Does income-based repayment get forgiven? Yes, income-based repayment (IBR) plans offer loan forgiveness after a certain period, providing a significant opportunity for individuals seeking financial relief and strategic partnership prospects. At income-partners.net, we aim to connect you with resources and partners to navigate loan forgiveness and explore income growth opportunities. Discover various repayment plans and loan management strategies, and let us guide you toward financial freedom and collaborative success.

1. What Is Income-Based Repayment (IBR) and How Does It Work?

Yes, Income-Based Repayment (IBR) is a federal student loan repayment plan that sets your monthly payment amount based on your income and family size. This plan is designed to make student loan debt more manageable by ensuring payments are affordable. The remaining loan balance is forgiven after a specific repayment period, typically 20 or 25 years, depending on when you initially took out the loans.

IBR plans are a lifeline for borrowers with high debt compared to their income. Payments are capped at a percentage of your discretionary income, making budgeting more predictable. According to the Department of Education, IBR plans are available for eligible federal student loans, including Direct Loans and FFEL loans. The specific terms and eligibility criteria may vary, so understanding the details of your plan is crucial.

Key benefits of IBR plans:

- Affordable Payments: Payments are based on income and family size.

- Loan Forgiveness: Remaining balance is forgiven after 20 or 25 years.

- Flexibility: Adjustments can be made as income changes.

The application process involves submitting income documentation and updating it annually to ensure your payments remain aligned with your financial situation. This ongoing management is vital for maximizing the benefits of IBR and staying on track for loan forgiveness.

2. What Are the Different Types of Income-Driven Repayment Plans?

Yes, there are several types of Income-Driven Repayment (IDR) plans, each designed to cater to different financial situations and loan types. The main IDR plans include:

- SAVE (Saving on a Valuable Education): This plan, replacing REPAYE, offers the lowest monthly payments and faster forgiveness for smaller loan balances.

- PAYE (Pay As You Earn): Caps monthly payments at 10% of discretionary income.

- IBR (Income-Based Repayment): Payments are based on income, family size, and loan balance.

- ICR (Income Contingent Repayment): Payments are adjusted annually based on income, family size, and loan balance.

Each plan has unique features, benefits, and eligibility requirements.

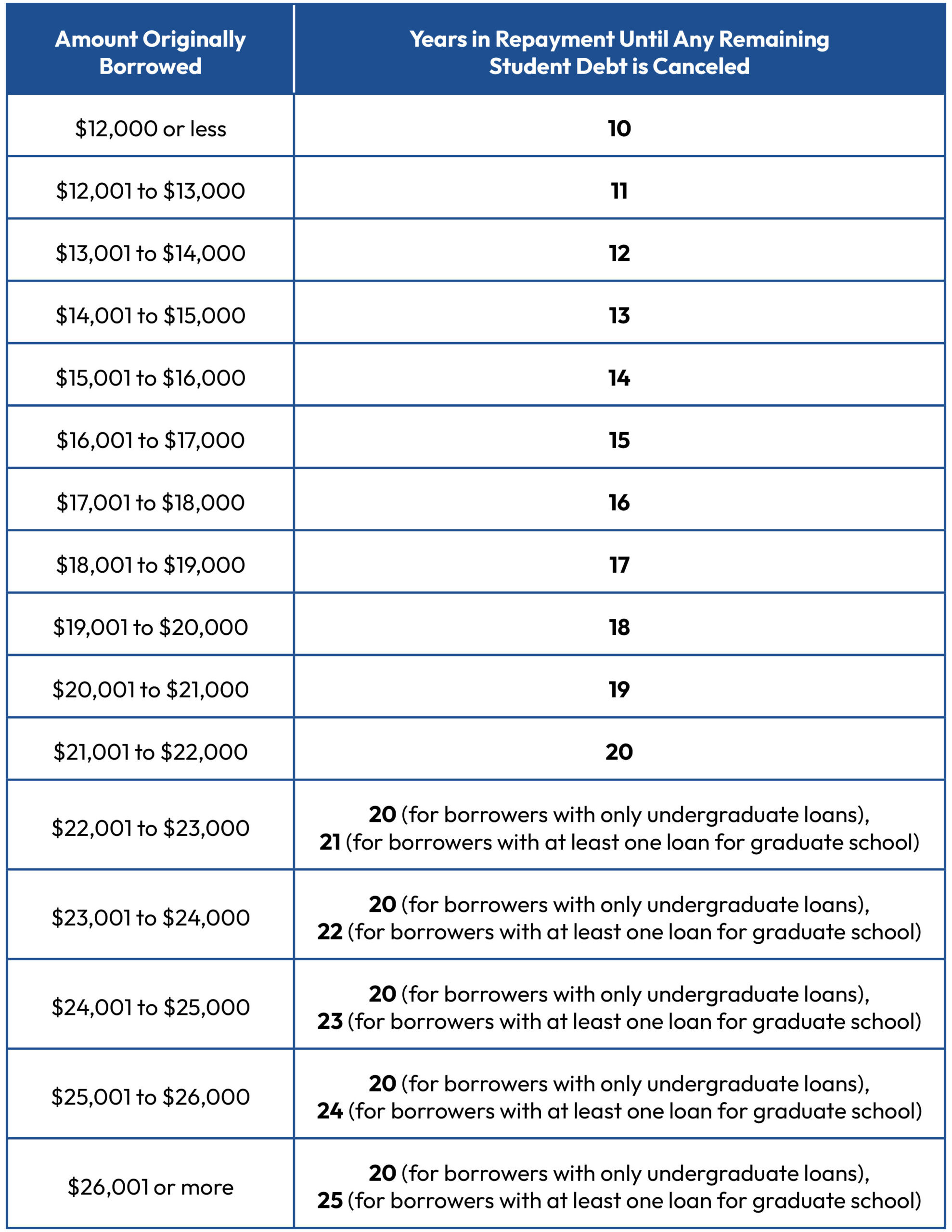

SAVE (Saving on a Valuable Education) Plan: This is the newest IDR plan, offering potentially the lowest monthly payments. If you borrowed $12,000 or less, your loans may be forgiven after just 10 years of payments. It also protects more of your income from being counted towards your monthly payment.

PAYE (Pay As You Earn) Plan: This plan is available to borrowers who demonstrate a partial financial hardship. It caps your monthly payments at 10% of your discretionary income, but never more than the 10-year Standard Repayment Plan amount. Any remaining balance is forgiven after 20 years.

IBR (Income-Based Repayment) Plan: There are actually two versions of IBR. The original IBR plan is available to borrowers who took out loans before July 1, 2014. Payments are capped at 15% of discretionary income, and the repayment period is 25 years. For borrowers who took out loans on or after July 1, 2014, payments are capped at 10% of discretionary income, and the repayment period is 20 years.

ICR (Income Contingent Repayment) Plan: This plan is available to any borrower with eligible federal student loans. Payments are calculated based on your income, family size, and the total amount of your Direct Loans. Payments are adjusted annually, and any remaining balance is forgiven after 25 years.

According to a study by the Brookings Institution, choosing the right IDR plan can significantly impact the total amount repaid and the timeline for loan forgiveness. Understanding the specifics of each plan and how they align with your financial goals is essential for effective student loan management.

3. How Long Does It Take For Income-Based Repayment to Be Forgiven?

Yes, the timeline for Income-Based Repayment (IBR) forgiveness depends on the specific plan you are enrolled in and the type of loans you have. Generally, forgiveness occurs after 20 to 25 years of qualifying payments.

Here’s a breakdown of the timelines for different IDR plans:

- SAVE Plan: 10 years for borrowers with original principal balances of $12,000 or less; 20 or 25 years for others, depending on loan type and amount borrowed.

- PAYE Plan: 20 years of qualifying payments.

- IBR Plan: 20 years for new borrowers as of July 1, 2014; 25 years for older borrowers.

- ICR Plan: 25 years of qualifying payments.

These timelines highlight the long-term commitment required to achieve loan forgiveness through IBR. Borrowers need to consistently make qualifying payments and adhere to the plan’s requirements to remain eligible. A report by the Congressional Budget Office emphasizes that consistent compliance with IDR plan requirements is crucial for borrowers aiming to receive loan forgiveness.

4. What Types of Loans Qualify for Income-Based Repayment Forgiveness?

Yes, several types of federal student loans qualify for Income-Based Repayment (IBR) forgiveness, including:

- Direct Subsidized Loans: Loans made directly by the U.S. Department of Education to eligible students.

- Direct Unsubsidized Loans: Loans made directly by the U.S. Department of Education to eligible students, but interest accrues from the time the loan is disbursed.

- Direct PLUS Loans: Loans made to graduate or professional students and parents of dependent undergraduate students.

- Direct Consolidation Loans: Loans that combine multiple federal student loans into one new loan.

Certain types of loans may not be eligible for IBR forgiveness on their own but can become eligible if consolidated into a Direct Consolidation Loan. Private student loans are generally not eligible for IBR forgiveness.

According to Federal Student Aid, eligible loans must be in good standing to qualify for IBR. Loans in default are not eligible until they are brought back into good standing through rehabilitation or consolidation. Borrowers should also be aware of specific loan types that may have different eligibility requirements, such as those with a variable interest rate.

5. How Is the Forgiveness Amount Calculated Under IBR?

Yes, the forgiveness amount under Income-Based Repayment (IBR) is calculated based on the remaining loan balance after the borrower has made the required number of qualifying payments. This balance includes both the principal and any accrued interest that has not been paid off during the repayment period.

The process involves several steps:

- Calculate Discretionary Income: Discretionary income is your adjusted gross income (AGI) minus a percentage of the poverty guideline for your family size and state.

- Determine Monthly Payment: Your monthly payment is a percentage of your discretionary income, depending on the specific IBR plan.

- Make Qualifying Payments: You must make the required number of qualifying payments (typically 20 or 25 years) under the IBR plan.

- Calculate Remaining Balance: After the repayment period, the remaining balance, including unpaid interest, is forgiven.

Keep in mind that, while the forgiven amount is calculated based on the remaining balance, changes in income, family size, and loan interest rates can influence the final forgiveness amount. A case study by the National Consumer Law Center found that borrowers with consistently low incomes and high loan balances benefit the most from IBR forgiveness, as they are likely to have a significant amount forgiven after the repayment period.

6. What Are the Requirements to Qualify for IBR Forgiveness?

Yes, to qualify for Income-Based Repayment (IBR) forgiveness, borrowers must meet several requirements:

- Eligible Loans: Must have eligible federal student loans, such as Direct Loans or FFEL loans.

- IBR Plan Enrollment: Must be enrolled in an Income-Based Repayment plan.

- Income Qualification: Must demonstrate a partial financial hardship based on income and loan debt.

- Qualifying Payments: Must make a certain number of qualifying payments (20 or 25 years, depending on the plan).

- Annual Income Recertification: Must annually recertify income and family size.

Maintaining eligibility requires consistent adherence to the plan’s requirements. Failure to recertify income or defaulting on the loan can result in disqualification from IBR and loss of eligibility for forgiveness. A report by the Urban Institute highlights the importance of staying informed about the plan requirements and promptly addressing any issues that may arise.

7. What Happens If My Income Increases During the IBR Repayment Period?

Yes, if your income increases during the Income-Based Repayment (IBR) period, your monthly payments will likely increase as well. IBR plans are designed to adjust your payments based on your current income and family size.

Here’s how it works:

- Annual Income Recertification: You are required to recertify your income and family size annually.

- Payment Adjustment: Based on your updated income, your monthly payments will be recalculated.

- Payment Cap: Some IBR plans have a payment cap, ensuring your payments never exceed the amount you would pay under the standard 10-year repayment plan.

Despite the potential for increased payments, remaining in the IBR plan can still be advantageous if your income fluctuates. The ultimate goal of IBR is loan forgiveness after a set period, regardless of income changes. According to the Education Data Initiative, even with fluctuating income, IBR provides a safety net, ensuring payments remain affordable and leading to eventual forgiveness.

8. Can I Lose Eligibility for IBR Forgiveness?

Yes, you can lose eligibility for Income-Based Repayment (IBR) forgiveness if you fail to meet certain requirements or comply with the terms of the plan. Common reasons for losing eligibility include:

- Failure to Recertify Income: Failing to annually recertify your income and family size can result in being removed from the IBR plan.

- Changing Loan Types: Consolidating eligible loans into ineligible loan types can disqualify you from IBR forgiveness.

- Defaulting on Loans: Defaulting on your student loans makes you ineligible for IBR.

- Exceeding Income Limits: If your income significantly increases and you no longer demonstrate a partial financial hardship, you may lose eligibility.

Maintaining eligibility requires diligence and adherence to the IBR plan’s requirements. Borrowers should regularly review their loan status and ensure they are meeting all necessary criteria. A study by the National Foundation for Credit Counseling emphasizes the importance of proactive loan management to avoid losing eligibility for IBR forgiveness.

9. Are There Tax Implications for IBR Loan Forgiveness?

Yes, the tax implications of Income-Based Repayment (IBR) loan forgiveness can be a significant consideration for borrowers. Generally, the amount of student loan debt forgiven under IBR is considered taxable income by the IRS.

However, there are exceptions:

- Through 2025: Under current law, student loan forgiveness is tax-free through December 31, 2025, due to provisions in the American Rescue Plan Act.

- Insolvency: If you are insolvent (meaning your liabilities exceed your assets) at the time of forgiveness, you may not have to pay taxes on the forgiven amount.

Given the potential tax implications, it’s wise to consult a tax professional to understand your specific situation and plan accordingly. The IRS provides detailed guidance on student loan forgiveness and tax obligations, which can help borrowers prepare for any potential tax liabilities.

10. What Is the SAVE Plan and How Does It Affect IBR Forgiveness?

Yes, the SAVE (Saving on A Valuable Education) Plan is a new income-driven repayment plan that replaces the REPAYE plan. It offers more favorable terms for many borrowers, including:

- Lower Monthly Payments: Payments are calculated based on a smaller percentage of discretionary income.

- Faster Forgiveness: Borrowers with original loan balances of $12,000 or less may receive forgiveness after just 10 years of payments.

- Interest Benefit: Unpaid interest is waived, preventing loan balances from growing.

The SAVE Plan impacts IBR forgiveness by providing a more affordable and accelerated path to loan forgiveness. It is designed to help borrowers manage their student loan debt more effectively. According to the Department of Education, the SAVE Plan is expected to significantly reduce the financial burden of student loans for millions of Americans.

11. Can I Include Spousal Income in IBR Calculations?

Yes, whether you include spousal income in Income-Based Repayment (IBR) calculations depends on your marital status and the specific IBR plan you are enrolled in.

- Married Filing Jointly: If you are married and file your taxes jointly, your spouse’s income will be included in the IBR calculation. This can result in higher monthly payments.

- Married Filing Separately: If you are married and file your taxes separately, your spouse’s income may or may not be included, depending on the specific IBR plan. Some plans, like the original IBR, may exclude spousal income if you file separately, while others, like REPAYE, always include it.

Understanding how your marital status and tax filing status impact your IBR payments is essential for effective financial planning. A financial advisor can provide personalized guidance on the best approach for managing your student loans as a married individual.

12. How Does Loan Consolidation Affect IBR Forgiveness?

Yes, loan consolidation can affect Income-Based Repayment (IBR) forgiveness in several ways. Consolidating your federal student loans into a Direct Consolidation Loan can make you eligible for IBR if you have loans that don’t qualify on their own.

Benefits of Consolidation:

- Eligibility for IBR: Consolidation can make ineligible loans eligible for IBR.

- Simplified Payments: Combining multiple loans into one can simplify your monthly payments.

Drawbacks of Consolidation:

- Interest Accrual: Consolidation can capitalize unpaid interest, increasing the overall loan balance.

- Loss of Credit: Consolidating can reset the count of qualifying payments toward forgiveness, potentially delaying your forgiveness timeline.

Before consolidating, carefully consider the potential benefits and drawbacks. Consult with a student loan advisor to determine if consolidation aligns with your financial goals. Federal Student Aid provides resources and guidance on loan consolidation and its impact on IBR forgiveness.

13. What Is the One-Time IDR Account Adjustment and How Does It Help?

Yes, the one-time IDR account adjustment is a special initiative by the U.S. Department of Education to give borrowers credit for past payments that may not have been accurately counted toward Income-Driven Repayment (IDR) forgiveness.

The adjustment aims to:

- Correct Past Errors: Address inaccuracies in payment counts due to servicing errors or forbearance steering.

- Give Credit for Prior Payments: Provide credit for payments made under any repayment plan, as well as certain periods of deferment and forbearance.

- Accelerate Forgiveness: Help eligible borrowers reach IDR forgiveness faster.

This initiative is particularly beneficial for borrowers who have been in repayment for many years but have not yet received forgiveness due to servicing issues. The Department of Education provides detailed information on the one-time IDR account adjustment and how borrowers can benefit from it.

14. How Do Deferment and Forbearance Affect IBR Forgiveness?

Yes, deferment and forbearance can affect Income-Based Repayment (IBR) forgiveness by temporarily suspending your loan payments. While these options can provide short-term relief, they generally do not count toward your qualifying payments for IBR forgiveness.

- Deferment: A period of authorized temporary suspension of loan payments.

- Forbearance: A period of authorized temporary postponement or reduction of loan payments.

During deferment and forbearance, interest may continue to accrue on your loans, increasing the overall balance. Although these periods typically don’t count toward IBR forgiveness, the one-time IDR account adjustment may provide credit for certain periods of deferment and forbearance. Reviewing the terms of your IBR plan and understanding how deferment and forbearance impact your forgiveness timeline is crucial for effective loan management.

15. What Happens After IBR Loan Forgiveness Is Granted?

Yes, after Income-Based Repayment (IBR) loan forgiveness is granted, the remaining balance on your eligible federal student loans is discharged. This means you are no longer obligated to repay that amount.

Here’s what typically happens:

- Notification: You will receive a notification from your loan servicer confirming that your loans have been forgiven.

- Loan Status Update: Your loan status will be updated to reflect that the loans have been discharged.

- Tax Implications: Be aware of potential tax implications on the forgiven amount, though currently, loan forgiveness is tax-free through 2025.

- Credit Report: The forgiven loans will be reported to credit bureaus, which may impact your credit report.

It’s essential to keep records of your loan forgiveness documentation for tax purposes and to monitor your credit report for any discrepancies. A financial advisor can help you navigate the financial implications of loan forgiveness.

16. Can I Switch Between Different Income-Driven Repayment Plans?

Yes, you can switch between different Income-Driven Repayment (IDR) plans, but it’s important to carefully consider the implications before doing so. Switching plans can affect your monthly payments, the total amount you repay, and the timeline for loan forgiveness.

Here are some factors to consider:

- Eligibility: Ensure you meet the eligibility requirements for the new IDR plan.

- Payment Amount: Compare the estimated monthly payments under each plan.

- Forgiveness Timeline: Understand how switching plans may impact your forgiveness timeline.

- Interest Accrual: Consider how interest accrual may differ under each plan.

Before switching, use the loan simulator tool on the Federal Student Aid website to compare the potential outcomes under different IDR plans. A student loan advisor can provide personalized guidance on whether switching plans aligns with your financial goals.

17. What Resources Are Available to Help Me Understand IBR Forgiveness?

Yes, numerous resources are available to help you understand Income-Based Repayment (IBR) forgiveness and navigate the complexities of student loan repayment.

Key resources include:

- Federal Student Aid Website: Provides comprehensive information on IBR plans, eligibility requirements, and loan forgiveness.

- Student Loan Borrower Assistance: Offers resources and support for borrowers, including information on IDR plans and loan management strategies.

- U.S. Department of Education: Offers detailed guidance on federal student loan programs.

- Non-Profit Organizations: Such as the National Foundation for Credit Counseling, provide free or low-cost financial counseling and student loan advice.

- Financial Advisors: Offer personalized advice on managing student loans and achieving financial goals.

These resources can help you make informed decisions about your student loan repayment options and maximize your chances of achieving loan forgiveness. At income-partners.net, we also provide valuable information and connections to assist you in navigating your financial journey.

18. How Can I Maximize My Chances of Getting IBR Forgiveness?

Yes, maximizing your chances of getting Income-Based Repayment (IBR) forgiveness involves careful planning and diligent management of your student loans.

Here are key strategies:

- Choose the Right IBR Plan: Select the plan that best fits your financial situation and goals.

- Stay Eligible: Meet all eligibility requirements, including annual income recertification.

- Make Qualifying Payments: Consistently make your monthly payments on time.

- Avoid Default: Take steps to avoid defaulting on your loans.

- Keep Records: Maintain detailed records of your loan payments and communications with your loan servicer.

- Seek Professional Advice: Consult with a financial advisor or student loan expert for personalized guidance.

By following these strategies, you can increase your likelihood of successfully achieving IBR forgiveness and securing your financial future.

19. What Are the Potential Pitfalls of Relying on IBR Forgiveness?

Yes, while Income-Based Repayment (IBR) forgiveness can be a valuable option for managing student loan debt, there are potential pitfalls to consider:

- Long Repayment Period: The repayment period for IBR is typically 20 or 25 years, which is longer than standard repayment plans.

- Accrued Interest: Interest can accrue over time, increasing the overall loan balance.

- Tax Implications: The forgiven amount may be considered taxable income, though currently, loan forgiveness is tax-free through 2025.

- Income Fluctuations: Changes in income can impact monthly payments and eligibility for IBR.

- Plan Changes: IDR plan terms and eligibility requirements can change over time.

Being aware of these potential pitfalls can help you make informed decisions about whether IBR is the right option for you. A comprehensive financial plan can help you mitigate these risks and achieve your financial goals.

20. How Does IBR Forgiveness Compare to Public Service Loan Forgiveness (PSLF)?

Yes, Income-Based Repayment (IBR) forgiveness and Public Service Loan Forgiveness (PSLF) are both programs that forgive the remaining balance on federal student loans, but they have different eligibility requirements and terms.

IBR Forgiveness:

- Eligibility: Available to borrowers with eligible federal student loans who are enrolled in an IDR plan.

- Repayment Period: Typically 20 or 25 years of qualifying payments.

- Employment: Not tied to specific employment.

PSLF:

- Eligibility: Available to borrowers who work full-time for a qualifying public service employer.

- Repayment Period: Requires 10 years (120 qualifying payments) of public service employment.

- Employment: Requires specific public service employment.

The key difference is that PSLF requires employment in a qualifying public service job, while IBR forgiveness is available to any eligible borrower regardless of employment. PSLF also offers a shorter repayment period. Deciding which program is right for you depends on your career path and financial situation.

21. What Role Does Income-Partners.Net Play in Helping People Understand IBR?

Yes, income-partners.net plays a crucial role in helping individuals understand Income-Based Repayment (IBR) by providing:

- Comprehensive Information: Offering detailed articles, guides, and resources on IBR plans, eligibility requirements, and loan forgiveness.

- Expert Insights: Sharing insights and advice from financial experts and student loan advisors.

- Partnership Opportunities: Connecting individuals with partners and resources to manage their student loan debt effectively.

- Community Support: Fostering a community where borrowers can share experiences, ask questions, and find support.

- Up-to-Date Information: Keeping users informed about the latest changes and updates to IBR programs and policies.

We strive to empower individuals with the knowledge and resources they need to make informed decisions about their student loans and achieve financial freedom. At income-partners.net, we are committed to being your trusted partner in navigating the complexities of IBR and building a brighter financial future.

Student Loan Forgiveness Illustration

Student Loan Forgiveness Illustration

FAQ About Income-Based Repayment (IBR)

1. What is discretionary income in the context of IBR?

Discretionary income is your adjusted gross income (AGI) minus a percentage of the poverty guideline for your family size and state.

2. How often do I need to recertify my income for IBR?

You need to recertify your income annually to remain eligible for IBR.

3. Can private student loans be included in IBR?

No, private student loans are not eligible for IBR. Only federal student loans qualify.

4. What happens if I miss payments under IBR?

Missing payments can lead to default, which disqualifies you from IBR.

5. Is there a limit to how much my IBR payments can increase?

Some IBR plans have a payment cap, ensuring payments never exceed the standard 10-year repayment plan amount.

6. How does marriage affect my IBR payments?

If you file taxes jointly, your spouse’s income will be included in the IBR calculation.

7. Can I switch from IBR to PSLF?

Yes, you can switch to PSLF if you meet the eligibility requirements, including qualifying employment.

8. What is the SAVE plan, and how is it different from other IBR plans?

The SAVE plan offers lower monthly payments, faster forgiveness for smaller loan balances, and an interest benefit, making it more favorable than other IBR plans.

9. Will I receive a tax form for the forgiven amount under IBR?

Yes, you will typically receive a 1099-C form for the forgiven amount, which may be considered taxable income.

10. How do I apply for IBR forgiveness?

IBR loan forgiveness is automatically granted after you make your last qualifying payment, but you must ensure you are enrolled in an eligible IBR plan and have met all requirements.

Ready to explore your options for Income-Based Repayment and discover potential partnerships for income growth? Visit income-partners.net today to learn more about strategic financial planning and connect with experts who can guide you toward a brighter financial future. Don’t wait – your path to financial freedom and collaborative success starts here! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.