Does Medicaid Look At Household Income? Absolutely, and understanding how it affects your eligibility is key, especially if you’re seeking partnership opportunities to boost your income through income-partners.net. This guide will clarify how Medicaid assesses income, helping you navigate eligibility requirements and explore partnership avenues for financial growth. Understanding how your household income is assessed for Medicaid eligibility can open doors to strategic partnerships that enhance your financial stability.

1. What is MAGI and How Does it Relate to Medicaid Eligibility?

Yes, MAGI or Modified Adjusted Gross Income is the methodology used to determine income for Medicaid and CHIP eligibility, based on tax definitions of income and household. MAGI rules count income for Medicaid, CHIP, and premium tax credit eligibility.

Understanding MAGI

MAGI is a standardized approach used to assess financial eligibility for Medicaid and the Children’s Health Insurance Program (CHIP). According to healthcare.gov, MAGI impacts how most people apply and enroll for coverage, determining both eligibility and cost. It simplifies the process by aligning income calculations with federal income tax rules.

Key Components of MAGI

- Tax-Based Income: MAGI uses your adjusted gross income (AGI) from your tax return, plus any tax-exempt interest income, Social Security benefits, and foreign earned income.

- Household Composition: MAGI considers who is included in your household. This can impact eligibility, as Medicaid looks at household income rather than individual income in many cases.

- No Asset Tests: Unlike traditional Medicaid rules, MAGI does not consider assets like savings accounts or property when determining eligibility.

How MAGI Affects Medicaid Eligibility

MAGI is used to determine whether you qualify for Medicaid based on your income level. States set income thresholds, and if your MAGI falls below these thresholds, you may be eligible for Medicaid coverage.

According to a report by the Kaiser Family Foundation (KFF), the Affordable Care Act (ACA) expanded Medicaid eligibility based on MAGI, allowing more low-income individuals and families to access healthcare coverage.

2. Who Must Follow MAGI Rules for Medicaid Eligibility?

MAGI rules must be followed in all states regardless of the decision to expand Medicaid, but these rules only apply to specific categories of Medicaid eligibility, including parents and caregiver relatives, children, pregnant women, and the adult expansion group. States continue to use previous rules for the elderly, disabled, and children in foster care.

Categories Affected by MAGI

- Parents and Caregiver Relatives: Parents and relatives who act as caregivers for children often fall under MAGI rules. Their household income is assessed to determine Medicaid eligibility.

- Children: Eligibility for children is primarily determined using MAGI. Many states offer Medicaid or CHIP coverage to children in families with incomes above the standard Medicaid limits.

- Pregnant Women: Pregnant women are also assessed using MAGI. Many states provide Medicaid coverage to pregnant women with incomes higher than the typical Medicaid thresholds to ensure prenatal care.

- Adult Expansion Group: The Affordable Care Act (ACA) expanded Medicaid to cover adults with incomes up to 138% of the federal poverty level (FPL) in states that chose to expand Medicaid. This expansion group is evaluated using MAGI rules.

Non-MAGI Categories

- Elderly: Elderly individuals often qualify for Medicaid based on traditional income and asset tests, rather than MAGI.

- Disabled: People with disabilities may also be evaluated using traditional Medicaid rules, which consider both income and assets.

- Children in Foster Care: Children in foster care typically have separate eligibility criteria that do not fall under MAGI rules.

3. How Do Medicaid and Premium Tax Credit Household Rules Differ Under MAGI?

Medicaid and CHIP households are determined based on family, tax relationships, and living arrangements, affecting which Medicaid household rules apply. Premium tax credit household rules are based purely on tax relationships. The primary difference is that Medicaid household size and composition are determined separately for each member, whereas premium tax credit treats all members of a tax unit as a household. Medicaid also offers states options that affect household definitions, while premium tax credit rules are federally consistent.

Key Differences

-

Household Composition:

- Medicaid: Household size and composition are determined individually for each member. This means that within the same family, different members might have different household sizes for Medicaid purposes.

- Premium Tax Credit: All members of a tax unit are treated as a single household. If a family files taxes together, all members will have the same household size for premium tax credit calculations.

-

Flexibility:

- Medicaid: States have some flexibility in defining households for Medicaid eligibility. This can lead to variations in how household income is assessed across different states.

- Premium Tax Credit: The rules for premium tax credits are set at the federal level and are consistent across all states.

-

Tax Relationships:

- Medicaid: While tax relationships are considered, they are not the sole determinant of household composition. Living arrangements and family relationships also play a role.

- Premium Tax Credit: Household rules are based purely on tax relationships. The individuals included in your tax return determine your household size for the premium tax credit.

Example Scenario

Consider a family of three: a mother, a father, and their child. They file their taxes jointly.

- For Medicaid: Each family member’s household size might be assessed differently based on specific state rules and their individual circumstances. For instance, if the child is under 19 and living with both parents, the household might include the child, both parents, and any siblings.

- For Premium Tax Credit: All three family members would be considered part of the same household, and their household size would be three.

Understanding these distinctions is crucial for accurately determining eligibility for both Medicaid and premium tax credits.

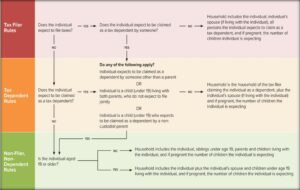

4. How Does Medicaid Determine Who is in a Household?

Medicaid determines household membership based on an individual’s plan to file a tax return, regardless of actual filing. It considers whether the individual plans to be a tax filer, a tax dependent, or neither, which dictates the applicable Medicaid household rules.

Factors Influencing Household Determination

- Tax Filer: If an individual plans to file a tax return and claim their own exemption, their household includes their spouse (if filing jointly) and anyone they claim as a tax dependent.

- Tax Dependent: If an individual expects to be claimed as a tax dependent, their household is the same as the tax filer claiming them, with a few exceptions.

- Non-Filer: For individuals who neither file a tax return nor are claimed as a tax dependent, household rules vary based on age.

Specific Rules for Different Scenarios

- Tax Filers: The household includes the tax filer, their spouse (if filing jointly), and all claimed dependents.

- Tax Dependents: Generally, the household is the same as the tax filer’s. However, exceptions apply when the individual is:

- Expected to be claimed by someone other than a parent.

- Under 19, living with both parents who do not file jointly.

- Under 19, claimed by a non-custodial parent.

- Non-Filers:

- 19 and Older: The household includes the individual, their spouse (if applicable), and children under 19 living with them.

- Under 19: The household includes the individual, siblings under 19, their children, and parents living with them.

Examples to Illustrate Household Determination

- Tax Filer: John files taxes, claiming his wife and two children as dependents. His Medicaid household includes himself, his wife, and their two children.

- Tax Dependent: Lisa, 16, is claimed as a tax dependent by her parents. Her Medicaid household is the same as her parents’ household.

- Non-Filer (Adult): Michael, 25, does not file taxes and is not claimed as a dependent. His Medicaid household includes himself and his spouse, if applicable.

- Non-Filer (Minor): Emily, 17, lives with her parents and siblings but is not claimed as a dependent. Her Medicaid household includes herself, her parents, and her siblings under 19.

5. What Are The Household Rules For A Tax Filer?

For tax filers claiming their own exemption and who can’t be claimed as a tax dependent, the household includes the tax filer, the spouse filing jointly, and everyone whom the tax filer claims as a tax dependent.

Defining the Tax Filer Household

When an individual files their taxes and claims their own exemption, their household for Medicaid purposes includes:

- The tax filer themselves.

- Their spouse, if they are filing jointly.

- Anyone whom the tax filer claims as a tax dependent.

This rule is straightforward and aligns with the IRS definition of a tax household.

Example Scenario

Let’s consider a hypothetical scenario:

- Tax Filer: David

- Spouse: Sarah (filing jointly with David)

- Dependents: Their two children, Emily (age 10) and Tom (age 15)

In this case, David’s Medicaid household would include David, Sarah, Emily, and Tom. This is because David is the tax filer, Sarah is his spouse filing jointly, and Emily and Tom are their tax dependents.

Implications for Medicaid Eligibility

The income of everyone in the tax filer’s household is considered when determining Medicaid eligibility. This means that the combined income of David, Sarah, Emily, and Tom would be assessed against the Medicaid income thresholds for their state.

Why This Rule Matters

This rule ensures that Medicaid eligibility is based on the resources available to the entire family unit, rather than just the individual applying for coverage. It prevents individuals from artificially reducing their household size to qualify for Medicaid.

6. What Are The Household Rules For Tax Dependents?

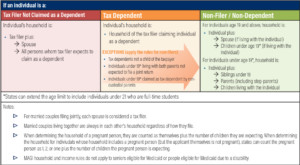

For tax dependents, the household is the same as the tax filer claiming the individual as a tax dependent. However, there are three exceptions to this rule, when the rule for non-filers is applied: Individuals who expect to be claimed as a dependent by someone other than a parent, Individuals (under 19) living with both parents, whose parents do not expect to file a joint tax return, and Individuals (under 19) who expect to be claimed as a dependent by a non-custodial parent.

General Rule for Tax Dependents

Generally, if you are claimed as a tax dependent, your Medicaid household is the same as the household of the person who claims you. This means that Medicaid considers the income and household composition of the tax filer when determining your eligibility.

Exceptions to the Rule

There are three key exceptions where the non-filer rules apply:

- Dependents Claimed by Non-Parents: If you are claimed as a dependent by someone other than your parent (e.g., a grandparent, aunt, or guardian), the non-filer rules apply.

- Minors Living with Parents Not Filing Jointly: If you are under 19 and living with both parents who do not expect to file a joint tax return, the non-filer rules apply.

- Minors Claimed by Non-Custodial Parents: If you are under 19 and expect to be claimed as a dependent by a non-custodial parent, the non-filer rules apply.

How the Non-Filer Rules Apply

Under the non-filer rules:

- For Individuals 19 and Older: The household includes the individual, their spouse (if living together), and any children under 19 living with them.

- For Individuals Under 19: The household includes the individual, any siblings under 19, children of the individual, and parents living with them.

Example Scenarios

- Claimed by Grandparent:

- Scenario: 10-year-old Lily lives with her grandparents, who claim her as a tax dependent.

- Rule Applied: Non-filer rules apply because Lily is claimed by someone other than her parents.

- Lily’s Household: Lily, her grandparents, and any other relatives under 19 living in the same household.

- Parents Not Filing Jointly:

- Scenario: 17-year-old David lives with both parents, but they file separate tax returns. One parent claims David as a dependent.

- Rule Applied: Non-filer rules apply because David’s parents do not file jointly.

- David’s Household: David, both parents, and any siblings under 19 living in the same household.

- Claimed by Non-Custodial Parent:

- Scenario: 16-year-old Maria lives primarily with her mother but is claimed as a dependent by her father (non-custodial parent).

- Rule Applied: Non-filer rules apply because Maria is claimed by a non-custodial parent.

- Maria’s Household: Maria, her mother, and any siblings under 19 living in the same household.

7. What Are The Household Rules For People Who Neither File A Tax Return Nor Are Claimed As A Tax Dependent?

For individuals who neither file a tax return nor are claimed as a tax dependent, the household rules differ based on whether the individual is an adult or a minor: For individuals 19 years and older, the household includes the individual plus, if living with the individual, their or her spouse and children who are under 19 years old. For individuals under 19 years old, the household includes the individual, plus any siblings under 19 years old, children of the individual and parents who live with the individual.

Household Rules for Non-Filers

When an individual does not file a tax return and is not claimed as a tax dependent, Medicaid determines their household based on their age:

- Individuals 19 Years and Older:

- The household includes the individual.

- If living with the individual, their spouse is included.

- Children under 19 living with the individual are included.

- Individuals Under 19 Years Old:

- The household includes the individual.

- Any siblings under 19 living with the individual are included.

- Children of the individual are included.

- Parents living with the individual are included.

Practical Examples

-

Adult Non-Filer (25 Years Old):

- Scenario: Emily, 25, does not file taxes and is not claimed as a dependent. She lives with her spouse, Alex, and their 2-year-old child, Sam.

- Household Composition: Emily’s household includes Emily, Alex, and Sam.

-

Minor Non-Filer (17 Years Old):

- Scenario: David, 17, does not file taxes and is not claimed as a dependent. He lives with his parents and his 15-year-old sister, Lisa.

- Household Composition: David’s household includes David, his parents, and Lisa.

-

Adult Non-Filer with No Dependents or Spouse (30 Years Old):

- Scenario: Sarah, 30, does not file taxes and is not claimed as a dependent. She lives alone.

- Household Composition: Sarah’s household includes only Sarah.

-

Minor Non-Filer with a Child (18 Years Old):

- Scenario: Maria, 18, does not file taxes and is not claimed as a dependent. She lives with her parents and her 1-year-old child, Junior.

- Household Composition: Maria’s household includes Maria, Junior, and her parents.

Household of a child

Household of a child

Key Considerations

- Living Arrangements: The primary factor in determining the household is who the individual lives with.

- Age Threshold: The age of 19 is a critical threshold for differentiating between adult and minor non-filers.

- Spouses and Children: Spouses and children under 19 are generally included in the household of adult non-filers.

- Parents and Siblings: Parents and siblings under 19 are included in the household of minor non-filers.

8. Are There Any Adjustments To The Three Rules Based On People’s Tax Filing?

Yes, In addition to the general rules for determining household size, some rules apply in all situations: Married couples who live together are always counted in each other’s household regardless of whether they file a joint or separate return and Family size adjustments need to be made if the individual is pregnant. In determining the household of a pregnant person, they are counted as themself plus the number of children they are expected to deliver.

Adjustments to Household Rules

Regardless of tax filing status, certain adjustments always apply:

- Married Couples: Married couples who live together are always included in each other’s household, regardless of whether they file jointly or separately.

- Pregnant Individuals: A pregnant individual is counted as themselves plus the number of children they are expected to deliver.

Detailed Explanation of Adjustments

-

Married Couples Living Together:

- Rule: If a married couple lives together, they are always considered part of the same household, even if they file separate tax returns.

- Rationale: This rule ensures that the resources available to both spouses are considered when determining Medicaid eligibility, regardless of their tax filing status.

- Example: John and Mary are married and live together. John files his taxes separately from Mary. Despite filing separately, they are both part of the same Medicaid household.

-

Pregnant Individuals:

- Rule: When determining the household size of a pregnant individual, they are counted as themselves plus the number of children they are expecting to deliver.

- Rationale: This adjustment accounts for the additional resources needed to support the unborn child or children.

- Example: Sarah is pregnant with twins. For Medicaid purposes, she is counted as three individuals (herself plus two children).

Impact on Medicaid Eligibility

These adjustments can significantly impact Medicaid eligibility:

- Married Couples: Including both spouses in the same household ensures that their combined income is assessed, which may affect their eligibility.

- Pregnant Individuals: Counting a pregnant individual as multiple household members increases the household size, potentially raising the income threshold for eligibility.

9. What Are Different Options That States Have For Implementing MAGI?

States have flexibility in how they implement the MAGI rules in two areas: First, in some instances the Medicaid household rules applied may depend on whether an individual is under 19 years old or not. Where the rules indicate an age limit, states have the option to extend that age limit to 21 if the individual is a full-time student. Second, for individuals whose household includes a pregnant person (but are not pregnant themselves), states can count the pregnant person as one, two, or one plus the number of children they are expecting.

State Options in Implementing MAGI

States have some flexibility in implementing MAGI rules, primarily in two areas:

- Age Limit for Students:

- Standard Rule: Medicaid household rules often differentiate between individuals under 19 years old and those 19 and older.

- State Option: States can extend the age limit to 21 for full-time students. This means that if a full-time student is under 21, they may be treated as part of their parents’ household, even if they would otherwise be considered an independent adult.

- Impact: This option can help students remain covered under their parents’ Medicaid, ensuring they have access to healthcare while pursuing their education.

- Counting Pregnant Individuals:

- Standard Rule: When determining the household size of a pregnant individual, they are counted as themselves plus the number of expected children.

- State Option: For individuals whose household includes a pregnant person (but are not pregnant themselves), states can choose to count the pregnant person as one, two, or one plus the number of children they are expecting.

- Impact: This flexibility allows states to adjust household size calculations to better reflect the needs of pregnant individuals and their families.

Examples of State Implementation

- Extending Age Limit for Students:

- Scenario: A state decides to extend the age limit to 21 for full-time students.

- Application: A 20-year-old full-time college student is claimed as a dependent by their parents. Under the state’s extended age limit, the student is considered part of their parents’ Medicaid household, even though they would be considered an adult under the standard rule.

- Counting Pregnant Individuals:

- Scenario: A state decides to count a pregnant individual as two household members.

- Application: A family of three (two parents and one child) includes a pregnant mother. The state counts the pregnant mother as two household members, increasing the family size to four for Medicaid eligibility purposes.

Married parents

Married parents

Implications for Medicaid Eligibility

- For Students: Extending the age limit can help full-time students maintain coverage under their parents’ Medicaid, providing them with access to necessary healthcare services.

- For Pregnant Individuals: How a state counts pregnant individuals can affect the income thresholds for Medicaid eligibility, potentially allowing more pregnant women and their families to qualify for coverage.

10. Are Married Couples Who File Taxes Separately Considered To Be In Separate Households?

Generally, no. Married couples who live together are always considered to be in each other’s household regardless of how they file taxes. However, married couples who don’t live together and who file taxes separately will be considered as separate households.

General Rule: Married Couples Living Together

The general rule is that married couples who live together are always considered part of the same household, regardless of their tax filing status. This means that even if they file their taxes separately, Medicaid will consider them as one household.

Exception: Married Couples Not Living Together

The exception to this rule is when married couples do not live together. In such cases, they are considered separate households for Medicaid purposes, especially if they file taxes separately.

Why This Rule Exists

- Combined Resources: The rule acknowledges that married couples who live together often share resources and finances, regardless of how they file their taxes.

- Preventing Manipulation: It prevents couples from manipulating their household size to qualify for Medicaid when they otherwise would not.

Examples

-

Married Couple Living Together, Filing Separately:

- Scenario: John and Mary are married and live in the same house. They choose to file their taxes separately.

- Medicaid Determination: Despite filing separately, Medicaid considers John and Mary to be part of the same household.

-

Married Couple Not Living Together, Filing Separately:

- Scenario: Sarah and Tom are married but live in different states due to work. They file their taxes separately.

- Medicaid Determination: Sarah and Tom are considered separate households for Medicaid purposes.

-

Married Couple Living Together, One Spouse Not Filing:

- Scenario: Emily and Chris are married and live together. Emily files taxes, but Chris does not.

- Medicaid Determination: Emily and Chris are considered part of the same household.

Impact on Medicaid Eligibility

The determination of whether a married couple is considered part of the same household significantly impacts Medicaid eligibility:

- Combined Income: When couples are considered part of the same household, their combined income is used to determine eligibility.

- Household Size: A larger household size may increase the income threshold for eligibility.

11. How Does Medicaid Determine The Household Size Of Family Members When The Parents Live Together But Are Not Married?

As long as both parents file taxes, non-married parents living in the same household would still use the rule for tax filers to determine each parent’s Medicaid household. This means their household includes themselves and anyone claimed as a dependent on their tax return. However, a child under 19 living with non-married parents and being claimed as a tax dependent by one of the parents, would fall into the non-filer rule. Therefore, the child’s household size for Medicaid would include themself, both parents, and any siblings living with the child.

Rules for Non-Married Parents Living Together

When parents live together but are not married, Medicaid determines household size based on the following rules:

- Tax Filers: If both parents file taxes, each parent’s household includes themselves and anyone they claim as a dependent on their tax return.

- Children Under 19: A child under 19 living with both parents and claimed as a tax dependent by one parent falls under the non-filer rule. The child’s household includes themselves, both parents, and any siblings living with them.

Detailed Explanation

- Tax Filer Rule: Each parent who files taxes includes in their household anyone they claim as a dependent. This aligns with standard tax-based household determinations.

- Non-Filer Rule Exception: Children living with both parents are treated differently. Even if one parent claims the child as a dependent, the child’s household includes both parents and all siblings under 19.

Example Scenario

- Scenario: Lisa and Mark live together with their two children, Emily (10) and Tom (15). Lisa claims Emily and Tom as tax dependents. Mark files as a single person and claims no dependents.

- Lisa’s Household: Lisa and anyone claimed as a dependent, so only Lisa is in her household.

- Mark’s Household: Mark and anyone claimed as a dependent, so only Mark is in his household.

- Emily’s and Tom’s Household: Because they are children under 19 living with both parents, their household includes Emily, Tom, Lisa, and Mark.

Practical Implications

This approach ensures that Medicaid considers the resources available to the entire family unit when determining eligibility for children, even if the parents are not married.

12. How Does Medicaid Determine The Household Of An Adult Child Who Is Claimed As A Tax Dependent By His Parents?

The household of an individual who is at least 19 years old and is claimed as a tax dependent by their parents is always the same as the household of the parents claiming them. This is true even if the individual was much older, say 35 years old. For example, under some circumstances parents can claim their child who is 35 years old as a qualifying relative on their tax return. In this scenario, Medicaid would use the tax dependent rule for determining the household of this individual, which means their household would be the same as the household of their parent (the tax filer) claiming them as a dependent. The following examples illustrate how the Medicaid rules would be applied:

General Rule for Adult Children

When an adult child (19 years or older) is claimed as a tax dependent by their parents, their Medicaid household is the same as their parents’ household. This rule applies regardless of the adult child’s age.

Detailed Explanation

- Tax Dependent Rule: The adult child’s household is determined by the tax filer’s household.

- Age Irrelevance: Even if the adult child is significantly older (e.g., 35 years old), the same rule applies if they are claimed as a dependent.

Example Scenarios

- Adult Child Claimed as Dependent:

- Scenario: John, 29, is claimed as a tax dependent by his parents. His parents also claim his younger siblings, 15 and 17.

- Medicaid Determination: John’s Medicaid household includes himself, his parents, and his younger siblings (household size of five).

- Adult Child Living with Parents Filing Separately:

- Scenario: Carla, 28, lives with her parents who file separate tax returns. Her father claims her as a dependent.

- Medicaid Determination: Even though her parents file separately, they are considered in the same household. Carla’s father’s household includes himself, his spouse, and Carla (household size of three). Therefore, Carla’s household is also three.

Practical Implications

This rule ensures that the adult child’s Medicaid eligibility is based on the resources available to the entire family unit, as defined by the tax filer’s household.

13. Does The Exception To The Tax Dependent Rule For Tax Dependents Who Are Not A Child Of The Taxpayer Only Apply To Adult Tax Dependents?

No. This exception also applies to minors claimed as a tax dependent by someone other than their parent. Anytime an individual — regardless of age — is claimed as a tax dependent by someone other than their parents, the non-filer rules apply in determining that individual’s household.

Clarification of the Exception

The exception to the tax dependent rule applies to anyone, regardless of age, who is claimed as a tax dependent by someone other than their parents. In such cases, the non-filer rules are used to determine the individual’s household.

Detailed Explanation

- Non-Parent Tax Filers: If an individual is claimed as a tax dependent by someone other than their parent (e.g., a grandparent, aunt, or legal guardian), the non-filer rules apply.

- Application of Non-Filer Rules: The non-filer rules dictate that the household includes specific individuals based on age and living arrangements.

Example Scenario

-

Minor Claimed by Aunt:

- Scenario: Leena, 5, lives with her aunt, who is her legal guardian. Leena’s aunt claims her as a tax dependent.

- Medicaid Determination: Because Leena is claimed by someone other than her parents, the non-filer rules apply. Leena’s household consists only of herself.

Practical Implications

This exception ensures that Medicaid eligibility is determined appropriately when a child is not living with their parents and is claimed as a dependent by another relative or guardian.

FAQ: Medicaid and Household Income

1. Does Medicaid always look at household income, or are there exceptions?

Medicaid typically considers household income for most eligibility categories, including parents, children, and pregnant women, using MAGI rules. Exceptions exist for the elderly and disabled, who may be evaluated using traditional income and asset tests.

2. How does filing taxes jointly or separately affect Medicaid eligibility?

If you are married and living together, Medicaid considers you part of the same household, regardless of whether you file taxes jointly or separately. If you are not living together, separate filing may lead to separate household determinations.

3. What if I am claimed as a dependent on someone else’s taxes?

If you are claimed as a tax dependent, your Medicaid household is generally the same as the tax filer claiming you, unless you meet certain exceptions, such as being claimed by someone other than a parent.

4. What is MAGI, and how does it simplify Medicaid eligibility?

MAGI (Modified Adjusted Gross Income) is a tax-based method to determine income for Medicaid eligibility, aligning income calculations with federal tax rules and eliminating asset tests for many categories.

5. How do state options affect MAGI implementation?

States have flexibility in extending age limits for full-time students and in how they count pregnant individuals, affecting household size and income thresholds for eligibility.

6. What happens if my income changes during the year?

If your income changes significantly, you should report the change to Medicaid, as it may affect your eligibility. Medicaid will reassess your eligibility based on your current income.

7. Are there resources to help me understand Medicaid eligibility?

Yes, many resources are available, including state Medicaid agencies, healthcare.gov, and community organizations that offer assistance with enrollment and eligibility questions.

8. Can I qualify for Medicaid even if my income is above the limit?

In some cases, you may still qualify for Medicaid through a “spend-down” program, which allows you to deduct medical expenses from your income to meet the eligibility threshold.

9. How does Medicaid determine eligibility for children in non-traditional households?

Medicaid uses specific rules for children living with non-married parents or with guardians to ensure accurate household size and income assessments, often applying non-filer rules.

10. How does income-partners.net help me navigate Medicaid eligibility while seeking partnership opportunities?

Income-partners.net provides resources and opportunities to explore partnerships that can enhance your financial stability, helping you better understand and manage your income in relation to Medicaid eligibility requirements.

Navigating Medicaid eligibility can be complex, but understanding these rules is essential for accessing healthcare coverage. Income-partners.net offers resources to explore partnership opportunities that can improve your financial situation while staying informed about Medicaid requirements.

Ready to explore partnership opportunities and improve your financial outlook? Visit income-partners.net today to discover strategic alliances that can drive your income growth and help you navigate Medicaid eligibility requirements effectively. Let income-partners.net be your guide to financial empowerment through strategic collaboration and informed decision-making.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.