Does Farmers Pay Income Tax? Yes, farmers generally do pay income tax, but there are specific rules and exceptions designed to accommodate the unique nature of the farming business. At income-partners.net, we help you navigate these regulations and find potential partners to optimize your tax strategy and boost your income. Farmers’ tax, agriculture tax, and farm partnership are key for financial success.

1. Who Qualifies as a Farmer for Tax Purposes?

To understand whether a farmer pays income tax, we first need to define who qualifies as a farmer under IRS regulations.

Answer: An individual is considered a qualifying farmer if at least 66 ⅔ percent of their total gross income comes from farming activities, either in the current or preceding tax year.

Elaboration: This definition, as outlined in IRC § 6654(i), recognizes the unique income patterns of farmers, which can be unpredictable due to weather, market fluctuations, and other factors. This provision protects farmers from the burden of making quarterly estimated tax payments, which are typically required for self-employed individuals. Understanding this rule is crucial for tax planning and potential partnership opportunities, which you can explore further on income-partners.net.

1.1. What is Included in “Gross Income from Farming”?

It’s essential to know what the IRS considers farming income.

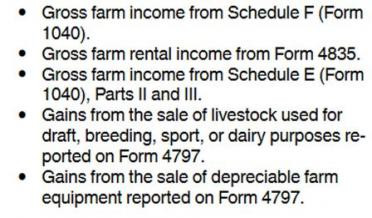

Answer: Gross income from farming includes income from cultivating the soil, raising livestock, dairy farming, beekeeping, and operating a poultry or fruit farm.

Elaboration: According to Publication 225, gross income from farming encompasses a broad range of activities directly related to agricultural production. This includes, but is not limited to:

- Sale of Crops: Income from selling grains, vegetables, fruits, and other agricultural products.

- Livestock Sales: Revenue from selling cattle, hogs, poultry, and other animals raised on the farm.

- Dairy Products: Income from the sale of milk, cheese, and other dairy products.

- Poultry and Eggs: Revenue from raising poultry and selling eggs.

- Other Farm Products: Income from beekeeping, honey production, and the sale of other farm-related products.

In 2023, the IRS added gains from the sale of depreciable farm equipment reported on Form 4797 to the list of farm income in Publication 225. This inclusion acknowledges the financial impact of equipment sales on a farmer’s income and simplifies tax reporting. This change helps farmers understand their tax obligations and potentially identify new partnership opportunities through income-partners.net.

Farmers examining crops in a field, symbolizing the core of agricultural income

Farmers examining crops in a field, symbolizing the core of agricultural income

1.2. What is “Total Gross Income”?

Understanding total gross income is just as important as knowing what constitutes farming income.

Answer: Total gross income includes all income from any source, including farming and non-farming activities.

Elaboration: “Total gross income” is a comprehensive measure of all revenue a taxpayer receives during the year. This includes income from farming, wages, investments, business ventures, and any other source of revenue. This figure is used to determine whether the 66 ⅔ percent threshold is met for qualifying as a farmer under the IRS rules. This threshold is important because it dictates whether a farmer can take advantage of special tax provisions, such as exemptions from quarterly estimated tax payments. income-partners.net can help you find resources and partners to diversify your income streams and manage your overall tax burden effectively.

2. What Are the Estimated Tax Payment Rules for Farmers?

Farmers have different rules for estimated tax payments compared to other self-employed individuals.

Answer: Farmers are exempt from quarterly estimated tax payments if they meet specific conditions, such as filing their return and paying all tax due by March 1 or meeting certain income tax withholding requirements.

Elaboration: According to IRC § 6654(i), farmers who meet the definition of “farmer” are given considerable flexibility in meeting their tax obligations. This flexibility recognizes the seasonal and often unpredictable nature of farming income. Farmers can avoid penalties for failing to make quarterly estimated tax payments if they meet one of the following requirements:

- File and Pay by March 1: Farmers can file their tax return and pay all tax due by March 1 of the following year. This allows them to calculate their income for the entire year and make a single payment, rather than estimating their income quarterly.

- Meet Income Tax Withholding Threshold: Farmers can also avoid penalties if their income tax withholding is at least 66 ⅔% of the total tax shown on their current year tax return or 100% of the total tax shown on their prior year return. This option is particularly useful for farmers who also have income from sources subject to withholding, such as wages or salaries.

These rules can significantly ease the administrative burden on farmers, allowing them to focus on their operations without the added stress of quarterly tax calculations. At income-partners.net, we understand the importance of these provisions and can help you find resources and partners to optimize your tax strategy and take full advantage of available benefits.

2.1. What Are the Options for Farmers to Pay Estimated Taxes?

Farmers have multiple options for fulfilling their estimated tax obligations.

Answer: Farmers can either make a single estimated tax payment by January 15 of the following tax year or file their return and pay all tax due by March 1.

Elaboration: Farmers have two primary options for paying estimated taxes:

-

Single Estimated Tax Payment: Farmers can make a single estimated tax payment by January 15 of the following tax year. This payment must be the smaller of 66 ⅔% of the tax from the current year or 100% of the tax shown on the prior year’s return. This option allows farmers to delay their tax payment until after the end of the tax year, giving them more time to calculate their income and make a single payment.

-

File and Pay by March 1: Farmers can file their tax return and pay all tax due by March 1 of the following year. This option allows farmers to avoid making any estimated tax payments altogether, as long as they file their return and pay their taxes by the March 1 deadline.

These options offer farmers flexibility in managing their tax obligations, allowing them to choose the method that best suits their individual circumstances. At income-partners.net, we can help you find resources and partners to determine the most advantageous tax payment strategy for your farming operation.

2.2. What Happens if a Farmer Misses the March 1 Deadline?

Missing the March 1 deadline can have consequences.

Answer: If a farmer misses the March 1 deadline, they may owe an underpayment of estimated tax penalty.

Elaboration: Farmers who do not pay their required estimated tax by January 15 or file their returns and pay any tax due by March 1 may be subject to an underpayment of estimated tax penalty. This penalty is calculated using Form 2210-F, Underpayment of Estimated Tax by Farmers and Fishermen, which determines the amount owed. It is crucial for farmers to be aware of these deadlines and plan accordingly to avoid potential penalties. income-partners.net provides resources and potential partners to help manage tax obligations and avoid costly mistakes.

3. How is the Underpayment Penalty Calculated for Farmers?

Understanding how the underpayment penalty is calculated can help farmers avoid it.

Answer: The penalty for underpayment of estimated tax equals the amount of the underpayment for the period of underpayment multiplied by the applicable underpayment rate.

Elaboration: The penalty for underpayment of estimated tax is determined by IRC § 6654(a), which states that the penalty equals the amount of the underpayment for the period of underpayment multiplied by the applicable underpayment rate. The underpayment rate is typically three percentage points above the federal short-term interest rate. The IRS determines this rate every quarter, and the rate that applies to a calendar-year qualifying farmer’s underpayment is the rate for the first quarter of the year following the tax year under which the tax liability arose.

For example, the underpayment rate for the first quarter of 2024 was eight percent, up one percent from 2023. This means that farmers who underpaid their estimated taxes in 2023 and paid the underpayment in the first quarter of 2024 would be subject to an eight percent penalty on the underpaid amount. This penalty serves as an interest payment to compensate the government for the delayed tax revenue.

Understanding how this penalty is calculated is crucial for farmers to avoid potential financial burdens. By staying informed about the applicable underpayment rates and planning their tax payments accordingly, farmers can minimize their risk of incurring penalties. income-partners.net can help you find resources and partners to stay up-to-date on tax regulations and optimize your tax strategy.

3.1. What is the Underpayment Rate?

The underpayment rate can fluctuate, so staying informed is essential.

Answer: The underpayment rate is determined by the IRS and is typically three percentage points above the federal short-term interest rate.

Elaboration: The underpayment rate is a key factor in calculating the penalty for underpayment of estimated tax. This rate is determined by the IRS and is typically three percentage points above the federal short-term interest rate, as specified in IRC § 6621(a)(2). The IRS determines this rate every quarter, but the rate that applies to a calendar-year qualifying farmer’s underpayment is the rate for the first quarter of the year following the tax year under which the tax liability arose.

This rate can fluctuate depending on economic conditions, making it essential for farmers to stay informed about the current rate. For example, until April 1, 2022, the underpayment rate was 3%. However, in the first quarter of 2024, this rate was eight percent, up one percent from 2023. These changes highlight the importance of staying current with tax regulations to avoid potential penalties.

Understanding the underpayment rate and its impact on potential penalties is crucial for farmers to manage their tax obligations effectively. income-partners.net can provide access to resources and partners who can help you stay informed about these rates and optimize your tax strategy.

3.2. Example of Underpayment Penalty Calculation

A real-world example can clarify how the underpayment penalty is applied.

Answer: If a qualified farmer, Larry, had a $21,000 tax liability for 2023 but missed the January 16, 2024, deadline to pay estimated taxes, and also missed the March 1 deadline to file his return and pay his taxes, he would owe an underpayment penalty.

Elaboration: Let’s break down the example provided:

Larry is a qualified farmer who did not pay estimated taxes by January 16, 2024, for 2023 (January 15 was a holiday). He also missed the March 1 deadline to file his return and pay his taxes to avoid the underpayment penalty. For 2023, Larry had $21,000 in overall tax liability. As a qualified farmer, his estimated tax liability was 66 ⅔ percent of that amount, or $14,000. The due date for this tax was January 16. He files his return and pays the tax due on April 15, 2024. Because the underpayment rate for the first quarter of 2024 is eight percent, Larry owes an eight percent underpayment penalty for the proportion of the year for which his payment was delinquent, calculated as follows:

$14,000 (estimated tax liability) x 90/365 (days delinquent / days in the year) = $3,452 x .08 (underpayment rate) = $276.

In this scenario, Larry owes $276 in penalties. income-partners.net can help you avoid similar situations by connecting you with tax professionals and providing resources to manage your tax obligations effectively.

4. How Can Farmers Avoid the Underpayment Penalty?

Avoiding penalties requires proactive planning and adherence to deadlines.

Answer: Farmers can avoid the underpayment penalty by filing their return and paying all tax due by March 1, ensuring their income tax withholding meets certain thresholds, or making a single estimated tax payment by January 15.

Elaboration: Farmers have several strategies to avoid the underpayment penalty:

- File and Pay by March 1: By filing their tax return and paying all tax due by March 1, farmers can avoid the need to make estimated tax payments altogether. This option allows them to calculate their income for the entire year and make a single payment, rather than estimating their income quarterly.

- Meet Income Tax Withholding Threshold: Farmers can also avoid penalties if their income tax withholding is at least 66 ⅔% of the total tax shown on their current year tax return or 100% of the total tax shown on their prior year return. This option is particularly useful for farmers who also have income from sources subject to withholding, such as wages or salaries.

- Make a Single Estimated Tax Payment by January 15: Farmers can make a single estimated tax payment by January 15 of the following tax year. This payment must be the smaller of 66 ⅔% of the tax from the current year or 100% of the tax shown on the prior year’s return.

These strategies offer farmers flexibility in managing their tax obligations, allowing them to choose the method that best suits their individual circumstances. At income-partners.net, we can help you find resources and partners to determine the most advantageous tax payment strategy for your farming operation and avoid potential penalties.

4.1. Should Farmers Make Estimated Tax Payments Even if Not Required?

Making estimated tax payments, even when not required, can be a prudent financial strategy.

Answer: Yes, making estimated tax payments can help farmers avoid a large tax bill at the end of the year and manage their cash flow more effectively.

Elaboration: Even if farmers meet the criteria to avoid mandatory estimated tax payments, making voluntary payments can be a wise financial strategy. By making regular payments throughout the year, farmers can:

- Avoid a Large Tax Bill: Making estimated tax payments can prevent a large, unexpected tax bill at the end of the year. This can help farmers manage their cash flow more effectively and avoid potential financial strain.

- Manage Cash Flow: Regular tax payments can help farmers budget and manage their cash flow more predictably. This can be particularly important for farmers with fluctuating income, as it allows them to set aside funds for taxes throughout the year.

- Reduce Potential Penalties: While farmers who meet certain criteria are exempt from mandatory estimated tax payments, making voluntary payments can further reduce the risk of underpayment penalties. By paying taxes throughout the year, farmers can ensure they are meeting their tax obligations and avoid potential penalties.

While making estimated tax payments may require some additional effort, the benefits of avoiding a large tax bill and managing cash flow more effectively can be significant. income-partners.net can connect you with financial advisors and tax professionals who can help you develop a tax payment strategy that aligns with your financial goals.

4.2. What Records Should Farmers Keep for Tax Purposes?

Maintaining thorough records is crucial for accurate tax reporting.

Answer: Farmers should keep records of all income and expenses related to their farming business, including sales receipts, purchase invoices, and bank statements.

Elaboration: Maintaining accurate and complete records is essential for farmers to accurately report their income and expenses and comply with tax regulations. Farmers should keep records of all income and expenses related to their farming business, including:

- Sales Receipts: Records of all sales of crops, livestock, and other farm products.

- Purchase Invoices: Records of all purchases of supplies, equipment, and other inputs used in the farming business.

- Bank Statements: Records of all deposits and withdrawals related to the farming business.

- Expense Records: Documentation of all expenses incurred in the farming business, including labor costs, rent, utilities, and other operating expenses.

- Depreciation Schedules: Records of the depreciation of farm equipment and other assets.

- Inventory Records: Records of the quantity and value of crops, livestock, and other farm products on hand at the beginning and end of the tax year.

Maintaining these records will help farmers accurately calculate their income and expenses, claim all eligible deductions and credits, and comply with tax regulations. income-partners.net can provide access to resources and partners who can help you establish and maintain effective record-keeping practices.

5. What Tax Forms Do Farmers Need to File?

Farmers use specific tax forms to report their income and expenses.

Answer: Farmers typically need to file Schedule F (Form 1040), Profit or Loss From Farming, to report their farm income and expenses, as well as Form 4797 for sales of business property.

Elaboration: Farmers are required to file specific tax forms to report their income and expenses to the IRS. The most common forms include:

-

Schedule F (Form 1040), Profit or Loss From Farming: This form is used to report farm income and expenses. It includes information on sales of crops, livestock, and other farm products, as well as expenses such as labor, rent, and supplies.

-

Form 4797, Sales of Business Property: This form is used to report sales of business property, such as farm equipment and machinery. It includes information on the cost basis, depreciation, and sale price of the property.

In addition to these forms, farmers may also need to file other forms depending on their specific circumstances, such as:

- Form 1040-ES, Estimated Tax for Individuals: This form is used to calculate and pay estimated taxes.

- Form 2210-F, Underpayment of Estimated Tax by Farmers and Fishermen: This form is used to determine and pay any underpayment of estimated tax.

- Schedule SE (Form 1040), Self-Employment Tax: This form is used to calculate self-employment tax, which includes Social Security and Medicare taxes.

It is essential for farmers to understand which forms they need to file and to complete them accurately and on time. income-partners.net can connect you with tax professionals who can help you navigate the complexities of farm tax reporting and ensure compliance with IRS regulations.

5.1. What is Schedule F (Form 1040)?

Schedule F is a key form for reporting farm income and expenses.

Answer: Schedule F (Form 1040) is used by farmers to report their profit or loss from farming activities, including income from sales of crops and livestock, as well as farm-related expenses.

Elaboration: Schedule F (Form 1040) is a crucial tax form for farmers as it allows them to report their profit or loss from farming activities. The form includes detailed sections for reporting:

- Farm Income: This includes income from the sale of crops, livestock, dairy products, poultry, and other farm-related products.

- Farm Expenses: This includes expenses such as labor costs, rent, utilities, repairs, and depreciation of farm assets.

- Net Farm Profit or Loss: This is the difference between farm income and farm expenses. It represents the farmer’s profit or loss from their farming activities.

The information reported on Schedule F is used to calculate the farmer’s taxable income, which is subject to income tax and self-employment tax. This form is essential for farmers to accurately report their financial performance and comply with tax regulations. income-partners.net can provide access to resources and partners who can help you complete Schedule F accurately and optimize your tax strategy.

5.2. What is Form 4797?

Form 4797 is used for reporting sales of business property, including farm equipment.

Answer: Form 4797, Sales of Business Property, is used to report the sale or exchange of business assets, including depreciable property like farm equipment, and helps calculate any gain or loss from these transactions.

Elaboration: Form 4797, Sales of Business Property, is used to report the sale or exchange of business assets, including depreciable property like farm equipment. This form is essential for farmers who sell or exchange assets used in their farming business, as it helps calculate any gain or loss from these transactions.

The form includes detailed sections for reporting:

- Description of Property: This includes a description of the asset being sold or exchanged, such as farm equipment or machinery.

- Date Acquired and Sold: This includes the dates the asset was acquired and sold or exchanged.

- Cost or Basis: This includes the original cost of the asset, as well as any adjustments to the basis, such as depreciation.

- Sales Price: This includes the amount received from the sale or exchange of the asset.

- Gain or Loss: This is the difference between the sales price and the adjusted basis of the asset.

The information reported on Form 4797 is used to calculate the farmer’s taxable income, which is subject to income tax. This form is essential for farmers to accurately report their financial performance and comply with tax regulations. income-partners.net can provide access to resources and partners who can help you complete Form 4797 accurately and optimize your tax strategy.

6. What Tax Deductions and Credits Are Available to Farmers?

Farmers can take advantage of various deductions and credits to reduce their tax liability.

Answer: Farmers can claim various deductions and credits, including deductions for farm expenses, depreciation, and the qualified business income (QBI) deduction, as well as credits for fuel and other eligible expenses.

Elaboration: Farmers can reduce their tax liability by claiming various deductions and credits. Some of the most common deductions and credits available to farmers include:

-

Farm Expenses: Farmers can deduct ordinary and necessary expenses incurred in their farming business, such as labor costs, rent, utilities, repairs, and supplies.

-

Depreciation: Farmers can deduct the depreciation of farm equipment and other assets over their useful life.

-

Qualified Business Income (QBI) Deduction: Farmers who operate their farming business as a pass-through entity, such as a sole proprietorship, partnership, or S corporation, may be eligible for the QBI deduction. This deduction allows them to deduct up to 20% of their qualified business income.

-

Fuel Tax Credit: Farmers can claim a credit for fuel used in their farming operations.

-

Other Eligible Expenses: Farmers may also be eligible for other deductions and credits, such as the deduction for self-employment tax and the credit for increasing research activities.

These deductions and credits can significantly reduce a farmer’s tax liability, allowing them to reinvest in their business and improve their financial stability. income-partners.net can connect you with tax professionals who can help you identify and claim all eligible deductions and credits, maximizing your tax savings.

6.1. What is the Qualified Business Income (QBI) Deduction for Farmers?

The QBI deduction can provide significant tax savings for eligible farmers.

Answer: The Qualified Business Income (QBI) deduction allows eligible farmers to deduct up to 20% of their qualified business income, reducing their overall tax liability.

Elaboration: The Qualified Business Income (QBI) deduction, established by the Tax Cuts and Jobs Act of 2017, allows eligible farmers to deduct up to 20% of their qualified business income. This deduction is available to farmers who operate their farming business as a pass-through entity, such as a sole proprietorship, partnership, or S corporation.

Qualified business income (QBI) is defined as the net amount of income, gains, deductions, and losses from a qualified trade or business. It does not include certain items, such as capital gains or losses, interest income, and wage income. The QBI deduction is subject to certain limitations, depending on the farmer’s taxable income.

The QBI deduction can provide significant tax savings for eligible farmers, reducing their overall tax liability and allowing them to reinvest in their business. income-partners.net can connect you with tax professionals who can help you determine your eligibility for the QBI deduction and maximize your tax savings.

6.2. How Does Depreciation Work for Farm Assets?

Understanding depreciation is essential for managing farm assets and taxes.

Answer: Depreciation allows farmers to deduct a portion of the cost of farm assets, like equipment and buildings, over their useful life, reducing their taxable income.

Elaboration: Depreciation is a key tax deduction for farmers, allowing them to deduct a portion of the cost of farm assets, such as equipment and buildings, over their useful life. This deduction recognizes that assets wear out over time and lose value. Farmers can deduct a portion of the asset’s cost each year, reducing their taxable income.

The amount of depreciation a farmer can deduct each year depends on the asset’s cost, useful life, and depreciation method. The IRS provides guidance on the useful life of various assets, as well as acceptable depreciation methods. Farmers can use the Modified Accelerated Cost Recovery System (MACRS) to calculate depreciation. This system assigns assets to different classes based on their useful life and prescribes specific depreciation methods for each class.

Depreciation can significantly reduce a farmer’s tax liability, allowing them to recover the cost of their assets over time. income-partners.net can connect you with tax professionals who can help you understand depreciation rules and maximize your depreciation deductions.

A farmer inspecting a tractor, highlighting the importance of depreciable farm equipment

A farmer inspecting a tractor, highlighting the importance of depreciable farm equipment

7. What Are the Special Tax Considerations for Farm Partnerships?

Farm partnerships have unique tax considerations.

Answer: Farm partnerships have specific tax rules, including how income and expenses are allocated among partners and the treatment of partnership distributions.

Elaboration: Farm partnerships have unique tax considerations that require careful planning and compliance. Some of the key tax rules for farm partnerships include:

-

Allocation of Income and Expenses: Partnership income and expenses are allocated among the partners according to their partnership agreement. This agreement should clearly outline how income, expenses, and losses are shared among the partners.

-

Partnership Distributions: Distributions from the partnership to the partners are generally not taxable, unless they exceed the partner’s basis in their partnership interest.

-

Self-Employment Tax: Partners are subject to self-employment tax on their share of the partnership’s income.

-

Partnership Tax Return: Partnerships are required to file an annual tax return (Form 1065) to report their income and expenses.

Understanding these rules is essential for farm partnerships to accurately report their income and expenses and comply with tax regulations. income-partners.net can connect you with tax professionals who can help you navigate the complexities of farm partnership taxation and optimize your tax strategy.

7.1. How Are Profits and Losses Divided in a Farm Partnership?

The partnership agreement dictates how profits and losses are shared.

Answer: Profits and losses in a farm partnership are divided among the partners according to the terms outlined in the partnership agreement.

Elaboration: In a farm partnership, the division of profits and losses is a critical aspect that must be clearly defined in the partnership agreement. This agreement serves as the governing document for the partnership and outlines the rights, responsibilities, and obligations of each partner. The allocation of profits and losses is typically based on factors such as:

- Capital Contributions: The amount of capital each partner has contributed to the partnership.

- Services Provided: The value of the services each partner provides to the partnership.

- Management Responsibilities: The level of management responsibilities each partner assumes.

The partnership agreement should specify the percentage or formula used to allocate profits and losses among the partners. This allocation should be based on sound business principles and reflect the relative contributions of each partner. income-partners.net can connect you with legal and financial professionals who can help you draft a comprehensive partnership agreement that addresses these important issues.

7.2. What is a Guaranteed Payment in a Farm Partnership?

Guaranteed payments offer partners a stable income.

Answer: A guaranteed payment in a farm partnership is a payment made to a partner for services or capital, determined without regard to the partnership’s income, and is deductible by the partnership.

Elaboration: A guaranteed payment in a farm partnership is a payment made to a partner for services or capital, determined without regard to the partnership’s income. These payments are treated as if they were made to a non-partner and are deductible by the partnership as a business expense. The partner receiving the guaranteed payment must report it as ordinary income on their individual tax return. Guaranteed payments are often used to compensate partners for their contributions to the partnership, such as management services or the use of their personal assets. income-partners.net can connect you with financial advisors who can help you structure guaranteed payments in a way that benefits both the partnership and the individual partners.

8. How Does the Sale of Farmland Affect Income Taxes?

The sale of farmland can have significant tax implications.

Answer: The sale of farmland can result in capital gains or losses, and may also be subject to depreciation recapture, affecting the seller’s income taxes.

Elaboration: The sale of farmland can have significant tax implications for farmers. When farmland is sold, the seller may realize a capital gain or loss, depending on the difference between the sale price and the adjusted basis of the land. The adjusted basis is typically the original cost of the land, plus any improvements, less any depreciation taken.

If the sale results in a capital gain, the gain may be taxed at either the short-term or long-term capital gains rate, depending on how long the land was held. Short-term capital gains are taxed at the seller’s ordinary income tax rate, while long-term capital gains are taxed at a lower rate. In addition to capital gains, the sale of farmland may also be subject to depreciation recapture. This occurs when the seller has previously deducted depreciation on improvements to the land, such as buildings or fences. The amount of depreciation that is recaptured is taxed as ordinary income.

Understanding these tax implications is essential for farmers considering selling their farmland. income-partners.net can connect you with tax professionals who can help you navigate the complexities of farmland sales and minimize your tax liability.

8.1. What is a 1031 Exchange for Farmland?

A 1031 exchange can defer capital gains taxes on the sale of farmland.

Answer: A 1031 exchange allows farmers to defer capital gains taxes when selling farmland if they reinvest the proceeds into a similar property within a specified timeframe.

Elaboration: A 1031 exchange, also known as a like-kind exchange, is a powerful tax-deferral strategy that allows farmers to postpone paying capital gains taxes when selling farmland. This strategy involves selling farmland and reinvesting the proceeds into a similar property within a specified timeframe. To qualify for a 1031 exchange, the properties must be “like-kind,” meaning they are of the same nature or character, even if they differ in grade or quality. In the context of farmland, this generally means that the replacement property must also be farmland.

The 1031 exchange allows farmers to defer capital gains taxes, providing them with more capital to reinvest in their farming operation. income-partners.net can connect you with real estate and tax professionals who can help you navigate the complexities of 1031 exchanges and ensure compliance with IRS regulations.

8.2. How Does Depreciation Recapture Affect the Sale of Farmland?

Depreciation recapture can increase the tax liability when selling farmland.

Answer: Depreciation recapture occurs when a farmer sells farmland and must pay income tax on the amount of depreciation previously claimed on improvements to the property, such as buildings or fences.

Elaboration: Depreciation recapture is a tax rule that can increase the tax liability when selling farmland. This rule applies when a farmer has previously deducted depreciation on improvements to the land, such as buildings or fences. When the land is sold, the amount of depreciation that was previously deducted is “recaptured” and taxed as ordinary income, rather than capital gains. The depreciation recapture rule is designed to prevent farmers from taking excessive depreciation deductions and then selling the property at a profit, without paying tax on the previously deducted depreciation.

Understanding the depreciation recapture rule is essential for farmers considering selling their farmland. income-partners.net can connect you with tax professionals who can help you calculate the potential depreciation recapture and minimize your tax liability.

9. What Estate Tax Considerations Are There for Farmers?

Estate planning is crucial for farmers to protect their assets.

Answer: Farmers need to consider estate tax implications, including valuation of farm assets, special use valuation, and strategies to minimize estate taxes and ensure a smooth transition of the farm to the next generation.

Elaboration: Estate planning is crucial for farmers to protect their assets and ensure a smooth transition of the farm to the next generation. Estate tax is a tax on the transfer of assets from a deceased person to their heirs. Farmers need to consider the following estate tax implications:

- Valuation of Farm Assets: Farm assets, such as land, equipment, and livestock, must be valued for estate tax purposes.

- Special Use Valuation: Farmers may be able to use special use valuation to reduce the value of their farmland for estate tax purposes.

- Strategies to Minimize Estate Taxes: Farmers can use various strategies to minimize estate taxes, such as gifting assets to heirs during their lifetime, establishing trusts, and purchasing life insurance.

These considerations are essential for farmers to minimize estate taxes and ensure a smooth transition of the farm to the next generation. income-partners.net can connect you with estate planning attorneys and financial advisors who can help you develop a comprehensive estate plan that meets your specific needs.

9.1. What is Special Use Valuation for Farmland?

Special use valuation can reduce estate taxes on farmland.

Answer: Special use valuation allows qualified farmers to value their farmland at its agricultural value, rather than its fair market value, potentially reducing estate taxes.

Elaboration: Special use valuation is a provision in the tax law that allows qualified farmers to value their farmland at its agricultural value, rather than its fair market value, for estate tax purposes. This can significantly reduce the value of the farmer’s estate and, as a result, reduce the amount of estate tax owed. To qualify for special use valuation, the following requirements must be met:

- Qualified Heir: The property must pass to a qualified heir, such as a family member who will continue to operate the farm.

- Material Participation: The farmer or a member of their family must have materially participated in the operation of the farm for a specified period of time.

- Percentage Requirements: The value of the farmland must meet certain percentage requirements relative to the total value of the estate.

Special use valuation can be a valuable tool for farmers to reduce estate taxes and ensure the continued operation of the farm by future generations. income-partners.net can connect you with estate planning attorneys and financial advisors who can help you determine your eligibility for special use valuation and navigate the complexities of estate planning.

9.2. How Can Farmers Plan for Estate Taxes?

Proactive planning is essential to minimize estate tax burdens.

Answer: Farmers can plan for estate taxes by using strategies like gifting assets, establishing trusts, and purchasing life insurance to minimize their estate tax liability and ensure a smooth transfer of their farm.

Elaboration: Planning for estate taxes is crucial for farmers to protect their assets and ensure a smooth transition of the farm to the next generation. Some effective strategies for estate tax planning include:

-

Gifting Assets: Farmers can gift assets, such as farmland or equipment, to their heirs during their lifetime. This can reduce the value of their estate and potentially lower estate taxes.

-

Establishing Trusts: Farmers can establish trusts to hold assets and control their distribution to heirs. Trusts can also provide creditor protection and other benefits.

-

Purchasing Life Insurance: Farmers can purchase life insurance to provide funds to pay estate taxes or to provide income for their heirs.

By implementing these strategies, farmers can minimize their estate tax liability and ensure that their farm is passed on to the next generation in a financially secure manner. income-partners.net can connect you with estate planning attorneys and financial advisors who can help you develop a comprehensive estate plan that meets your specific needs.

10. Where Can Farmers Find Help with Income Taxes?

Farmers have several resources available to help them with income taxes.

Answer: Farmers can find help with income taxes from various sources, including tax professionals, government agencies like the IRS, and online resources, ensuring they comply with tax laws and optimize their financial strategies.

Elaboration: Farmers have several resources available to help them navigate the complexities of income taxes and ensure compliance with tax regulations. Some of the most helpful resources include:

- Tax Professionals: Tax professionals, such as certified public accountants (CPAs) and enrolled agents, can provide expert advice and assistance with tax planning, preparation, and filing.

- Government Agencies: The IRS offers a variety of resources for farmers, including publications, online tools, and workshops.

- Online Resources: Many websites and online forums provide information and advice on farm taxes.

By utilizing these resources, farmers can stay informed about tax regulations, optimize their tax strategies, and avoid potential penalties. income-partners.net can connect you with tax professionals and provide access to valuable online resources to help you manage your farm taxes effectively.

10.1. How Can a Tax Professional Help Farmers?

Tax professionals offer expertise and tailored advice.

Answer: A tax professional can help farmers