Does Dividend Income Affect Social Security benefits? Yes, while dividend income doesn’t directly reduce your Social Security benefits, it can influence how much of your benefits are subject to federal and potentially state taxes, impacting your net income. At income-partners.net, we help you navigate these complexities to optimize your retirement income strategy. We’ll explore how dividends interact with Social Security, offering insights into maximizing your returns through strategic partnership and financial planning, dividend taxation, and income optimization.

1. How Are Social Security Benefits Determined?

The amount you receive in monthly Social Security benefits depends primarily on your earnings history and the age at which you begin claiming benefits. Let’s break it down.

-

Earnings History: Social Security calculates your benefits using your average indexed monthly earnings (AIME) over your 35 highest-earning years.

-

Retirement Age: Your “full retirement age” (FRA) is crucial, as claiming benefits before this age results in a reduction.

- For those born in 1960 or later, the full retirement age is 67.

- Claiming benefits at age 62 can result in a reduction of up to 30%.

-

Primary Insurance Amount (PIA): This is the benefit you’d receive at your full retirement age, calculated based on your AIME.

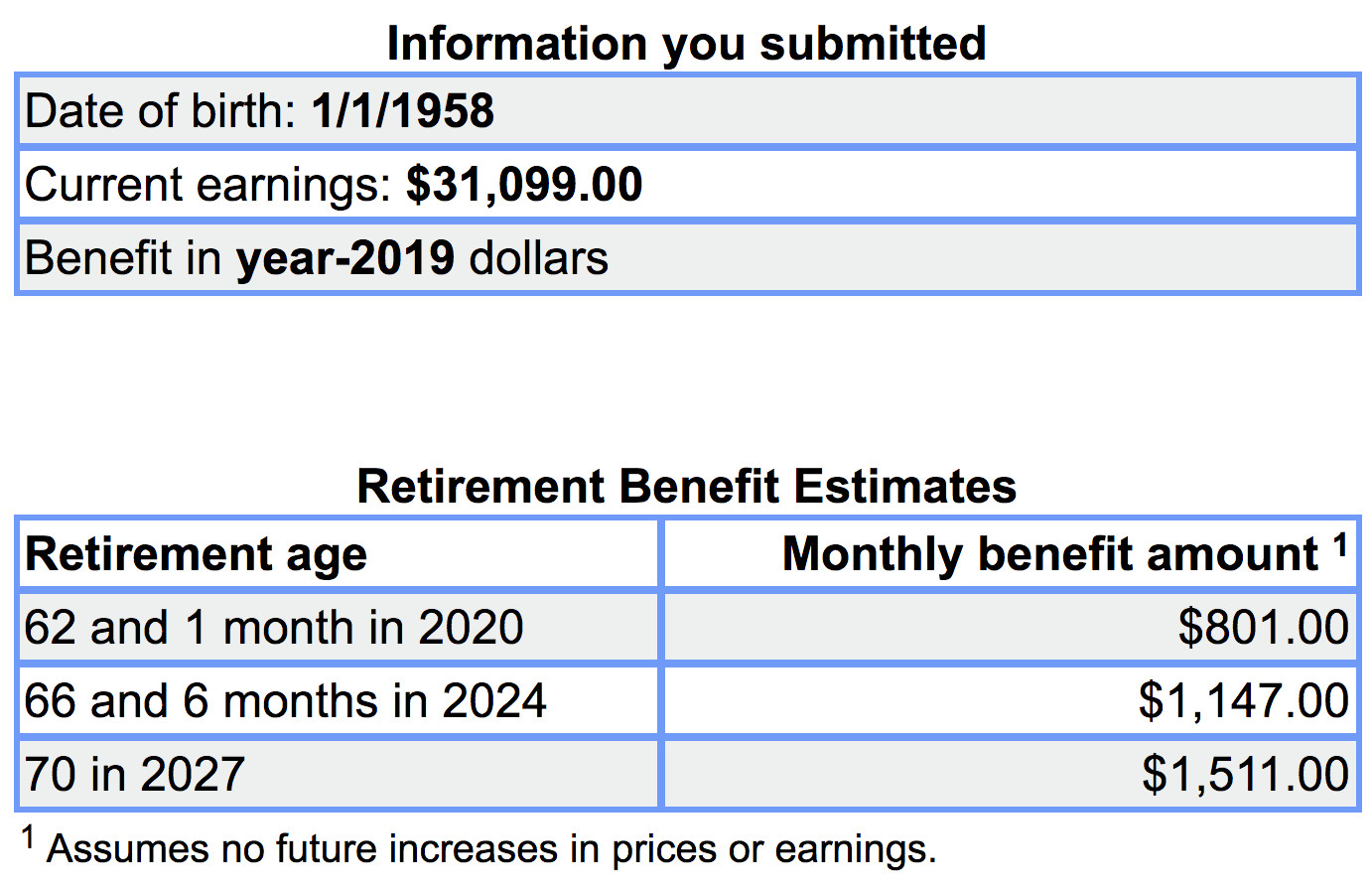

- For example, someone with a consistent median U.S. income might receive around $1,147 per month at full retirement age.

The Social Security Administration emphasizes that benefits are designed to supplement, not replace, your pre-retirement income. Many retirees rely on additional income sources, such as pensions and investments, to meet their expenses. According to the Social Security Administration, nearly nine out of ten individuals age 65 and older receive Social Security benefits.

Social Security Benefits Calculator

Social Security Benefits Calculator

2. How Dividends Interact with Social Security Benefits

While dividend income doesn’t directly reduce your Social Security benefits, it can impact the amount of your benefits subject to taxation. Here’s how:

- Earnings Limit Before Full Retirement Age: If you claim Social Security benefits before your full retirement age and continue to work, an earnings limit applies. In 2019, this limit was $17,040 per year. Exceeding this limit reduces your benefits by $1 for every $2 earned above it. However, this limit only applies to work-related income (wages or self-employment).

- Dividends Don’t Count Against Earnings Limit: Importantly, investment income, including dividends, does not count toward this earnings limit. You can receive dividend income without directly affecting your Social Security benefits.

3. Understanding Taxes on Social Security Benefits

Dividend and capital gains income can indirectly affect your Social Security benefits due to federal income taxes. Up to 85% of your Social Security benefits may be taxable, depending on your combined income.

-

Combined Income Calculation:

- Combined Income = Adjusted Gross Income (AGI) + Nontaxable Interest + Half of Your Social Security Benefits

-

Taxability Thresholds:

-

Single Filers:

- $25,000 – $34,000 combined income: up to 50% of benefits taxable

- Above $34,000 combined income: up to 85% of benefits taxable

-

Married Filing Jointly:

- $32,000 – $44,000 combined income: up to 50% of benefits taxable

- Above $44,000 combined income: up to 85% of benefits taxable

-

Example Scenario:

Let’s say a married couple has an adjusted gross income (AGI) of $40,000, receives $20,000 in Social Security benefits, and has no nontaxable interest. Their combined income would be calculated as:

Combined Income = $40,000 (AGI) + $0 (Nontaxable Interest) + ($20,000 / 2) = $50,000

Since their combined income exceeds $44,000, up to 85% of their Social Security benefits could be taxable.

- Impact of Dividends: Dividends are included in your adjusted gross income (AGI), which impacts your combined income calculation. Higher dividend income can increase the amount of your Social Security benefits subject to federal tax.

4. Tax Advantages of Qualified Dividends

Qualified dividends are taxed at lower long-term capital gains rates, providing a tax-efficient income source. The rates are as follows:

| Taxable Income (Single Filers) | Taxable Income (Married Filing Jointly) | Long-Term Capital Gains Rate |

|---|---|---|

| Up to $40,400 | Up to $80,800 | 0% |

| $40,401 to $445,850 | $80,801 to $501,600 | 15% |

| Over $445,850 | Over $501,600 | 20% |

For instance, a married couple could earn up to $80,800 in taxable income and pay 0% federal taxes on their qualified dividends.

5. State Taxes on Social Security Benefits

It’s essential to be aware of state taxes on Social Security benefits. Thirteen states currently tax these benefits, but the rules vary significantly:

-

States That Tax Social Security Benefits:

- Colorado

- Connecticut

- Kansas

- Minnesota

- Missouri

- Montana

- Nebraska

- New Mexico

- North Dakota

- Rhode Island

- Utah

- Vermont

- West Virginia

-

Variations in State Rules:

- Vermont follows federal rules.

- Connecticut only taxes benefits for individuals earning above $75,000 and couples earning above $100,000.

If you reside in one of these states, understand the specific rules and income limits to optimize your tax planning.

6. Strategic Dividend Investing for Retirement

Effective retirement planning involves maximizing income while minimizing taxes. Here’s how to strategically use dividend investing:

- Maximize Tax-Advantaged Accounts: Utilize 401(k)s, IRAs, and Roth accounts to shield investments from current taxes.

- Tax-Efficient Portfolio Allocation: Hold dividend-paying stocks in taxable accounts, and growth stocks in tax-advantaged accounts.

- Dividend Reinvestment: Reinvest dividends in tax-advantaged accounts to grow your investments without immediate tax implications.

- Tax-Loss Harvesting: Offset capital gains with investment losses to reduce your overall tax liability.

- Consult a Financial Advisor: Work with a financial advisor to create a personalized tax and investment strategy tailored to your retirement goals.

7. Integrating Dividends with Social Security: Key Strategies

Several strategies can help you effectively integrate dividend income with Social Security benefits:

- Delay Social Security: Waiting to claim Social Security increases your monthly benefit, potentially offsetting the impact of taxes on dividend income.

- Manage AGI: Control your adjusted gross income (AGI) by strategically timing dividend income and other taxable events.

- Utilize Retirement Accounts: Maximize contributions to tax-deferred accounts to reduce your taxable income in retirement.

- Consider Roth Conversions: Convert traditional IRA funds to a Roth IRA to pay taxes upfront and enjoy tax-free withdrawals in retirement.

- Diversify Income Sources: Diversify your income with pensions, annuities, and other sources to reduce reliance on dividends and Social Security.

8. Real-Life Examples of Successful Dividend and Social Security Integration

Let’s consider a few examples:

Example 1: The Early Retiree

- Situation: John retires at 62, claiming Social Security early. He also has a substantial dividend income from his investment portfolio.

- Strategy: John manages his part-time work income to stay below the earnings limit while strategically using tax-advantaged accounts to reduce his AGI.

- Outcome: John enjoys a comfortable retirement, supplementing his reduced Social Security benefits with tax-efficient dividend income.

Example 2: The Delayed Gratification Planner

- Situation: Mary delays claiming Social Security until age 70, maximizing her monthly benefit. She also has a significant dividend income.

- Strategy: Mary benefits from a higher Social Security payment, offsetting the impact of taxes on her dividend income. She also uses tax-loss harvesting to manage her AGI.

- Outcome: Mary enjoys a secure retirement with a substantial, inflation-protected income stream.

Example 3: The State Tax Strategist

- Situation: Tom lives in a state that taxes Social Security benefits. He has a moderate dividend income.

- Strategy: Tom plans his income to stay below the state’s income threshold for taxing Social Security benefits. He also uses municipal bonds to generate tax-free income.

- Outcome: Tom minimizes his state tax liability, maximizing his after-tax retirement income.

9. Latest Trends and Opportunities in Partnership and Dividend Investing

Staying informed about current trends can help you optimize your strategies:

- ESG Investing: Environmental, Social, and Governance (ESG) factors are increasingly important for dividend investors. Consider companies with strong ESG profiles for sustainable long-term returns.

- Real Estate Investment Trusts (REITs): REITs offer attractive dividend yields and can diversify your portfolio.

- Master Limited Partnerships (MLPs): MLPs in the energy sector can provide high dividend income but be mindful of the tax implications.

- Dividend Growth Stocks: Focus on companies with a history of increasing dividends, offering both income and capital appreciation potential.

10. Navigating Retirement Income Challenges

Retirement planning involves addressing several key challenges:

- Longevity Risk: Planning for a longer lifespan requires a sustainable income strategy.

- Inflation: Protecting your income from inflation is crucial for maintaining your living standards.

- Healthcare Costs: Budgeting for healthcare expenses is a significant consideration in retirement.

- Market Volatility: Managing market risk is essential for preserving your investment portfolio.

Working with a financial advisor can help you navigate these challenges and create a comprehensive retirement plan.

Social Security provides a crucial foundation for retirement income, but strategic dividend investing can enhance your financial security. Understanding the interplay between dividend income and Social Security benefits, along with effective tax planning, empowers you to optimize your retirement income. At income-partners.net, we offer resources and partnerships to help you achieve your retirement goals.

Remember, dividend and capital gains won’t reduce your gross benefits; however, both dividends and capital gains can affect how your Social Security benefits get taxed and thus impact your net benefits.

Ultimately, remember that Social Security was not designed to provide sufficient income during retirement, but be supplemented by other sources of income or private savings. A quality dividend growth portfolio can serve as an attractive foundation from which to generate a steady and growing income stream in retirement.

For further assistance and personalized advice, contact us at:

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net.

Retirement Planning Strategy

Retirement Planning Strategy

FAQ: Dividend Income and Social Security Benefits

Here are some frequently asked questions:

1. Do dividends directly reduce my Social Security benefits?

No, dividend income does not directly reduce your Social Security benefits. However, it can impact the amount of your benefits subject to federal and state income taxes.

2. How does dividend income affect the taxation of my Social Security benefits?

Dividend income is included in your adjusted gross income (AGI), which is used to calculate your combined income. A higher combined income can increase the amount of your Social Security benefits subject to taxation.

3. What is “combined income” for Social Security purposes?

Combined income is calculated as adjusted gross income (AGI) plus nontaxable interest plus half of your Social Security benefits.

4. What are the income thresholds for taxing Social Security benefits?

For single filers, up to 50% of benefits are taxable if combined income is between $25,000 and $34,000, and up to 85% is taxable if combined income exceeds $34,000. For married couples filing jointly, up to 50% of benefits are taxable if combined income is between $32,000 and $44,000, and up to 85% is taxable if combined income exceeds $44,000.

5. Are qualified dividends taxed differently than ordinary income?

Yes, qualified dividends are taxed at lower long-term capital gains rates, which can be more tax-efficient than ordinary income rates.

6. How can I minimize the impact of dividend income on my Social Security benefits?

Strategies include maximizing tax-advantaged accounts, managing your AGI, utilizing tax-loss harvesting, and consulting a financial advisor.

7. Does the earnings limit before full retirement age include dividend income?

No, the earnings limit before full retirement age only applies to work-related income (wages or self-employment) and does not include investment income like dividends.

8. Which states tax Social Security benefits?

The states that tax Social Security benefits include Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont, and West Virginia.

9. How do Required Minimum Distributions (RMDs) affect my Social Security benefits?

Required Minimum Distributions (RMDs) from retirement accounts are included in your AGI and thus combined income calculations, potentially increasing the amount of your Social Security benefits subject to taxation.

10. Where can I find more resources and support for retirement planning?

Visit income-partners.net for comprehensive resources, partnership opportunities, and personalized advice to help you achieve your retirement goals.