Does Dividend Income Affect Social Security Benefits? Absolutely, it’s essential to understand how dividend income interacts with your Social Security benefits to maximize your retirement income. At income-partners.net, we help you navigate the complexities of income strategies, including understanding how unearned income, retirement income, and passive income can affect your financial future and Social Security payouts. Let’s dive into how dividends can play a role in your overall benefits.

1. Understanding Social Security Benefit Calculation

Social Security benefits are calculated based on your earnings history.

How are Social Security benefits determined? Social Security benefits are primarily determined by two key factors: your average lifetime earnings and the age at which you start claiming benefits. Your average indexed monthly earnings (AIME) over your 35 highest-earning years is used to calculate your primary insurance amount (PIA), which is the benefit you’d receive at your full retirement age. Remember, dividend income doesn’t directly contribute to your AIME.

1.1. Earnings and the Primary Insurance Amount (PIA)

The Social Security Administration (SSA) calculates your benefit based on your highest 35 years of earnings.

How does the Social Security system determine my primary insurance amount (PIA)? The Social Security system uses a formula that looks at your average inflation-adjusted earnings over your 35 highest earning years to determine your primary insurance amount (PIA). Your PIA is the foundation upon which your Social Security benefits are built. It is the amount you would receive if you start receiving retirement payouts at your normal (full) retirement age. According to research from the University of Texas at Austin’s McCombs School of Business, understanding this calculation is critical for retirement planning, ensuring you optimize your earnings years to maximize your PIA.

1.2. Full Retirement Age: What You Need to Know

Your full retirement age is the age at which you are entitled to full Social Security benefits.

What is the full retirement age, and how does it impact my Social Security benefits? The full retirement age is the age at which you are entitled to full Social Security benefits. It varies based on your birth year. For those born between 1943 and 1954, it’s 66. For those born in 1960 or later, it’s 67. Claiming benefits before this age reduces your monthly payment, while delaying it increases your benefits.

Here’s a breakdown of full retirement ages:

| Year of Birth | Full Retirement Age |

|---|---|

| 1937 or before | 65 |

| 1938 to 1942 | 65 and 2-10 months |

| 1943 to 1954 | 66 |

| 1955 to 1959 | 66 and 2-10 months |

| 1960 or later | 67 |

1.3. Early vs. Delayed Retirement: Maximizing Your Benefits

Claiming Social Security before or after your full retirement age can significantly impact your benefit amount.

What are the implications of claiming Social Security benefits early or delaying them? Claiming early, as early as age 62, reduces your benefits by up to 30%. Delaying until age 70 can increase your benefits by up to 24-32% beyond your full retirement age amount.

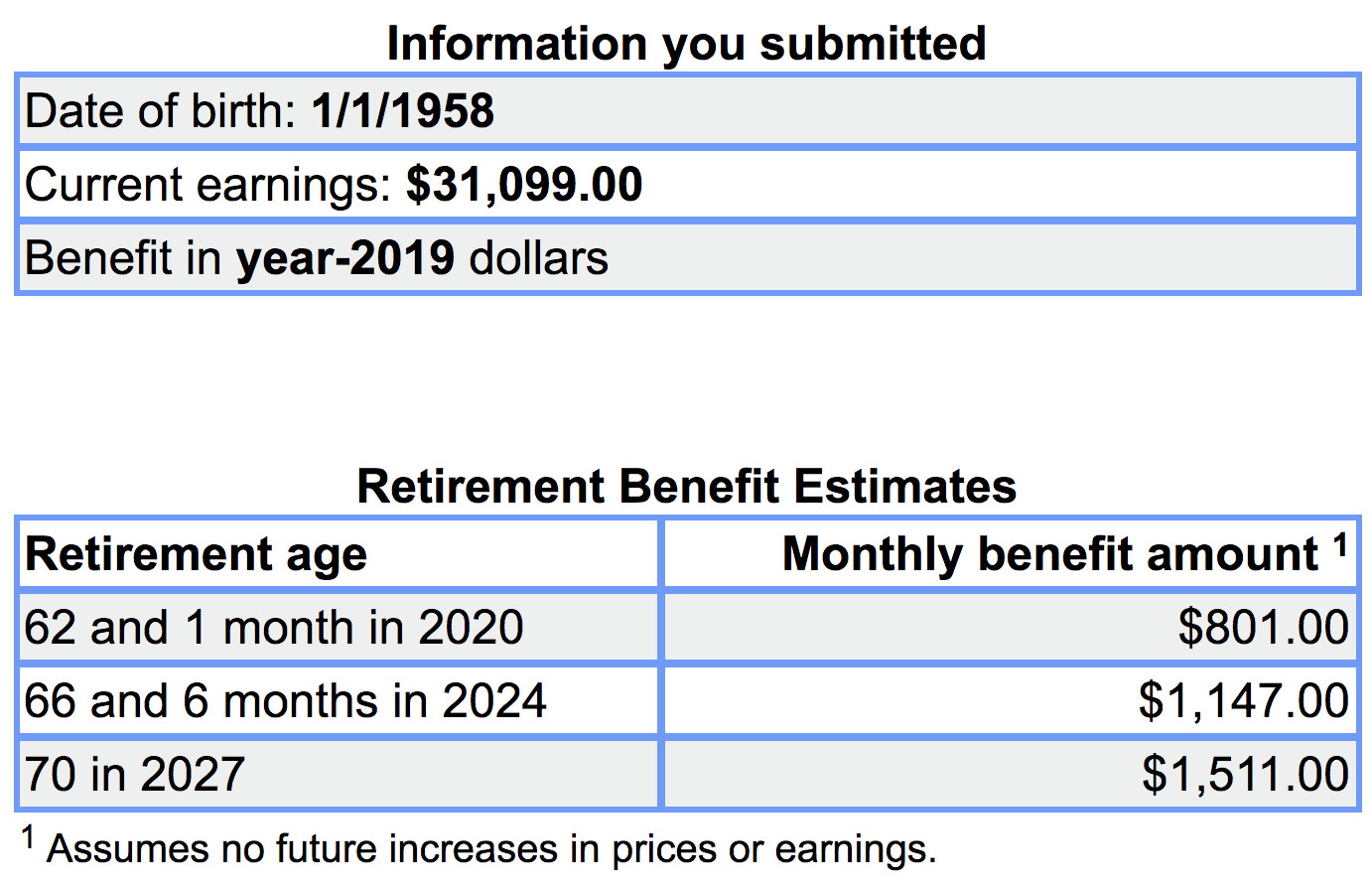

For example, consider someone born on January 1, 1958, with a median U.S. income of $31,099. If they worked until their full retirement age (66 and 6 months) in 2024, they would receive $1,147 per month. However, claiming at 62 would reduce this to $801. Waiting until 70 would increase it substantially.

Social Security benefit estimator example showing reduced payments for early retirement

Social Security benefit estimator example showing reduced payments for early retirement

1.4. Maximizing Social Security: Strategies for Higher Earners

Higher earners need to be aware of the maximum benefit amount and how their income affects it.

What is the maximum Social Security benefit, and how can high earners maximize their payments? For 2019, the maximum monthly benefit at full retirement age was $2,861. This assumes your earnings were at or above the maximum taxable amount each year ($132,900 in 2019). To maximize your benefits, ensure you work and earn at or above this cap for at least 35 years.

1.5. Social Security as Part of Retirement Income

Social Security is an essential, but often insufficient, part of retirement income.

How significant is Social Security in covering retirement expenses? Social Security benefits were not designed to completely replace one’s working income. Even maxing out benefits may not provide sufficient funds for retirement. For instance, the average monthly benefit for retired workers in December 2018 was $1,461, or $17,532 per year. This only covers a portion of the average household’s annual expenses.

According to the Social Security Administration, benefits only represent about 33% of the income of the elderly. The rest needs to come from other sources, like dividends, pensions, and savings. The average household run by someone 65 or older spends about $49,542 per year. Even a couple maximizing their benefits by delaying until age 70 would only receive $36,264, or 73% of their expenses.

2. The Direct Impact of Dividends on Social Security

While dividends won’t directly reduce your Social Security benefits, they can indirectly affect your net benefits through taxes.

How do dividends directly affect my Social Security benefits? Dividends do not directly reduce your gross Social Security benefits. This is because Social Security benefits are primarily based on your earned income history and the age at which you claim benefits. However, dividends can influence the taxation of your benefits.

2.1. Earnings Limits and Social Security

An earnings limit can reduce your benefits if you claim them before your full retirement age.

What earnings limits apply to Social Security benefits, and how do they work? If you claim Social Security benefits before your full retirement age and continue to work, an earnings limit applies. In 2019, this limit was $17,040 per year. If you exceed this limit, your benefits are reduced by $1 for every $2 earned above it. This limit does not include investment income, pensions, or capital gains.

Remember, according to Entrepreneur.com, once you reach full retirement age, this penalty disappears, and you can earn as much as you want without affecting your benefits.

2.2. What Counts as Earnings?

Understanding what counts as earnings is critical for managing your benefits.

What types of income are considered “earnings” for Social Security purposes? Earnings include wages and net earnings from self-employment, along with bonuses, commissions, and severance pay. They do not include investment income such as dividends, capital gains, pensions, or inheritances. Thus, dividends and capital gains won’t negatively affect your Social Security benefits directly, even if you decide to file earlier than your full retirement age.

2.3. Dividends and Capital Gains: The Good News

The good news is that dividends and capital gains do not directly reduce your Social Security benefits.

Are dividends and capital gains considered “earnings” that reduce my Social Security benefits? No, dividends and capital gains are not considered “earnings” for Social Security reduction purposes. They do not directly reduce your Social Security benefits, making them an attractive source of income in retirement. This means you can receive dividend income without worrying about an immediate reduction in your benefits.

3. The Indirect Impact: Taxation of Social Security Benefits

Dividends can indirectly affect your Social Security benefits through taxation.

How can dividend income indirectly impact my Social Security benefits? Dividend income can indirectly affect your Social Security benefits due to the taxation of those benefits. Up to 85% of your Social Security benefits may be taxable at the federal level, based on your combined income, which includes adjusted gross income (AGI), nontaxable interest, and half of your Social Security benefits.

3.1. Understanding Combined Income

Your combined income determines how much of your Social Security benefits are taxable.

What is “combined income,” and how does it affect the taxation of my Social Security benefits? Combined income is calculated as your adjusted gross income (AGI) plus nontaxable interest plus half of your Social Security benefits. The higher your combined income, the more of your Social Security benefits may be subject to federal income tax.

Here’s a breakdown of how much of your benefits can be taxed based on your combined income:

| Filing Status | Combined Income | Percentage of Benefits Taxable |

|---|---|---|

| Single | $25,000 to $34,000 | Up to 50% |

| Married Filing Jointly | $32,000 to $44,000 | Up to 50% |

| Single | Above $34,000 | Up to 85% |

| Married Filing Jointly | Above $44,000 | Up to 85% |

3.2. Adjusted Gross Income (AGI) and Dividends

Dividends are included in your adjusted gross income (AGI), which can affect the taxation of your benefits.

How does adjusted gross income (AGI) factor into the taxation of Social Security benefits, and how do dividends affect my AGI? Adjusted gross income (AGI) is your total income minus certain deductions. Unfortunately, capital gains and dividends are included in your AGI figure and thus count in your combined income calculation. This means that dividends can increase the amount of your Social Security benefits that are subject to federal income tax.

3.3. Qualified vs. Ordinary Dividends: Tax Implications

Qualified dividends have more favorable tax rates than ordinary dividends.

What is the difference between qualified and ordinary dividends, and how are they taxed? Qualified dividends are taxed at the long-term capital gains rate, which is generally lower than the ordinary income tax rate. Ordinary dividends are taxed at your marginal income tax rate. Despite these differences, both qualified and ordinary dividends are included in your AGI and can affect the taxation of your Social Security benefits.

Following tax reform, the long-term capital gain rates look like this for different filers and taxable income levels:

| Taxable Income | Single Filers | Married Filing Jointly | Rate |

|---|---|---|---|

| $0 to $40,000 | $0 to $80,000 | 0% | |

| $40,001 to $441,450 | $80,001 to $496,600 | 15% | |

| Over $441,450 | Over $496,600 | 20% |

3.4. Strategies to Minimize Taxes on Social Security

Strategic planning can help minimize the taxes you pay on your Social Security benefits.

What strategies can I use to minimize the tax impact of dividends on my Social Security benefits? Strategies to minimize taxes on Social Security benefits include managing your dividend income to stay below the combined income thresholds, using tax-advantaged accounts, and taking advantage of deductions. For example, a married couple could generate up to $80,000 of taxable income and pay 0% federal taxes on their qualified dividends. However, exceeding the Social Security benefits combined income limit of $44,000 for couples would mean that 85% of their Social Security benefits would be classified as taxable income.

A standard deduction can help reduce their taxable income. The table below shows the marginal income tax rates this couple would face at the federal level.

Tax rates table for married couples

Tax rates table for married couples

3.5. Retirement Accounts and Required Minimum Distributions (RMDs)

RMDs from retirement accounts can also impact the taxation of your benefits.

How do required minimum distributions (RMDs) from retirement accounts affect the taxation of my Social Security benefits? Required Minimum Distributions (RMDs) from retirement accounts, such as IRAs or 401(k)s, are included in your AGI and thus your combined income calculation. This means that RMDs can increase the amount of your Social Security benefits that are subject to federal income tax. Planning for RMDs is essential to manage your tax liability in retirement.

4. State Taxes on Social Security Benefits

Some states also tax Social Security benefits, which can further affect your net income.

Do any states tax Social Security benefits, and how do these taxes vary? Yes, 13 states tax Social Security benefits: Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont, and West Virginia. The way these states tax benefits varies significantly. For example, Vermont uses the same rules as the federal government, while Connecticut only taxes benefits for individuals and married couples earning at least $50,000 or $60,000, respectively.

4.1. State-Specific Rules

Understanding the rules in your state is crucial for effective retirement planning.

Where can I find specific information about how my state taxes Social Security benefits? If you live in one of these states, make sure you check how your benefits will be taxed and what potential AGI limits should be kept in mind. Contact your state’s tax agency or consult with a tax professional to understand the specific rules that apply to you.

5. Building a Dividend Growth Portfolio for Retirement

A well-constructed dividend growth portfolio can provide a steady income stream in retirement.

How can I build a dividend growth portfolio to supplement my Social Security benefits in retirement? Building a dividend growth portfolio involves investing in companies with a history of consistently increasing their dividend payouts. This can provide a growing income stream that supplements your Social Security benefits, helping you maintain your standard of living in retirement.

5.1. Benefits of Dividend Growth Investing

Dividend growth investing offers several benefits, including a steady income stream and potential capital appreciation.

What are the key benefits of dividend growth investing for retirees? Dividend growth investing provides a steady, growing income stream, potential capital appreciation, and diversification benefits. It can also offer a hedge against inflation, as companies tend to increase dividends over time.

5.2. Tax-Advantaged Investing

Using tax-advantaged accounts can help minimize the tax impact of your dividend income.

How can I use tax-advantaged accounts to minimize taxes on my dividend income? Tax-advantaged accounts, such as 401(k)s and IRAs, can help minimize the tax impact of your dividend income. Contributions to these accounts may be tax-deductible, and earnings grow tax-deferred. Additionally, Roth accounts offer tax-free withdrawals in retirement, which can further reduce your tax liability.

5.3. Income-Partners.Net: Your Resource for Partnership Opportunities

At income-partners.net, we provide resources and opportunities to enhance your income strategies.

How can income-partners.net help me find partnership opportunities to increase my income? At income-partners.net, we provide a variety of resources and opportunities to help you enhance your income strategies, including dividend growth investing. We offer insights, tools, and connections to help you build a robust portfolio and achieve your financial goals. Consider us your partners in income.

6. Case Studies: Real-Life Examples

Real-life examples can illustrate how dividends and Social Security interact.

Can you provide examples of how dividend income affects Social Security benefits in different scenarios? Let’s consider a couple of scenarios. First, imagine a retiree earning $30,000 annually from dividends and receiving $20,000 in Social Security benefits. Their combined income would be $40,000, meaning up to 50% of their Social Security benefits could be taxable. Now, consider another retiree with $15,000 in dividend income and $20,000 in Social Security benefits. Their combined income would be $25,000, potentially reducing the taxable portion of their Social Security benefits.

6.1. Maximizing Income with Dividends

Understanding how to maximize income with dividends can improve your financial security.

How can I maximize my income using dividends while minimizing the impact on my Social Security benefits? Maximizing income with dividends while minimizing the impact on your Social Security benefits involves strategic planning. This includes using tax-advantaged accounts, managing your AGI, and understanding the state tax rules. Additionally, partnering with platforms like income-partners.net can provide access to additional resources and opportunities to enhance your income strategies.

7. Retirement Planning Tools

Helpful tools can make retirement planning easier.

What tools and resources are available to help me plan for retirement and understand the interaction between dividend income and Social Security benefits? Several tools and resources are available to help you plan for retirement. These include Social Security benefit estimators, tax calculators, and financial planning software. Additionally, consulting with a financial advisor can provide personalized guidance based on your specific circumstances.

7.1. Online Calculators and Estimators

Online calculators and estimators can help you project your Social Security benefits and estimate your tax liability.

Where can I find online calculators and estimators to help me project my Social Security benefits and estimate my tax liability? The Social Security Administration (SSA) website offers a benefits calculator to estimate your future benefits. Additionally, many financial websites provide tax calculators to estimate your tax liability based on your income and deductions.

7.2. Consulting with a Financial Advisor

A financial advisor can provide personalized guidance based on your specific circumstances.

When should I consider consulting with a financial advisor to discuss my retirement plan? Consulting with a financial advisor can be beneficial at any stage of your career, but it’s particularly important as you approach retirement. A financial advisor can help you develop a comprehensive retirement plan, understand the interaction between dividend income and Social Security benefits, and make informed decisions to achieve your financial goals.

8. Conclusion: Dividends and Social Security Benefits

Understanding the relationship between dividends and Social Security benefits is key to a secure retirement.

What are the key takeaways regarding how dividend income affects Social Security benefits? Dividends and capital gains won’t reduce your gross benefits. However, both dividends and capital gains can affect how your Social Security benefits get taxed and thus impact your net benefits. Social Security was not designed to provide sufficient income during retirement, but be supplemented by other sources of income or private savings.

8.1. Maximizing Your Retirement Income

Strategic planning can help you maximize your retirement income.

What steps can I take now to maximize my retirement income and ensure financial security? To maximize your retirement income and ensure financial security, start by understanding the rules governing Social Security benefits and how dividend income affects them. Next, develop a diversified investment strategy that includes dividend growth stocks and other income-producing assets. Finally, seek professional guidance from a financial advisor and leverage resources like income-partners.net to make informed decisions.

At income-partners.net, we’re committed to helping you navigate the complexities of retirement planning. We provide the resources and opportunities you need to build a secure financial future. Explore our website today to discover how we can help you achieve your retirement goals.

9. Frequently Asked Questions (FAQs)

9.1. Will receiving dividends reduce my Social Security benefits directly?

No, dividends do not directly reduce your Social Security benefits. Social Security benefits are based on your earnings history and the age at which you claim benefits.

9.2. How do dividends affect the taxation of my Social Security benefits?

Dividends are included in your adjusted gross income (AGI), which is part of the combined income used to determine how much of your Social Security benefits are taxable.

9.3. What is “combined income” for Social Security purposes?

Combined income is your adjusted gross income (AGI) plus nontaxable interest plus half of your Social Security benefits.

9.4. Are qualified dividends taxed differently than ordinary dividends?

Yes, qualified dividends are taxed at the long-term capital gains rate, which is generally lower than the ordinary income tax rate. However, both are included in your AGI.

9.5. What are Required Minimum Distributions (RMDs), and how do they affect my Social Security benefits?

RMDs are withdrawals you must take from certain retirement accounts after age 70 ½ (or 73, depending on your birth year). They are included in your AGI and can increase the taxable portion of your Social Security benefits.

9.6. Which states tax Social Security benefits?

Thirteen states tax Social Security benefits: Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont, and West Virginia.

9.7. Can I avoid paying taxes on my Social Security benefits?

You may be able to reduce the amount of taxes you pay on your Social Security benefits by managing your income and taking advantage of deductions and tax credits.

9.8. What is the earnings limit for Social Security if I claim benefits before full retirement age?

In 2019, the earnings limit was $17,040 per year. If you exceed this limit, your benefits are reduced by $1 for every $2 earned above it.

9.9. How can a financial advisor help me with retirement planning and Social Security?

A financial advisor can provide personalized guidance, help you develop a comprehensive retirement plan, and make informed decisions about Social Security and investments.

9.10. Where can I find more information about Social Security benefits and retirement planning?

You can find more information on the Social Security Administration (SSA) website, financial websites, and through resources like income-partners.net.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

By understanding the relationship between dividend income and Social Security benefits, you can make informed decisions to maximize your retirement income and financial security. Whether you’re just starting to plan for retirement or are already enjoying your golden years, strategic planning and informed decision-making can help you achieve your financial goals.