Does Ira Withdrawal Count As Income? Yes, traditional IRA withdrawals are generally considered income for tax purposes, which can influence your Social Security benefits and overall financial strategy. Income-partners.net is here to guide you through understanding how IRA distributions affect your income, enabling you to make informed decisions. Let’s explore how to optimize your retirement income and leverage strategic partnerships for financial success. We’ll cover topics like taxable income, adjusted gross income, and retirement planning.

1. Understanding IRA Withdrawals and Social Security: The Basics

Do IRA withdrawals count as income? This is a crucial question for anyone planning their retirement. The answer lies in understanding how different types of IRA distributions are treated by the IRS and how they interact with Social Security benefits. Let’s break down the key aspects to help you navigate this complex topic.

1.1. The Two Main Types of IRAs: Traditional vs. Roth

The first step in understanding how IRA withdrawals affect your income is to differentiate between traditional and Roth IRAs.

-

Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred. However, withdrawals in retirement are taxed as ordinary income.

-

Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free and tax-free growth.

The type of IRA you have significantly impacts how withdrawals are treated for tax purposes and their effect on your Social Security benefits.

1.2. How IRA Distributions Are Generally Taxed

Generally, distributions from a traditional IRA are taxed as ordinary income in the year they are withdrawn. This means the amount you withdraw is added to your other sources of income and taxed at your applicable tax bracket.

In contrast, qualified distributions from a Roth IRA are tax-free, provided certain conditions are met, such as being at least 59 1/2 years old and having the account open for at least five years.

1.3. Social Security Benefits and Income: What You Need to Know

Social Security benefits can be affected by your income in two primary ways:

- The Social Security Earnings Test: If you claim Social Security benefits before reaching your full retirement age (FRA), your benefits may be reduced if your earned income exceeds certain limits.

- Taxation of Social Security Benefits: Depending on your overall income, a portion of your Social Security benefits may be subject to federal income tax.

Understanding these two aspects is crucial in determining how IRA withdrawals might impact your Social Security.

1.4. Earned vs. Unearned Income: A Critical Distinction

When it comes to Social Security, it’s essential to differentiate between earned and unearned income.

- Earned Income: This includes wages, salaries, tips, and net earnings from self-employment.

- Unearned Income: This includes investment income, interest, dividends, capital gains, pensions, annuities, and IRA distributions.

The Social Security earnings test only considers earned income. However, both earned and unearned income can affect the taxation of your Social Security benefits.

1.5. Seeking Expert Guidance

Navigating the complexities of IRA withdrawals and Social Security can be challenging. At income-partners.net, we provide resources and partnerships to help you make informed decisions.

For personalized advice, consider consulting with a qualified financial advisor or tax professional who can assess your unique situation and provide tailored recommendations.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

2. The Social Security Earnings Test: How IRA Withdrawals Are Treated

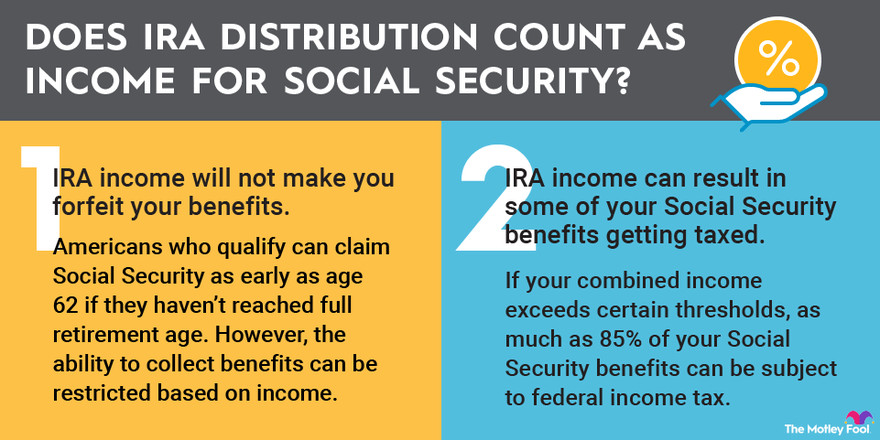

Does IRA withdrawal count as income under the Social Security earnings test? The good news is that IRA withdrawals do not count as earned income for the purposes of the Social Security earnings test. This test only considers income from wages, salaries, and self-employment.

2.1. Understanding the Social Security Earnings Test

The Social Security earnings test applies to individuals who claim Social Security benefits before reaching their full retirement age (FRA). In 2024, if you are under FRA for the entire year, the Social Security Administration (SSA) will deduct $1 from your benefit for every $2 you earn above a certain limit ($22,320 in 2024).

In the year you reach FRA, the SSA deducts $1 from your benefits for every $3 you earn above a different limit ($59,520 in 2024). This threshold applies only to earnings made before the month you reach FRA.

2.2. Why IRA Withdrawals Are Exempt from the Earnings Test

IRA withdrawals are considered unearned income, similar to investment income or pension payments. Since the earnings test only focuses on earned income, your IRA withdrawals will not reduce your Social Security benefits if you are subject to the earnings test.

2.3. Strategic Implications for Early Retirees

This distinction is particularly important for early retirees who are considering taking IRA distributions while also claiming Social Security. Because IRA withdrawals do not count against the earnings test, you can access your retirement savings without affecting your Social Security benefits (although taxes may still apply, as discussed later).

2.4. Examples of Earned vs. Unearned Income

To further clarify, here are some examples of income types that are either subject to or exempt from the Social Security earnings test:

| Income Type | Subject to Earnings Test? |

|---|---|

| Wages from a Job | Yes |

| Self-Employment Income | Yes |

| Traditional IRA Withdrawals | No |

| Roth IRA Withdrawals | No |

| Pension Payments | No |

| Investment Income | No |

2.5. Navigating the Earnings Test with Confidence

Understanding the nuances of the Social Security earnings test can help you make informed decisions about when to claim Social Security and how to manage your retirement income. Income-partners.net offers resources and expert guidance to help you navigate these complexities and optimize your financial strategy.

Understanding the Social Security Earnings Test

Understanding the Social Security Earnings Test

3. Taxation of Social Security Benefits: How IRA Withdrawals Can Impact Your Taxes

While IRA withdrawals don’t affect your eligibility for Social Security benefits under the earnings test, they can impact the taxation of your benefits. So, does IRA withdrawal count as income that affects your taxes? The answer is a conditional yes, depending on the type of IRA.

3.1. Understanding the Taxation of Social Security Benefits

Depending on your overall income, a portion of your Social Security benefits may be subject to federal income tax. The amount of your benefits that is taxable depends on your “combined income,” which is calculated as follows:

Combined Income = Adjusted Gross Income (AGI) + Nontaxable Interest + 1/2 of Social Security Benefits

3.2. How Traditional IRA Withdrawals Affect Your Taxes

Traditional IRA withdrawals are generally included in your Adjusted Gross Income (AGI). This means that taking distributions from a traditional IRA can increase your combined income, potentially leading to a higher percentage of your Social Security benefits being taxed.

3.3. How Roth IRA Withdrawals Affect Your Taxes

In contrast, qualified Roth IRA withdrawals are tax-free and are not included in your AGI. Therefore, taking distributions from a Roth IRA will not increase your combined income and will not affect the taxation of your Social Security benefits.

3.4. Income Thresholds for Taxing Social Security Benefits

The IRS has established income thresholds that determine how much of your Social Security benefits may be taxable:

| Filing Status | Combined Income | Percentage of Social Security Benefits Taxable |

|---|---|---|

| Single, Head of Household | Below $25,000 | 0% |

| $25,000 – $34,000 | Up to 50% | |

| Above $34,000 | Up to 85% | |

| Married Filing Jointly | Below $32,000 | 0% |

| $32,000 – $44,000 | Up to 50% | |

| Above $44,000 | Up to 85% | |

| Married Filing Separately | Any Amount | Up to 85% |

3.5. Strategic Tax Planning with IRA Withdrawals

Understanding how IRA withdrawals affect the taxation of your Social Security benefits can help you develop a strategic tax plan. If you are concerned about minimizing taxes on your Social Security, consider the following:

- Roth Conversions: Converting traditional IRA assets to a Roth IRA can reduce your future taxable income and prevent your Social Security benefits from being taxed.

- Withdrawal Timing: Carefully plan the timing and amount of your IRA withdrawals to stay below the income thresholds for taxing Social Security benefits.

- Tax-Efficient Investments: Consider investing in tax-efficient assets that generate less taxable income.

3.6. Seeking Expert Tax Advice

Tax planning can be complex, and it’s essential to seek professional advice to ensure you are making the most informed decisions. Income-partners.net can connect you with qualified financial advisors and tax professionals who can help you optimize your retirement income strategy.

4. Real-Life Scenarios: How IRA Withdrawals Impact Social Security

To illustrate how IRA withdrawals can affect Social Security, let’s look at a few real-life scenarios. These examples will help clarify the concepts discussed and provide practical insights into managing your retirement income.

4.1. Scenario 1: Early Retirement with Traditional IRA Withdrawals

Situation: John retires at age 62 and begins taking Social Security benefits. He also needs to withdraw $30,000 per year from his traditional IRA to cover his living expenses. His earned income is minimal.

Impact: Because John is claiming Social Security before his full retirement age, he is subject to the earnings test. However, since his IRA withdrawals are not considered earned income, they do not reduce his Social Security benefits.

However, the $30,000 he withdraws from his traditional IRA is included in his AGI, potentially increasing the amount of his Social Security benefits that are subject to tax.

4.2. Scenario 2: Roth IRA Withdrawals in Retirement

Situation: Mary retires at age 65 and takes $40,000 per year from her Roth IRA. She also receives Social Security benefits.

Impact: Because Mary’s Roth IRA withdrawals are qualified and tax-free, they do not increase her AGI or her combined income. As a result, her Roth IRA withdrawals have no impact on the taxation of her Social Security benefits.

4.3. Scenario 3: High-Income Retiree with Traditional IRA and Social Security

Situation: David is a high-income retiree with a significant amount of assets in his traditional IRA. He takes large withdrawals from his IRA each year, resulting in a high AGI. He also receives Social Security benefits.

Impact: Because David’s AGI is high due to his traditional IRA withdrawals, up to 85% of his Social Security benefits may be subject to federal income tax. This significantly reduces the overall value of his Social Security benefits.

4.4. Scenario 4: Roth Conversion Strategy

Situation: Susan is planning for retirement and has a substantial amount in her traditional IRA. To minimize future taxes, she decides to convert a portion of her traditional IRA to a Roth IRA each year.

Impact: By converting to a Roth IRA, Susan increases her taxable income in the year of the conversion. However, future withdrawals from the Roth IRA will be tax-free, and will not affect the taxation of her Social Security benefits. This can result in significant tax savings over the long term.

4.5. Key Takeaways from the Scenarios

These scenarios illustrate the importance of understanding how IRA withdrawals can impact your Social Security benefits. Key takeaways include:

- Traditional IRA withdrawals can increase the taxation of your Social Security benefits.

- Roth IRA withdrawals do not affect the taxation of your Social Security benefits.

- Strategic tax planning, such as Roth conversions, can help minimize taxes in retirement.

4.6. Tailoring Your Retirement Income Strategy

Your retirement income strategy should be tailored to your unique circumstances and financial goals. Income-partners.net provides the resources and expert guidance you need to make informed decisions and optimize your retirement income.

5. Strategic Planning: Maximizing Your Retirement Income

To effectively manage your retirement income and minimize taxes, it’s essential to develop a strategic plan that considers all aspects of your financial situation. Here are some key strategies to consider:

5.1. Roth Conversions: A Powerful Tax Planning Tool

Converting traditional IRA assets to a Roth IRA can be a powerful tax planning tool. While you will owe taxes on the converted amount in the year of the conversion, future withdrawals from the Roth IRA will be tax-free. This can be particularly beneficial if you expect to be in a higher tax bracket in retirement.

5.2. Withdrawal Sequencing: Optimizing Your Income Sources

Carefully plan the order in which you withdraw funds from your various retirement accounts. For example, you may want to withdraw from taxable accounts first, followed by tax-deferred accounts (such as traditional IRAs), and finally from tax-free accounts (such as Roth IRAs). This can help minimize your overall tax liability.

5.3. Tax-Efficient Investing: Minimizing Your Taxable Income

Consider investing in tax-efficient assets that generate less taxable income. Examples include municipal bonds, which are exempt from federal income tax, and certain types of stock funds that generate lower capital gains.

5.4. Managing Your Adjusted Gross Income (AGI)

Be mindful of your AGI, as it can impact a variety of tax-related items, including the taxation of your Social Security benefits, eligibility for certain tax deductions and credits, and Medicare premiums. Strategies to manage your AGI include:

- Timing your IRA withdrawals to avoid exceeding income thresholds.

- Maximizing deductions and credits to reduce your taxable income.

- Considering tax-loss harvesting to offset capital gains.

5.5. Working with a Financial Advisor

A qualified financial advisor can help you develop a comprehensive retirement income plan that takes into account your unique circumstances and financial goals. They can provide personalized advice on topics such as:

- IRA withdrawal strategies

- Roth conversions

- Tax planning

- Investment management

5.6. Leveraging Resources from Income-Partners.Net

Income-partners.net offers a wealth of resources to help you plan for retirement and manage your income effectively. Explore our articles, guides, and tools to learn more about:

- Retirement planning strategies

- Tax planning tips

- Investment management

- Finding the right financial advisor

6. Common Mistakes to Avoid with IRA Withdrawals and Social Security

Planning for retirement and managing IRA withdrawals can be complex, and it’s easy to make mistakes that can negatively impact your financial situation. Here are some common mistakes to avoid:

6.1. Not Understanding the Tax Implications of IRA Withdrawals

One of the biggest mistakes is not fully understanding the tax implications of IRA withdrawals. Failing to account for taxes can lead to unpleasant surprises and reduce your overall retirement income.

6.2. Withdrawing Too Much Too Soon

Withdrawing too much from your IRA early in retirement can deplete your savings and leave you with insufficient funds later in life. Develop a sustainable withdrawal strategy that balances your current needs with your long-term financial security.

6.3. Ignoring the Impact on Social Security Benefits

Failing to consider how IRA withdrawals can impact the taxation of your Social Security benefits can result in higher taxes and reduced overall income. Plan your withdrawals carefully to minimize the impact on your Social Security.

6.4. Not Taking Required Minimum Distributions (RMDs)

Once you reach age 73 (or 75, depending on your birth year), you are required to take minimum distributions from your traditional IRA. Failing to take RMDs can result in significant penalties.

6.5. Not Diversifying Your Retirement Savings

Putting all your eggs in one basket can be risky. Diversify your retirement savings across a variety of asset classes to reduce risk and improve your long-term returns.

6.6. Not Reviewing Your Retirement Plan Regularly

Your retirement plan should be a living document that is reviewed and updated regularly to reflect changes in your circumstances, financial goals, and the economic environment.

6.7. Not Seeking Professional Advice

Going it alone can be challenging. Don’t hesitate to seek professional advice from a qualified financial advisor or tax professional who can help you navigate the complexities of retirement planning.

6.8. Partnering with Income-Partners.Net for Success

Income-partners.net is committed to providing you with the resources and support you need to avoid these common mistakes and achieve your retirement goals. Explore our website to learn more about:

- Retirement planning

- Tax planning

- Investment management

- Finding a financial advisor

7. The Future of Retirement Planning: Trends and Opportunities

As the world evolves, so too does the landscape of retirement planning. Staying informed about emerging trends and opportunities can help you maximize your retirement income and achieve your financial goals.

7.1. The Rise of the Gig Economy

More and more people are participating in the gig economy, working as freelancers, consultants, or independent contractors. This can provide additional income in retirement, but it also requires careful planning to manage taxes and Social Security benefits.

7.2. The Growing Importance of Healthcare Planning

Healthcare costs are a major concern for retirees. Planning for healthcare expenses is essential to ensure you have sufficient funds to cover your medical needs.

7.3. The Impact of Technology on Retirement Planning

Technology is transforming the way we plan for retirement. Online tools, robo-advisors, and financial planning apps can help you manage your finances and make informed decisions.

7.4. The Increasing Focus on Socially Responsible Investing

More and more investors are interested in socially responsible investing (SRI), which involves investing in companies that align with your values and have a positive impact on society.

7.5. The Need for Lifelong Learning

Staying engaged and learning new skills can help you remain active and productive in retirement. Consider pursuing hobbies, taking courses, or volunteering in your community.

7.6. Embracing Innovation with Income-Partners.Net

Income-partners.net is at the forefront of innovation in retirement planning. We are constantly exploring new trends and opportunities to help you maximize your retirement income and achieve your financial goals. Visit our website to learn more about:

- Emerging retirement planning strategies

- Innovative investment solutions

- The future of retirement

8. Frequently Asked Questions (FAQ) About IRA Withdrawals and Income

Here are some frequently asked questions about IRA withdrawals and their impact on your income and Social Security benefits:

8.1. Do IRA withdrawals count as income for Social Security purposes?

Traditional IRA withdrawals are generally considered taxable income, which can affect the taxation of your Social Security benefits. However, they do not count as earned income for the Social Security earnings test. Roth IRA withdrawals are generally tax-free and do not affect your Social Security benefits.

8.2. Will taking IRA withdrawals reduce my Social Security benefits?

Taking traditional IRA withdrawals will not directly reduce your Social Security benefits. However, they can increase your adjusted gross income (AGI), which can lead to a higher percentage of your Social Security benefits being taxed.

8.3. How are Roth IRA withdrawals treated for Social Security purposes?

Qualified Roth IRA withdrawals are tax-free and are not included in your adjusted gross income (AGI). Therefore, they have no impact on the taxation of your Social Security benefits.

8.4. What is the Social Security earnings test, and how does it affect IRA withdrawals?

The Social Security earnings test applies to individuals who claim Social Security benefits before reaching their full retirement age (FRA). This test only considers earned income, such as wages and salaries. IRA withdrawals are considered unearned income and do not reduce your Social Security benefits under the earnings test.

8.5. Can I avoid taxes on my IRA withdrawals?

You can avoid taxes on your IRA withdrawals by taking qualified distributions from a Roth IRA. Alternatively, you can convert traditional IRA assets to a Roth IRA, although you will owe taxes on the converted amount in the year of the conversion.

8.6. How do I calculate the amount of my Social Security benefits that may be taxable?

The amount of your Social Security benefits that may be taxable depends on your combined income, which is calculated as follows:

Combined Income = Adjusted Gross Income (AGI) + Nontaxable Interest + 1/2 of Social Security Benefits

8.7. What are required minimum distributions (RMDs), and how do they affect my taxes?

Required minimum distributions (RMDs) are mandatory withdrawals that you must take from your traditional IRA once you reach age 73 (or 75, depending on your birth year). These withdrawals are taxed as ordinary income and can increase your AGI, potentially affecting the taxation of your Social Security benefits.

8.8. How can Income-Partners.Net help me plan for retirement and manage my IRA withdrawals?

Income-partners.net offers a wealth of resources to help you plan for retirement and manage your IRA withdrawals effectively. Explore our articles, guides, and tools to learn more about retirement planning strategies, tax planning tips, investment management, and finding a financial advisor.

8.9. Where can I find a financial advisor to help me with my retirement planning?

Income-partners.net can connect you with qualified financial advisors who can help you develop a comprehensive retirement plan that takes into account your unique circumstances and financial goals.

8.10. What are some additional resources for learning more about retirement planning and Social Security benefits?

Here are some additional resources for learning more about retirement planning and Social Security benefits:

- Social Security Administration (SSA): ssa.gov

- Internal Revenue Service (IRS): irs.gov

- Financial Industry Regulatory Authority (FINRA): finra.org

9. Partnering for Prosperity: The Income-Partners.Net Advantage

At income-partners.net, our mission is to empower you with the knowledge, resources, and partnerships you need to achieve financial success in retirement. We believe that strategic partnerships are essential for building wealth and maximizing your income.

9.1. Discovering Partnership Opportunities

We offer a platform where you can discover and connect with potential partners who share your vision and goals. Whether you’re looking for investment opportunities, business collaborations, or joint ventures, income-partners.net can help you find the right fit.

9.2. Building Strong Relationships

We provide resources and guidance to help you build strong, mutually beneficial relationships with your partners. Effective communication, trust, and shared values are essential for long-term success.

9.3. Maximizing Your Income Potential

By partnering with others, you can leverage their expertise, resources, and networks to maximize your income potential. Whether you’re looking to generate passive income, start a new business, or expand your existing operations, strategic partnerships can help you achieve your goals.

9.4. Accessing Expert Guidance

We connect you with qualified financial advisors, tax professionals, and legal experts who can provide personalized advice and support. Our network of experts can help you navigate the complexities of retirement planning, investment management, and tax optimization.

9.5. Joining a Community of Like-Minded Individuals

When you join income-partners.net, you become part of a community of like-minded individuals who are passionate about financial success. Share ideas, exchange insights, and collaborate with others to achieve your goals.

9.6. Taking the Next Step Towards Financial Freedom

Are you ready to take control of your financial future and unlock the power of strategic partnerships? Visit income-partners.net today to:

- Explore partnership opportunities

- Access expert resources

- Connect with like-minded individuals

- Start building your path to prosperity

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net