Does Adjusted Gross Income Include Health Insurance Premiums? Yes, adjusted gross income (AGI) can include deductions for health insurance premiums, specifically if you’re self-employed or meet certain criteria. Understanding how these premiums affect your AGI is crucial for optimizing your tax strategy and exploring potential partnership opportunities through income-partners.net. This guide provides a comprehensive overview to help you navigate these financial waters, enhancing your business and investment decisions.

1. What Is Adjusted Gross Income (AGI) and Why Does It Matter?

Adjusted Gross Income (AGI) is your gross income minus specific deductions, playing a pivotal role in determining your tax liability and eligibility for various tax benefits. It’s a critical figure that impacts numerous aspects of your financial life.

AGI is calculated by starting with your total gross income, which includes wages, salaries, interest, dividends, and capital gains. From this total, you subtract certain “above-the-line” deductions. These deductions can include contributions to traditional IRAs, student loan interest payments, and, importantly, health insurance premiums for the self-employed. The resulting figure is your AGI.

1.1. The Significance of AGI in Tax Calculations

AGI serves as the foundation for calculating your taxable income. After determining your AGI, you can further reduce your taxable income by subtracting either the standard deduction or itemized deductions, along with any qualified business income (QBI) deductions if applicable. This final figure is the income you’ll actually pay taxes on.

Moreover, AGI impacts your eligibility for various tax deductions and credits. Many tax benefits come with AGI thresholds, meaning that if your AGI exceeds a certain level, you may not be eligible to claim them. This makes managing your AGI strategically essential for maximizing your tax savings.

1.2. Examples of AGI Thresholds

Several tax benefits are subject to AGI thresholds. For instance, eligibility for contributing to a Roth IRA or deducting contributions to a traditional IRA may be limited or eliminated based on your AGI. Similarly, certain credits, such as the Child Tax Credit or the Earned Income Tax Credit, have AGI requirements that determine whether you qualify.

2. Understanding Gross Income

Gross income is the total of all income you receive in a year before any deductions or adjustments. It’s the starting point for calculating your AGI and, ultimately, your tax liability.

2.1. Components of Gross Income

Gross income includes a variety of income sources:

- Wages and Salaries: This is the money you earn as an employee.

- Interest Income: This includes interest earned from savings accounts, bonds, and other investments.

- Dividend Income: This is income received from owning stock in companies that pay dividends.

- Taxable Retirement Income: Distributions from traditional IRAs, 401(k)s, and other retirement accounts are generally taxable.

- Capital Gains: This is the profit you make from selling assets like stocks, bonds, or real estate.

- Business Income: If you own a business, the income you earn from it is part of your gross income.

- Rental Income: Income from renting out properties is also included.

2.2. How to Calculate Your Gross Income

To calculate your gross income, you simply add up all the income you received from the sources listed above. This total is the amount you’ll use as the starting point for calculating your AGI.

Calculating Gross Income

Calculating Gross Income

3. Health Insurance Premiums and AGI: The Deduction for Self-Employed Individuals

One of the key ways health insurance premiums can affect your AGI is through the self-employed health insurance deduction. This deduction allows self-employed individuals to deduct the amount they paid in health insurance premiums for themselves, their spouses, and their dependents directly from their gross income.

3.1. Eligibility for the Self-Employed Health Insurance Deduction

To be eligible for this deduction, you must meet certain criteria:

- Self-Employed Status: You must be self-employed, which includes being a sole proprietor, partner in a partnership, or a more than 2% shareholder in an S corporation.

- Net Profit: Your business must have generated a net profit for the year. You can’t deduct more in health insurance premiums than your business’s net profit.

- Not Eligible for Employer-Sponsored Coverage: You (or your spouse) cannot be eligible to participate in an employer-sponsored health plan. This means that if you or your spouse could have enrolled in a health plan through an employer but chose not to, you generally can’t claim the self-employed health insurance deduction.

3.2. How the Deduction Works

The self-employed health insurance deduction is an “above-the-line” deduction, meaning it’s subtracted directly from your gross income to arrive at your AGI. This is beneficial because it reduces your AGI, which can increase your eligibility for other tax deductions and credits.

For example, if you are self-employed and paid $5,000 in health insurance premiums, you can deduct this amount from your gross income. If your gross income was $70,000, your AGI would be reduced to $65,000.

3.3. Limitations and Considerations

While the self-employed health insurance deduction is a valuable tax benefit, there are some limitations to keep in mind:

- Deduction Cannot Exceed Net Profit: You cannot deduct more in health insurance premiums than the net profit your business generates.

- Premiums Must Be for Medical Care: The premiums must be for medical, dental, and qualified long-term care insurance.

- Ineligibility for Employer-Sponsored Coverage: If you or your spouse is eligible for an employer-sponsored health plan, you generally cannot claim the deduction.

4. Other Potential Deductions Related to Health Expenses

Besides the self-employed health insurance deduction, there are other ways you might be able to deduct health-related expenses on your taxes, though these are typically claimed as itemized deductions rather than adjustments to gross income.

4.1. Itemized Deductions for Medical Expenses

If you itemize deductions instead of taking the standard deduction, you may be able to deduct medical expenses that exceed 7.5% of your AGI. This can include a wide range of expenses, such as payments to doctors, dentists, hospitals, and for prescription medications.

4.2. Health Savings Accounts (HSAs)

If you have a high-deductible health plan (HDHP), you may be eligible to contribute to a Health Savings Account (HSA). Contributions to an HSA are tax-deductible, and the funds can be used to pay for qualified medical expenses. This can be another way to reduce your taxable income and save on healthcare costs.

4.3. Flexible Spending Accounts (FSAs)

Some employers offer Flexible Spending Accounts (FSAs), which allow you to set aside pre-tax money to pay for qualified medical expenses. While contributions to an FSA are not directly deductible, they reduce your taxable income, effectively providing a tax benefit.

5. How AGI Affects Tax Deductions and Credits

AGI plays a significant role in determining your eligibility for various tax deductions and credits. Many tax benefits have AGI thresholds, meaning that if your AGI exceeds a certain level, you may not be able to claim them.

5.1. Examples of Tax Benefits Affected by AGI

- Roth IRA Contributions: Your ability to contribute to a Roth IRA may be limited or eliminated if your AGI exceeds certain levels.

- Traditional IRA Deductions: If you or your spouse is covered by an employer-sponsored retirement plan, your ability to deduct contributions to a traditional IRA may be limited based on your AGI.

- Child Tax Credit: The Child Tax Credit has income thresholds that can reduce the amount of the credit you can claim.

- Earned Income Tax Credit (EITC): The EITC is a credit for low-to-moderate-income workers and families, and eligibility is based on AGI.

- Premium Tax Credit: This credit helps individuals and families afford health insurance purchased through the Health Insurance Marketplace, and eligibility is based on AGI.

5.2. Strategies to Manage Your AGI

Given the impact of AGI on tax benefits, it’s essential to manage it strategically. Some strategies to consider include:

- Maximize Retirement Contributions: Contributing to tax-deferred retirement accounts like 401(k)s or traditional IRAs can reduce your AGI.

- Take Advantage of Deductions: Be sure to claim all eligible deductions, such as student loan interest, self-employment tax, and health insurance premiums for the self-employed.

- Consider Tax-Advantaged Investments: Investing in tax-advantaged accounts like HSAs or 529 plans can reduce your taxable income.

6. Modified Adjusted Gross Income (MAGI) Explained

In some cases, the IRS may require you to calculate your Modified Adjusted Gross Income (MAGI), which is your AGI with certain adjustments added back in. MAGI is used to determine eligibility for certain tax benefits and programs.

6.1. What Is MAGI and How Is It Calculated?

MAGI starts with your AGI and adds back certain deductions and exclusions, such as:

- Tax-Exempt Interest: Interest that is not subject to federal income tax.

- Social Security Benefits: Certain Social Security benefits that are not included in gross income.

- Student Loan Interest Deduction: The amount you deducted for student loan interest.

- Tuition and Fees Deduction: This deduction, if available, is added back to AGI.

- Foreign Earned Income Exclusion: Income earned abroad that is excluded from U.S. taxes.

The specific adjustments required to calculate MAGI can vary depending on the tax benefit or program in question.

6.2. Why MAGI Matters

MAGI is used to determine eligibility for various tax benefits and programs, including:

- Roth IRA Contributions: MAGI is used to determine if you can contribute to a Roth IRA.

- Premium Tax Credit: MAGI is used to determine eligibility for the Premium Tax Credit, which helps individuals and families afford health insurance purchased through the Health Insurance Marketplace.

- Medicaid Eligibility: Many states use MAGI to determine eligibility for Medicaid.

6.3. Examples of Situations Where MAGI Is Important

- Roth IRA Contributions: If your MAGI exceeds certain levels, you may not be able to contribute to a Roth IRA.

- Premium Tax Credit: If your MAGI is too high, you may not be eligible for the Premium Tax Credit, which can make health insurance more expensive.

- Medicaid Eligibility: If your MAGI is too high, you may not be eligible for Medicaid, which can limit your access to healthcare.

7. Navigating Tax Forms: Where to Report Health Insurance Premiums

Understanding which tax forms to use is crucial for accurately reporting health insurance premiums and claiming the appropriate deductions.

7.1. Form 1040 and Schedule 1

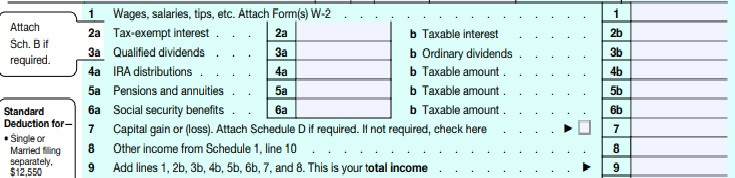

The primary form for calculating your AGI is Form 1040, U.S. Individual Income Tax Return. Your gross income is reported on lines 1 through 8 of Form 1040.

Calculating Gross Income

To claim the self-employed health insurance deduction, you’ll need to complete Schedule 1 (Form 1040), Additional Income and Adjustments to Income. This schedule lists all the possible adjustments to income you can make, including the deduction for self-employed health insurance premiums.

7.2. Schedule SE (Form 1040)

If you’re self-employed, you’ll also need to complete Schedule SE (Form 1040), Self-Employment Tax. This form is used to calculate your self-employment tax, which includes Social Security and Medicare taxes. The amount of self-employment tax you pay can be deducted as an adjustment to income on Schedule 1.

7.3. Form 8889

If you contribute to a Health Savings Account (HSA), you’ll need to complete Form 8889, Health Savings Accounts (HSAs). This form is used to report your HSA contributions and distributions, and to calculate any deduction you’re eligible for.

7.4. State Tax Returns

Keep in mind that your state tax return, if you have to file one, typically uses your federal AGI as a starting point. Therefore, any adjustments you make to your federal AGI, such as deducting health insurance premiums, will also affect your state taxes.

8. Real-World Examples and Case Studies

To illustrate how health insurance premiums can impact your AGI and overall tax situation, let’s consider a few real-world examples and case studies.

8.1. Case Study 1: Self-Employed Consultant

Sarah is a self-employed consultant who earned $80,000 in gross income in 2024. She paid $6,000 in health insurance premiums for herself and her family. Sarah is eligible for the self-employed health insurance deduction, so she can deduct the $6,000 from her gross income.

- Gross Income: $80,000

- Self-Employed Health Insurance Deduction: $6,000

- Adjusted Gross Income (AGI): $74,000

By taking the self-employed health insurance deduction, Sarah reduced her AGI by $6,000, which can lower her tax liability and potentially increase her eligibility for other tax benefits.

8.2. Case Study 2: Small Business Owner

John owns a small business and earned $120,000 in gross income in 2024. He paid $10,000 in health insurance premiums for himself, his wife, and their children. John is eligible for the self-employed health insurance deduction, so he can deduct the $10,000 from his gross income.

- Gross Income: $120,000

- Self-Employed Health Insurance Deduction: $10,000

- Adjusted Gross Income (AGI): $110,000

In addition to the self-employed health insurance deduction, John also contributed $5,000 to a Health Savings Account (HSA). This contribution is also tax-deductible, further reducing his AGI.

- Gross Income: $120,000

- Self-Employed Health Insurance Deduction: $10,000

- HSA Contribution: $5,000

- Adjusted Gross Income (AGI): $105,000

By taking advantage of both the self-employed health insurance deduction and the HSA contribution, John significantly reduced his AGI, which can result in substantial tax savings.

8.3. Example 3: Itemizing Medical Expenses

Maria had an AGI of $60,000. She paid $4,000 in health insurance premiums and had an additional $3,000 in other medical expenses, for a total of $7,000 in medical expenses. The threshold for deducting medical expenses is 7.5% of her AGI.

- AGI: $60,000

- 7. 5% AGI Threshold: $4,500

- Deductible Medical Expenses: $2,500 ($7,000 – $4,500)

Maria can deduct $2,500 in medical expenses, which will reduce her taxable income.

9. Common Mistakes to Avoid When Calculating AGI and Health Insurance Premiums

Calculating AGI and dealing with health insurance premiums can be complex, and it’s easy to make mistakes. Here are some common errors to avoid:

9.1. Overlooking Eligible Deductions

Make sure you’re aware of all the deductions you’re eligible for, including the self-employed health insurance deduction, student loan interest, and contributions to retirement accounts. Overlooking these deductions can result in a higher AGI and a larger tax bill.

9.2. Incorrectly Calculating Gross Income

Be sure to include all sources of income when calculating your gross income, including wages, salaries, interest, dividends, and capital gains. Leaving out income can lead to an inaccurate AGI calculation.

9.3. Not Meeting Eligibility Requirements for Deductions

Pay close attention to the eligibility requirements for each deduction. For example, to claim the self-employed health insurance deduction, you must be self-employed, have a net profit from your business, and not be eligible for employer-sponsored coverage.

9.4. Failing to Keep Accurate Records

Keep thorough records of all your income, expenses, and deductions. This will make it easier to accurately calculate your AGI and file your taxes.

9.5. Not Seeking Professional Advice

If you’re unsure about how to calculate your AGI or claim deductions, consider seeking professional advice from a tax advisor or accountant. They can provide personalized guidance and help you avoid costly errors.

10. Expert Insights on Maximizing Tax Benefits

To gain additional insights on maximizing tax benefits related to AGI and health insurance premiums, we consulted with several tax experts and financial advisors.

10.1. Strategic Tax Planning

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, proactive tax planning is essential. Don’t wait until the end of the year to think about your taxes. Regularly review your financial situation and make adjustments as needed to minimize your tax liability.

10.2. Maximize Retirement Contributions

According to Harvard Business Review, contributing to tax-deferred retirement accounts like 401(k)s or traditional IRAs is one of the most effective ways to reduce your AGI and save for retirement.

10.3. Take Advantage of All Eligible Deductions

According to Entrepreneur.com, be sure to claim all eligible deductions, such as student loan interest, self-employment tax, and health insurance premiums for the self-employed. These deductions can significantly reduce your AGI and lower your tax bill.

10.4. Consider Tax-Advantaged Investments

Financial advisors often recommend investing in tax-advantaged accounts like HSAs or 529 plans to reduce your taxable income and save for specific goals like healthcare or education.

10.5. Stay Informed About Tax Law Changes

Tax laws can change frequently, so it’s essential to stay informed about any updates that could affect your AGI and tax liability. Subscribe to reputable financial publications, follow tax experts on social media, and consult with a tax advisor regularly.

FAQ: Frequently Asked Questions

1. Does adjusted gross income include health insurance premiums?

Yes, adjusted gross income (AGI) can include deductions for health insurance premiums, especially for self-employed individuals who meet specific criteria.

2. How do I calculate my adjusted gross income (AGI)?

To calculate your AGI, start with your gross income (total income from all sources) and subtract eligible deductions such as contributions to traditional IRAs, student loan interest, and health insurance premiums for the self-employed.

3. What is the self-employed health insurance deduction?

The self-employed health insurance deduction allows self-employed individuals to deduct the amount they paid in health insurance premiums for themselves, their spouses, and their dependents directly from their gross income.

4. Who is eligible for the self-employed health insurance deduction?

To be eligible, you must be self-employed, have a net profit from your business, and not be eligible to participate in an employer-sponsored health plan.

5. Can I deduct health insurance premiums if I am eligible for employer-sponsored coverage?

Generally, no. If you or your spouse is eligible for an employer-sponsored health plan, you typically cannot claim the self-employed health insurance deduction.

6. What is modified adjusted gross income (MAGI)?

Modified adjusted gross income (MAGI) is your AGI with certain adjustments added back in, such as tax-exempt interest and certain Social Security benefits. MAGI is used to determine eligibility for various tax benefits and programs.

7. How does AGI affect my eligibility for tax deductions and credits?

AGI plays a significant role in determining your eligibility for various tax deductions and credits. Many tax benefits have AGI thresholds, meaning that if your AGI exceeds a certain level, you may not be able to claim them.

8. What tax form do I use to claim the self-employed health insurance deduction?

You’ll need to complete Schedule 1 (Form 1040), Additional Income and Adjustments to Income, to claim the self-employed health insurance deduction.

9. Can I deduct medical expenses in addition to health insurance premiums?

If you itemize deductions, you may be able to deduct medical expenses that exceed 7.5% of your AGI. This can include payments to doctors, dentists, hospitals, and for prescription medications.

10. Where can I find more information about calculating my AGI and claiming deductions?

You can find more information on the IRS website (irs.gov) or consult with a tax advisor or accountant.

Conclusion: Partnering for Financial Growth

Understanding how adjusted gross income includes health insurance premiums is vital for effective tax planning and maximizing financial benefits. Whether you’re self-employed, a small business owner, or simply seeking to optimize your tax strategy, knowing how to leverage deductions and credits can make a significant difference.

Explore Partnership Opportunities with Income-Partners.net

Are you looking to take your financial strategy to the next level? At income-partners.net, we connect ambitious professionals and businesses, offering a platform to explore strategic partnerships that drive revenue growth and expansion.

Why Partner with Us?

- Diverse Opportunities: Discover a wide range of partnership opportunities tailored to your business goals.

- Expert Guidance: Access resources and support to build strong, profitable relationships.

- Community: Join a network of like-minded individuals and businesses.

Don’t miss out on the chance to elevate your financial future. Visit income-partners.net today to explore potential partnerships and start building your path to financial success!

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net