Yes, bad debt expense appears on the income statement, reflecting uncollectible receivables and impacting your bottom line. At income-partners.net, we help businesses understand how managing and minimizing bad debt can improve financial health through strategic partnerships and informed financial decisions. By exploring the intricacies of bad debt expense, you can gain a competitive edge and foster revenue partnerships that enhance your financial resilience. This guide explores the nature of bad debt, its recording methods, and collaborative strategies to minimize its impact, ensuring your financial statements accurately reflect your business performance.

1. What Is Bad Debt Expense?

Bad debt expense (BDE) represents the portion of a company’s accounts receivable that is deemed uncollectible. This expense is recorded on the income statement under Sales, General, and Administrative (SG&A) expenses, reducing the company’s profit. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, effectively managing BDE is crucial for maintaining accurate financial reporting and assessing the true profitability of a business.

1.1. Why Is Bad Debt Expense Important?

Recording bad debt is essential for several reasons:

- Accurate Financial Reporting: It provides a realistic view of a company’s financial health by acknowledging potential losses from uncollectible receivables.

- Compliance with Accounting Standards: Following the accrual accounting system, as mandated by Generally Accepted Accounting Principles (GAAP), requires recognizing expenses in the same period as the related revenue.

- Performance Evaluation: It helps in evaluating the effectiveness of credit and collection policies.

While recording bad debt reduces the value of receivables, companies still retain the right to pursue collection if circumstances change.

1.2. Accrual vs. Cash Accounting and Bad Debt

The method of accounting a company uses dictates how bad debt is handled:

- Accrual Accounting: Revenue is recognized when earned, regardless of when payment is received. Therefore, bad debt expense is necessary to offset previously recorded revenue when invoices become uncollectible.

- Cash Accounting: Revenue is recognized only when cash is received. If payment is never received, the revenue is never recorded, eliminating the need for a bad debt expense entry.

Accrual accounting provides a more accurate picture of a company’s financial performance, but it requires careful management of potential bad debts.

1.3. How Bad Debt Expense Impacts the Income Statement

Bad debt expense directly reduces a company’s net income. Here’s how it fits into the income statement:

- Revenue: Total sales revenue is listed.

- Cost of Goods Sold (COGS): The direct costs associated with producing goods or services are subtracted.

- Gross Profit: Revenue minus COGS.

- Operating Expenses: Includes SG&A expenses, where bad debt expense is listed.

- Operating Income: Gross profit minus operating expenses.

- Other Income and Expenses: Any non-operating income or expenses.

- Net Income Before Taxes: Operating income plus or minus other income and expenses.

- Income Tax Expense: Taxes owed on the net income.

- Net Income: The final profit after all expenses and taxes are deducted.

By accurately recording bad debt expense, companies can present a more realistic view of their financial performance to stakeholders, including investors and creditors.

2. Why Do Bad Debts Happen?

Bad debts arise from various factors. Understanding these reasons can help businesses mitigate risks and improve their accounts receivable management.

2.1. Common Causes of Bad Debt

- Customer Disputes: Disagreements over product or service quality can lead customers to refuse payment.

- Customer Bankruptcy: When customers become insolvent, they may be unable to fulfill their financial obligations.

- Economic Downturns: During recessions or economic slowdowns, customers may struggle to pay their bills.

- Inefficient Credit Policies: Lax credit standards can result in extending credit to high-risk customers.

- Poor Communication: Misunderstandings or lack of clarity regarding payment terms can lead to non-payment.

2.2. The Accounts Receivable Disconnect

The Accounts Receivable (AR) Disconnect refers to the communication gaps between AR departments and their customers. This disconnect often results from a lack of integrated systems and clear communication channels. According to a survey by Wakefield Research and Versapay, 85% of C-level executives said miscommunication between their AR department and a customer has resulted in the customer not paying in full.

2.3. Optimizing Customer Experience to Minimize Bad Debt

Improving the customer experience can significantly reduce the likelihood of bad debts. Strategies include:

- Clear Communication: Ensuring customers understand payment terms and have access to necessary information.

- Easy Payment Options: Providing multiple payment methods to suit customer preferences.

- Prompt Issue Resolution: Addressing customer disputes and concerns quickly and efficiently.

- Personalized Service: Tailoring the billing and payment experience to meet individual customer needs.

By prioritizing customer satisfaction and clear communication, businesses can foster stronger relationships and reduce the risk of non-payment.

3. How to Record Bad Debt Expense

There are two primary methods for recording bad debt expense: the direct write-off method and the allowance method. Each has its advantages and disadvantages, depending on the specific needs and accounting practices of the business.

3.1. Direct Write-Off Method

The direct write-off method involves recognizing bad debt expense only when an account is deemed uncollectible. This method is straightforward but may not accurately reflect the company’s financial performance in the period when the sale occurred.

3.1.1. How the Direct Write-Off Method Works

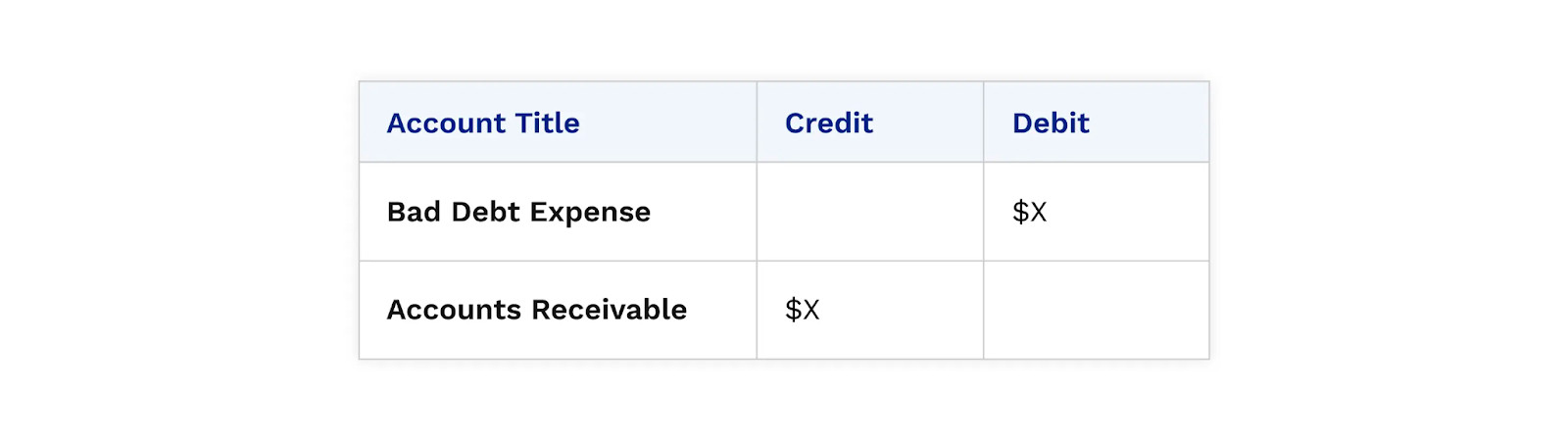

When an invoice is determined to be uncollectible, the following journal entry is made:

- Debit: Bad Debt Expense

- Credit: Accounts Receivable

This entry directly reduces the accounts receivable balance and recognizes the expense in the current period.

3.1.2. Advantages and Disadvantages

- Advantages:

- Simple and easy to implement.

- Suitable for small businesses with few uncollectible accounts.

- Disadvantages:

- Violates the matching principle, as the expense is not recognized in the same period as the revenue.

- May misstate income if bad debt expense is recorded in a different period from the sales entry.

3.1.3. IRS Conditions for Writing Off Debt

To satisfy the IRS’ conditions for writing off debt, a business must:

- Have firm evidence that the customer will not pay.

- Take reasonable steps to collect the amount owed, such as contacting the customer or addressing disputes.

3.2. Allowance Method

The allowance method is a more accurate approach to recording bad debt expense, aligning with the matching principle and GAAP requirements. This method involves estimating and recording bad debt expense at the end of each accounting period.

3.2.1. How the Allowance Method Works

- Create an Allowance for Doubtful Accounts (AFDA): This is a contra-asset account that reduces the total value of accounts receivable on the balance sheet.

- Estimate AFDA: Use one of the methods discussed in the next section to estimate the amount of uncollectible receivables.

- Record Bad Debt Expense: Make a journal entry to recognize the estimated bad debt expense.

The journal entry is:

- Debit: Bad Debt Expense

- Credit: Allowance for Doubtful Accounts

3.2.2. Advantages and Disadvantages

- Advantages:

- Complies with the matching principle by recognizing expenses in the same period as revenue.

- Provides a more accurate representation of a company’s financial position.

- Disadvantages:

- More complex than the direct write-off method.

- Requires estimating the amount of uncollectible receivables, which can be subjective.

3.2.3. The Matching Principle and the Allowance Method

The matching principle requires companies to record expenses in the same period as the revenue they help generate. The allowance method adheres to this principle by estimating and recording bad debt expense in the same period as the related sales revenue, providing a more accurate picture of profitability.

4. How to Estimate Bad Debt Expense Using the Allowance Method

Estimating bad debt expense involves using historical data and industry trends to predict the portion of receivables that will likely become uncollectible. There are three common methods for estimating AFDA: percentage of sales, percentage of accounts receivable, and accounts receivable aging.

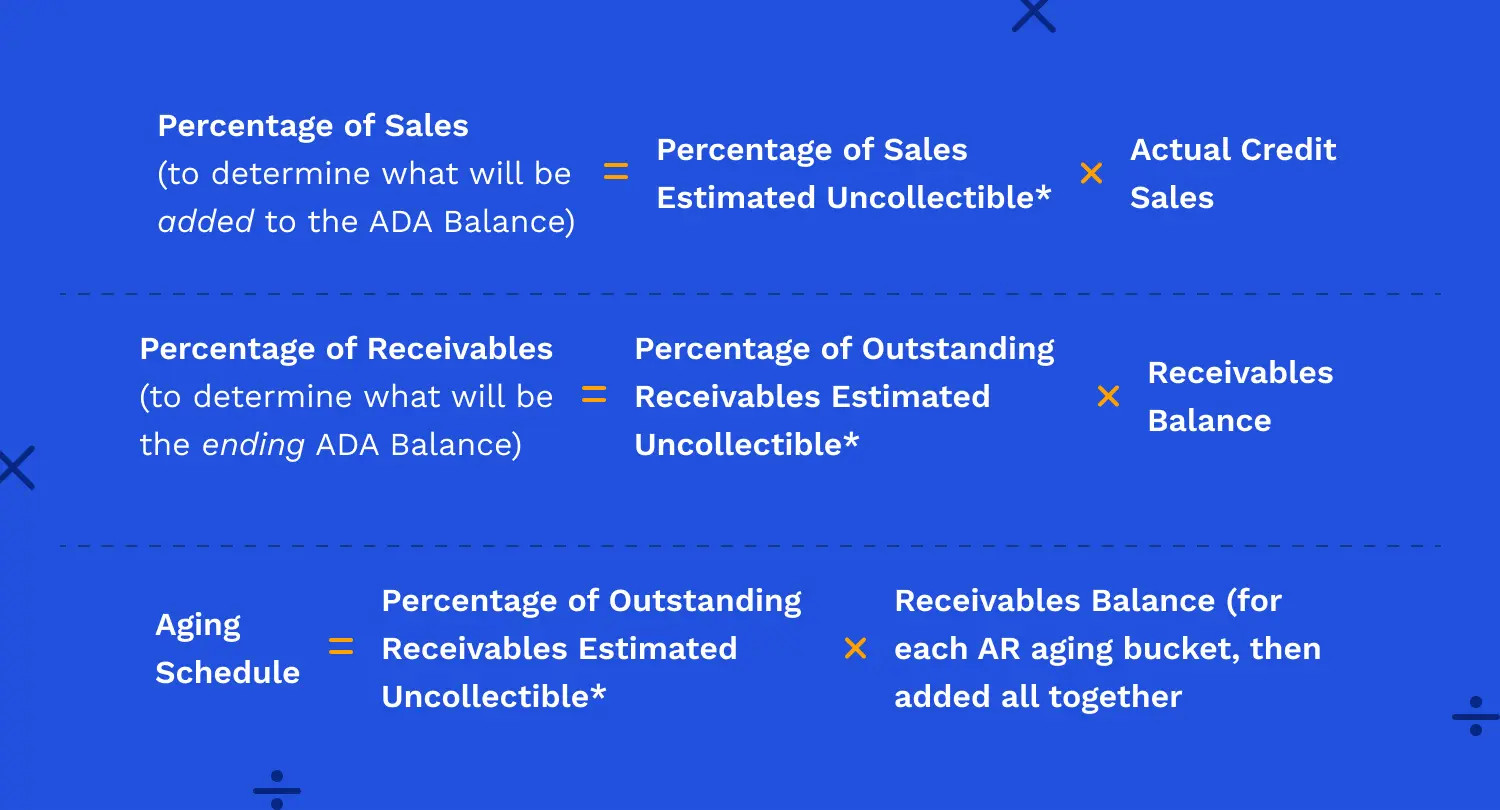

4.1. Percentage of Sales Method

The percentage of sales method estimates bad debt expense as a percentage of total credit sales. This method is straightforward and directly ties bad debt expense to sales revenue.

4.1.1. Formula and Calculation

The formula for the percentage of sales method is:

- Bad Debt Expense = Percentage of Sales Estimated Uncollectible × Actual Credit Sales

Example:

- Historical Average Annual Credit Sales: $10,000,000

- Historical Average Uncollected Credit Sales: $500,000

- Historical Percentage of Uncollected Credit Sales: 5%

If actual credit sales for the current period are $12,000,000, the bad debt expense allowance is:

- BDE Allowance: 5% of $12,000,000 = $600,000

4.1.2. Recording the Adjustment

The result of this calculation is the adjustment to the AFDA balance. When recording allowance for doubtful accounts on the accounts receivable balance sheet, you’ll add any existing AFDA balance (from the year prior) to the adjustment balance to find the ending balance. When recording bad debt expense on the income statement, you’ll just record the adjustment value.

4.2. Percentage of Receivables Method

The percentage of receivables method estimates bad debt expense as a percentage of outstanding accounts receivable. This method focuses on the balance sheet and provides an estimate of the uncollectible portion of receivables at a specific point in time.

4.2.1. Formula and Calculation

The formula for the percentage of receivables method is:

- Bad Debt Expense = Percentage Receivables Estimated Uncollectible × Receivables Balance

Example:

- Historical Average Accounts Receivable: $15,000,000

- Historical Cash Collected from Accounts Receivable: $1,200,000

- Historical Percentage of Uncollected Receivables: 8%

If the current receivables balance is $18,000,000, the bad debt expense allowance is:

- BDE Allowance: 8% of $18,000,000 = $1,440,000

4.2.2. Recording the Adjustment

The result from this calculation is your company’s ending AFDA balance for the end of the period. This is because any overdue receivables from the year prior are already accounted for in the receivables balance for the current period. The result of your calculation is what you’ll record on the accounts receivable balance sheet. When recording bad debt expense on the income statement, however, you’ll just record the adjustment value. The adjustment value is the difference between the ending AFDA balance and the starting AFDA balance.

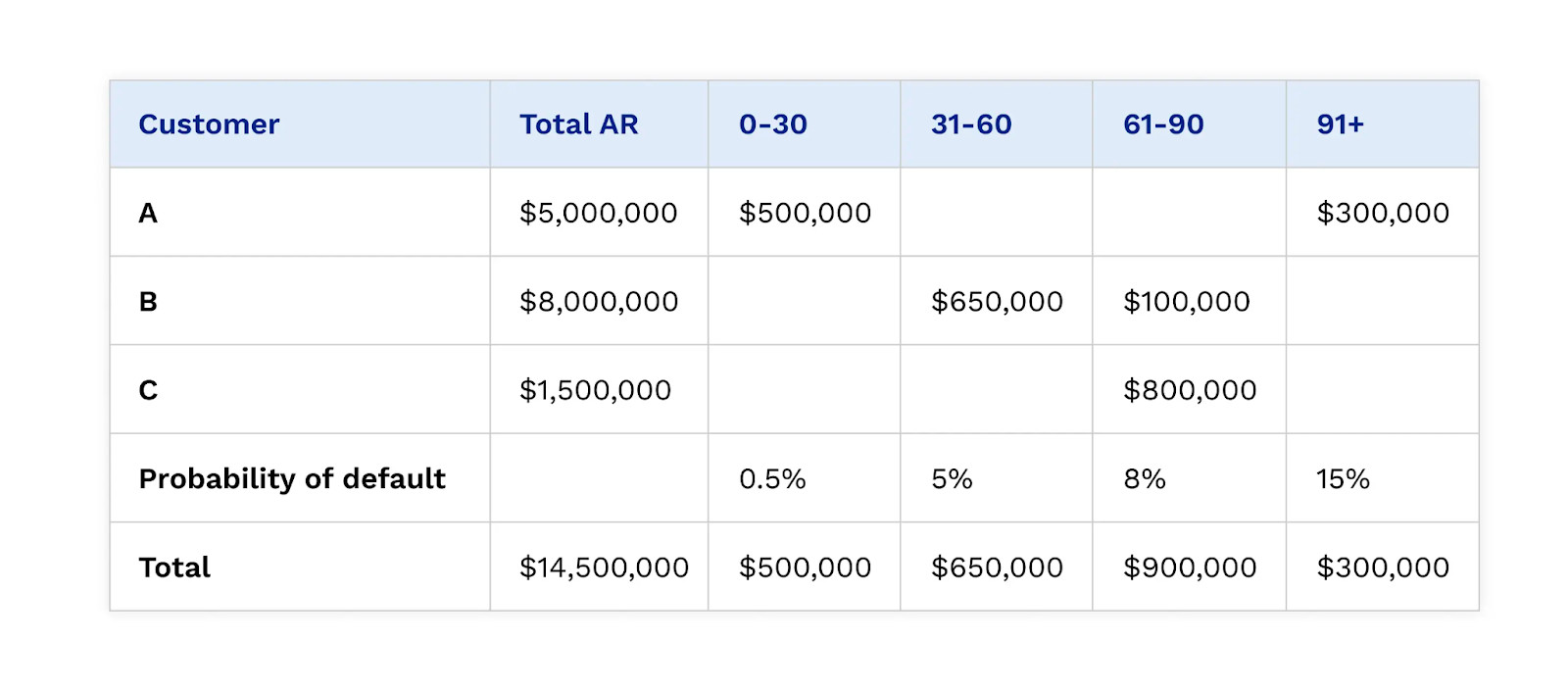

4.3. Accounts Receivable Aging Method

The accounts receivable aging method is a more detailed approach that categorizes receivables by age and assigns a different uncollectible percentage to each category. This method provides a more accurate estimate of bad debt expense by considering the likelihood of collection based on how long an invoice has been outstanding.

4.3.1. How the Accounts Receivable Aging Method Works

- Create an AR Aging Report: This report categorizes receivables into different age groups, such as 0-30 days, 31-60 days, 61-90 days, and over 90 days.

- Assign Collection Probabilities: Assign a percentage of uncollectibility to each aging category based on historical data and industry trends.

- Calculate Bad Debt Allowance: Multiply the balance in each aging category by the corresponding uncollectibility percentage.

- Total the Allowances: Add the bad debt allowances for each aging category to determine the total bad debt reserve.

4.3.2. Example of an AR Aging Report

| Aging Category | Receivables Balance | Uncollectibility Percentage | Bad Debt Allowance |

|---|---|---|---|

| 0-30 days | $100,000 | 1% | $1,000 |

| 31-60 days | $50,000 | 5% | $2,500 |

| 61-90 days | $20,000 | 15% | $3,000 |

| Over 90 days | $10,000 | 30% | $3,000 |

| Total | $180,000 | $9,500 |

In this example, the total bad debt reserve is $9,500.

4.3.3. Advantages of the Accounts Receivable Aging Method

The accounts receivable aging method offers a more precise estimate of uncollectible receivables by considering the age of outstanding invoices. This allows for a more accurate representation of the company’s financial position and helps in making informed decisions about credit and collection policies.

4.4. Factors Affecting the Accuracy of Estimates

Several factors can influence the accuracy of bad debt expense estimates:

- Economic Conditions: Economic downturns can increase the likelihood of customers defaulting on payments.

- Industry Trends: Changes in the industry can impact customer payment behavior.

- Customer Base: The creditworthiness and payment history of a company’s customer base can affect the accuracy of estimates.

- Company Policies: Credit and collection policies can influence the likelihood of collecting receivables.

4.5. Consistency in Method Selection

Consistency in using a particular method is crucial for accurate financial reporting. While businesses can change methods, they must disclose the change and its impact on financial statements.

5. How Collaborative Accounts Receivable Minimizes Bad Debt Expense

Collaborative Accounts Receivable (AR) solutions leverage technology to streamline communication, automate processes, and improve customer relationships. By fostering collaboration between AR teams, sales teams, and customers, these solutions can significantly reduce bad debt expense.

5.1. What Is Collaborative AR?

Collaborative AR involves using cloud-based platforms and automation tools to connect AR teams with customers and internal stakeholders. These solutions provide real-time visibility into account status, facilitate communication, and streamline payment processes.

5.2. Benefits of Collaborative AR

- Improved Communication: Streamlines communication between AR teams and customers, reducing misunderstandings and disputes.

- Enhanced Efficiency: Automates invoicing, payment processing, and cash application workflows, freeing up AR staff to focus on strategic tasks.

- Better Customer Relationships: Provides customers with self-service portals and personalized communication, improving their overall experience.

- Increased Transparency: Offers real-time visibility into account status and payment history, enabling better decision-making.

5.3. How Collaborative AR Minimizes Bad Debt Expense

- More Transparent Lines of Communication:

- Collaborative AR solutions make it easier for AR staff to communicate with customers to resolve issues that often lead to payment delays, such as disputed invoice charges or missing remittance information.

- Instead of sifting through multiple email threads, AR staff and customers alike can find all the information they need in one place.

- Better Alignment Between Sales and AR Teams:

- Collaborative AR allows sales teams to access customer payment history and cash flow data, helping them make more informed credit decisions.

- Improved communication between sales and AR departments ensures there are no misunderstandings about credit terms and early payment incentives.

- Greater Focus on Value-Added Work:

- By automating routine tasks, collaborative AR frees up AR teams to focus on more strategic, value-added work, such as uncovering the causes of payment delays and working with customers to better understand their needs.

- This not only helps forge better customer relationships but also minimizes bad debt expense by reducing the likelihood of receivables becoming uncollectible.

5.4. Real-World Examples of Collaborative AR Success

- Case Study 1: A manufacturing company implemented a collaborative AR solution and reduced its bad debt expense by 30% within the first year. By automating invoicing and payment reminders, the company improved its collection rate and reduced the number of overdue invoices.

- Case Study 2: A technology company used a collaborative AR platform to improve communication with its customers and resolve disputes more quickly. As a result, the company reduced its days sales outstanding (DSO) by 15% and improved customer satisfaction.

6. Best Practices for Managing Bad Debt Expense

Effective management of bad debt expense requires a proactive approach that combines sound credit policies, efficient collection processes, and collaborative communication.

6.1. Establishing Sound Credit Policies

- Creditworthiness Assessment: Evaluate the creditworthiness of new customers before extending credit.

- Credit Limits: Set appropriate credit limits based on customer risk profiles.

- Payment Terms: Clearly communicate payment terms to customers.

6.2. Implementing Efficient Collection Processes

- Timely Invoicing: Send invoices promptly and accurately.

- Payment Reminders: Send regular payment reminders to customers.

- Collection Calls: Make collection calls to follow up on overdue invoices.

- Dispute Resolution: Establish a process for resolving customer disputes quickly and efficiently.

6.3. Utilizing Technology and Automation

- AR Automation Software: Implement AR automation software to streamline invoicing, payment processing, and cash application workflows.

- Customer Portals: Provide customers with self-service portals to view their account status and make payments online.

- Data Analytics: Use data analytics to identify trends and patterns in customer payment behavior.

6.4. Continuous Monitoring and Review

- Regular Reporting: Generate regular reports on key AR metrics, such as DSO and collection rates.

- Performance Evaluation: Evaluate the performance of credit and collection policies and make adjustments as needed.

- Risk Assessment: Continuously assess the risk of bad debt and adjust reserves accordingly.

6.5. Training and Development

- AR Staff Training: Provide AR staff with training on credit and collection best practices.

- Sales Team Alignment: Ensure sales teams are aligned with AR policies and understand the importance of credit management.

- Customer Communication Skills: Train staff on effective communication techniques for interacting with customers.

7. Bad Debt Expense and Financial Health

Bad debt expense is more than just an accounting entry; it’s an indicator of a company’s financial health and operational efficiency. Understanding its implications can lead to better financial strategies and improved profitability.

7.1. Indicators of High Bad Debt Expense

Several factors can indicate a company is experiencing high bad debt expense:

- Increasing DSO: A rising DSO suggests it takes longer to collect receivables, increasing the risk of bad debt.

- High Percentage of Overdue Invoices: A significant portion of invoices that are past due indicates collection issues.

- Customer Complaints: Frequent complaints about billing or service issues can lead to payment disputes.

- Economic Downturns: Economic recessions or industry-specific challenges can impact customers’ ability to pay.

7.2. Strategies for Improving Financial Health

- Strengthen Credit Policies: Implement stricter credit evaluation processes to minimize extending credit to high-risk customers.

- Enhance Collection Efforts: Improve collection processes with timely reminders, proactive follow-ups, and clear dispute resolution mechanisms.

- Invest in Technology: Adopt AR automation tools to streamline processes, improve communication, and provide better customer service.

- Diversify Customer Base: Reduce reliance on a few large customers to mitigate the impact of potential defaults.

7.3. The Role of Partnerships in Financial Stability

Forming strategic partnerships can help businesses improve their financial stability by:

- Sharing Resources: Pooling resources with partners can reduce costs and improve efficiency.

- Expanding Market Reach: Collaborating with partners can open new markets and increase revenue opportunities.

- Mitigating Risks: Sharing risks with partners can reduce the impact of potential losses.

At income-partners.net, we specialize in connecting businesses with strategic partners to foster growth and financial resilience.

7.4. Income-Partners.Net: Your Partner in Financial Success

At income-partners.net, we understand the challenges businesses face in managing bad debt expense and maintaining financial health. Our platform offers a range of resources and services to help you:

- Connect with Strategic Partners: Find partners who can help you expand your market reach and improve your financial stability.

- Access Expert Insights: Gain access to expert insights and best practices for managing bad debt expense.

- Utilize Cutting-Edge Technology: Discover innovative technology solutions that can streamline your AR processes and improve customer communication.

- Tailored Solutions: You will find tailored strategies to address your specific needs and challenges.

Contact us at [Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.] to discover how we can help you minimize bad debt expense and maximize your financial potential.

Bad Debt Expense Journal Entry

Bad Debt Expense Journal Entry

Collaborative accounts receivable solutions significantly minimize bad debt expense by streamlining collections and avoiding miscommunications.

8. The Future of Bad Debt Management

As technology continues to evolve, the future of bad debt management will likely be shaped by increased automation, artificial intelligence, and real-time data analytics.

8.1. Emerging Technologies

- AI-Powered Credit Scoring: AI algorithms can analyze vast amounts of data to provide more accurate credit scores, helping businesses make informed decisions about extending credit.

- Predictive Analytics: Predictive analytics can forecast the likelihood of customers defaulting on payments, allowing businesses to take proactive measures to mitigate risks.

- Blockchain Technology: Blockchain can enhance transparency and security in payment processes, reducing the risk of fraud and payment disputes.

8.2. Trends in AR Automation

- Cloud-Based Solutions: Cloud-based AR automation solutions offer greater flexibility, scalability, and accessibility, allowing businesses to manage their AR processes from anywhere.

- Mobile Payment Options: Mobile payment options are becoming increasingly popular, providing customers with convenient ways to pay their invoices.

- Integration with ERP Systems: Integration with Enterprise Resource Planning (ERP) systems streamlines data flow and improves overall efficiency.

8.3. Preparing for the Future

To prepare for the future of bad debt management, businesses should:

- Embrace Technology: Adopt new technologies and automation tools to streamline AR processes and improve customer communication.

- Invest in Data Analytics: Use data analytics to gain insights into customer payment behavior and identify potential risks.

- Foster Collaboration: Encourage collaboration between AR teams, sales teams, and customers to improve communication and resolve disputes quickly.

- Stay Informed: Stay up-to-date on the latest trends and best practices in bad debt management.

9. FAQ About Bad Debt Expense

9.1. What is the primary goal of recording bad debt expense?

The primary goal is to accurately reflect the potential losses from uncollectible receivables, ensuring financial statements provide a realistic view of a company’s financial health.

9.2. How does the allowance method comply with GAAP?

The allowance method complies with the Generally Accepted Accounting Principles (GAAP) by adhering to the matching principle, which requires expenses to be recognized in the same period as the related revenue.

9.3. What are the main reasons why bad debts occur?

Common reasons include customer disputes, bankruptcy, economic downturns, inefficient credit policies, and poor communication.

9.4. Why is the accounts receivable aging method considered more accurate?

It is more accurate because it assigns different uncollectible percentages to various aging categories of receivables, reflecting the varying likelihood of collection based on how long an invoice has been outstanding.

9.5. How does collaborative AR improve customer relationships?

Collaborative AR improves customer relationships by providing self-service portals, personalized communication, and quick resolution of disputes, enhancing the overall customer experience.

9.6. What key AR metrics should be regularly monitored?

Key metrics include Days Sales Outstanding (DSO) and collection rates, which help in evaluating the effectiveness of credit and collection policies.

9.7. Can AI improve credit scoring accuracy?

Yes, AI algorithms can analyze extensive data to provide more accurate credit scores, enabling businesses to make informed decisions about extending credit.

9.8. What role do partnerships play in enhancing financial stability?

Partnerships can help businesses share resources, expand market reach, and mitigate risks, thus improving their overall financial stability.

9.9. How can a business prepare for the future of bad debt management?

Businesses should embrace new technologies, invest in data analytics, foster collaboration, and stay informed on the latest trends and best practices.

9.10. What services does income-partners.net offer to help manage bad debt expense?

Income-partners.net offers connections to strategic partners, expert insights, innovative technology solutions, and tailored strategies to help businesses minimize bad debt expense and maximize financial potential.

10. Conclusion: Taking Control of Bad Debt Expense

Managing bad debt expense is crucial for maintaining accurate financial reporting, improving cash flow, and fostering sustainable growth. By understanding the causes of bad debt, implementing effective recording methods, and leveraging collaborative strategies, businesses can minimize their risk and enhance their financial health. Income-partners.net is dedicated to providing the resources and connections you need to succeed in today’s dynamic business environment. We invite you to explore the opportunities for collaboration, discover new strategies for growth, and connect with partners who share your vision. Visit income-partners.net today and take the first step toward a more secure and prosperous future.

AR Aging Report Example

AR Aging Report Example

Utilizing an accounts receivable aging report to calculate total bad debt reserve.

Bad Debt Expense Calculator Overview

Bad Debt Expense Calculator Overview

The three methods for recording bad debt expense are percentage of sales, percentage of receivables, and aging schedule.