Does Income Tax Vary By State? Absolutely, and this variation significantly impacts your financial strategies and potential partnership opportunities. At income-partners.net, we help you navigate these differences to identify the most advantageous locations and collaborations for boosting your income.

Understanding state income tax laws is crucial for making informed financial and business decisions. Let’s delve into the intricacies of how income tax varies across states, offering insights and strategies to help you maximize your financial potential and discover partnership opportunities.

1. What is State Income Tax and How Does It Work?

State income tax is a levy imposed by individual U.S. states on the income earned by residents or those who work within the state. It functions similarly to federal income tax but is determined and collected at the state level.

State income tax is a key revenue source for state governments, funding essential public services like education, infrastructure, and healthcare. Understanding its mechanics helps individuals and businesses optimize their financial strategies. Here’s a detailed look at how it works:

-

Taxable Income Calculation:

- Gross Income: This includes all income sources such as wages, salaries, tips, business profits, investment income, and retirement distributions.

- Adjustments: Certain deductions, like contributions to retirement accounts, student loan interest, and health savings account (HSA) contributions, are subtracted from gross income to arrive at adjusted gross income (AGI).

- Deductions: Taxpayers can choose between a standard deduction (a fixed amount based on filing status) or itemized deductions (like mortgage interest, state and local taxes up to $10,000, and charitable donations). The higher amount reduces taxable income further.

- Exemptions: Personal exemptions are subtracted for each taxpayer, their spouse, and dependents. However, the federal personal exemption is currently set at $0 through 2025 due to the Tax Cuts and Jobs Act (TCJA).

- Taxable Income: The result after subtracting deductions and exemptions from AGI is the income subject to state income tax.

-

Tax Rates and Brackets:

- Tax Rate: This is the percentage at which income is taxed.

- Tax Brackets: Many states use a graduated tax system with different rates for various income ranges or brackets. Income within each bracket is taxed at that bracket’s rate.

- Marginal Tax Rate: This is the rate applied to the last dollar of income earned. It’s crucial for understanding the tax impact of additional earnings.

-

Tax Credits:

- Tax Credits: These directly reduce the amount of tax owed.

- Types: Common credits include those for child and dependent care, education expenses, energy-efficient home improvements, and low-income earners.

- Refundable vs. Non-Refundable: Refundable credits can result in a refund even if the tax liability is reduced to zero, while non-refundable credits are limited to the amount of tax owed.

-

Filing and Payment:

- Filing Requirements: Most states require residents who meet certain income thresholds to file an income tax return annually.

- Tax Forms: State tax forms mirror federal forms but are specific to each state’s tax laws.

- Due Date: Generally, state income tax returns are due on the same day as federal returns, typically April 15th, unless an extension is filed.

- Payment Methods: States offer various payment options, including online payments, mail-in checks, and electronic funds transfers.

-

State Conformity to Federal Tax Law:

- Starting Point: Many states use the federal tax code as the starting point for calculating state taxable income.

- Conformity: States decide how closely to conform to federal tax laws, which can simplify tax preparation but also mean that federal changes automatically affect state taxes unless the state legislature acts.

- Decoupling: States can decouple from specific federal provisions to maintain control over their tax policies.

-

Types of State Income Tax Systems:

- Graduated Income Tax: This system features multiple tax brackets with increasing rates for higher income levels.

- Flat Income Tax: A single tax rate applies to all taxable income, regardless of the amount.

- No Income Tax: Some states do not levy a state income tax, relying instead on other revenue sources like sales taxes, property taxes, and excise taxes.

Navigating state income tax requires understanding these components and staying updated on legislative changes. By doing so, individuals and businesses can make informed decisions to optimize their tax liabilities and financial planning.

2. Which States Have No Income Tax?

Currently, nine states have no state income tax, offering potential financial advantages for residents and businesses.

Nine states currently do not impose a state income tax on their residents, which can be a significant draw for individuals and businesses seeking to minimize their tax burden. These states rely on alternative revenue sources such as sales tax, property tax, and excise taxes to fund state services. Here’s an overview of these states:

-

Alaska:

- No Income Tax: Alaska has no state income tax or sales tax.

- Revenue Source: The state relies heavily on revenue from oil production.

- Additional Benefit: Residents receive an annual dividend from the Permanent Fund, which invests in the state’s oil revenues.

-

Florida:

- No Income Tax: Florida does not have a state income tax.

- Revenue Source: The state depends on tourism, sales tax, and property tax revenues.

- Economic Impact: The absence of income tax can attract retirees and businesses, boosting the economy.

-

Nevada:

- No Income Tax: Nevada has no state income tax.

- Revenue Source: The state relies on tourism, gaming, and sales tax.

- Business-Friendly Environment: Nevada is known for its business-friendly tax environment, attracting many companies.

-

New Hampshire:

- Limited Income Tax: New Hampshire only taxes interest and dividend income at a rate of 3 percent in 2024, phasing out completely in 2025.

- Revenue Source: The state depends on property taxes and local taxes.

- “Live Free or Die” State: The state motto reflects its commitment to low taxes and minimal government intervention.

-

South Dakota:

- No Income Tax: South Dakota has no state income tax.

- Revenue Source: The state relies on sales tax and property tax revenues.

- Economic Development: The absence of income tax is a tool for attracting new residents and businesses.

-

Tennessee:

- No Income Tax: Tennessee has no state income tax.

- Revenue Source: The state relies on sales tax and excise taxes.

- Economic Growth: Tennessee has seen significant economic growth in recent years, partly due to its favorable tax climate.

-

Texas:

- No Income Tax: Texas has no state income tax.

- Revenue Source: The state depends on sales tax and property tax revenues.

- Business Hub: Texas is a major business hub, with many companies attracted by its low-tax environment.

-

Washington:

- No Income Tax: Washington has no state income tax but does impose a 7 percent tax on capital gains income above $250,000.

- Revenue Source: The state relies on sales tax and excise taxes.

- Tech Industry: Washington is home to major tech companies like Amazon and Microsoft.

-

Wyoming:

- No Income Tax: Wyoming has no state income tax.

- Revenue Source: The state relies on mineral extraction and property tax revenues.

- Low Tax Burden: Wyoming is known for its low overall tax burden, making it attractive to residents and businesses.

These states offer unique economic environments and opportunities. The absence of state income tax can lead to increased disposable income for residents and reduced operating costs for businesses, making them attractive destinations for relocation and investment.

Office and Living Arrangement Opportunities

Office and Living Arrangement Opportunities

3. Which States Have Flat Income Tax?

Twelve states employ a flat income tax system, where a single tax rate applies to all taxable income, simplifying tax calculations.

Twelve states currently feature a flat income tax system, where a single tax rate is applied to all taxable income regardless of the income level. This approach simplifies tax calculations and offers predictability for taxpayers. Here’s an overview of these states:

-

Arizona:

- Flat Tax Rate: 2.5 percent.

- Simplicity: Arizona’s flat tax rate streamlines tax calculations for all residents.

- Economic Impact: This rate aims to attract businesses and residents, fostering economic growth.

-

Colorado:

- Flat Tax Rate: 4.40 percent.

- Business Climate: Colorado’s flat tax supports a stable and predictable business environment.

- привлекательность: The tax structure is designed to attract a skilled workforce and growing industries.

-

Georgia:

- Flat Tax Rate: 5.49 percent.

- Recent Transition: Georgia transitioned to a flat tax in 2024, simplifying its tax system.

- Personal Exemption: The state also increased its personal exemption, providing additional tax relief.

-

Idaho:

- Flat Tax Rate: 5.8 percent on income above $4,489.

- Tax Relief: Idaho’s flat tax provides consistent tax rates across income levels.

-

Illinois:

- Flat Tax Rate: 4.95 percent.

- Constitutional Requirement: Illinois’s constitution mandates a flat income tax.

- Budget Stability: The flat tax provides a consistent revenue stream for state services.

-

Indiana:

- Flat Tax Rate: 3.05 percent (scheduled to decrease further in coming years).

- Tax Reduction: Indiana has been gradually reducing its income tax rate, enhancing its appeal.

- Economic Growth: The lower tax rate is intended to spur economic growth and investment.

-

Kentucky:

- Flat Tax Rate: 4.00 percent.

- Recent Reduction: Kentucky reduced its flat tax rate in 2024, making it more competitive.

- Fiscal Responsibility: The tax cut is part of broader fiscal reforms in the state.

-

Michigan:

- Flat Tax Rate: 4.25 percent.

- Economic Competitiveness: Michigan’s flat tax helps maintain a competitive business environment.

- Workforce: The stable tax climate attracts and retains a skilled workforce.

-

Mississippi:

- Flat Tax Rate: 4.7 percent on income above $10,000.

- Gradual Reduction: Mississippi is in the process of gradually reducing its income tax rate.

-

North Carolina:

- Flat Tax Rate: 4.5 percent (scheduled to decrease further in coming years).

- Long-Term Goal: North Carolina aims to further reduce its flat tax rate in the coming years.

- Economic Development: The tax policy supports long-term economic development.

-

Pennsylvania:

- Flat Tax Rate: 3.07 percent.

- Simplicity: Pennsylvania’s flat tax offers a straightforward tax system for residents.

-

Utah:

- Flat Tax Rate: 4.65 percent.

- Economic Stability: Utah’s flat tax supports economic stability and predictability.

These states offer a straightforward approach to taxation, which can be appealing to both individuals and businesses. The simplicity of a flat tax system reduces compliance costs and makes financial planning more predictable.

4. What Are Graduated Income Tax Systems?

Twenty-nine states and the District of Columbia use graduated income tax systems, with varying tax rates based on income levels.

A graduated income tax system, used by 29 states and the District of Columbia, involves multiple tax brackets with increasing rates for higher income levels. This progressive approach is designed to distribute the tax burden more equitably. Here’s a detailed overview of how these systems work and their implications:

-

How Graduated Income Tax Systems Work:

- Tax Brackets: Income is divided into multiple brackets, each taxed at a different rate. For example, the first $10,000 might be taxed at 2 percent, the next $20,000 at 4 percent, and so on.

- Progressive Taxation: Higher earners pay a larger percentage of their income in taxes compared to lower earners.

- Marginal Tax Rate: The tax rate applied to the last dollar of income earned is known as the marginal tax rate.

-

Key Features and Components:

- Number of Brackets: States vary widely in the number of tax brackets, ranging from just a few to over a dozen.

- Bracket Widths: The income range within each bracket also varies significantly. Some states have narrow brackets clustered at lower income levels, while others have wider brackets at higher income levels.

- Income Thresholds: The income levels at which tax rates change are crucial in determining the overall tax burden.

- Inflation Adjustment: Some states adjust their tax brackets annually to account for inflation, preventing bracket creep (where inflation pushes taxpayers into higher brackets even without real income gains).

-

Examples of States with Graduated Income Tax Systems:

- California: Known for having one of the most progressive tax systems with multiple brackets and high top marginal rates.

- New York: Features a multi-bracket system with varying rates based on income level.

- Massachusetts: Implements a surtax on high earners, resulting in a two-tiered system.

- Oregon: Has multiple tax brackets and also includes a high-income surtax.

- Hawaii: Features as many as 12 brackets.

-

Advantages of Graduated Income Tax Systems:

- Fairness: These systems are generally considered fairer because they distribute the tax burden based on the ability to pay.

- Revenue Generation: Graduated systems can generate more revenue for state governments, especially when top marginal rates are high.

- Social Equity: The progressive nature can help reduce income inequality by redistributing wealth.

-

Disadvantages of Graduated Income Tax Systems:

- Complexity: These systems can be more complex to understand and administer, leading to higher compliance costs.

- Disincentives: High marginal tax rates can discourage high earners from working, investing, or starting businesses in the state.

- Tax Avoidance: High-income earners may seek ways to reduce their tax liability through tax planning, deductions, and credits.

-

Economic Impact:

- Income Distribution: Progressive tax systems can lead to a more equitable distribution of income.

- Economic Growth: The impact on economic growth is debated. Some argue that high taxes can hinder growth, while others contend that adequate public services funded by these taxes can support growth.

- Business Location: States with high tax rates may struggle to attract and retain businesses, impacting job creation and investment.

-

Considerations for Businesses and Individuals:

- Tax Planning: Understanding the marginal tax rates and brackets is essential for effective tax planning.

- Location Decisions: The tax climate can influence decisions about where to live and conduct business.

- Investment Strategies: High-income earners may need to adjust their investment strategies to minimize tax liabilities.

Graduated income tax systems are a key component of state fiscal policy, balancing revenue generation with considerations of fairness and economic impact. By understanding the nuances of these systems, individuals and businesses can make informed financial decisions.

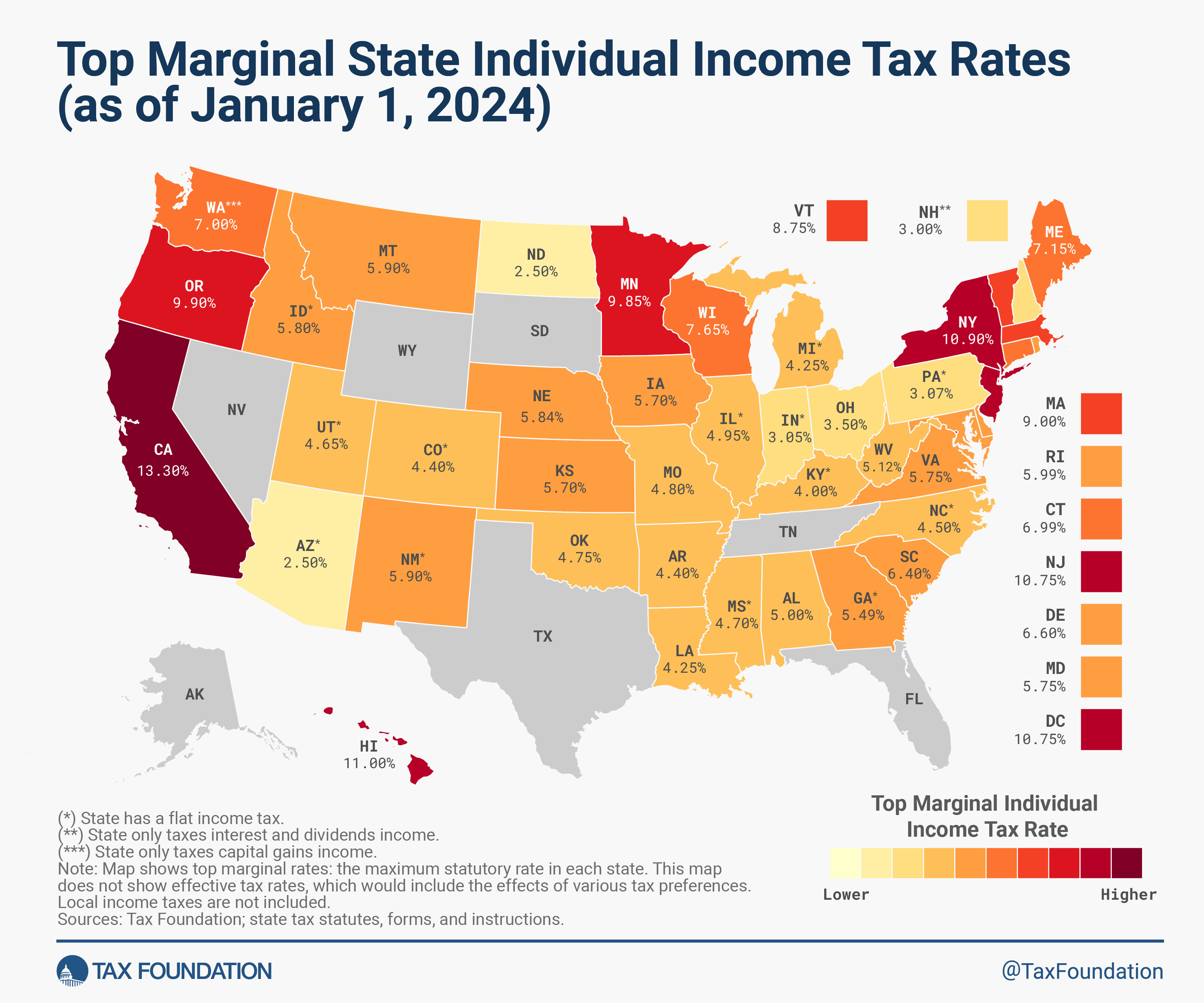

5. How Do State Income Tax Rates and Brackets Vary?

State income tax rates and brackets vary significantly. Top marginal rates range from 2.5 percent in Arizona and North Dakota to 13.3 percent in California.

The structure of state individual income taxes varies considerably across the United States, with significant differences in tax rates, income brackets, and other provisions. These variations can have a substantial impact on individuals’ tax liabilities and financial planning. Here’s a comprehensive overview of how state income tax rates and brackets differ:

-

Range of Top Marginal Tax Rates:

- Lowest Rates: Some states have very low top marginal rates. For example, Arizona and North Dakota have rates as low as 2.5 percent.

- Highest Rates: On the other end, states like California have top marginal rates as high as 13.3 percent (plus an additional payroll tax of 1.1 percent on wage income, bringing the all-in top rate to 14.4 percent as of 2024).

-

Number of Tax Brackets:

- Few Brackets: Some states have a simplified structure with only a few tax brackets. For example, Montana has just two brackets.

- Many Brackets: Other states have a more complex system with numerous brackets. Hawaii, for instance, has 12 brackets.

-

Income Thresholds for Top Rates:

- Low Thresholds: In some states, the top tax rate kicks in at relatively low income levels. Virginia, for example, applies its top rate to taxable income above $17,000.

- High Thresholds: In contrast, states like California, Massachusetts, New Jersey, New York, and the District of Columbia apply their top rates to income above $1 million.

-

Indexing for Inflation:

- Indexed Brackets: Some states adjust their tax brackets annually to account for inflation, preventing bracket creep.

- Non-Indexed Brackets: Other states do not adjust their brackets, meaning that taxpayers can move into higher tax brackets even if their real income has not increased.

-

Standard Deductions and Personal Exemptions:

- Varying Amounts: The amount of standard deductions and personal exemptions varies widely by state. Some states tie these to the federal tax code, while others set their own amounts.

- Federal Conformity: Many states use the federal tax code as a starting point for calculating their standard deductions and personal exemptions.

-

Tax Benefit Recapture:

- High-Income Taxpayers: Some states like Connecticut and New York have a “tax benefit recapture” mechanism, where high-income taxpayers end up paying their top tax rate on all income, not just the portion above the benefit threshold.

-

Impact of State Policies:

- Marriage Penalty: Some states double their single-filer bracket widths for married filers to avoid imposing a “marriage penalty,” where married couples pay more in taxes than they would if they were both single.

- Tax Credits: States offer various tax credits for things like child care, education, and energy efficiency, which can significantly reduce tax liabilities.

-

Recent Tax Changes:

- Rate Reductions: Many states have been reducing their income tax rates in recent years. From 2021 to 2023, 26 states enacted individual income tax rate reductions.

- Flat Tax Transitions: Some states are transitioning to flat tax systems. For example, Georgia transitioned to a flat tax in 2024.

-

Regional Variations:

- Southern States: Tend to have lower income tax rates and simpler tax structures.

- Northeastern States: Often have higher tax rates and more complex tax systems.

- Western States: Exhibit a mix of tax policies, with some states having high rates and others having no income tax.

-

Examples of Specific State Income Tax Structures:

- Arkansas: Reduced its top individual income tax rate from 4.7 percent to 4.4 percent in 2024.

- Connecticut: Reduced individual income tax rates for the two lowest brackets in 2024.

- Iowa: Consolidated its four individual income tax brackets into three and is transitioning to a flat income tax system.

- Mississippi: Is gradually reducing its flat individual income tax rate from 2024 to 2026.

- Nebraska: Reduced its top individual income tax rate from 6.64 percent in 2023 to 5.84 percent in 2024 and plans further reductions.

- North Carolina: Reduced its flat individual income tax rate from 4.75 percent to 4.5 percent in 2024 and plans further reductions.

- Ohio: Reduced the number of individual income tax brackets from three to two and lowered the top rate.

- South Carolina: Reduced its top individual income tax rate from 6.5 percent to 6.4 percent in 2024 and plans further reductions subject to revenue triggers.

- Montana: Simplified the individual income tax system and reduced the number of tax brackets from seven to two in 2024.

The wide variations in state income tax rates and brackets highlight the importance of understanding these differences for effective financial planning and location decisions.

6. How Do Standard Deductions and Exemptions Vary by State?

Standard deductions and exemptions vary significantly by state, affecting taxable income and overall tax liability.

The amounts and availability of standard deductions and exemptions vary significantly from state to state, greatly impacting an individual’s taxable income and overall tax liability. These deductions and exemptions are essential components of state income tax systems, providing tax relief and simplifying the tax filing process. Here’s a detailed overview:

-

Standard Deductions:

-

Definition: A standard deduction is a fixed dollar amount that reduces the income subject to tax. Taxpayers can choose to take the standard deduction or itemize deductions, selecting whichever results in a lower tax liability.

-

Variation: The amount of the standard deduction varies widely by state and filing status (single, married filing jointly, etc.).

-

Federal Conformity: Some states use the federal standard deduction amounts, while others set their own.

-

Examples:

- Arizona: $14,600 for single filers and $29,200 for married couples filing jointly, conforming to the federal standard deduction.

- Georgia: $12,000 for single taxpayers and $24,000 for married couples filing jointly.

- New Mexico: $14,600 for single filers and $29,200 for married couples filing jointly, conforming to the federal standard deduction.

-

-

Personal Exemptions:

-

Definition: A personal exemption is a specific dollar amount that taxpayers can subtract for themselves, their spouse, and their dependents.

-

Federal Changes: The federal personal exemption is currently set at $0 through 2025 due to the Tax Cuts and Jobs Act (TCJA).

-

State Approaches: Some states still provide state-defined personal exemptions, even though the federal exemption is $0. Others have eliminated or reduced their personal exemptions.

-

Examples:

- Delaware: $3,250 for single filers and $6,500 for married couples filing jointly.

- Hawaii: $2,200 for single filers and $4,400 for married couples filing jointly, plus additional exemptions for dependents.

- New York: $8,000 for single filers and $16,050 for married couples filing jointly.

-

-

Dependent Exemptions and Credits:

-

Exemptions: Some states offer additional exemptions for dependents, reducing taxable income further.

-

Credits: Other states provide tax credits for dependents, which directly reduce the amount of tax owed.

-

Examples:

- Arizona: Offers a dependent tax credit of $100 per dependent under the age of 17 and $25 per dependent age 17 and older.

- New Mexico: Provides a deduction of $4,000 for all but one of a taxpayer’s dependents.

- Ohio: Offers a dependent exemption of $2,500 for children under the age of 18.

-

-

Indexing for Inflation:

- Adjustments: Some states adjust their standard deductions and personal exemptions annually to account for inflation.

- Impact: Indexing helps prevent bracket creep and ensures that tax relief keeps pace with rising costs of living.

-

Phase-Out Provisions:

-

Income Limits: Some states phase out or reduce the amount of standard deductions and personal exemptions for high-income earners.

-

Examples:

- Maine: Personal exemption begins to phase out for taxpayers with income exceeding $305,150 (single filers) or $366,100 (MFJ). The standard deduction also phases out for taxpayers with Maine income over $97,150 (single filers) or $194,300 (MFJ).

- Maryland: The exemption amount phases out for single filers with AGI above $100,000 and married filers with AGI above $150,000.

-

-

Combined Standard Deductions and Personal Exemptions:

- Simplification: Some states combine standard deductions and personal exemptions into a single deduction amount.

- Example:

- Louisiana: Combines standard deductions and personal exemptions into a single amount: $4,500 for single filers and married filing separately, and $9,000 for MFJ and head of household.

-

State-Specific Deductions:

-

Unique Provisions: Some states offer unique deductions or credits tailored to specific circumstances or industries.

-

Examples:

- Arizona: Standard deduction can be adjusted upward by an amount equal to 31 percent of the amount the taxpayer would have claimed in charitable deductions if the taxpayer had claimed itemized deductions.

-

-

Impact on Tax Planning:

- Taxable Income Reduction: Understanding the available standard deductions and exemptions is crucial for reducing taxable income and minimizing tax liabilities.

- Location Decisions: Differences in these provisions can influence decisions about where to live and conduct business.

- Financial Planning: Taxpayers should consider these factors when making financial plans and investment decisions.

The variations in standard deductions and exemptions across states highlight the importance of understanding these differences for effective tax planning and financial decision-making.

7. What Are Tax Credits and How Do They Differ by State?

Tax credits directly reduce tax liability and vary significantly by state, offering targeted incentives for specific activities.

Tax credits are powerful tools that directly reduce the amount of tax owed, offering targeted incentives for specific activities and benefiting various groups. These credits differ significantly by state, reflecting diverse policy priorities and economic goals. Here’s an in-depth look at how tax credits work and how they vary across states:

-

How Tax Credits Work:

- Direct Reduction: Tax credits directly reduce the amount of tax a taxpayer owes, unlike deductions, which reduce taxable income.

- Dollar-for-Dollar: A $1,000 tax credit reduces the tax liability by $1,000.

- Refundable vs. Non-Refundable:

- Refundable Credits: Can reduce the tax liability to below zero, resulting in a refund to the taxpayer.

- Non-Refundable Credits: Can only reduce the tax liability to zero; any remaining credit amount is lost.

-

Common Types of State Tax Credits:

- Earned Income Tax Credit (EITC): Provides tax relief to low- to moderate-income working individuals and families. Many states offer a state-level EITC that supplements the federal EITC.

- Child and Dependent Care Credit: Helps offset the costs of child care and care for other dependents, allowing taxpayers to work or look for work.

- Education Credits: Support educational expenses, such as tuition, fees, and books. These credits can be for higher education, vocational training, or even K-12 expenses.

- Energy Credits: Incentivize investments in renewable energy and energy efficiency, such as solar panels, energy-efficient appliances, and home improvements.

- Credits for Charitable Contributions: Encourage donations to charitable organizations.

- Credits for Specific Industries: Support industries important to the state’s economy, such as agriculture, film production, and technology.

- Credits for Historic Preservation: Encourage the preservation and rehabilitation of historic buildings and sites.

-

Examples of State Tax Credits and Their Variations:

- Earned Income Tax Credit (EITC):

- California: Offers a state EITC that supplements the federal EITC, providing additional tax relief to low-income workers.

- Maryland: Has a refundable EITC, providing additional support to eligible taxpayers.

- Child and Dependent Care Credit:

- Iowa: Offers a child and dependent care credit, structured as a tax credit.

- Education Credits:

- Rhode Island: Features personal tax credits based upon adjusted gross income.

- Energy Credits:

- Many States: Offer credits for installing solar panels or making energy-efficient home improvements.

- Earned Income Tax Credit (EITC):

-

Targeted Tax Credits:

- Specific Groups: Some states offer tax credits targeted at specific groups, such as veterans, seniors, or individuals with disabilities.

- Economic Activities: Other credits are designed to encourage specific economic activities, such as job creation, research and development, or investment in underserved areas.

-

Impact of Tax Credits on State Budgets:

- Revenue Reduction: Tax credits reduce state tax revenues, impacting the state budget.

- Economic Stimulus: Credits can stimulate economic activity and provide support to targeted groups.

- Cost-Benefit Analysis: States must carefully evaluate the costs and benefits of tax credits to ensure they are achieving their intended goals.

-

Considerations for Taxpayers:

- Eligibility: Taxpayers must meet specific eligibility requirements to claim tax credits.

- Documentation: Proper documentation is required to substantiate claims for tax credits.

- Planning: Taxpayers should plan ahead to take advantage of available tax credits and maximize their tax savings.

-

Examples of Unique State Tax Credits:

- Arizona: Offers a dependent tax credit of $100 per dependent under the age of 17 and $25 per dependent age 17 and older.

- Oregon: The personal exemption credit is not allowed if federal AGI exceeds $100,000 for single filers or $200,000 for MFJ.

Tax credits are a vital tool for state governments to achieve specific policy objectives and provide targeted tax relief. By understanding the available tax credits and their eligibility requirements, taxpayers can optimize their tax planning and reduce their overall tax burden.

8. How Do Local Income Taxes Fit In?

Eleven states allow county- or city-level income taxes, adding another layer of complexity to the overall tax landscape.

Local income taxes add another layer of complexity to the tax landscape, as they are imposed at the county or city level in addition to state and federal taxes. These taxes are typically used to fund local government services such as schools, infrastructure, and public safety. Here’s a detailed overview of local income taxes and how they fit into the overall tax system:

-

Prevalence of Local Income Taxes:

- Eleven States: Allow county- or city-level income taxes.

- Varied Rates: The rates and structures of these local taxes vary significantly by jurisdiction.

- Examples:

- Alabama: Has county- or city-level income taxes with an average rate of 0.10 percent of adjusted gross income (AGI).

- Delaware: Features local income taxes with an average rate of 0.16 percent of AGI.

- Indiana: Has local income taxes with an average rate of 0.62 percent of AGI.

- Kentucky: Features local income taxes with an average rate of 1.33 percent of AGI.

- Maryland: Has local income taxes with an average rate of 2.40 percent of AGI.

- Michigan: Features local income taxes with an average rate of 0.17 percent of AGI.

- Missouri: Has local income taxes with an average rate of 0.22 percent of AGI.

- New York: Features local income taxes with an average rate of 1.63 percent of AGI.

- Ohio: Has local income taxes with an average rate of 1.57 percent of AGI.

- Pennsylvania: Features local income taxes with an average rate of 1.23 percent of AGI.

-

Types of Local Income Taxes:

- Wage Taxes: Imposed on wages and salaries earned within the jurisdiction.

- Resident Taxes: Levied on the income of residents, regardless of where it is earned.

- Earnings Taxes: Applied to both wages and net profits of businesses operating within the jurisdiction.

-

How Local Income Taxes Work:

- Tax Base: The tax base for local income taxes is typically similar to that of state income taxes, with some variations.

- Tax Rates: Local income tax rates are generally lower than state income tax rates.

- Collection: Local income taxes may be collected through withholding from wages or through direct payments by taxpayers.

-

Impact on Taxpayers:

- Additional Burden: Local income taxes add to the overall tax burden on individuals and businesses.

- Complexity: They increase the complexity of tax filing, as taxpayers must comply with both state and local tax laws.

- Location Decisions: Local income taxes can influence decisions about where to live and conduct business.

-

Benefits of Local Income Taxes:

- Funding Local Services: Local income taxes provide a dedicated revenue stream for funding local government services.

- Revenue Diversification: They diversify the local tax base, reducing reliance on property taxes and other revenue sources.

- Local Control: Local income taxes give local governments more control over their finances.

-

Challenges of Local Income Taxes:

- Economic Competitiveness: High local income taxes can make a jurisdiction less competitive for businesses and residents.

- Administrative Costs: Administering local income taxes can be costly and complex.

- Equity Concerns: Local income taxes can be regressive, disproportionately affecting low-income earners.

-

Interaction with State Income Taxes:

- Deductibility: In some cases, local income taxes may be deductible on state income tax returns, reducing the overall tax burden.

- Coordination: States and local governments must coordinate their tax systems to avoid double taxation and ensure compliance.

-

Other Local Taxes:

- Payroll Taxes: In California, Colorado, Kansas, New Jersey, Oregon, and West Virginia, some jurisdictions have payroll taxes, flat-rate wage taxes, or interest and dividend income taxes.

Local income taxes are an important part of the overall tax system in many states, providing crucial funding for local government services. However, they also add complexity and can impact decisions about where to live and conduct business.

9. What Recent Changes Have Occurred in State Income Tax Laws?

Recent changes in state income tax laws include rate reductions, bracket adjustments, and transitions to flat tax systems in several states.

State income tax laws are dynamic, with frequent changes driven by economic conditions, policy priorities, and legislative action. In recent years, several notable changes have occurred, including rate reductions, bracket adjustments, and transitions to flat tax systems. Here’s a detailed overview of recent state income tax changes:

-

Overall Trends:

- Rate Reductions: Many states have been reducing their individual income tax rates in recent years. From 2021 to 2023, 26 states enacted individual income tax rate reductions.

- Flat Tax Transitions: Some states are transitioning to flat tax systems, simplifying their tax structures.

- Bracket Adjustments: States are adjusting their tax brackets to account for inflation or to provide targeted tax relief.

-

Specific State Changes:

- Arkansas: