Does Medicaid Go By Household Income? Yes, Medicaid eligibility often considers household income, but the specifics can be complex. Let’s delve into how Medicaid assesses income to determine who qualifies, and how understanding these rules can empower you to explore partnership opportunities and boost your income, as highlighted by income-partners.net.

1. What is MAGI and How Does it Affect Medicaid Eligibility?

Yes, MAGI (Modified Adjusted Gross Income) is a crucial methodology used to determine income eligibility for Medicaid and the Children’s Health Insurance Program (CHIP). MAGI simplifies income assessment by aligning with tax definitions, considering taxable income and certain deductions. It’s important because it standardizes how income is counted, impacting who qualifies for these essential healthcare programs. MAGI rules ensure that assets are not considered, focusing instead on income. It also focuses on tax definitions of income and household, offering a consistent approach for determining eligibility. This shift aimed to streamline the process and expand coverage to more individuals and families, based on their current financial situation rather than complex asset evaluations. For a deeper understanding of income definitions under MAGI, income-partners.net can be a great resource.

2. Who Must Follow MAGI Rules for Medicaid?

Yes, all states must use MAGI rules for specific Medicaid eligibility categories, regardless of Medicaid expansion decisions. MAGI primarily applies to parents, caregiver relatives, children, pregnant women, and the adult expansion group. MAGI rules apply to specific groups, ensuring consistent income assessment for those most in need of healthcare coverage. The elderly, disabled, and children in foster care are not subject to MAGI rules, but are subject to previous income and household determination rules. The implementation of MAGI has significantly altered how states determine Medicaid eligibility for these groups, streamlining the process and expanding access to coverage. It is useful to understand the nuances of these regulations.

3. How Do Medicaid Household Rules Differ From Premium Tax Credit Rules?

Yes, Medicaid and premium tax credit household rules differ significantly, especially in how household size is determined. Medicaid considers family, tax relationships, and living arrangements for each household member. In contrast, premium tax credits rely solely on tax relationships, treating all members of a tax unit as a single household. Because Medicaid determines household size separately for each member, families filing taxes together may have varying household sizes for Medicaid eligibility. This contrasts with premium tax credits, where all tax filers have the same household size. The variability in Medicaid household size determination can impact eligibility thresholds and benefits for different family members. Further, Medicaid offers states options to define households, whereas premium tax credit rules remain consistent nationwide due to their federal nature.

4. How Does Medicaid Determine Who Is In A Household?

Medicaid determines household composition based on an individual’s plan to file taxes, irrespective of actual filing, focusing on whether they intend to be a tax filer, dependent, or neither. It is based on their intended tax filing status, which dictates the applicable household rules. People’s intention determines which Medicaid household rules apply. Medicaid does not mandate prior-year tax filings, prioritizing current circumstances. This forward-looking approach ensures that eligibility aligns with present financial realities, accommodating those with fluctuating income or changing household structures. This approach allows for a more accurate and responsive assessment of eligibility. The details of these rules are available in the Reference Guide: Medicaid Household Rules.

MAGI Rules for Determining Medicaid and CHIP Households

MAGI Rules for Determining Medicaid and CHIP Households

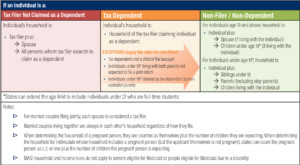

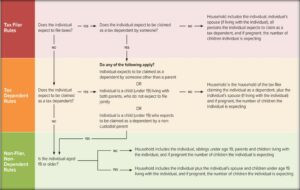

5. What Household Rules Apply To Tax Filers?

For tax filers claiming their own exemption and not claimed as dependents, the household includes the filer, their spouse if filing jointly, and all claimed tax dependents. This definition focuses on the tax filer’s immediate family and dependents, providing a clear framework for household determination. This straightforward rule simplifies the process for many applicants, aligning household composition with tax filing status. The household size directly impacts the income threshold for Medicaid eligibility, making it crucial to understand who counts as a member.

6. What Household Rules Apply to Tax Dependents?

For tax dependents, the household mirrors that of the tax filer claiming them, but there are exceptions. This rule generally aligns a dependent’s household with their provider’s, simplifying eligibility assessment. However, exceptions exist for those under 19 living with parents not filing jointly, or those claimed by non-custodial parents, where non-filer rules apply. These exceptions ensure fair consideration for unique family structures. These exceptions apply when the tax dependent is:

- Individuals who expect to be claimed as a dependent by someone other than a parent;

- Individuals (under 19) living with both parents, whose parents do not expect to file a joint tax return; and

- Individuals (under 19) who expect to be claimed as a dependent by a non-custodial parent.

7. What Household Rules Apply to People Who Don’t File Taxes or Aren’t Claimed as Dependents?

Yes, for individuals not filing taxes or claimed as dependents, household rules vary by age. Those 19 and older include their spouse and children under 19 if living together. For those under 19, the household includes siblings under 19, their children, and parents living with them. The household composition expands for minors to include immediate family, while adults are considered more independent. These rules recognize the differing levels of financial interdependence at different ages. These distinctions ensure appropriate consideration of family support structures for Medicaid eligibility.

8. Are There Adjustments to Household Rules Based on Tax Filing?

Yes, in all cases, married couples living together are always included in each other’s household. Additionally, adjustments are made for pregnant individuals, who are counted as themselves plus the number of expected children. Marriage and pregnancy trigger automatic adjustments to household size, regardless of tax filing status. Counting a pregnant person as multiple household members acknowledges the increased financial needs. These adjustments ensure accurate reflection of household size and needs for Medicaid eligibility.

9. What Options Do States Have for Implementing MAGI Rules?

States can extend the age limit for certain rules to 21 for full-time students. For households with pregnant individuals, states can count them as one, two, or one plus the number of expected children. Extending the age limit to 21 for full-time students acknowledges their continued dependence. Giving states flexibility in counting pregnant individuals allows them to tailor benefits to local needs. These options enable states to customize MAGI implementation to better serve their populations.

10. Are Married Couples Who File Separately Considered Separate Households?

Generally, no, married couples living together are considered part of the same household, regardless of filing status. Cohabitation typically overrides separate filing, emphasizing the economic unity of married couples. However, couples not living together and filing separately are treated as separate households, recognizing their financial independence. These distinctions ensure fair assessment of household income and resources for Medicaid eligibility.

11. How Does Medicaid Determine the Household Size of Family Members When the Parents Live Together but are Not Married?

When unmarried parents live together and file taxes, each parent’s household includes themselves and their tax dependents. Children under 19 living with unmarried parents are considered part of a household that includes both parents and all siblings under 19. The tax filer rule applies to the parents, while the non-filer rule applies to the children. This ensures comprehensive consideration of all family members in the household.

Example: Unmarried Parents

Dan and Jen live together with their two children, Drew and Mary. Because they are not married, Dan and Jen must file separate returns. Jen claims Drew and Mary as tax dependents on her tax return. Dan files as a single person and doesn’t claim any tax dependents. Table 1 illustrates the household size determination for each member of the family. To determine the household size for Dan and Jen, Medicaid would apply the tax filer rule and include everyone in each of their specific tax household. To determine the household size for Drew and Mary, Medicaid would apply the non-filer rule because they are children living with both parents who are not expected to file a joint return.

| Filing Status | Counted in Household | Household Size | Medicaid Rule Applied |

|---|---|---|---|

| Dan | Jen | Drew | Mary |

| Dan | Tax filer | X | 1 |

| Jen | Tax filer | X | X |

| Drew | Tax dependent | X | X |

| Mary | Tax dependent | X | X |

12. How Does Medicaid Determine the Household of an Adult Child Claimed as a Tax Dependent by Their Parents?

Yes, the household of an adult child (19 or older) claimed as a tax dependent by their parents is the same as the parents’ household. The tax dependent rule applies, regardless of the adult child’s age. The child’s household size mirrors the tax filer’s, consolidating the family unit for Medicaid assessment. This approach simplifies eligibility determination, reflecting the financial interdependencies within the family.

Examples of Adult Children

- Barry is 29 and is claimed as a tax dependent by his parents. His parents also claim Barry’s younger brother and sister, who are 15 and 17. When determining his household for Medicaid, Barry has the same household as the tax filer claiming him as a dependent, thus Barry would have a household size of five: himself, both of his parents, and his brother and sister.

- Carla is 28 years and lives with both parents who are married. However, her parents file separate tax returns and Carla’s father claims her as a dependent on his tax return. Even though Carla’s parents file separate returns, married people living together are always in the same household as their spouse. As a result, Carla’s father has a household of three: himself, his spouse, and Carla. This means that Carla also has a household of three.

13. Does the Exception to the Tax Dependent Rule Only Apply to Adult Tax Dependents?

No, the exception to the tax dependent rule applies to both adult and minor tax dependents claimed by someone other than their parents. Anytime an individual is claimed as a tax dependent by someone other than their parents, the non-filer rules apply. This ensures consistent treatment regardless of age, when the dependent is not claimed by their parents. This exception accommodates various caregiving scenarios, aligning household determination with actual living arrangements and dependencies.

Example: Non-Parent Tax Dependent

Leena lives with and is under the guardianship of her aunt. She is five years old and doesn’t have any siblings or parents living with her. Leena’s aunt claims her as a qualifying relative on her tax return. Leena is a tax dependent but she falls under one of the exceptions to the tax dependent rule because she is not the tax dependent of her parents. This means Medicaid will use the non-filer rules to determine her household, and as a result, Leena’s household consists only of herself.

Understanding Medicaid and CHIP: A Pathway to Strategic Partnerships

Navigating the complexities of Medicaid and CHIP eligibility, particularly concerning household income, is vital for families seeking healthcare coverage. The MAGI methodology provides a structured approach, but understanding its nuances can be challenging. This is where strategic partnerships become invaluable. For entrepreneurs, business owners, marketers, investors, product developers, and anyone seeking new business ventures, understanding these dynamics can open doors to innovative solutions and collaborations, and income-partners.net is the place to find them.

How to Determine An Individual’s Medicaid Household

How to Determine An Individual’s Medicaid Household

Unlocking Opportunities Through Strategic Partnerships

The intricacies of Medicaid and CHIP create unique challenges that innovative partnerships can address. Here are several avenues where collaboration can lead to mutual success and increased income:

1. Tailored Financial Solutions for Medicaid Recipients

- Challenge: Medicaid recipients often face financial constraints that limit their access to healthcare services and related resources.

- Partnership Opportunity: Collaborate with financial advisors to provide tailored solutions such as budgeting tools, financial literacy programs, and micro-loan services designed to help Medicaid recipients manage their finances effectively.

- Benefits: Enhances financial stability for Medicaid recipients, reduces financial barriers to healthcare, and establishes a reputation for social responsibility.

2. Innovative Healthcare Delivery Models

- Challenge: Traditional healthcare delivery models may not adequately serve the unique needs of Medicaid populations, leading to inefficiencies and gaps in care.

- Partnership Opportunity: Develop and implement innovative healthcare delivery models such as mobile clinics, telehealth services, and community-based healthcare programs that improve access to care for Medicaid recipients.

- Benefits: Increases healthcare access, improves health outcomes, and reduces healthcare costs through efficient service delivery.

3. Educational Programs on Medicaid Eligibility

- Challenge: Many individuals and families struggle to understand the complex eligibility requirements for Medicaid and CHIP, resulting in missed opportunities for coverage.

- Partnership Opportunity: Partner with community organizations, schools, and healthcare providers to offer educational programs and resources that simplify Medicaid eligibility criteria and application processes.

- Benefits: Empowers individuals to navigate the Medicaid system confidently, increases enrollment rates, and reduces administrative burdens for healthcare providers.

4. Technology Solutions for Healthcare Management

- Challenge: Managing healthcare information and coordinating care for Medicaid recipients can be cumbersome and inefficient, leading to errors and delays.

- Partnership Opportunity: Create technology solutions such as mobile apps, online portals, and data analytics tools that streamline healthcare management, improve communication between providers and patients, and enhance care coordination.

- Benefits: Improves healthcare efficiency, reduces administrative costs, and enhances patient engagement and satisfaction.

5. Employment and Job Training Programs

- Challenge: Many Medicaid recipients face barriers to employment, such as lack of skills, education, or job opportunities, hindering their ability to achieve financial independence.

- Partnership Opportunity: Develop and implement employment and job training programs tailored to the needs of Medicaid recipients, providing skills development, job placement assistance, and ongoing support.

- Benefits: Increases employment rates among Medicaid recipients, reduces reliance on public assistance, and stimulates economic growth.

6. Transportation Assistance Programs

- Challenge: Lack of reliable transportation can prevent Medicaid recipients from accessing essential healthcare services, leading to missed appointments and delayed care.

- Partnership Opportunity: Establish transportation assistance programs that provide free or subsidized transportation to medical appointments, pharmacies, and other healthcare facilities.

- Benefits: Improves healthcare access, reduces missed appointments, and promotes preventive care among Medicaid recipients.

7. Nutrition and Wellness Programs

- Challenge: Poor nutrition and unhealthy lifestyles contribute to chronic health conditions among Medicaid recipients, increasing healthcare costs and reducing quality of life.

- Partnership Opportunity: Offer nutrition and wellness programs that promote healthy eating habits, physical activity, and preventive healthcare practices, such as cooking classes, fitness programs, and health screenings.

- Benefits: Improves health outcomes, reduces chronic disease rates, and lowers healthcare costs through preventive interventions.

8. Mental Health Support Services

- Challenge: Mental health issues are prevalent among Medicaid recipients, yet access to mental health services remains limited, resulting in untreated conditions and adverse outcomes.

- Partnership Opportunity: Expand access to mental health support services, such as counseling, therapy, and psychiatric care, through telehealth platforms, community-based clinics, and integrated healthcare models.

- Benefits: Improves mental health outcomes, reduces hospitalizations and emergency room visits, and enhances overall quality of life for Medicaid recipients.

9. Affordable Housing Initiatives

- Challenge: Housing instability and homelessness can exacerbate health problems among Medicaid recipients, making it difficult to manage chronic conditions and access healthcare services.

- Partnership Opportunity: Collaborate with housing developers, landlords, and social service agencies to create affordable housing options for Medicaid recipients, providing stable living environments and supportive services.

- Benefits: Improves housing stability, reduces homelessness, and enhances health outcomes among Medicaid recipients.

10. Legal Assistance Programs

- Challenge: Medicaid recipients often face legal challenges related to housing, employment, benefits eligibility, and other issues that can impact their health and well-being.

- Partnership Opportunity: Offer legal assistance programs that provide free or low-cost legal services to Medicaid recipients, helping them navigate complex legal systems and protect their rights.

- Benefits: Addresses legal barriers to health and well-being, promotes social justice, and empowers Medicaid recipients to advocate for their needs.

Maximizing Income Through Understanding Medicaid

Entrepreneurs can leverage this knowledge to create solutions that address these challenges, potentially increasing their income while making a positive impact. Income-partners.net serves as a hub for identifying and connecting with partners who share a vision for innovative solutions within the healthcare sector.

Income-Partners.net: Your Gateway to Collaboration and Growth

For entrepreneurs, business owners, marketers, investors, product developers, and anyone seeking new business ventures, understanding these dynamics can open doors to innovative solutions and collaborations. Income-partners.net is your gateway to identifying and connecting with partners who share your vision.

Explore Partnership Opportunities

Discover a wide range of potential partners who are eager to collaborate on projects that address the challenges and opportunities within the Medicaid landscape.

Develop Strategic Alliances

Form strategic alliances with like-minded professionals to create comprehensive solutions that deliver value to Medicaid recipients and stakeholders.

Increase Your Income

By leveraging the power of collaboration, you can tap into new revenue streams and build a sustainable business that makes a positive impact on society.

Call to Action: Connect, Collaborate, and Grow

Ready to take your business to the next level? Visit income-partners.net today to explore partnership opportunities, develop strategic alliances, and unlock new income streams within the Medicaid landscape. Together, we can create innovative solutions that improve healthcare access and outcomes for those who need it most.

Frequently Asked Questions (FAQs) About Medicaid and Household Income

1. How does Medicaid define “household income” for eligibility purposes?

Medicaid uses Modified Adjusted Gross Income (MAGI) to define household income, based on tax definitions of income and household composition.

2. Are assets considered when determining Medicaid eligibility based on household income?

No, under MAGI rules, an individual’s or family’s assets do not count when determining Medicaid eligibility.

3. Does Medicaid look at past income or current income to determine eligibility?

Medicaid focuses on current income and the individual’s plan to file taxes, rather than requiring previous years’ tax returns.

4. What happens if my income changes while I’m enrolled in Medicaid?

You must report income changes to Medicaid, as this may affect your eligibility or the level of benefits you receive.

5. If I am married, does my spouse’s income affect my Medicaid eligibility?

Yes, if you are married and living with your spouse, their income is generally included in your household income, regardless of whether you file taxes jointly or separately.

6. How does Medicaid treat income for self-employed individuals?

For self-employed individuals, Medicaid considers their adjusted gross income (AGI) after deducting business expenses.

7. Are there income deductions that can lower my MAGI for Medicaid eligibility?

Yes, certain deductions, such as student loan interest and contributions to retirement accounts, can lower your MAGI.

8. If I receive child support, is that counted as income for Medicaid eligibility?

In most cases, child support is not counted as income for Medicaid eligibility.

9. How does Medicaid handle unearned income, such as Social Security benefits or unemployment compensation?

Unearned income, like Social Security benefits or unemployment compensation, is generally included in your household income for Medicaid eligibility.

10. Can I still qualify for Medicaid if my income is slightly above the eligibility limit?

Some states offer Medicaid programs with higher income thresholds or allow individuals to “spend down” excess income to qualify.

By understanding these FAQs, you can better navigate Medicaid eligibility requirements and explore opportunities to optimize your financial situation through strategic partnerships with income-partners.net.