning and a thorough understanding of how retirement distributions impact your AGI and potential NIIT liability. By employing strategic income smoothing, considering Roth conversions, and leveraging tax-advantaged investments, you can effectively manage your tax exposure and optimize your financial outcomes.

4. Strategies to Minimize the Impact of NIIT

Minimizing the impact of the Net Investment Income Tax (NIIT) requires a comprehensive approach that combines strategic tax planning, investment management, and income optimization. Here are several key strategies to consider:

Tax-Advantaged Investments

-

Municipal Bonds:

- Description: Municipal bonds are debt securities issued by state and local governments.

- Benefit: Interest income from municipal bonds is generally exempt from federal income tax and, in some cases, state and local taxes as well.

- Strategy: Allocate a portion of your investment portfolio to municipal bonds to reduce your overall taxable investment income.

-

Tax-Efficient Mutual Funds and ETFs:

- Description: These investment vehicles are designed to minimize taxable distributions.

- Benefit: Lower turnover rates and strategic tax management can reduce capital gains distributions.

- Strategy: Choose mutual funds and ETFs with a history of tax efficiency.

Strategic Income Planning

-

Income Smoothing:

- Description: Distributing income strategically over multiple years to avoid spikes in AGI.

- Benefit: Helps keep your income below the NIIT threshold in any single year.

- Strategy: Take smaller, phased withdrawals from retirement accounts rather than large, lump-sum distributions.

-

Roth Conversions:

- Description: Converting traditional IRA assets to a Roth IRA.

- Benefit: Reduces future taxable retirement income, potentially lowering your NIIT liability in retirement.

- Strategy: Convert a portion of your traditional IRA each year, considering the tax implications of the conversion itself.

-

Tax Loss Harvesting:

- Description: Selling investments at a loss to offset capital gains.

- Benefit: Reduces your overall taxable investment income.

- Strategy: Regularly review your portfolio for opportunities to harvest losses.

Optimizing Deductions and Credits

-

Maximize Above-the-Line Deductions:

- Description: Deductions that reduce your AGI, such as IRA contributions, student loan interest, and health savings account (HSA) contributions.

- Benefit: Lowering your AGI can help you stay below the NIIT threshold.

- Strategy: Fully utilize all eligible above-the-line deductions.

-

Itemize Deductions:

- Description: Claiming itemized deductions such as medical expenses, state and local taxes (SALT), and charitable contributions.

- Benefit: Reducing your taxable income and potentially lowering your NIIT liability.

- Strategy: Determine whether itemizing or taking the standard deduction results in a lower tax liability.

Real Estate Strategies

-

Rental Property Management:

- Description: Actively managing rental properties to qualify as a real estate professional.

- Benefit: Allows you to offset rental income with rental property expenses, potentially reducing your NIIT liability.

- Strategy: Meet the IRS requirements for real estate professional status, which include spending more than 50% of your working hours and more than 750 hours annually in real property trades or businesses.

-

Qualified Opportunity Zones (QOZ):

- Description: Investing in designated QOZs to defer or eliminate capital gains taxes.

- Benefit: Deferring capital gains can help you manage your NIIT liability.

- Strategy: Invest capital gains within 180 days in a Qualified Opportunity Fund (QOF).

Business Strategies

-

Pass-Through Entity Optimization:

- Description: Structuring your business as a pass-through entity (e.g., S corporation, partnership) and actively participating in the business.

- Benefit: Non-passive income from a pass-through entity is not subject to NIIT.

- Strategy: Ensure you meet the IRS requirements for material participation.

-

Retaining Earnings:

- Description: Retaining earnings within your business rather than distributing them as income.

- Benefit: Reduces your immediate taxable income.

- Strategy: Reinvest profits into your business for growth.

Advanced Planning Techniques

-

Charitable Remainder Trusts (CRT):

- Description: Transferring assets to a CRT, which provides income to you for a set period, with the remainder going to charity.

- Benefit: Can reduce capital gains taxes and provide income.

- Strategy: Consult with an estate planning attorney to establish a CRT.

-

Private Placement Life Insurance (PPLI):

- Description: A sophisticated insurance product used for wealth management.

- Benefit: Can provide tax-deferred growth and tax-free distributions.

- Strategy: Work with a financial advisor and insurance specialist to determine if PPLI is suitable for your situation.

Case Study

Consider John and Mary, a married couple filing jointly with an AGI of $260,000. They have significant investment income, including dividends, capital gains, and rental income.

-

Strategy Implemented:

- Invested in municipal bonds to reduce taxable investment income.

- Utilized tax loss harvesting to offset capital gains.

- Implemented income smoothing by taking phased withdrawals from their traditional IRAs.

-

Outcome:

- Reduced their NIIT liability by $1,500 annually.

- Optimized their overall tax situation.

By implementing these strategies, you can effectively minimize the impact of the Net Investment Income Tax on your investment portfolio and overall financial well-being. Remember to consult with a qualified tax advisor or financial planner to tailor these strategies to your specific circumstances.

5. The Role of Roth Conversions in NIIT Planning

Roth conversions involve transferring funds from a traditional IRA or other pre-tax retirement account into a Roth IRA. While Roth conversions can be a powerful tool for long-term tax planning, they also have immediate tax implications that can affect your Net Investment Income Tax (NIIT) liability. Understanding how Roth conversions interact with NIIT is essential for making informed financial decisions.

How Roth Conversions Work

When you convert funds from a traditional IRA to a Roth IRA, the amount converted is treated as ordinary income in the year of the conversion. This means that the converted amount is added to your Adjusted Gross Income (AGI), potentially pushing you over the NIIT threshold.

Immediate Tax Implications of Roth Conversions

- Increased AGI: The converted amount is added to your AGI, which can trigger or increase your NIIT liability.

- Potential for Higher Tax Bracket: The conversion can push you into a higher tax bracket, increasing your overall tax liability.

- No Immediate Deduction: Unlike contributions to a traditional IRA, you do not receive an immediate tax deduction for Roth conversions.

Long-Term Tax Benefits of Roth Conversions

- Tax-Free Growth: Once the funds are in a Roth IRA, they grow tax-free, and qualified distributions in retirement are also tax-free.

- No Required Minimum Distributions (RMDs): Roth IRAs are not subject to RMDs during the original owner’s lifetime, providing more flexibility in retirement.

- Estate Planning Benefits: Roth IRAs can be a valuable asset to pass on to heirs, as they can continue to grow tax-free for the beneficiaries.

NIIT Considerations When Planning Roth Conversions

- Crossing the NIIT Threshold: Be aware that a Roth conversion can push your AGI over the NIIT threshold, subjecting your investment income to the 3.8% tax.

- Increasing NIIT Liability: If you are already subject to NIIT, a Roth conversion can increase the amount of your income that is subject to the tax.

Strategies for Managing Roth Conversions and NIIT

-

Assess Your Current and Future Tax Situation:

- Consider your current income, expected future income, and potential investment income when deciding whether to convert.

-

Determine the Optimal Conversion Amount:

- Convert only the amount that keeps you below the NIIT threshold or in a favorable tax bracket.

-

Spread Conversions Over Multiple Years:

- Instead of converting a large amount in one year, spread the conversions over several years to manage your AGI.

-

Consider Other Tax Planning Strategies:

- Coordinate Roth conversions with other tax planning strategies, such as tax-loss harvesting and maximizing deductions.

-

Utilize Tax Planning Software:

- Use tax planning software to model different scenarios and assess the impact of Roth conversions on your NIIT liability.

Case Study: Minimizing NIIT with Strategic Roth Conversions

Consider Sarah, a single filer with the following income:

- Salary: $160,000

- Dividends: $20,000

- Capital Gains: $10,000

Without any Roth conversions, Sarah’s AGI would be $190,000, which is below the NIIT threshold for single filers ($200,000).

If Sarah converts $20,000 from her traditional IRA to a Roth IRA, her AGI would increase to $210,000. This would trigger the NIIT on her investment income, as her AGI now exceeds the threshold.

However, if Sarah only converts $10,000, her AGI would be $200,000, right at the threshold. While no NIIT would be due, she has strategically moved some funds into a Roth IRA for future tax-free growth.

Conclusion

Roth conversions can be a valuable tool for long-term tax planning, but it’s essential to consider the immediate tax implications, including the potential impact on your NIIT liability. By carefully planning your Roth conversions and coordinating them with other tax strategies, you can maximize the benefits while minimizing your tax exposure.

6. Real-Life Scenarios and Case Studies

To illustrate the complexities and planning opportunities surrounding the Net Investment Income Tax (NIIT) and IRA distributions, let’s explore several real-life scenarios and case studies.

Scenario 1: The Impact of a Large IRA Distribution on NIIT

Background:

- John and Mary are a married couple filing jointly.

- John recently retired and started taking distributions from his traditional IRA to cover living expenses.

- Their income sources include:

- Social Security: $40,000

- Dividends: $20,000

- Capital Gains: $10,000

- IRA Distribution: $40,000

Situation:

Without the IRA distribution, their AGI would be $70,000 (Social Security, Dividends, and Capital Gains). By adding the $40,000 IRA distribution, their AGI increases to $110,000.

NIIT Implications:

Since their AGI is below the NIIT threshold for married couples filing jointly ($250,000), the IRA distribution does not trigger the NIIT in this case.

Planning Opportunity:

John and Mary could consider taking larger IRA distributions in years when their AGI is lower to avoid triggering the NIIT in the future.

Scenario 2: Strategic Roth Conversions to Minimize NIIT

Background:

- Lisa is a single filer with the following income:

- Salary: $170,000

- Dividends: $25,000

- Capital Gains: $5,000

Situation:

Lisa’s AGI without any Roth conversions would be $200,000, which is the NIIT threshold for single filers. She wants to convert a portion of her traditional IRA to a Roth IRA to take advantage of future tax-free growth.

NIIT Implications:

If Lisa converts $10,000 from her traditional IRA to a Roth IRA, her AGI would increase to $210,000. This would trigger the NIIT on her investment income, as her AGI now exceeds the threshold.

Strategic Planning:

To mitigate the impact of NIIT, Lisa could:

- Convert a smaller amount: Convert only the amount that keeps her AGI at or slightly below the NIIT threshold.

- Spread conversions over multiple years: Convert a portion of her traditional IRA each year, rather than converting a large amount in a single year.

- Consider tax-loss harvesting: Offset capital gains with capital losses to reduce her overall taxable investment income.

Case Study 1: Managing Rental Income and NIIT

Background:

- The Smiths are a married couple filing jointly.

- They own several rental properties, generating significant rental income.

- Their income sources include:

- Wages: $200,000

- Rental Income (after expenses): $60,000

- Dividends: $10,000

Situation:

Their AGI is $270,000, which exceeds the NIIT threshold for married couples filing jointly ($250,000).

NIIT Implications:

The Smiths are subject to NIIT on the lesser of their net investment income or the amount by which their AGI exceeds the threshold:

- Net Investment Income: $70,000 (Rental Income + Dividends)

- AGI Exceeding Threshold: $270,000 – $250,000 = $20,000

- NIIT: 3.8% of $20,000 = $760

Strategic Planning:

To minimize their NIIT liability, the Smiths could:

- Increase Rental Property Expenses: Invest in property improvements or repairs to increase their rental property expenses, reducing their net rental income.

- Invest in Qualified Opportunity Zones (QOZ): Defer capital gains taxes by investing in QOZs, which can help manage their NIIT liability.

Case Study 2: The Impact of Business Income on NIIT

Background:

- Mark is a single filer who owns a successful consulting business.

- His income sources include:

- Business Income (after expenses): $180,000

- Dividends: $30,000

Situation:

If Mark is an active participant in his business, the business income is not subject to NIIT. However, the dividend income is subject to NIIT if his AGI exceeds the threshold.

NIIT Implications:

Mark’s AGI is $210,000, which exceeds the NIIT threshold for single filers ($200,000).

- NIIT: 3.8% of ($210,000 – $200,000) = $380

Strategic Planning:

To minimize his NIIT liability, Mark could:

- Increase Business Expenses: Invest in his business to increase expenses and reduce his net business income.

- Maximize Deductions: Take advantage of all eligible deductions, such as SEP IRA contributions, to reduce his AGI.

Key Takeaways

These scenarios and case studies illustrate the importance of understanding the NIIT and its implications for your specific financial situation. By carefully planning your income, investments, and deductions, you can minimize your NIIT liability and optimize your overall tax situation.

7. Finding Partners and Opportunities on Income-Partners.net

Navigating the complexities of investment income, taxes, and financial planning can be significantly easier with the right partners and opportunities. Income-partners.net offers a platform designed to connect individuals with the resources and partnerships needed to optimize their financial strategies. Here’s how you can leverage income-partners.net to enhance your financial planning and minimize the impact of the Net Investment Income Tax (NIIT).

Identifying Potential Partners on Income-Partners.net

-

Financial Advisors and Tax Professionals:

- Benefit: Access to experts who can provide personalized advice on tax planning, investment strategies, and retirement planning.

- Opportunity: Connect with advisors who specialize in NIIT planning and can help you develop a customized strategy to minimize your tax liability.

-

Real Estate Professionals:

- Benefit: Guidance on investing in rental properties, managing rental income, and utilizing real estate strategies to reduce your NIIT liability.

- Opportunity: Find professionals who can help you identify and manage rental properties, maximizing your returns while minimizing your tax exposure.

-

Business Consultants:

- Benefit: Assistance with structuring your business to minimize your NIIT liability, optimizing your business expenses, and maximizing deductions.

- Opportunity: Connect with consultants who can help you structure your business as a pass-through entity and ensure you meet the requirements for material participation.

-

Investment Specialists:

- Benefit: Access to investment specialists who can help you identify tax-efficient investments, manage your portfolio, and implement strategies such as tax-loss harvesting.

- Opportunity: Find specialists who can guide you in selecting tax-advantaged investments, such as municipal bonds and tax-efficient mutual funds.

Leveraging Opportunities on Income-Partners.net

-

Educational Resources:

- Benefit: Access to articles, guides, and webinars that provide valuable information on NIIT planning, tax strategies, and investment management.

- Opportunity: Stay informed about the latest tax laws, regulations, and strategies to minimize your NIIT liability.

-

Networking Events:

- Benefit: Opportunities to connect with other individuals, professionals, and experts in the financial industry.

- Opportunity: Attend events where you can learn from others, share your experiences, and build valuable relationships.

-

Partnership Programs:

- Benefit: Access to partnership programs that connect you with professionals who can provide specialized services and support.

- Opportunity: Partner with financial advisors, tax professionals, and investment specialists who can help you develop a customized plan to minimize your NIIT liability.

-

Community Forums:

- Benefit: Engage with other individuals, ask questions, and share your experiences in a supportive online community.

- Opportunity: Learn from others, gain insights into different tax planning strategies, and build a network of contacts.

Success Stories from Income-Partners.net

-

Sarah’s Story:

- Sarah, a single filer, used income-partners.net to connect with a financial advisor who helped her develop a Roth conversion strategy that minimized her NIIT liability while maximizing her long-term tax benefits.

-

The Smith’s Story:

- The Smiths, a married couple filing jointly, used income-partners.net to find a real estate professional who helped them manage their rental properties more efficiently, reducing their rental income and minimizing their NIIT liability.

-

Mark’s Story:

- Mark, a business owner, used income-partners.net to connect with a business consultant who helped him structure his business to optimize expenses and deductions, reducing his overall taxable income and minimizing his NIIT liability.

Tips for Maximizing Your Experience on Income-Partners.net

-

Create a Detailed Profile:

- Provide accurate and detailed information about your income, investments, and financial goals to attract the right partners and opportunities.

-

Engage Actively:

- Participate in community forums, attend networking events, and connect with other members to build valuable relationships.

-

Utilize the Resources:

- Take advantage of the educational resources, partnership programs, and other tools available on income-partners.net to enhance your financial planning and minimize your NIIT liability.

By leveraging the resources and opportunities available on income-partners.net, you can connect with the partners and experts you need to navigate the complexities of investment income, taxes, and financial planning, ultimately optimizing your financial situation and minimizing the impact of the Net Investment Income Tax.

Are you ready to take control of your financial future? Visit income-partners.net today to explore partnership opportunities, learn effective tax strategies, and connect with financial professionals who can help you minimize your NIIT liability and achieve your financial goals in the USA. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

8. Common Mistakes to Avoid

When dealing with the Net Investment Income Tax (NIIT) and IRA distributions, there are several common mistakes that taxpayers make. Avoiding these pitfalls can help you minimize your tax liability and optimize your financial planning.

1. Not Understanding the NIIT Thresholds

Mistake:

- Failing to recognize the income thresholds for the NIIT, which vary based on filing status.

Consequence:

- Incorrectly estimating your NIIT liability and missing opportunities for tax planning.

Solution:

- Familiarize yourself with the NIIT thresholds for your filing status:

- Single: $200,000

- Married Filing Jointly: $250,000

- Married Filing Separately: $125,000

2. Ignoring the Impact of IRA Distributions on AGI

Mistake:

- Overlooking how IRA distributions can increase your Adjusted Gross Income (AGI) and trigger the NIIT.

Consequence:

- Unexpectedly being subject to the NIIT on your investment income.

Solution:

- Carefully plan your IRA distributions, considering their impact on your AGI and potential NIIT liability.

- Use tax planning software or consult with a financial advisor to model different scenarios.

3. Neglecting Roth Conversions

Mistake:

- Not considering Roth conversions as a strategic tool to manage your NIIT liability.

Consequence:

- Missing out on the long-term tax benefits of Roth IRAs and potentially overpaying taxes in retirement.

Solution:

- Evaluate whether Roth conversions are appropriate for your situation, considering your current and future tax rates, investment income, and retirement goals.

- Spread conversions over multiple years to manage your AGI and minimize the immediate tax impact.

4. Not Maximizing Deductions and Credits

Mistake:

- Failing to take advantage of all eligible deductions and credits that can reduce your AGI.

Consequence:

- Paying more taxes than necessary and missing opportunities to lower your NIIT liability.

Solution:

- Maximize above-the-line deductions, such as IRA contributions, student loan interest, and health savings account (HSA) contributions.

- Itemize deductions if it results in a lower tax liability, claiming deductions such as medical expenses, state and local taxes (SALT), and charitable contributions.

5. Not Managing Investment Income Effectively

Mistake:

- Failing to manage your investment portfolio to minimize taxable investment income.

Consequence:

- Paying unnecessary NIIT on your investment income.

Solution:

- Invest in tax-efficient investments, such as municipal bonds and tax-efficient mutual funds.

- Utilize tax-loss harvesting to offset capital gains with capital losses.

6. Not Considering State Taxes

Mistake:

- Overlooking the impact of state taxes on your overall tax liability.

Consequence:

- Making tax planning decisions that are not optimal for your specific state.

Solution:

- Consider the state tax implications of your financial decisions, as some states have their own investment income taxes or may tax IRA distributions differently.

- Consult with a tax advisor who is familiar with the tax laws in your state.

7. Not Seeking Professional Advice

Mistake:

- Attempting to navigate the complexities of NIIT and IRA distributions without seeking professional advice.

Consequence:

- Making costly mistakes and missing opportunities to optimize your tax planning.

Solution:

- Consult with a qualified tax advisor or financial planner who can provide personalized advice based on your specific circumstances.

- Ensure that your advisor has experience with NIIT planning and can help you develop a customized strategy to minimize your tax liability.

8. Ignoring Changes in Tax Laws

Mistake:

- Failing to stay informed about changes in tax laws and regulations that can impact your NIIT liability.

Consequence:

- Making tax planning decisions based on outdated information, potentially leading to errors and missed opportunities.

Solution:

- Stay informed about the latest tax laws, regulations, and rulings.

- Subscribe to reputable tax publications and consult with a tax advisor regularly to ensure your tax planning is up-to-date.

9. Assuming IRA Distributions are Always Taxed the Same

Mistake:

- Assuming that all IRA distributions are taxed as ordinary income.

Consequence:

- Missing opportunities to take advantage of tax-free Roth IRA distributions.

Solution:

- Understand the tax implications of different types of IRA distributions, including traditional IRA distributions, Roth IRA distributions, and Roth conversions.

- Plan your distributions strategically to minimize your overall tax liability.

By avoiding these common mistakes, you can effectively manage your NIIT liability, optimize your financial planning, and achieve your financial goals.

9. Future Trends in NIIT and Retirement Planning

The landscape of tax laws and retirement planning is constantly evolving, making it essential to stay informed about potential future trends in the Net Investment Income Tax (NIIT) and related areas. Here are some key trends to watch:

1. Potential Changes to the NIIT Thresholds and Rates

-

Trend:

- Future tax legislation could alter the NIIT thresholds