Navigating the world of financial partnerships can be complex, especially when personal relationships intersect with financial considerations. A key question often arises: Does your boyfriend’s income count as household income when determining eligibility for programs or partnerships? At income-partners.net, we aim to provide clarity and guidance to help you make informed decisions. This article will explore the intricacies of household income, focusing on whether a boyfriend’s income is included, and offer insights on how to optimize your partnership strategies for maximum financial benefit. Let’s delve in to understand household income, eligibility criteria, and smart partnership strategies for a thriving financial future.

1. Understanding Household Income

Household income is the total income of all individuals residing in a single household. This figure is used to assess eligibility for various government assistance programs, loans, and other financial opportunities. Understanding how household income is calculated is crucial for accurate reporting and effective financial planning.

1.1. What Constitutes Household Income?

Household income typically includes wages, salaries, tips, investment income, rental income, and government benefits received by all household members. However, the specific definition can vary depending on the program or entity assessing the income. For example, some programs may exclude certain types of income, such as student financial aid or specific tax credits.

1.2. Importance of Accurate Income Reporting

Accurate reporting of household income is essential for several reasons:

- Eligibility: Ensures you qualify for programs or partnerships based on their income criteria.

- Legal Compliance: Prevents fraud and penalties associated with misreporting income.

- Financial Planning: Provides a clear picture of your financial situation for effective budgeting and investment.

1.3. Resources for Determining Household Income

Several resources can help you determine your household income accurately:

- IRS Guidelines: The Internal Revenue Service (IRS) provides detailed instructions on calculating adjusted gross income (AGI) and modified adjusted gross income (MAGI), which are often used to determine household income.

- Government Assistance Programs: Each program, such as Medicaid or CHIP, provides specific guidelines on what income to include.

- Financial Advisors: Professionals who can offer personalized advice based on your unique financial situation. Income-partners.net can connect you with experienced financial advisors.

2. Does a Boyfriend’s Income Count as Household Income?

The question of whether a boyfriend’s income counts as household income depends on several factors, including marital status, tax filing status, and the specific rules of the program or entity assessing the income. Generally, if you are not married and file taxes separately, your boyfriend’s income may not automatically be included in your household income.

2.1. Marital Status and Tax Filing Status

- Married Filing Jointly: If you are married and file taxes jointly, your spouse’s income is always included in your household income.

- Married Filing Separately: Even if married but filing separately, some programs may still consider your spouse’s income.

- Unmarried: If you are unmarried, the rules can vary. Some programs may not include your boyfriend’s income unless he is a tax dependent or you file taxes together.

2.2. Rules for Government Assistance Programs

Government assistance programs like Medicaid, CHIP, and SNAP have specific rules for determining household income. These rules often consider tax relationships and living arrangements.

2.2.1. Medicaid and CHIP

Medicaid and the Children’s Health Insurance Program (CHIP) use a methodology called Modified Adjusted Gross Income (MAGI) to determine financial eligibility. MAGI is based on tax definitions of income and household. According to healthcare.gov, in general, if you are not married, only your income counts. However, if you claim your boyfriend as a dependent, his income might be considered.

2.2.2. SNAP (Supplemental Nutrition Assistance Program)

SNAP considers all individuals who live together and purchase and prepare meals together as part of the same household. Therefore, if you and your boyfriend share living expenses and meals, his income may be included in your household income for SNAP eligibility.

2.3. Impact on Partnership Opportunities

When considering business partnerships, lenders or investors may assess your personal financial situation, including household income. In these cases, the inclusion of a boyfriend’s income can affect your eligibility or the terms of the partnership.

2.3.1. Loan Applications

Lenders may consider the income of all household members to assess your ability to repay a loan. If your boyfriend contributes to household expenses, his income might be considered, even if you are not married.

2.3.2. Investment Opportunities

Investors may want to understand your overall financial stability, including household income. Disclosing your boyfriend’s income can provide a more complete picture of your financial situation and potentially improve your chances of securing investment.

Couple reviewing financial documents, discussing investment opportunities

Couple reviewing financial documents, discussing investment opportunities

3. Understanding MAGI (Modified Adjusted Gross Income)

Modified Adjusted Gross Income (MAGI) is a key concept in determining eligibility for Medicaid and CHIP. It’s essential to understand what MAGI is and how it’s calculated to accurately assess your eligibility for these programs.

3.1. What is MAGI?

MAGI is a method used to determine income for Medicaid and CHIP eligibility. It is based on tax definitions of income and household. Under MAGI rules, an individual or family’s assets do not count in determining eligibility. It’s important to note that while the rules for determining what income to count are mostly aligned, the rules determining who is in a household can vary significantly.

3.2. Who Must Use MAGI Rules?

All states must use MAGI rules regardless of their decision to expand Medicaid. However, MAGI rules apply only to certain categories of Medicaid eligibility, including parents and caregiver relatives, children, pregnant women, and the adult expansion group. States’ previous rules for determining income and households continue to apply to the elderly, disabled, and children in foster care.

3.3. How Does MAGI Differ from Premium Tax Credit Household Rules?

Medicaid and CHIP households are determined based on a person’s family and tax relationships as well as their living arrangements. How people file taxes and who is in their tax unit doesn’t always determine who is in their Medicaid household, but it determines which Medicaid household rules apply in defining the household. Premium tax credit household rules, on the other hand, are based purely on tax relationships.

3.3.1. Key Differences

The most important difference between Medicaid and premium tax credit households is that for Medicaid, household size and composition are determined separately for each member of the household. For the premium tax credit, members of a tax unit are always treated as a household. This means that for Medicaid, household size may differ for family members even when they are in the same tax filing household.

3.3.2. State Options

Medicaid provides states with several options that affect how they define households when determining Medicaid eligibility. However, because the premium tax credit is a federal benefit, the rules are established at the federal level and are consistent across states.

3.4. Determining Household Size Under MAGI

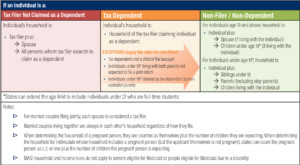

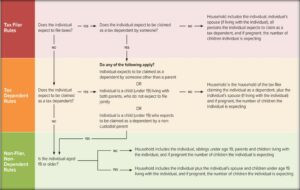

Medicaid determines an individual’s household based on their plan to file a tax return, regardless of whether or not they actually file a return at the end of the year. Medicaid also does not require people to file a federal income tax return in previous years. For each individual applying for coverage, Medicaid looks at whether they plan to be a tax filer, a tax dependent, or neither a tax filer nor a dependent.

3.4.1. Household Rules for Tax Filers

For tax filers claiming their own exemption and who can’t be claimed as a tax dependent, the household includes the tax filer, the spouse filing jointly, and everyone whom the tax filer claims as a tax dependent.

3.4.2. Household Rules for Tax Dependents

For tax dependents, the household is the same as the tax filer claiming the individual as a tax dependent. However, there are three exceptions to this rule, when the rule for non-filers is applied:

- Individuals who expect to be claimed as a dependent by someone other than a parent.

- Individuals (under 19) living with both parents, whose parents do not expect to file a joint tax return.

- Individuals (under 19) who expect to be claimed as a dependent by a non-custodial parent.

3.4.3. Household Rules for Non-Filers

For individuals who neither file a tax return nor are claimed as a tax dependent, the household rules differ based on whether the individual is an adult or a minor:

- For individuals 19 years and older, the household includes the individual plus, if living with the individual, their or her spouse and children who are under 19 years old.

- For individuals under 19 years old, the household includes the individual, plus any siblings under 19 years old, children of the individual and parents who live with the individual.

3.5. Adjustments to Household Rules

In addition to the general rules for determining household size, some rules apply in all situations:

- Married couples who live together are always counted in each other’s household regardless of whether they file a joint or separate return.

- Family size adjustments need to be made if the individual is pregnant. In determining the household of a pregnant person, they are counted as themself plus the number of children they are expected to deliver.

Flowchart illustrating how to determine an individual's Medicaid household

Flowchart illustrating how to determine an individual's Medicaid household

4. Strategies to Optimize Partnership Opportunities

Optimizing partnership opportunities involves careful financial planning and strategic decision-making. Here are some strategies to consider when navigating the complexities of household income and partnership eligibility.

4.1. Separate Finances

Maintaining separate finances can simplify income reporting and protect your individual financial interests. This is particularly important for unmarried couples.

4.1.1. Separate Bank Accounts

Keep separate bank accounts for income and expenses. This makes it easier to track your individual financial activity and avoid commingling funds.

4.1.2. Independent Credit Files

Ensure you and your boyfriend have independent credit files. This can prevent his credit history from affecting your ability to secure loans or other financial opportunities.

4.2. Legal Agreements

Consider creating legal agreements to define financial responsibilities and protect your assets.

4.2.1. Cohabitation Agreement

A cohabitation agreement can outline how assets and expenses are divided if the relationship ends. This can provide financial security and clarity.

4.2.2. Partnership Agreement

If you are entering a business partnership with your boyfriend, create a formal partnership agreement that specifies each partner’s roles, responsibilities, and financial contributions.

4.3. Professional Advice

Seek advice from financial advisors and legal professionals to navigate complex financial situations and ensure you are making informed decisions.

4.3.1. Financial Planning

A financial advisor can help you create a budget, manage debt, and plan for the future. They can also provide guidance on how to optimize your finances for partnership opportunities.

4.3.2. Legal Counsel

A lawyer can help you draft legal agreements and ensure you understand your rights and responsibilities. They can also provide advice on how to protect your assets.

4.4. Transparent Communication

Open and honest communication with your boyfriend is essential for effective financial planning.

4.4.1. Discuss Financial Goals

Discuss your financial goals and priorities with your boyfriend. This can help you align your financial strategies and work together to achieve your goals.

4.4.2. Share Financial Information

Be transparent about your income, expenses, and debts. This can help you make informed decisions and avoid misunderstandings.

4.5. Exploring Different Partnership Structures

Consider different partnership structures to find the one that best suits your financial situation and goals.

4.5.1. Limited Liability Company (LLC)

An LLC can provide liability protection and tax benefits. It can also simplify income reporting and asset management.

4.5.2. Joint Venture

A joint venture is a temporary partnership for a specific project. It can be a good option if you want to collaborate on a single venture without forming a long-term partnership.

5. Real-World Examples and Case Studies

Examining real-world examples and case studies can provide valuable insights into how household income and partnership eligibility are handled in practice.

5.1. Case Study 1: Medicaid Eligibility

Sarah and her boyfriend, Mark, live together but are not married. Sarah is applying for Medicaid. Mark is not her tax dependent. In this case, only Sarah’s income will be considered for her Medicaid eligibility. According to MAGI rules, since they are not married and Mark is not Sarah’s dependent, his income does not count towards her household income for Medicaid purposes.

5.2. Case Study 2: Loan Application

Emily and her boyfriend, David, are applying for a home loan. They are not married, but they share household expenses. The lender asks for information about all household income. In this scenario, the lender may consider David’s income to assess their ability to repay the loan, even though they are not married. Emily and David should be prepared to provide documentation of David’s income and explain their financial arrangement.

5.3. Case Study 3: Business Partnership

Jessica and her boyfriend, Chris, are starting a business together. They decide to form an LLC. In this case, they should create a partnership agreement that clearly outlines each partner’s financial contributions, responsibilities, and ownership stake. The agreement should also address how income and expenses will be divided.

5.4. Success Story: Strategic Financial Planning

Lisa and her boyfriend, Tom, sought advice from a financial advisor before entering a business partnership. The advisor helped them create separate bank accounts, draft a cohabitation agreement, and form an LLC for their business. As a result, they were able to protect their individual financial interests and successfully manage their business partnership.

5.5. Expert Insight: University of Texas Study

According to research from the University of Texas at Austin’s McCombs School of Business, strategic financial planning can significantly improve the success rate of business partnerships. The study emphasizes the importance of clear communication, legal agreements, and professional advice in navigating the complexities of partnership finances.

6. Common Mistakes to Avoid

Avoiding common mistakes in financial planning and partnership arrangements can save you time, money, and stress.

6.1. Not Understanding Eligibility Requirements

Failing to understand the eligibility requirements for programs and partnerships can lead to disappointment and wasted effort. Always research the specific rules and guidelines before applying.

6.2. Misreporting Income

Misreporting income, whether intentionally or unintentionally, can have serious consequences, including penalties and legal action. Always report your income accurately and honestly.

6.3. Commingling Funds

Commingling funds can create confusion and complicate financial planning. Keep your personal and business finances separate.

6.4. Neglecting Legal Agreements

Neglecting to create legal agreements can leave you vulnerable to financial risk and disputes. Always draft formal agreements to protect your interests.

6.5. Ignoring Professional Advice

Ignoring professional advice can lead to costly mistakes. Seek guidance from financial advisors and legal professionals to make informed decisions.

7. Frequently Asked Questions (FAQs)

Navigating household income and partnership eligibility can raise many questions. Here are some frequently asked questions to provide further clarity.

7.1. Does my boyfriend’s income count as household income for Medicaid?

Generally, no. If you are not married and do not claim your boyfriend as a tax dependent, his income typically does not count towards your household income for Medicaid eligibility.

7.2. How does MAGI determine household size?

MAGI determines household size based on tax filing status, including whether you plan to file as a tax filer, a tax dependent, or neither.

7.3. What is a cohabitation agreement?

A cohabitation agreement is a legal document that outlines how assets and expenses are divided if an unmarried couple separates.

7.4. Should I keep separate bank accounts from my boyfriend?

Yes, keeping separate bank accounts can simplify income reporting and protect your individual financial interests.

7.5. What is an LLC?

An LLC (Limited Liability Company) is a business structure that provides liability protection and tax benefits.

7.6. How can a financial advisor help with partnership planning?

A financial advisor can help you create a budget, manage debt, and plan for the future. They can also provide guidance on how to optimize your finances for partnership opportunities.

7.7. What are the benefits of a partnership agreement?

A partnership agreement clearly outlines each partner’s financial contributions, responsibilities, and ownership stake, which can prevent disputes and protect your interests.

7.8. Does SNAP consider my boyfriend’s income?

If you and your boyfriend live together and share meals, SNAP may consider his income as part of your household income.

7.9. Are married couples who file taxes separately considered in separate households for Medicaid?

Generally, no. Married couples who live together are always considered to be in each other’s household regardless of how they file taxes.

7.10. How does Medicaid determine the household of an adult child claimed as a tax dependent by their parents?

The household of an individual who is at least 19 years old and is claimed as a tax dependent by their parents is always the same as the household of the parents claiming them.

8. Latest Trends and Opportunities in Partnership

Staying updated on the latest trends and opportunities in partnership can help you make informed decisions and maximize your financial success.

8.1. Rise of Strategic Alliances

Strategic alliances are becoming increasingly popular as businesses seek to expand their reach and access new markets. These partnerships involve collaboration between companies to achieve mutual goals.

8.2. Focus on Sustainability

Sustainability is a growing concern for businesses and consumers. Partnerships focused on sustainability initiatives are gaining traction.

8.3. Digital Transformation

Digital transformation is reshaping industries and creating new partnership opportunities. Companies are collaborating to develop innovative digital solutions.

8.4. Remote Collaboration

Remote collaboration tools and technologies are making it easier for partners to work together from different locations.

8.5. Data-Driven Partnerships

Data-driven partnerships involve sharing data and insights to improve decision-making and drive growth.

| Trend | Description | Benefits |

|---|---|---|

| Strategic Alliances | Collaboration between companies to achieve mutual goals. | Expanded reach, access to new markets, shared resources. |

| Sustainability Focus | Partnerships focused on environmental and social responsibility. | Enhanced brand reputation, access to eco-conscious consumers, positive impact on the environment. |

| Digital Transformation | Collaboration to develop innovative digital solutions. | Improved efficiency, enhanced customer experience, access to cutting-edge technologies. |

| Remote Collaboration | Using technology to enable partners to work together from different locations. | Increased flexibility, reduced costs, access to a wider talent pool. |

| Data-Driven Partnerships | Sharing data and insights to improve decision-making and drive growth. | Better-informed decisions, improved efficiency, enhanced customer targeting. |

9. Conclusion: Navigating Household Income for Successful Partnerships

Understanding whether a boyfriend’s income counts as household income is crucial for accurate financial planning and successful partnership endeavors. By considering marital status, tax filing status, and the specific rules of relevant programs, you can make informed decisions that protect your financial interests and optimize your opportunities. Remember to maintain separate finances, create legal agreements, seek professional advice, and communicate transparently with your partner.

At income-partners.net, we are dedicated to providing you with the resources and guidance you need to navigate the complexities of financial partnerships. Explore our website to discover a wealth of information on various partnership types, effective relationship-building strategies, and potential collaboration opportunities.

Ready to take the next step? Contact us today to explore partnership opportunities, learn about building effective relationships, and connect with potential partners in the USA. Our team at income-partners.net is here to support you in creating profitable partnerships and achieving your financial goals.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net