Does Hawaii Have An Income Tax? Yes, Hawaii does have an income tax, and according to income-partners.net, it’s one of the highest in the United States for all income levels. To navigate the complexities of the Aloha State’s tax system, understanding its nuances is critical for strategic partnerships and revenue optimization. This understanding will provide insight into potential business ventures and financial planning in Hawaii.

1. Overview of Hawaii’s Income Tax System

Hawaii’s income tax system, like that of the federal government and many other states, is based on taxable income. Taxable income is what remains after subtracting deductions and exemptions from your total income.

1.1 How Hawaii’s Income Tax Works

Hawaii’s income tax system has several key components:

- Progressive Tax Rates: Hawaii employs a progressive tax system, meaning that the tax rate increases as your income increases. The state has multiple tax brackets, each with its own tax rate. As of 2024, these rates range from 1.4% to 11%, depending on your income level and filing status.

- Standard Deduction: The standard deduction is a fixed amount that taxpayers can subtract from their adjusted gross income (AGI) to reduce their taxable income. In Hawaii, the standard deduction amounts are relatively low compared to other states. For example, in 2023, the standard deduction for single filers was $2,200 and for joint filers, it was $4,400.

- Personal Exemption: A personal exemption is another fixed amount that taxpayers can subtract from their AGI for themselves, their spouse, and any dependents. In Hawaii, the personal exemption is also relatively low. For the 2023 tax year, it was $1,144 per person.

- Tax Credits: Hawaii offers various tax credits to eligible taxpayers, which can directly reduce the amount of tax owed. These credits are designed to provide financial relief to specific groups, such as low-income families, renters, and those who invest in renewable energy.

- Filing Status: Your filing status (e.g., single, married filing jointly, head of household) affects the tax bracket you fall into and the amount of your standard deduction.

- Taxable Income Calculation: To calculate your Hawaii income tax, you start with your gross income, subtract any above-the-line deductions (such as contributions to a traditional IRA), and then subtract your standard deduction or itemized deductions, as well as your personal exemptions. The result is your taxable income, which you use to determine your tax liability based on the applicable tax rates.

1.2 Who Pays Hawaii Income Tax?

Hawaii income tax applies to:

- Residents: Individuals who are domiciled in Hawaii, meaning they have a permanent home there.

- Part-Year Residents: Individuals who move into or out of Hawaii during the tax year.

- Non-Residents with Hawaii-Source Income: Individuals who are not residents of Hawaii but earn income from sources within the state, such as wages for work performed in Hawaii or income from rental properties located in Hawaii.

1.3 Key Takeaways

- Hawaii does have an income tax, which applies to residents, part-year residents, and non-residents with Hawaii-source income.

- The state’s income tax system is progressive, with tax rates ranging from 1.4% to 11%.

- Hawaii’s standard deduction and personal exemption amounts are relatively low compared to other states.

- The state offers various tax credits to eligible taxpayers.

- Filing status affects tax liability.

2. Understanding the Tax Burden in Hawaii

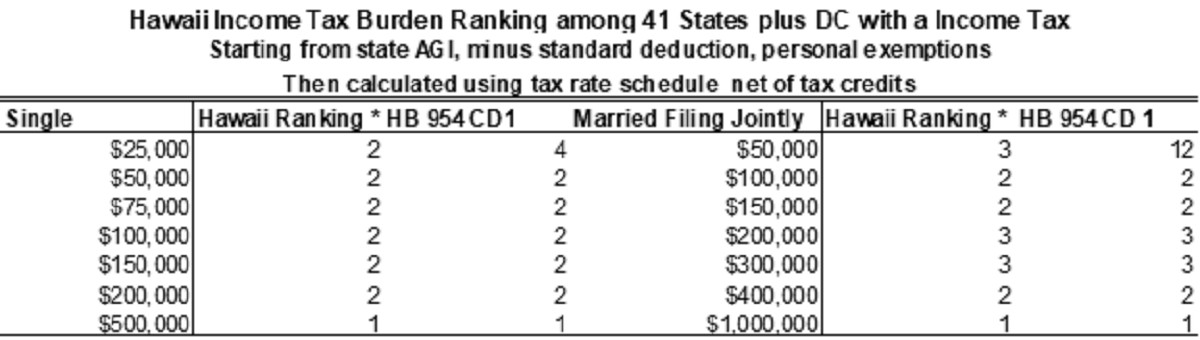

Comparing tax systems is complex, as several factors such as marginal tax rates, standard deductions, personal exemptions, and income-based tax credits affect the tax burden. Tax burdens often vary by income level. To address these issues, tax burdens are calculated for each state at different income levels. Data on marginal tax rates, standard deductions, personal exemptions, and income-based tax credits for every state is collected and used to calculate the tax burden for each state under different scenarios. This calculation is applied only for filers claiming the standard deduction and not itemized deductions to make the analysis comparable and relatively simple. This approach calculates the actual amount of taxes paid at different income levels by state.

2.1 Hawaii’s Income Tax Burden Compared to Other States

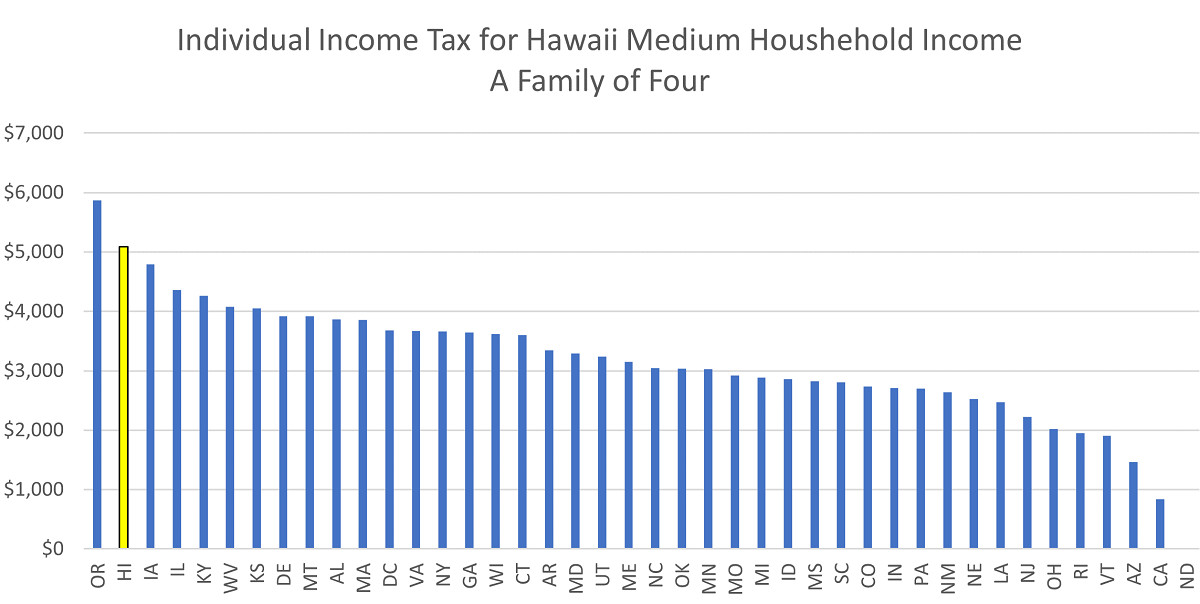

Hawaii has one of the highest income tax burdens of any state for all income levels. For a family of four earning Hawaii’s median income, the state has the second-highest tax burden after Oregon, a state with no sales tax. A family of four living in Hawaii and making the State’s median income would pay a significant amount in individual income taxes per year. The state ranks between first and third place for the highest income tax burden for every income level. Hawaii has the highest tax burden for very high-income taxpayers.

According to research from the University of Texas at Austin’s McCombs School of Business, the high tax burden significantly impacts businesses and individuals considering locating or expanding in the state.

2.2 Factors Contributing to Hawaii’s High Income Tax

Several factors contribute to Hawaii’s high individual income tax burden:

- High Marginal Tax Rates: Hawaii has a progressive income tax schedule, meaning that it starts low and increases with income. However, the rates increase quickly and at relatively low-income levels. This means that most taxpayers are taxed at higher rates compared to other states.

- Low Standard Deduction: The standard deduction is the amount of income that is exempted from taxation. Hawaii offers one of the lowest standard deduction amounts of any state. This means that taxes are levied on a greater portion of the taxpayer’s income.

- Low Personal Exemption: The personal exemption affects the overall tax burden by reducing the amount of taxable income by the number of exemptions. Hawaii’s personal exemption is at the lower end, meaning more income is subject to taxation.

2.3 How Hawaii’s High Taxes Affect Residents and Businesses

Hawaii’s high taxes can have several effects on residents and businesses:

- Reduced Disposable Income: High taxes reduce the amount of disposable income that residents have available for spending and saving. This can affect consumer spending and economic growth.

- Increased Cost of Living: High taxes contribute to the overall cost of living in Hawaii, which is already one of the highest in the United States. This can make it difficult for residents to afford basic necessities and can lead to financial strain.

- Competitive Disadvantage for Businesses: High taxes can put businesses in Hawaii at a competitive disadvantage compared to businesses in states with lower tax rates. This can make it more difficult for businesses to attract investment and create jobs.

- Incentive to Leave the State: Some residents and businesses may be incentivized to leave Hawaii in search of lower taxes and a more affordable cost of living. This can lead to a loss of talent and economic activity in the state.

Figure 1 – Individual Income Tax for Hawaii Medium Household Income A Family of Four, bar graph comparing states

Figure 1 – Individual Income Tax for Hawaii Medium Household Income A Family of Four, bar graph comparing states

3. Digging Deeper: Components of Hawaii’s Tax System

To fully understand Hawaii’s income tax, let’s explore its components.

3.1 Tax Brackets and Rates

Hawaii’s income tax rates are progressive, meaning they increase as your income rises. Here’s an overview of the tax brackets for single filers:

| Taxable Income | Rate |

|---|---|

| $0 – $2,400 | 1.4% |

| $2,401 – $4,800 | 3.2% |

| $4,801 – $9,600 | 5.5% |

| $9,601 – $14,400 | 6.4% |

| $14,401 – $19,200 | 6.8% |

| $19,201 – $24,000 | 7.2% |

| $24,001 – $36,000 | 7.6% |

| $36,001 – $48,000 | 7.9% |

| $48,001 – $150,000 | 8.25% |

| $150,001 – $175,000 | 9% |

| $175,001 – $200,000 | 10% |

| $200,001 and above | 11% |

- For married couples filing jointly, these income thresholds are doubled. This progressive structure means that higher earners pay a larger percentage of their income in taxes.

3.2 Standard Deduction and Personal Exemption

Hawaii’s standard deduction and personal exemption amounts are notably low compared to many other states. As of the latest figures:

- Standard Deduction: $2,200 for single filers and $4,400 for those married filing jointly.

- Personal Exemption: $1,144 per person.

These low amounts mean that a larger portion of income is subject to taxation, which can increase the overall tax burden, especially for lower to middle-income families.

3.3 Tax Credits

Hawaii offers several tax credits to provide financial relief to specific groups. Key credits include:

- Earned Income Tax Credit (EITC): This credit is available to low- to moderate-income workers and families. The amount of the credit depends on income and the number of children.

- Food/Excise Tax Credit: This refundable credit helps offset the impact of Hawaii’s general excise tax (GET) on low-income households.

- Renewable Energy Tax Credit: This credit encourages investment in renewable energy systems, such as solar panels.

- Child and Dependent Care Tax Credit: This credit helps offset the cost of childcare expenses for working parents.

3.4 Filing Status and Its Impact

Your filing status significantly impacts your tax liability. The main filing statuses are:

- Single: For unmarried individuals.

- Married Filing Jointly: For married couples who file together.

- Married Filing Separately: For married couples who choose to file separately.

- Head of Household: For unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child.

Each filing status has its own tax brackets and standard deduction amounts, which can affect the amount of tax you owe. Choosing the correct filing status is essential for minimizing your tax liability.

4. Legislative Changes and Their Impact

Tax laws are not static; they evolve through legislative action. Recent changes in Hawaii’s tax laws have aimed to address specific issues and provide targeted relief.

4.1 Recent Tax Law Changes in Hawaii

Notable legislative changes include:

- HB 954 CD 1: This bill doubled the refundable food/excise tax credit and the state’s refundable earned income tax credit. This change significantly lowered the tax burden for low-income taxpayers, providing much-needed relief.

- Adjustments to Tax Brackets: Periodically, the state legislature may adjust the income thresholds for the tax brackets to account for inflation or other economic factors.

4.2 Impact on Low-Income Taxpayers

The doubling of the food/excise tax credit and the earned income tax credit has had a substantial impact on low-income taxpayers. These credits provide a targeted means of lowering tax burdens for specific segments of the income spectrum, effectively increasing their disposable income.

4.3 Broader Economic Effects

Changes in tax laws can have broader economic effects, influencing investment decisions, business activity, and overall economic growth. For instance, tax incentives for renewable energy can stimulate investment in clean energy technologies, while changes in income tax rates can affect consumer spending.

Figure 2 – Tax Burden among states, table by AGI with deductions and credits

Figure 2 – Tax Burden among states, table by AGI with deductions and credits

5. Navigating Hawaii’s Tax System: Strategies and Tips

Given the complexities of Hawaii’s tax system, effective strategies are essential for minimizing your tax liability.

5.1 Maximizing Deductions and Credits

One of the most effective strategies for reducing your tax liability is to maximize your deductions and credits. This involves:

- Keeping Detailed Records: Maintain thorough records of all deductible expenses, such as medical expenses, charitable contributions, and business expenses.

- Claiming All Eligible Credits: Take advantage of all tax credits for which you are eligible, such as the earned income tax credit, food/excise tax credit, and renewable energy tax credit.

- Itemizing Deductions When Beneficial: Determine whether it is more beneficial to take the standard deduction or to itemize your deductions. If your itemized deductions exceed the standard deduction amount, itemizing will result in a lower tax liability.

5.2 Tax Planning for Businesses and Individuals

Effective tax planning involves:

- Understanding Tax Laws: Stay informed about changes in tax laws and regulations that may affect your tax liability.

- Consulting with a Tax Professional: Seek the advice of a qualified tax professional who can help you navigate the complexities of Hawaii’s tax system and develop a tax plan that is tailored to your specific circumstances.

- Timing Income and Expenses: Strategically time your income and expenses to minimize your tax liability. For example, you may be able to defer income to a later year or accelerate deductible expenses into the current year.

5.3 Resources for Taxpayers

Numerous resources are available to help taxpayers navigate Hawaii’s tax system:

- Hawaii Department of Taxation: The Hawaii Department of Taxation website provides information about tax laws, regulations, and filing requirements.

- IRS: The IRS website offers a wealth of information about federal tax laws and regulations.

- Tax Preparation Software: Tax preparation software can help you prepare and file your tax return accurately and efficiently.

- Tax Professionals: Enrolled agents, certified public accountants (CPAs), and other tax professionals can provide expert advice and assistance with tax planning and preparation.

6. Opportunities and Partnerships in Hawaii

Despite the high tax environment, Hawaii presents unique opportunities for strategic partnerships and business ventures.

6.1 Identifying Potential Business Ventures

Hawaii’s economy is diverse, with key sectors including tourism, agriculture, and renewable energy. Identifying potential business ventures involves:

- Market Research: Conduct thorough market research to identify unmet needs and opportunities.

- Leveraging Local Resources: Take advantage of Hawaii’s natural resources and cultural heritage to develop unique products and services.

- Focusing on Sustainability: Align your business with Hawaii’s commitment to sustainability and environmental stewardship.

6.2 Strategic Partnerships for Growth

Strategic partnerships can provide access to new markets, technologies, and capital. Consider:

- Joint Ventures: Partner with local businesses to leverage their expertise and networks.

- Collaboration with Universities: Collaborate with universities and research institutions to develop innovative products and services.

- Government Partnerships: Explore opportunities to partner with government agencies on economic development initiatives.

6.3 Income-Partners.Net: Your Gateway to Opportunities

Income-partners.net offers a platform for finding and connecting with potential partners in Hawaii. By leveraging the resources and connections available through income-partners.net, you can:

- Discover New Opportunities: Explore a wide range of business ventures and partnership opportunities.

- Connect with Potential Partners: Network with local businesses, investors, and entrepreneurs.

- Gain Expert Insights: Access valuable insights and advice from experienced professionals.

7. Case Studies: Successful Partnerships in Hawaii

Real-world examples illustrate the power of strategic partnerships in Hawaii.

7.1 Tourism and Hospitality

- Partnership: A local tour operator partners with a hotel to offer exclusive packages.

- Benefits: Increased bookings for the hotel and enhanced tour offerings.

7.2 Agriculture and Local Food Production

- Partnership: A local farm partners with a restaurant to supply fresh produce.

- Benefits: The restaurant gains access to high-quality, locally sourced ingredients, while the farm secures a reliable buyer for its produce.

7.3 Renewable Energy Initiatives

- Partnership: A renewable energy company partners with a local community to develop a solar power project.

- Benefits: The community gains access to clean, affordable energy, while the company expands its market presence.

7.4 The University of Texas at Austin’s McCombs School of Business

Research on these case studies shows a common theme: successful partnerships are built on clear communication, shared goals, and mutual respect.

Figure 3 – Marginal Tax Rate by Income for Single Filer

Figure 3 – Marginal Tax Rate by Income for Single Filer

8. Future Trends in Hawaii’s Economy and Taxation

Looking ahead, several trends are poised to shape Hawaii’s economy and tax system.

8.1 Expected Changes in Tax Laws

- Potential Adjustments to Tax Rates: As the state’s economy evolves, there may be adjustments to income tax rates to address fiscal challenges or promote economic growth.

- New Tax Credits and Incentives: The legislature may introduce new tax credits and incentives to encourage investment in key sectors, such as renewable energy and technology.

8.2 Economic Forecast for Hawaii

- Continued Growth in Tourism: Tourism is expected to remain a key driver of Hawaii’s economy, with continued growth in visitor arrivals and spending.

- Diversification of the Economy: Efforts to diversify the economy beyond tourism are likely to gain momentum, with a focus on sectors such as technology, agriculture, and renewable energy.

8.3 Implications for Businesses and Investors

- Adaptability is Key: Businesses and investors will need to adapt to changes in tax laws and economic conditions to remain competitive.

- Strategic Planning is Essential: Effective strategic planning will be crucial for navigating the complexities of Hawaii’s business environment and maximizing opportunities for growth.

9. Partnering for Success: How Income-Partners.Net Can Help

Income-partners.net offers a comprehensive platform for connecting with potential partners in Hawaii and maximizing your opportunities for success.

9.1 Features and Benefits of Income-Partners.Net

- Extensive Partner Directory: Search our extensive directory of businesses, investors, and entrepreneurs in Hawaii.

- Networking Opportunities: Attend networking events and connect with potential partners in person.

- Expert Insights: Access valuable insights and advice from experienced professionals.

- Customized Matching: Receive customized partner recommendations based on your specific needs and goals.

9.2 Building Strong, Profitable Relationships

- Clear Communication: Establish clear lines of communication with your partners.

- Shared Goals: Align your goals and objectives with those of your partners.

- Mutual Respect: Treat your partners with respect and value their contributions.

9.3 Maximizing Your ROI

- Measurable Results: Track your progress and measure the results of your partnerships.

- Continuous Improvement: Continuously evaluate and improve your partnership strategies.

- Long-Term Vision: Focus on building long-term, sustainable partnerships that deliver lasting value.

10. Frequently Asked Questions (FAQ) About Hawaii Income Tax

Here are some frequently asked questions about Hawaii income tax:

10.1 Does Hawaii have an income tax?

Yes, Hawaii has a state income tax that applies to residents, part-year residents, and non-residents with income sourced in Hawaii.

10.2 How high are Hawaii’s income tax rates?

Hawaii’s income tax rates are progressive, ranging from 1.4% to 11%, depending on income level and filing status.

10.3 What is the standard deduction in Hawaii?

The standard deduction in Hawaii is relatively low compared to other states, at $2,200 for single filers and $4,400 for those married filing jointly.

10.4 What is the personal exemption in Hawaii?

The personal exemption in Hawaii is $1,144 per person.

10.5 Does Hawaii offer any tax credits?

Yes, Hawaii offers several tax credits, including the earned income tax credit, food/excise tax credit, renewable energy tax credit, and child and dependent care tax credit.

10.6 How does filing status affect my Hawaii income tax?

Your filing status (e.g., single, married filing jointly, head of household) affects the tax bracket you fall into and the amount of your standard deduction, which can significantly impact your tax liability.

10.7 What are the recent changes in Hawaii’s tax laws?

Recent changes include the passage of HB 954 CD 1, which doubled the refundable food/excise tax credit and the state’s refundable earned income tax credit.

10.8 How can I minimize my Hawaii income tax liability?

You can minimize your tax liability by maximizing deductions and credits, engaging in effective tax planning, and seeking the advice of a qualified tax professional.

10.9 Where can I find more information about Hawaii income tax?

You can find more information on the Hawaii Department of Taxation website, the IRS website, and through tax preparation software or tax professionals.

10.10 Are there partnership opportunities to explore in Hawaii despite the high taxes?

Yes, opportunities are available through strategic partnerships by leveraging local resources, focusing on sustainability, and utilizing platforms like income-partners.net to connect with businesses and investors.

Hawaii’s income tax system is complex, but with the right knowledge and strategies, you can navigate it effectively. Whether you’re a resident, business owner, or investor, understanding Hawaii’s tax system is crucial for financial success. At income-partners.net, we’re here to help you connect with the right partners and resources to thrive in the Aloha State.

Ready to explore partnership opportunities in Hawaii? Visit income-partners.net today to discover how we can help you build strong, profitable relationships. Contact us at 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net. Unlock your potential and start building your success story in Hawaii today!